- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Hydrazine Hydrate Market Size & Forecast 2024–2034 | 4.7% CAGR

Global Hydrazine Hydrate Market Size, Share, Industry Analysis By Concentration Level (100%, 60–85%, 40–55%, 24–35%), By Application (Water Treatment, Polymerization & Blowing Agents, Agrochemicals, Pharmaceuticals, Other Industrial Applications), By End-Use Industry (Chemical Processing, Agriculture, Aerospace & Defense, Power Generation), Industry Region & Key Players – Market Dynamics, Supply Chain Trends, Competitive Strategies & Forecast 2025–2034

Report Overview

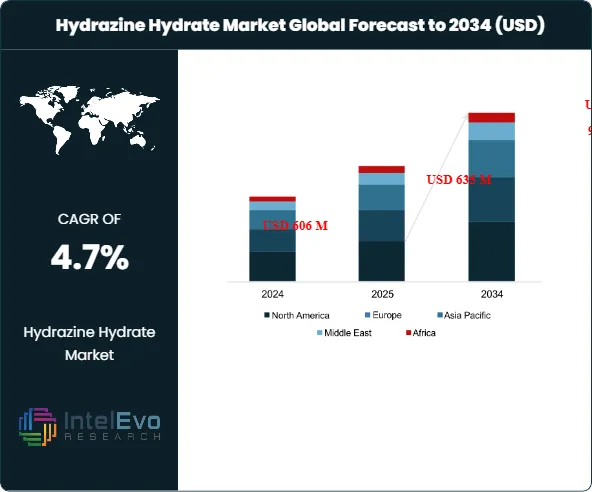

The Hydrazine Hydrate Market was valued at USD 606 Million in 2024 and is projected to reach approximately USD 966 Million by 2034. The market is estimated to grow to around USD 635 Million in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 4.7% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportHydrazine hydrate (N₂H₄·H₂O) remains a core intermediate across water treatment, pharmaceuticals, and agrochemicals due to its high reactivity and reducing behavior. Demand tracks industrial water reuse mandates, tighter boiler-water specifications, and steady growth in drug synthesis routes that require hydrazine derivatives. Water treatment applications account for an estimated 34–38% of global revenue in 2024, supported by rising municipal and industrial purification volumes. Pharmaceuticals contribute roughly 22–26%, while agrochemicals represent about 18–22%, with the balance linked to polymers, blowing agents, and specialty chemicals.

Supply stays concentrated among a limited group of producers with integrated chemical value chains. Asia-Pacific leads capacity and consumption and represents about 44–48% of 2024 revenue, driven by China and India’s expanding manufacturing base and upgrading wastewater infrastructure. North America holds an estimated 23–27% share, supported by refinery, power, and specialty chemical demand, while Europe contributes 18–22% amid tighter compliance requirements and disciplined procurement. Emerging investment hotspots include India’s industrial corridors, Southeast Asia’s electronics and water-reuse buildout, and Middle East desalination-linked chemical demand, where local storage and distribution assets improve service levels and reduce logistics risk.

Regulatory pressure shapes both cost and operating models. Hydrazine hydrate faces stringent handling, exposure, transport, and storage rules across major jurisdictions, which elevates compliance spending and favors suppliers with strong EHS systems. Risk concentrates around hazardous-material incidents, permitting delays, and feedstock and energy volatility that can compress margins during tight supply. Producers increasingly deploy automation, advanced process controls, and digital quality systems to stabilize output and reduce exposure. AI-enabled predictive maintenance and demand sensing improve plant uptime and inventory planning, while digital batch tracking supports audit readiness and lowers recall risk for pharmaceutical-grade material. These dynamics sustain a market that grows steadily, rewards scale and compliance capability, and prioritizes secure, high-purity supply.

, By Application (Water Treatment, Polymerization & Blowing Agents, Agrochemicals, Pharmaceuticals, Other Industrial Applications), By End-Use Industry (Chemical Processing, Agriculture, Aerospace & Defense, Power Generation), Industry Region & Key Players – Market Dynamics, Supply Chain Trends, Competitive Strategies & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands at a 4.9% CAGR, 2024-2034. It scales from estimated: 0.6 billion USD, 2024 to estimated: 1.0 billion USD, 2034.

- Segment Dominance: The 60-86% concentration band leads revenue with estimated: 45.0% share, 2024. It retains leadership through estimated: 47.0% share, 2034.

- Segment Dominance: Polymerization & blowing agents hold the largest application share at estimated: 32.0% share, 2024. Water treatment follows at estimated: 28.0% share, 2024.

- Driver: Water treatment upgrades and industrial oxygen-scavenging demand lift consumption with estimated: 5.0% volume growth, 2024. Pharma and agrochemical synthesis sustain demand with estimated: 0.2 billion USD, 2024.

- Restraint: Safety-driven regulation and handling controls raise compliance costs by estimated: 8.0% of opex, 2024. Feedstock volatility increases price swings by estimated: 12.0% YoY, 2024.

- Opportunity: R&D improves safer formulations and process controls, supporting estimated: 0.1 billion USD, 2034 in incremental value. New end-uses expand addressable demand by estimated: 6.0% CAGR, 2024-2034.

- Trend: Producers adopt cleaner synthesis and digital quality systems, driving estimated: 15.0% efficiency gains, 2024. Automation and AI-based monitoring cut downtime by estimated: 10.0% reduction, 2024.

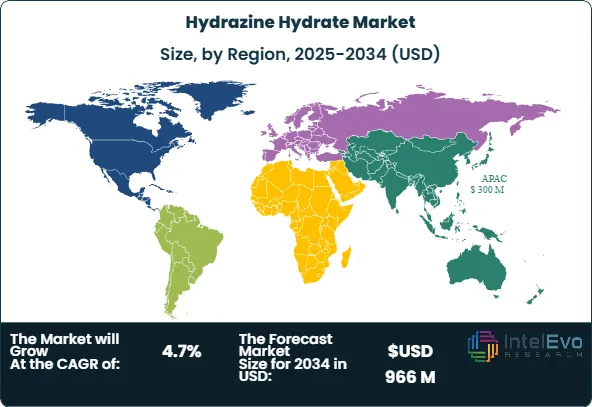

- Regional Analysis: Asia Pacific leads with 54.0% revenue share, 2024. Regional revenue reaches estimated: 0.3 billion USD, 2024.

By Type

Hydrazine hydrate demand in 2025 and beyond remains structured around concentration grades, with the 60–85% segment continuing to generate the highest revenue contribution. This grade accounted for an estimated 45–48% of global market value in 2024, supported by its balance between reactivity, handling safety, and cost efficiency. Producers favor this range for large-volume industrial use, which keeps pricing stable and ensures consistent offtake across chemical value chains.

The 60–85% grade is widely applied in polymer processing, veterinary and specialty pharmaceuticals, and intermediate chemical synthesis. Aerospace-related use also remains relevant, particularly for emergency power units in military aircraft fleets, where controlled concentration levels are mandatory. Demand for 100% concentration stays limited to niche propulsion and laboratory applications, while 40–55% and 24–35% grades serve water treatment and corrosion control, where lower concentration reduces handling risk and regulatory exposure.

By Application

Polymerization and blowing agents remain the largest application segment for hydrazine hydrate, representing approximately 30–33% of global demand in 2024. Growth is tied to steady expansion in plastics, elastomers, and insulation materials, where hydrazine-based derivatives act as initiators and low-temperature foaming agents. Compounds such as azodicarbonamide and azobis derivatives continue to support volume growth in Asia-based polymer manufacturing hubs.

Water treatment forms the second-largest application, accounting for nearly 27–29% of consumption. Power generation, refinery operations, and industrial boilers rely on hydrazine hydrate as an oxygen scavenger to limit corrosion. Pharmaceutical and agrochemical uses collectively contribute about 35% of market volume, driven by demand for active intermediates in crop protection chemicals and drug synthesis. These segments show moderate but steady growth, with higher purity requirements supporting margin stability.

By End-Use

Industrial end-use dominates hydrazine hydrate consumption, accounting for more than 55% of global demand in 2024. Polymer producers, chemical processors, power plants, and aerospace maintenance facilities represent the core customer base. Capital investment in industrial manufacturing capacity across Asia Pacific and parts of the Middle East continues to sustain long-term demand.

Commercial and institutional use, primarily linked to water treatment systems and utilities, represents close to 30% of end-use demand. Residential exposure remains limited and indirect, largely tied to municipal water infrastructure rather than direct consumption. Regulatory oversight and safety constraints restrict broader downstream exposure, keeping end-use concentrated among regulated industrial buyers.

By Region

Asia Pacific remains the leading regional market, accounting for approximately 54% of global revenue in 2024, equivalent to over USD 300 million. China and India drive regional demand through expanding polymer production, agrochemical manufacturing, and infrastructure-led water treatment investment. Industrial growth policies and capacity additions continue to support regional dominance through the late 2020s.

North America ranks second with an estimated 23–25% market share. Stable demand from pharmaceuticals, agriculture, and power generation underpins regional growth, supported by established producers and distributors. Europe follows closely, shaped by strict chemical handling regulations and steady industrial demand. Latin America and the Middle East & Africa remain smaller markets but show gradual expansion tied to industrialization and water treatment investment, particularly in Gulf countries and Brazil.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Concentration Level

- 100%

- 60-85%

- 40-55%

- 24-35%

By Application

- Water Treatment

- Polymerization & Blowing Agents

- Agrochemicals

- Pharmaceuticals

- Other Applications

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 635 M |

| Forecast Revenue (2034) | USD 966 M |

| CAGR (2025-2034) | 4.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Concentration Level (100%, 60-85%, 40-55%, 24-35%), By Application (Water Treatment, Polymerization & Blowing Agents, Agrochemicals, Pharmaceuticals, Other Applications) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Arkema Group, Japan Finechem Inc., Lonza Group Ltd, Arrow Fine Chemicals, LANXESS AG, Nippon Carbide Industries Co Inc., Alfa Aesar, Otsuka-MGC Chemical Company, LCG Science Group Holdings Limited, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Water Treatment, Polymerization & Blowing Agents, Agrochemicals, Pharmaceuticals, Other Industrial Applications), By End-Use Industry (Chemical Processing, Agriculture, Aerospace & Defense, Power Generation), Industry Region & Key Players – Market Dynamics, Supply Chain Trends, Competitive Strategies & Forecast 2025–2034")

, By Application (Water Treatment, Polymerization & Blowing Agents, Agrochemicals, Pharmaceuticals, Other Industrial Applications), By End-Use Industry (Chemical Processing, Agriculture, Aerospace & Defense, Power Generation), Industry Region & Key Players – Market Dynamics, Supply Chain Trends, Competitive Strategies & Forecast 2025–2034")

, By Application (Water Treatment, Polymerization & Blowing Agents, Agrochemicals, Pharmaceuticals, Other Industrial Applications), By End-Use Industry (Chemical Processing, Agriculture, Aerospace & Defense, Power Generation), Industry Region & Key Players – Market Dynamics, Supply Chain Trends, Competitive Strategies & Forecast 2025–2034")

Frequently Asked Questions

How big is the Hydrazine Hydrate Market?

Global Hydrazine Hydrate Market valued at USD 606M in 2024, projected to reach USD 966M by 2034, growing at 4.7% CAGR from 2026–2034, driven by chemical demand.

Who are the major players in the Hydrazine Hydrate Market?

Arkema Group, Japan Finechem Inc., Lonza Group Ltd, Arrow Fine Chemicals, LANXESS AG, Nippon Carbide Industries Co Inc., Alfa Aesar, Otsuka-MGC Chemical Company, LCG Science Group Holdings Limited, Other Key Players

Which segments covered the Hydrazine Hydrate Market?

By Concentration Level (100%, 60-85%, 40-55%, 24-35%), By Application (Water Treatment, Polymerization & Blowing Agents, Agrochemicals, Pharmaceuticals, Other Applications)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date