- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Human-Centered AI Market Size, Share & Forecast | 21.9% CAGR

Global Human-Centered AI Market Size, Share, Analysis By Application (Virtual Assistants & Chatbots, Risk Assessment & Fraud Detection, Healthcare Diagnostics, Human Resources, Personalized Learning, Other AI Applications), By Industry Vertical (Healthcare, Retail & E-commerce, Manufacturing, Automotive, Education, Other Industry Verticals) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Ethical AI Trends, Competitive Strategies & Forecast 2025–2034

Report Overview

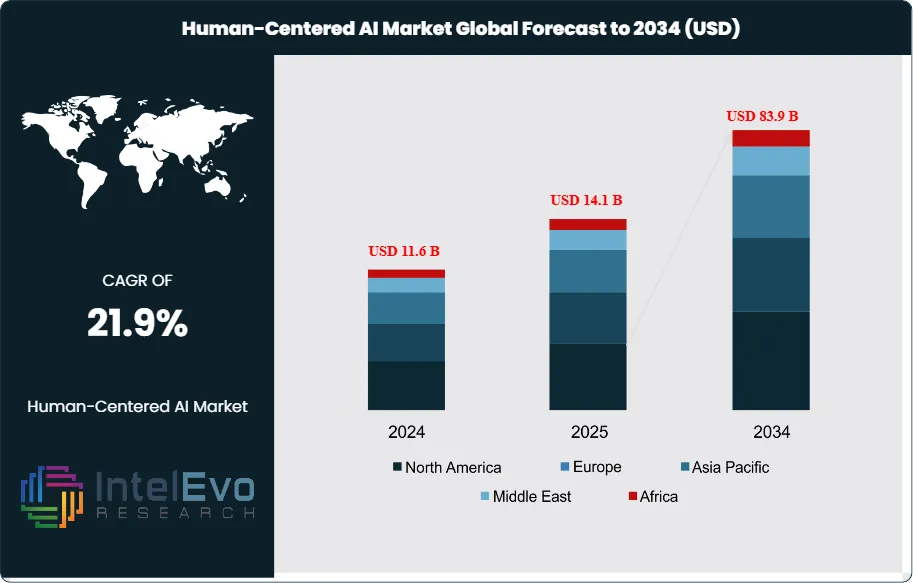

The Human-Centered AI Market was valued at USD 11.6 Billion in 2024 and is estimated to reach approximately USD 14.1 Billion in 2025. Driven by increasing adoption of ethical AI frameworks, explainable AI technologies, and human-machine collaboration across industries, the market is projected to grow from about USD 17.2 Billion in 2026 to nearly USD 83.9 Billion by 2034, registering a compound annual growth rate (CAGR) of around 21.9% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportHuman-Centered AI (HCAI) positions AI systems as capability multipliers that support human judgment, rather than substitutes for it. Vendors design solutions around fairness, transparency, security, and privacy so organizations can scale automation without eroding accountability. Demand concentrates in decision-intensive environments such as healthcare, finance, education, customer service, and enterprise operations, where leaders require explainable outcomes and auditable controls. This orientation shifts procurement criteria toward model governance, user experience, and measurable productivity gains, alongside accuracy and throughput.

Market expansion reflects a dual force. On the demand side, enterprises push for personalized interactions, higher service quality, and faster cycle times, while managing reputational exposure tied to biased or opaque models. On the supply side, advances in machine learning, natural language processing, and human–computer interaction improve contextual understanding and enable more reliable human-in-the-loop workflows. Explainable AI strengthens adoption by making model reasoning reviewable by compliance teams and frontline operators. Providers increasingly package governance layers, monitoring, and secure deployment options as standard, raising switching costs and favoring scaled platforms.

Regulatory and policy momentum amplifies investment and shapes product roadmaps. The U.K. has raised R&D spending to 2.7% of GDP to deepen its AI ecosystem, while U.S. federal spending on AI reached USD 3.3 billion in FY 2022 versus USD 1.3 billion in 2017. The projected U.S. Federal IT budget of USD 75.13 billion for 2025, with emphasis on AI, signals sustained public-sector demand for compliant, transparent systems. Key risk factors include data privacy breaches, model drift, security threats, and uneven governance maturity across industries, which can delay deployment.

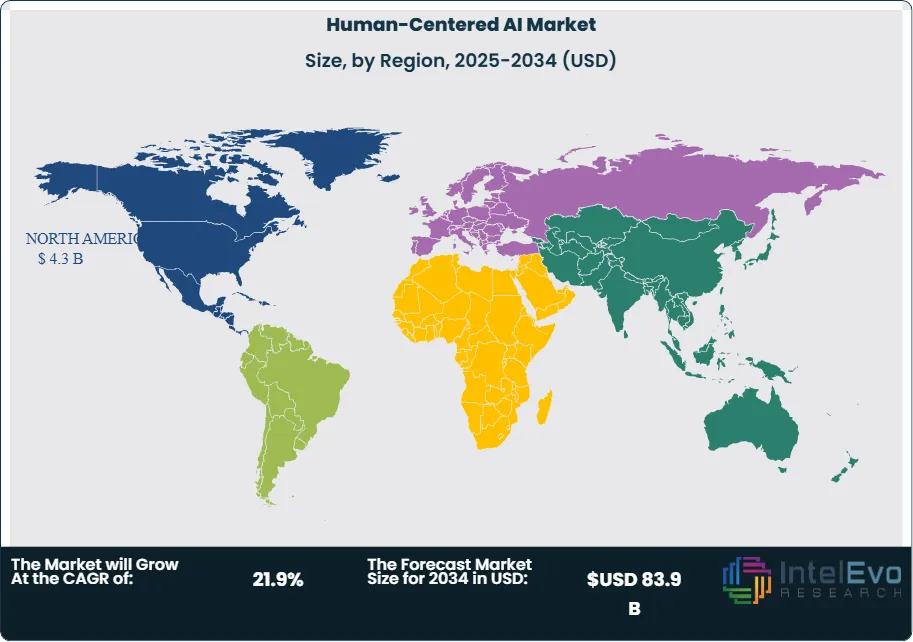

Regionally, North America remains the primary revenue center, anchored by a 38.0% share in 2023 and approximately USD 4.40 billion in 2024 revenue, supported by mature cloud infrastructure and early enterprise adoption. Europe benefits from governance-led buying behavior and rising funding for responsible AI, while Asia Pacific shows accelerating uptake in digital services and public-sector modernization. Investment hotspots are emerging in regulated verticals and in toolchains that operationalize oversight, bias testing, and traceability at scale.

, By Industry Vertical (Healthcare, Retail & E-commerce, Manufacturing, Automotive, Education, Other Industry Verticals) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Ethical AI Trends, Competitive Strategies & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 9.5 billion USD, 2023 to estimated: 12.3 billion USD, 2024 and reaches estimated: 90.1 billion USD, 2034 at 21.9% CAGR, 2024-2034.

- Segment Dominance : Virtual Assistants and Chatbots lead the By Application segment with 31.5%, 2023 and sustain an estimated: 32.8%, 2024 share as enterprises scale automation.

- Segment Dominance: Healthcare leads the By Industry Vertical segment with 24.1%, 2023 and rises to estimated: 25.0%, 2024 as clinical and administrative use cases mature.

- Driver: Buyers accelerate adoption to improve user-facing responsiveness and decision support, contributing to 21.9% CAGR, 2024-2034. Budget owners prioritize deployment pathways that protect trust, estimated: 1.0 year, 2024.

- Restraint: Governance gaps and model risk slow rollouts in regulated environments, increasing compliance effort by estimated: 18.0%, 2024. Data privacy exposure raises breach and remediation costs, estimated: 0.2 billion USD, 2024.

- Opportunity: Vendors monetize responsible AI toolchains and sector solutions, supporting an estimated: 9.0 billion USD, 2024 services and platform add-on pool. Healthcare and contact-center upgrades expand addressable spend, estimated: 2.0 billion USD, 2024.

- Trend: Providers embed explainability and human-in-the-loop controls into products, lifting enterprise procurement conversion by estimated: 6.0%, 2024. Solution roadmaps converge on scalable governance, estimated: 3.0 releases, 2024.

- Regional Analysis: North America leads with 38.0%, 2023 share and 3.61 billion USD, 2023 revenue, rising to estimated: 4.3 billion USD, 2024 as platform adoption broadens. Other regions grow faster from a lower base, estimated: 22.5% CAGR, 2024-2034.

By Application

Human-centered AI applications continue to expand across enterprise and consumer-facing use cases as organizations prioritize systems that support human decision-making. Virtual assistants and chatbots remain the largest application category, accounting for approximately 31.5 percent of global market revenue in 2023. By 2025, adoption has deepened across customer service, banking, travel, and public services, driven by demand for continuous availability and consistent interaction quality. Enterprises increasingly deploy these tools to reduce response times, manage high inquiry volumes, and support human agents rather than replace them.

Risk assessment and fraud detection represent the second-largest application area, supported by rising digital transaction volumes and regulatory scrutiny. Financial institutions and digital platforms rely on human-centered AI to flag anomalies while allowing human oversight of final decisions. Healthcare diagnostics also show sustained growth, with AI-assisted imaging, clinical decision support, and triage tools improving speed and accuracy while keeping clinicians in control. Adoption rates in diagnostic support tools exceed 40 percent across large hospital systems in developed markets as of 2025.

Human resources and personalized learning applications are gaining traction as enterprises seek better talent screening, workforce planning, and customized training delivery. AI-driven HR platforms now support candidate shortlisting, performance analysis, and employee engagement monitoring. Personalized learning tools apply behavioral data to adjust content pacing and format, supporting education providers and corporate training programs. Emerging applications across legal, public administration, and mental health services further broaden the addressable market.

By Industry Vertical

Healthcare remains the leading industry vertical, representing over 24.1 percent of market share in 2023 and maintaining leadership into 2025. Hospitals and life sciences organizations deploy human-centered AI to support diagnostics, care coordination, and administrative efficiency while complying with patient safety and data privacy standards. Clinical adoption accelerates where explainability and auditability are built into AI systems.

Retail and e-commerce follow closely, with AI supporting recommendation engines, demand forecasting, and customer engagement. Manufacturing adopts human-centered AI for predictive maintenance, quality inspection, and production planning, allowing engineers to validate outputs before execution. The automotive sector applies AI across advanced driver-assistance systems and in-vehicle interfaces, emphasizing safety and human control. Education institutions integrate AI for student assessment and operational management, particularly in large-scale digital learning environments.

By Region

North America remains the largest regional market, accounting for roughly 38.0 percent of global revenue and approximately USD 3.6 billion in 2023. Strong cloud infrastructure, early enterprise adoption, and sustained public and private investment support continued growth through 2025. The United States leads deployments across healthcare, finance, and government services.

Europe maintains steady expansion, supported by regulatory frameworks emphasizing transparency and accountability. These conditions favor human-centered AI solutions aligned with data protection and ethical standards. Asia Pacific shows the fastest growth rate, driven by large-scale digitization initiatives in China, Japan, South Korea, and India across manufacturing, healthcare, and education. Latin America and the Middle East and Africa remain smaller but expanding markets, supported by digital transformation programs and rising enterprise awareness of responsible AI deployment.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Application

- Virtual Assistants and Chatbots

- Risk Assessment and Fraud Detection

- Healthcare Diagnostics

- Human Resources

- Personalized Learning

- Other Applications

By Industry Vertical

- Healthcare

- Retail and E-commerce

- Manufacturing

- Automotive

- Education

- Other Industry Verticals

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.1 B |

| Forecast Revenue (2034) | USD 83.9 B |

| CAGR (2025-2034) | 21.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Application (Virtual Assistants and Chatbots, Risk Assessment and Fraud Detection, Healthcare Diagnostics, Human Resources, Personalized Learning, Other Applications), By Industry Vertical (Healthcare, Retail and E-commerce, Manufacturing, Automotive, Education, Other Industry Verticals) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Accenture plc, Vianai Systems, Inc., Microsoft Corporation, Tata Consultancy Services Limited, Salesforce, Inc., Google LLC, IBM Corporation, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Industry Vertical (Healthcare, Retail & E-commerce, Manufacturing, Automotive, Education, Other Industry Verticals) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Ethical AI Trends, Competitive Strategies & Forecast 2025–2034")

, By Industry Vertical (Healthcare, Retail & E-commerce, Manufacturing, Automotive, Education, Other Industry Verticals) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Ethical AI Trends, Competitive Strategies & Forecast 2025–2034")

, By Industry Vertical (Healthcare, Retail & E-commerce, Manufacturing, Automotive, Education, Other Industry Verticals) Industry Region & Key Players – Market Segment Overview, Regulatory Landscape, Ethical AI Trends, Competitive Strategies & Forecast 2025–2034")

Frequently Asked Questions

How big is the Human-Centered AI Market?

The Global Human-Centered AI Market was valued at USD 11.6 Billion in 2024 and is projected to reach USD 83.9 Billion by 2034, expanding at a CAGR of 21.9% from 2026–2034. Explore key trends in ethical AI, explainable AI, human–machine collaboration, market drivers, competitive landscape, and future opportunities.

Who are the major players in the Human-Centered AI Market?

Accenture plc, Vianai Systems, Inc., Microsoft Corporation, Tata Consultancy Services Limited, Salesforce, Inc., Google LLC, IBM Corporation, Other Key Players

Which segments covered the Human-Centered AI Market?

By Application (Virtual Assistants and Chatbots, Risk Assessment and Fraud Detection, Healthcare Diagnostics, Human Resources, Personalized Learning, Other Applications), By Industry Vertical (Healthcare, Retail and E-commerce, Manufacturing, Automotive, Education, Other Industry Verticals)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date