- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Hybrid Workplace Management Market Size, Share | CAGR 15.6%

Global Hybrid Workplace Management Market Size, Share, Analysis By Component (Software & Platforms, Desk & Room Booking, Visitor Management, Workforce Analytics, Professional & Managed Services), By Function (Workspace Scheduling, Employee Collaboration, Facility & Real Estate, Health & Compliance), By Organization Size (Large Enterprises, SMEs), By End-User Industry (IT & Telecom, BFSI, Healthcare, Education, Retail) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

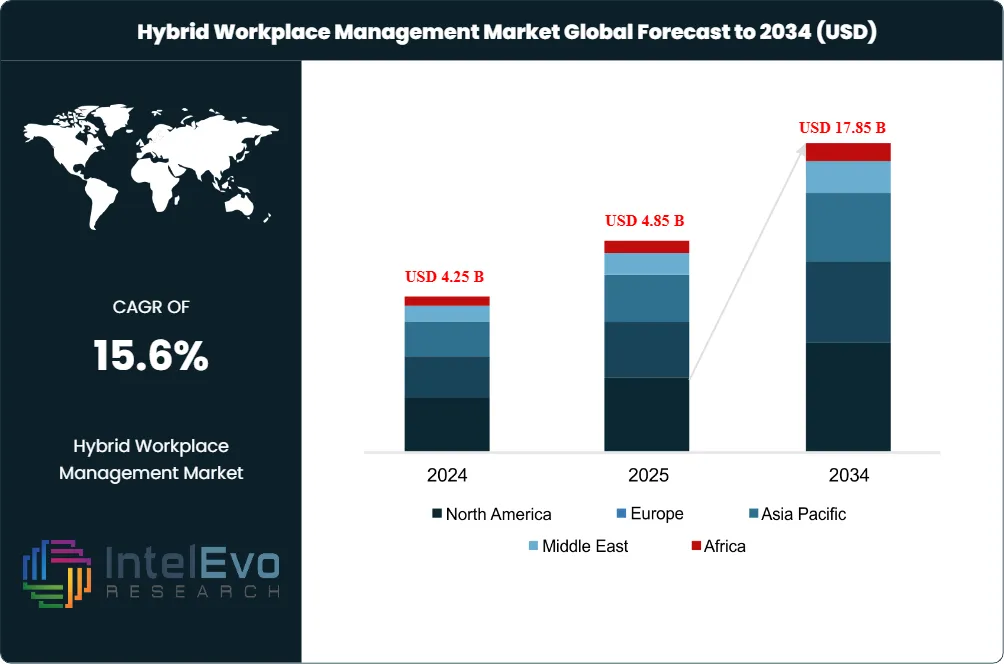

| USD 4.85 Billion | USD 17.85 Billion | 15.6% | North America, 38.4% |

The Hybrid Workplace Management Market was valued at USD 4.25 Billion in 2024 and USD 4.85 Billion in 2025. The market is projected to reach USD 17.85 Billion by 2034, expanding at a CAGR of 15.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.00 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportThe hybrid workplace management market spans desk booking and hot desking platforms, meeting room scheduling and conference room management, visitor management and access control integration, workplace analytics and space utilization dashboards, integrated workplace management systems (IWMS), facility maintenance and asset management modules, occupancy sensors and IoT integration, and AI-powered workplace operations platforms targeting hybrid teams. According to the Eptura 2025 Workplace Index, over 50% of organizations are currently using an average of 17 standalone worktech solutions, while 34% of companies plan to increase in-office days in 2025. Pilot success benchmarks include adoption rates above 75%, utilization lift of 20%, and no-show rates below 10%.

Regulatory anchors span employee data privacy and workplace surveillance restrictions. GDPR applies across EU member states under the European Data Protection Board, with national supervisory authorities including Germany's BfDI, France's CNIL, and Italy's Garante issuing workplace-specific guidance. The California Consumer Privacy Act (CCPA) and Colorado Privacy Act apply in U.S. jurisdictions, with the Americans with Disabilities Act (ADA) requiring accessible workspace booking interfaces. SOC 2 Type II and ISO 27001 certifications anchor enterprise procurement requirements; FedRAMP Authorization gates U.S. federal government deployment, with Eptura achieving FedRAMP Authorization for its Integrated Workplace Management System in May 2025. EU AI Act high-risk obligations enforceable August 2, 2026 affect AI-driven workplace analytics and occupancy prediction features.

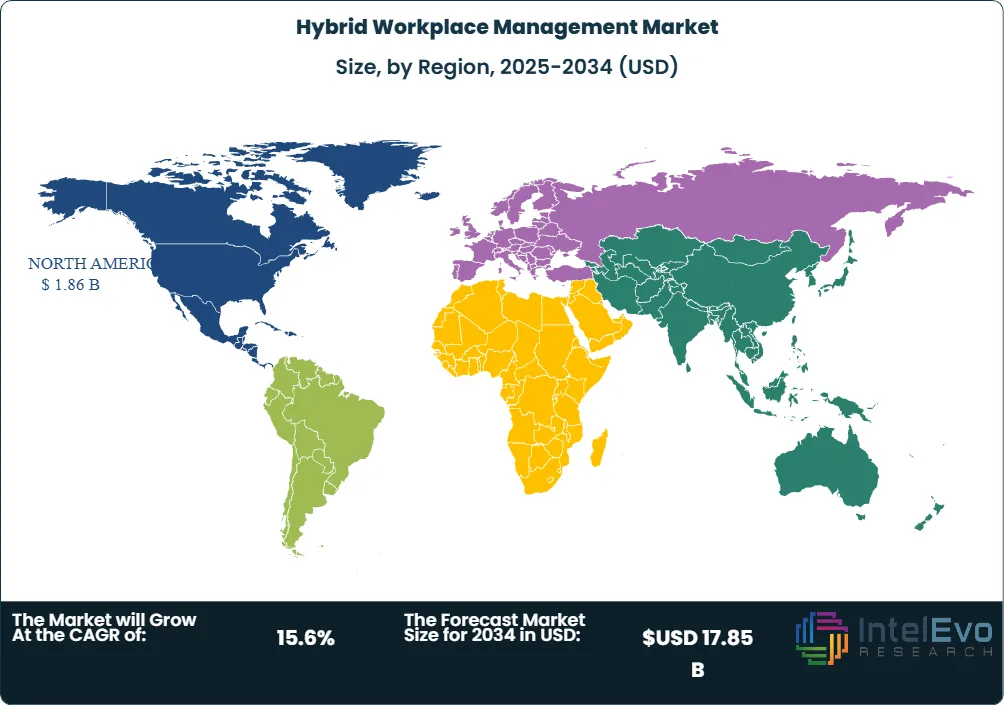

Industry consolidation accelerated through 2022-2025. Thoma Bravo merged Condeco, iOffice, and SpaceIQ in October 2022 to create Eptura, which now serves 16.3 Million users across 115+ countries and 16,000+ enterprise customers. JLL Technologies operates Archibus by JLL with over 200 enterprise clients and 250+ implementation specialists; the firm launched JLL GPT, a real-estate-specific large language model, for workspace planning. CBRE deployed AI building management technology across 1 Billion square feet of managed space. Cushman and Wakefield expanded its January 2024 Microsoft AI partnership through 2025, deploying Microsoft Azure OpenAI Service and Copilot for Microsoft 365. Independent leaders include Robin Powered (Boston, repositioning as AI-powered workplace operations), Envoy (San Francisco, founded 2013), Skedda, OfficeSpace Software, FM:Systems, Tactic, and Kadence. Regionally, North America held 38.4% revenue share in 2025, equating to approximately USD 1.86 Billion.

Market Definition and Scope

The hybrid workplace management market is defined as the segment of HR technology, facilities management software, and workplace SaaS covering platforms that enable organizations to manage flexible work environments combining in-office, remote, and distributed teams. The market encompasses desk booking and hot desking software, meeting room and conference room scheduling, visitor management and front-desk automation, workplace analytics and space utilization monitoring, integrated workplace management systems (IWMS), facility and maintenance management modules, asset and resource management, and AI-driven workplace optimization platforms.

This analysis covers vendor revenue from license, subscription, per-user, per-desk, and per-resource pricing models. Pricing ranges from USD 99 per location per month entry-tier (Envoy) to USD 2.80 per desk and USD 8 per room (Archie) to enterprise quote-based pricing for Robin, Eptura, OfficeSpace, and FM:Systems. Major participants include Eptura (Archibus, Condeco, iOffice + SpaceIQ), Robin Powered, Envoy, JLL Technologies, FM:Systems, OfficeSpace Software, Skedda, Microsoft (Places, Teams Rooms), Google (Workspace), Cisco (Webex), Maptician, Tactic, Kadence, Yarooms, Smartway2, Teem, Joan, Archie, deskbird, Officely, and DeskFlex. Excluded from this scope are pure-play unified communications platforms without spatial management features, broader human-capital management suites without dedicated hybrid workspace modules, and physical access control hardware. The parent global digital workplace market reached USD 67.57 Billion in 2025; hybrid workplace management software represented approximately 7.2% of broader digital workplace value.

, By Function (Workspace Scheduling, Employee Collaboration, Facility & Real Estate, Health & Compliance), By Organization Size (Large Enterprises, SMEs), By End-User Industry (IT & Telecom, BFSI, Healthcare, Education, Retail) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035")

Key Takeaways

- Market Growth: The hybrid workplace management market expanded from USD 4.85 Billion in 2025 toward a projected USD 17.85 Billion by 2034, registering a CAGR of 15.6% during the forecast period.

- Segment Dominance by Deployment: Cloud-based deployment captured approximately 81.4% revenue share in 2025, anchored by SaaS subscription economics, real-time updates, and seamless integration with Microsoft 365, Google Workspace, and Outlook calendars; on-premise represented 14.2% share preferred by enterprises with sensitive workplace data residency requirements.

- Segment Dominance by Function: Space and desk management captured approximately 38.6% revenue share in 2025, anchored by hot desking, neighborhood-based seating, interactive floor plans, and team-coordinated booking; facility and maintenance management followed at 24.4%.

- Driver: The Eptura 2025 Workplace Index reported 34% of companies plan to increase in-office days in 2025, with over 50% of organizations currently using an average of 17 standalone worktech solutions; consolidation onto unified hybrid workplace management platforms drives 15-25% recurring license cost reduction.

- Restraint: Initial implementation costs and complexity of integrating IWMS with existing infrastructure deter SMB adoption; enterprise deployments at FM:Systems and OfficeSpace require multi-month implementation cycles, while data privacy concerns under GDPR and CCPA add governance overhead for occupancy sensor and visitor tracking data.

- Opportunity: 75% of business leaders expect their workplace to transform by 2026 per Zoom research; AI-driven workplace optimization, IoT-enabled smart office solutions, and predictive occupancy analytics expand vendor wallet share, with mature deployments delivering 20% utilization lift and below 10% no-show rates.

- Trend: AI-powered workplace operations platforms expanded across leading vendors through 2026, with Robin Powered repositioning as an AI-powered platform for 500+ employee hybrid organizations, JLL Technologies launching JLL GPT for CRE workspace planning, and CBRE deploying AI building management across 1 Billion square feet.

- Regional: North America held the largest regional share at 38.4%, equating to approximately USD 1.86 Billion in 2025, anchored by U.S. enterprise hybrid work adoption, mature IWMS deployments, and concentrated venture activity in Boston, San Francisco, Atlanta, and New York; the U.S. workspace management software market alone reached approximately USD 1.00 Billion in 2025.

Key Insights Summary

- Eptura secured FedRAMP Authorization for its Integrated Workplace Management System on May 2, 2025, qualifying the company for U.S. federal procurement and placing it on the GSA-approved cloud service vendor list; the milestone supports Eptura's expansion across federal agency hybrid workplace mandates following return-to-office executive orders.

- The Eptura 2025 Workplace Index issued on March 18, 2025 reported that 34% of businesses intend to lift in-office attendance during 2025, while more than half of organizations operate an average of 17 separate worktech tools; the dataset established consolidation onto unified platforms as the dominant procurement direction through the forecast period.

- Eptura's customer base now spans 16.3 Million users across more than 115 countries and over 16,000 enterprise accounts including Fortune 500 organizations, a footprint built off the October 2022 Thoma Bravo combination of Condeco, iOffice, and SpaceIQ benchmarked against a USD 25 Billion total addressable market.

- CBRE has rolled out AI building management technology across 1 Billion square feet of managed space, capturing operations and utilization signals across 20,000 client sites, and introduced a generative AI platform that lets clients converse naturally with portfolio data; JLL Technologies likewise debuted JLL GPT, a CRE-specific large language model trained on real estate data.

- CBRE's 2026 Global Workplace and Occupancy Insights synthesized five years of office benchmarking across 303 Million square feet (28 Million square meters) with an average portfolio size of 5 Million square feet, establishing the benchmark dataset for hybrid workplace optimization; 43% of corporate leaders globally expect headcount growth and 33% expect footprint expansion over the next several years.

- Robin Powered focuses on organizations of 500+ employees achieving at least 33% office utilization, mirroring Zoom research showing 75% of business leaders expect workplace transformation by 2026; the company repositioned as an AI-powered workplace operations platform combining desk and room reservations, visitor management, employee engagement features, and AI-driven scheduling.

Competitive Landscape Overview

The hybrid workplace management market is moderately consolidated at the enterprise IWMS tier and highly fragmented at the SMB and mid-market tier. Enterprise platform leaders include Eptura (post-Thoma Bravo merger of Condeco, iOffice, and SpaceIQ; serving 16.3 Million users and 16,000+ companies), Robin Powered (Boston, AI-powered workplace operations for 500+ employee organizations), Envoy (San Francisco, founded 2013, mature visitor management plus workplace booking), JLL Technologies (Archibus by JLL serving 200+ enterprise clients with 250+ implementation specialists), FM:Systems (full IWMS with multi-month implementation), and OfficeSpace Software (enterprise space utilization analytics). Mid-market vendors include Skedda (Boston, founded 2013, G2 average 4.8 rating with largest review volume), Tactic, Kadence, Maptician, deskbird, Joan, and Archie. SMB and team-tier vendors include Officely (Slack-native), DeskFlex, Yarooms, Smartway2, and Dibsido. Adjacent platform competition includes Microsoft (Places, Teams Rooms), Google (Workspace, Calendar), Cisco (Webex Meeting Zones), and Cushman and Wakefield's Microsoft AI deployment. The market structure favors integration depth: enterprise plans from Skedda, Envoy, and Robin support SCIM, SSO via SAML/OIDC, and role-based admin; HID and Kisi access control connectors are required for security-sensitive deployments. Pricing models split between per-user (Envoy), per-resource desk and room (Archie at USD 2.80 per desk and USD 8 per room), per-space tier (Skedda from USD 99 per month), and quote-based enterprise (Robin, Eptura, OfficeSpace, FM:Systems).

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

| Eptura | Atlanta, USA | Leader | Archibus IWMS, Condeco, iOffice + SpaceIQ unified worktech suite | North America, EMEA, APAC | Achieved FedRAMP Authorization for IWMS in May 2025 |

| Robin Powered | Boston, USA | Leader | AI-powered workplace operations platform for hybrid teams | North America, EMEA | Repositioned as AI-powered workplace operations platform through 2025-2026 |

| Envoy | San Francisco, USA | Leader | Envoy Workplace + Visitors + Rooms + Desks suite | North America, EMEA, APAC | Module-based pricing scaling to enterprise compliance and access control |

| JLL Technologies | Chicago, USA | Leader | Archibus by JLL implementation services + JLL GPT LLM platform | North America, EMEA, APAC | JLL GPT generative AI platform launched for CRE workspace planning |

| FM:Systems (JM Solutions) | Raleigh, USA | Challenger | FM:Systems IWMS for facility, lease, and space management | North America, EMEA | Continued enterprise IWMS deployments with multi-month implementation cycles |

| OfficeSpace Software | San Francisco, USA | Challenger | OfficeSpace enterprise space utilization analytics platform | North America | Real estate portfolio reporting expansion through 2025-2026 |

| Skedda | Boston, USA | Niche Player | Cloud-based desk and meeting room booking platform | Global SMB and mid-market | G2 average 4.8 rating across largest review volume in segment |

| Microsoft Corporation | Redmond, USA | Challenger | Microsoft Places, Teams Rooms, Outlook integration | Global | Cushman & Wakefield AI partnership announced January 2024 expanded through 2025 |

| Tactic | Lehi, USA | Niche Player | Tactic hybrid workplace platform for SMB and mid-market | North America | Visitor management and floor plan views for small and midsize companies |

| Kadence | London, United Kingdom | Niche Player | Kadence hybrid scheduling and workspace coordination | EMEA, North America | HID and Kisi access control connector expansion through 2025 |

By Component

The hybrid workplace management market by component is led by software solutions, which captured approximately 64.8% revenue share in 2025 driven by core booking, scheduling, and analytics platform license revenue. Software solution sub-categories include space management tools (Eptura, Robin, OfficeSpace, Maptician), desk and room booking engines (Skedda, Envoy, Tactic, deskbird), visitor management modules (Envoy core product, Eptura, Robin, Proxyclick), and workplace analytics dashboards. Implementation and integration services captured 18.4% share, anchored by JLL Technologies (250+ Archibus specialists), FM:Systems consulting, and partner ecosystems including BGIS, CBRE, Cushman and Wakefield, JLL, and Newmark across enterprise IWMS deployments.

Support and maintenance subscriptions captured 12.6% share with annual renewal economics tied to license seat counts, while professional services and training contributed the residual 4.2% share. Comparison: software solution revenue grew at 17.2% CAGR through 2034 versus 11.8% CAGR for implementation services, reflecting the structural shift toward self-service SaaS deployment. Procurement leads should evaluate hybrid workplace management vendors against three criteria: SOC 2 Type II and ISO 27001 certification, FedRAMP Authorization for federal eligibility (Eptura achieved May 2025), and integration depth with Microsoft 365, Google Workspace, Outlook, Slack, and identity providers via SAML and SCIM.

By Function

The hybrid workplace management market by function is led by space and desk management at approximately 38.6% revenue share in 2025, anchored by hot desking, neighborhood-based seating, interactive floor plans, capacity enforcement, and team coordination. Robin, Skedda, Eptura, Envoy, and Maptician anchor enterprise space management with mobile-first booking interfaces. Facility and maintenance management captured 24.4% share, anchored by Eptura iOffice, FM:Systems, and Archibus by JLL across multi-site enterprise portfolios. Asset and resource management held 16.8% share, including parking space reservation, equipment booking, and laboratory resource scheduling.

Workplace analytics and occupancy intelligence captured 14.2% share, growing at the fastest 22.6% CAGR through 2034 driven by AI-powered space optimization, IoT sensor integration (occupancy sensors, environmental conditions, resource availability), and CBRE's 1 Billion square feet AI building management deployment. Visitor management and front desk automation contributed the residual 6.0% share, anchored by Envoy market leadership. ROI calculation for hybrid workplace management deployment must account for utilization lift (20% target), no-show rate reduction (below 10%), real estate portfolio cost reduction (typically 15% to 25% of underutilized space), and sustainability outcomes (51% of Eptura Flex/25 New York attendees identified sustainability as a top workplace outcome).

By Organization Size

The hybrid workplace management market by organization size is led by large enterprises (1,000+ employees) at approximately 58.4% revenue share in 2025, anchored by Eptura Fortune 500 deployments, Robin Powered's 500+ employee target customer profile (with at least 33% office utilization), and JLL Technologies Archibus by JLL implementations across 200+ enterprise clients. Mid-market organizations (100 to 999 employees) captured 28.6% share, anchored by Skedda, Envoy mid-tier plans, OfficeSpace, Tactic, and Kadence. SMB and startup organizations (fewer than 100 employees) captured 13.0% share, served by Officely (Slack-native), Joan, Archie (USD 159 per month minimum), Skedda entry tier, and DeskFlex SMB plans.

Volume of in-office attendance drives organization-size segmentation differently from typical SaaS markets: a 5,000-employee organization with 30% hybrid utilization presents a similar booked-resource volume to a 1,500-employee organization with 100% in-office attendance. Hybrid workplace management implementation timeline ranges from approximately three weeks (Maptician deployments per published case data) to multi-month enterprise IWMS programs, with FM:Systems and Archibus implementations typically spanning 6 to 18 months.

By End-User Industry

The hybrid workplace management market by end-user industry is led by IT and telecommunications at approximately 24.0% share in 2025, where engineering and software talent retention drives investment in flexible workspace solutions. BFSI (banking, financial services, insurance) captured 18.6% share, anchored by Goldman Sachs, JPMorgan Chase, Bank of America, and Synovus enterprise deployments; financial services firms have specific requirements that include visitor check-in workflows with compliance tracking, granular desk booking policies, and security certifications. Healthcare captured 16.4% share, growing at the fastest 19.8% CAGR through 2034 driven by digital transformation, multi-location coordination, and post-pandemic telehealth integration.

Education and government contributed 12.8% share, anchored by University of Nebraska Archibus deployment and FedRAMP-eligible Eptura federal procurement post-May 2025. Manufacturing and industrial captured 9.4% share. Professional services and law firms held 7.6% share with specific requirements for visitor check-in compliance, multi-floor occupancy tracking, and granular hot desking policies. Retail and e-commerce contributed 6.4% share, anchored by Apple, Amazon, and Walmart corporate office deployments. Other industries including hospitality, transportation, and nonprofit captured the residual 4.8% share.

Regional Analysis

The hybrid workplace management market by region is led by North America at 38.4% revenue share in 2025, equating to approximately USD 1.86 Billion. The United States dominates with USD 1.00 Billion U.S. workspace management software market value in 2025 and projected USD 3.97 Billion by 2035 at 14.78% U.S. CAGR. Concentrated venture activity centers in Boston (Robin Powered, Skedda), San Francisco (Envoy, OfficeSpace Software), Atlanta (Eptura headquarters), Chicago (JLL Technologies), Raleigh (FM:Systems), and Lehi (Tactic). Federal procurement opens following Eptura's May 2025 FedRAMP Authorization. Canada anchors regional supply through PIPEDA-compliant deployments and partnerships with BGIS facilities management. Major U.S. enterprise customers include Goldman Sachs, JPMorgan Chase, Synovus, Pratt Institute, and the University of Nebraska.

Europe held 28.6% share in 2025, equivalent to approximately USD 1.39 Billion. The EU AI Act high-risk obligations enforceable August 2, 2026 affect AI-driven workplace analytics and occupancy prediction features. GDPR enforcement applies across all member states with national supervisory authorities including Germany's BfDI, France's CNIL, the UK Information Commissioner's Office (ICO), and Italy's Garante issuing workplace-specific guidance. The United Kingdom hosts Kadence (London) and major enterprise demand from HSBC, Lloyd's of London, and the City of London corporate occupiers. Germany contributes through SAP integration and works council co-determination requirements limiting AI workplace analytics deployment. France hosts MOFFI (Lille, founded 2016). The Nordics contribute through HID Global Stockholm operations and Telia hybrid workplace deployments.

Asia Pacific captured 22.4% share in 2025, valued at approximately USD 1.09 Billion, projected at the fastest regional CAGR of 18.6% through 2034. Australia anchors regional development through Sapia.ai integrations and major enterprise demand from Commonwealth Bank, Westpac, and Atlassian. Japan advances through Recruit Holdings, NTT Limited (Tokyo), and Mitsubishi Estate corporate hybrid programs. India anchors expansion through Infosys, Tata Consultancy Services, and Wipro deployments processing 250,000+ corporate desks under hybrid policies. China contributes through domestic platforms aligned with state-supported smart workplace initiatives, with Asia Pacific smart workplace value reaching USD 15.47 Billion in 2025 (China captured 25.8%). South Korea contributes through Samsung and LG enterprise integration.

Middle East and Africa held 6.4% share in 2025, approximately USD 310 Million. The United Arab Emirates serves as regional hub for hybrid workplace deployments under Vision 2031 and Saudi Arabia's Vision 2030 NEOM initiatives. Latin America contributed 4.2% share, valued at approximately USD 204 Million in 2025. Brazil leads through banking and finance hybrid deployments at Itau Unibanco and Banco do Brasil.

Country Analysis

United States

The hybrid workplace management market in the United States was valued at approximately USD 1.62 Billion in 2025 and is projected to grow at a CAGR of 16.4% during 2025-2034, anchored by mature enterprise hybrid work adoption and the highest concentration of leading vendors globally. The U.S. workspace management software sub-segment alone reached USD 1.00 Billion in 2025 and is projected at USD 3.97 Billion by 2035 (14.78% CAGR). Eptura's May 2, 2025 FedRAMP Authorization for IWMS opened federal agency procurement; Eptura subsequently expanded its Fortune 500 reach amid AI innovation surge per its January 6, 2026 announcement and appointed a new Chief Revenue Officer on January 21, 2026. CBRE deployed AI building management technology across 1 Billion square feet of U.S. and global managed space. JLL Technologies launched JLL GPT for CRE workspace planning. Major U.S. enterprise customers include Goldman Sachs, JPMorgan Chase, Bank of America, Apple, Microsoft, Amazon, Synovus, and Pratt Institute. Federal Trade Commission and EEOC supplementary workplace AI guidance shapes vendor compliance posture.

United Kingdom

The United Kingdom's hybrid workplace management market reached approximately USD 380 Million in 2025 with a country CAGR of 14.8% during 2025-2034. Kadence (London) anchors domestic activity with hybrid scheduling and HID and Kisi access control connector integration. Major enterprise demand concentrates in financial services (HSBC, Barclays, Lloyd's of London), professional services (Big Four offices outside this analysis scope), and government departments adopting hybrid mandates. UK Information Commissioner's Office (ICO) administers GDPR enforcement applicable to occupancy and visitor data. The Department for Science, Innovation and Technology coordinates AI workplace governance under the AI Safety Institute framework published in 2025. Aerospace and life sciences clusters in Cambridge, Oxford, and Manchester contribute innovation demand.

Germany

Germany's hybrid workplace management market reached approximately USD 290 Million in 2025 with a country CAGR of 12.4% during 2025-2034. Domestic activity concentrates around SAP HCM integration in Walldorf, Allianz and Munich Re corporate hybrid programs, and BMW and Siemens manufacturing site deployments. The German Works Council (Betriebsrat) co-determination framework requires extensive consultation on workplace technology deployment, with Federal Labor Court decisions limiting AI-driven workplace analytics absent works council agreement. The Bundesbeauftragte fur den Datenschutz und die Informationsfreiheit (BfDI) administers GDPR enforcement. EU AI Act high-risk obligations applicable from August 2, 2026 require conformity assessments for AI-powered workplace analytics platforms. Aerospace innovation clusters concentrate in Munich, Hamburg, and Berlin.

Australia

Australia's hybrid workplace management market reached approximately USD 240 Million in 2025 with a country CAGR of 17.6% during 2025-2034, anchored by extensive enterprise hybrid adoption and concentrated mining and finance sector demand. Major enterprise customers include Commonwealth Bank, Westpac, ANZ, NAB, BHP, Rio Tinto, Telstra, and Atlassian. Domestic vendors include Sapia.ai (Melbourne) and Yarooms regional partnerships. The Office of the Australian Information Commissioner (OAIC) administers Privacy Act 1988 enforcement applicable to workplace data, with the Privacy and Other Legislation Amendment Bill 2024 introducing additional workplace privacy obligations. Hybrid work corridor concentration in Sydney CBD, Melbourne Docklands, and Brisbane corporate towers drives demand. The Fair Work Act flexible work arrangements provisions extended in 2024 reinforce hybrid adoption mandates.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Component

- Software

- Services

- Others

By Function

- Workforce Scheduling and Shift Management

- Employee Collaboration and Communication

- Facility and Asset Management

- Meeting Room and Space Management

- Others

By Organization Size

- Large Enterprises

- Small and Medium-Sized Enterprises (SMEs)

- Others

By End-User Industry

- Banking, Financial Services, and Insurance (BFSI)

- Information Technology and Telecommunications

- Healthcare and Life Sciences

- Retail and E-Commerce

- Education

- Energy and Utilities

- Transportation and Logistics

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.85 B |

| Forecast Revenue (2034) | USD 17.85 B |

| CAGR (2025-2034) | 15.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software, Services, Others), By Function, (Workforce Scheduling and Shift Management, Employee Collaboration and Communication, Facility and Asset Management, Meeting Room and Space Management, Others), By Organization Size, (Large Enterprises, Small and Medium-Sized Enterprises (SMEs), Others), By End-User Industry, (Banking, Financial Services, and Insurance (BFSI), Information Technology and Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Education, Energy and Utilities, Transportation and Logistics, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | EPTURA, ROBIN POWERED, ENVOY, JLL TECHNOLOGIES, FM:SYSTEMS, OFFICESPACE SOFTWARE, SKEDDA, MICROSOFT CORPORATION, TACTIC, KADENCE, MAPTICIAN, DESKBIRD, JOAN, ARCHIE, OFFICELY, DESKFLEX, YAROOMS, SMARTWAY2, TEEM, NTT LIMITED, SCHNEIDER ELECTRIC, CISCO SYSTEMS, GOOGLE WORKSPACE, ATOS SE, MOFFI, DIBSIDO, ACCRUENT, HQO, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Function (Workspace Scheduling, Employee Collaboration, Facility & Real Estate, Health & Compliance), By Organization Size (Large Enterprises, SMEs), By End-User Industry (IT & Telecom, BFSI, Healthcare, Education, Retail) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035")

, By Function (Workspace Scheduling, Employee Collaboration, Facility & Real Estate, Health & Compliance), By Organization Size (Large Enterprises, SMEs), By End-User Industry (IT & Telecom, BFSI, Healthcare, Education, Retail) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035")

, By Function (Workspace Scheduling, Employee Collaboration, Facility & Real Estate, Health & Compliance), By Organization Size (Large Enterprises, SMEs), By End-User Industry (IT & Telecom, BFSI, Healthcare, Education, Retail) Region & Key Players-Dynamics, Strategies & Forecast 2026-2035")

Frequently Asked Questions

How big is the Hybrid Workplace Management Market?

The Global Hybrid Workplace Management Market was valued at USD 4.25 Billion in 2024 and USD 4.85 Billion in 2025, and is projected to reach USD 17.85 Billion by 2034, growing at a CAGR of 15.6% from 2026 to 2034. Market growth is driven by hybrid work, smart workplace solutions, AI-powered workplace management, and cloud-based collaboration platforms.

Who are the major players in the Hybrid Workplace Management Market?

EPTURA, ROBIN POWERED, ENVOY, JLL TECHNOLOGIES, FM:SYSTEMS, OFFICESPACE SOFTWARE, SKEDDA, MICROSOFT CORPORATION, TACTIC, KADENCE, MAPTICIAN, DESKBIRD, JOAN, ARCHIE, OFFICELY, DESKFLEX, YAROOMS, SMARTWAY2, TEEM, NTT LIMITED, SCHNEIDER ELECTRIC, CISCO SYSTEMS, GOOGLE WORKSPACE, ATOS SE, MOFFI, DIBSIDO, ACCRUENT, HQO, Others

Which segments covered the Hybrid Workplace Management Market?

By Component, (Software, Services, Others), By Function, (Workforce Scheduling and Shift Management, Employee Collaboration and Communication, Facility and Asset Management, Meeting Room and Space Management, Others), By Organization Size, (Large Enterprises, Small and Medium-Sized Enterprises (SMEs), Others), By End-User Industry, (Banking, Financial Services, and Insurance (BFSI), Information Technology and Telecommunications, Healthcare and Life Sciences, Retail and E-Commerce, Education, Energy and Utilities, Transportation and Logistics, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Hybrid Workplace Management Market

Published Date : 30 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date