- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Hydrogen Fuel Cell Truck Market Size, Share | CAGR 24.8%

Global Hydrogen Fuel Cell Truck Market Size, Share, Growth Analysis By Truck Class (Class 8 Long-Haul, Class 6–7 Regional Haul, Class 4–5 Medium-Duty), By End-User (Logistics & Freight, Retail Distribution, Construction & Mining, Municipal Services), By Component (Fuel Cell Stack, Hydrogen Storage System, Power Electronics), By Fuel Type, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

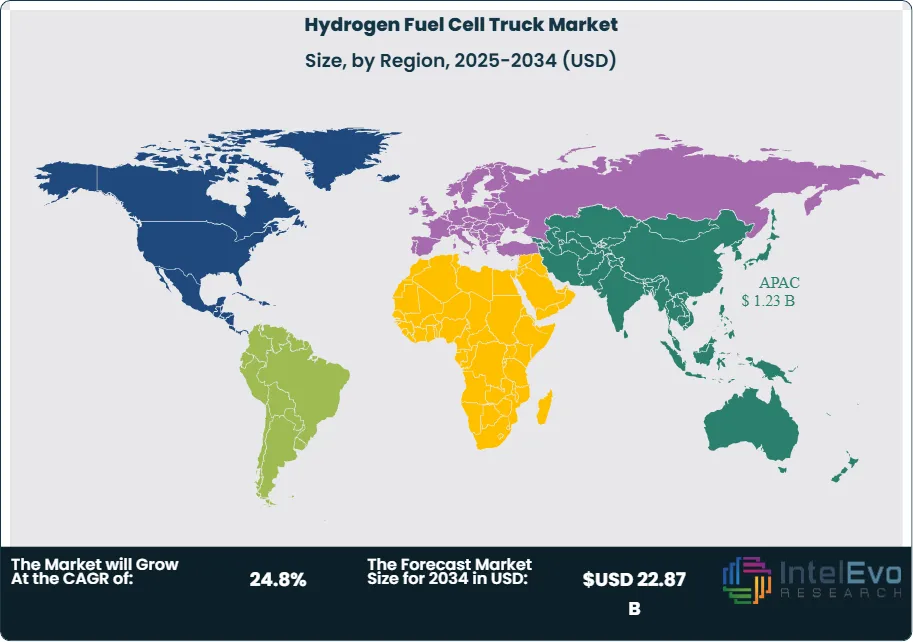

| USD 3.12 Billion | USD 22.87 Billion | 24.8% | Asia Pacific, 39.4% |

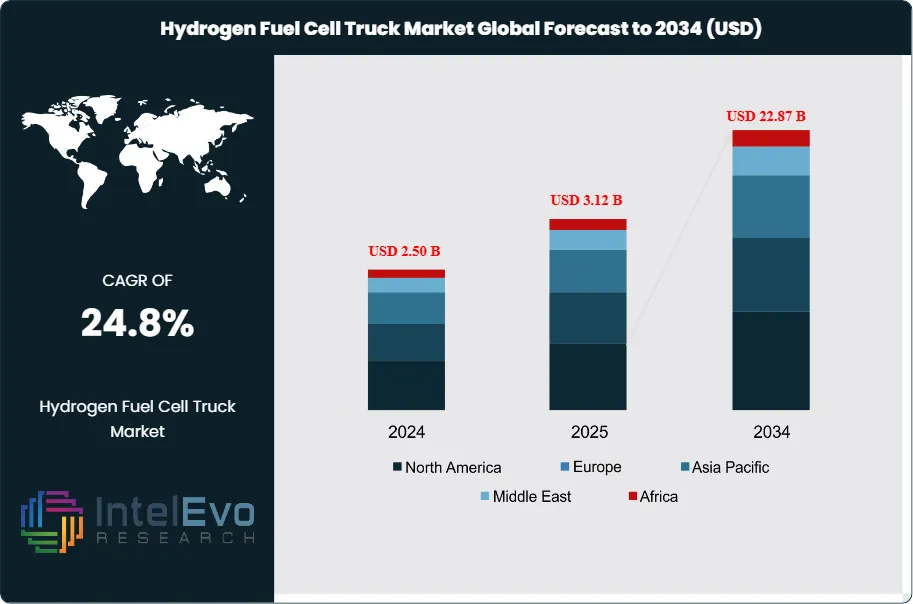

The Hydrogen Fuel Cell Truck Market was valued at approximately USD 2.50 Billion in 2024 and reached USD 3.12 Billion in 2025. The market is projected to grow to USD 22.87 Billion by 2034, expanding at a CAGR of 24.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 19.75 Billion over the analysis period, establishing the Hydrogen Fuel Cell Truck market as one of the highest-growth segments within the broader zero-emission heavy-duty transportation sector.

Get More Information about this report -

Request Free Sample ReportHydrogen fuel cell trucks use proton exchange membrane (PEM) fuel cell stacks to convert compressed hydrogen into electrical energy that drives one or more electric motors, emitting only water vapor as exhaust. The technology is particularly suited to long-haul Class 8 trucking applications where battery electric vehicles face range and payload limitations. A hydrogen fuel cell truck with a 80 kg hydrogen tank capacity can achieve ranges exceeding 1,000 km per fill, closely matching diesel operational profiles, while refueling in 15–20 minutes compared to multi-hour battery recharging windows. These operational characteristics are driving rapid adoption among logistics operators whose networks require high asset utilization rates and predictable total cost of ownership.

Market growth is anchored in three mutually reinforcing forces: decarbonization regulatory mandates, falling fuel cell system costs, and expanding hydrogen infrastructure investment. The European Union's FuelEU Maritime and Alternative Fuels Infrastructure Regulation (AFIR) mandates hydrogen refueling availability at 400 core network nodes across the Trans-European Transport Network (TEN-T) by 2030, directly enabling long-haul truck deployment economics. In the United States, the Department of Energy's Hydrogen Shot initiative targets green hydrogen production costs of USD 1.00 per kilogram by 2031, down from approximately USD 5.00–USD 8.00 per kilogram in 2025, a cost trajectory that fundamentally shifts hydrogen fuel cell truck total cost of ownership competitiveness. Fuel cell stack costs have fallen from approximately USD 300 per kilowatt in 2020 to an estimated USD 120–USD 150 per kilowatt in 2025, driven by volume manufacturing scale-up at Hyundai, Toyota, and Ballard Power Systems.

Asia Pacific leads global market revenue at 39.4% share in 2025, equivalent to approximately USD 1.23 Billion, driven by China's aggressive hydrogen heavy-duty vehicle subsidy program under the Fuel Cell Vehicle City Cluster initiative and South Korea's deployment of Hyundai XCIENT fuel cell trucks. Europe ranks second at 28.7%, underpinned by the EU's Clean Hydrogen Partnership and national hydrogen strategies in Germany, the Netherlands, and France. North America holds a 22.1% share, with California's Advanced Clean Trucks regulation and DOE Hydrogen Hub funding catalyzing fleet adoption. Competitive intensity is rising sharply, with OEM alliances, fuel cell stack supply agreements, and hydrogen infrastructure joint ventures proliferating across all three major regions since 2024.

The Hydrogen Fuel Cell Truck market is at an inflection point where demonstration-scale deployments of 2020–2024 are transitioning to commercial-scale fleet agreements in 2025–2027. Major logistics operators including DHL, DB Schenker, Amazon Logistics, and IKEA Supply Chain have committed to hydrogen truck procurement targets, creating order visibility that is enabling OEMs to justify fuel cell system manufacturing investments at gigawatt-scale. The combination of sovereign green hydrogen investment, declining stack costs, and fleet operator decarbonization commitments positions the Hydrogen Fuel Cell Truck market for sustained compound growth through 2034.

, By End-User (Logistics & Freight, Retail Distribution, Construction & Mining, Municipal Services), By Component (Fuel Cell Stack, Hydrogen Storage System, Power Electronics), By Fuel Type, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global Hydrogen Fuel Cell Truck market reached USD 3.12 Billion in 2025 and is forecast to reach USD 22.87 Billion by 2034, expanding at a CAGR of 24.8% over the 2026–2034 forecast period.

- Segment Dominance: By truck class, the Class 8 long-haul segment held the largest share at 58.3% of global revenue in 2025, reflecting the superior range and refueling-speed advantages of hydrogen fuel cells over battery alternatives at high utilization rates.

- Segment Dominance: By end-user, the logistics and freight transport segment dominated with a 46.2% share in 2025, as fleet operators with fixed long-haul routes and established depot infrastructure are the earliest and most economically motivated adopters.

- Driver: Stringent heavy-duty vehicle emissions regulations, including the EU's mandatory 90% CO2 reduction target for new heavy trucks by 2040 and California's Advanced Clean Trucks rule, are compelling OEMs and fleet operators to accelerate hydrogen fuel cell truck procurement beyond voluntary sustainability commitments.

- Restraint: Hydrogen refueling infrastructure scarcity remains the primary adoption barrier; as of 2025, fewer than 1,200 heavy-duty hydrogen refueling stations operate globally, compared to approximately 150,000 diesel truck refueling locations, limiting operational network coverage for long-haul routes.

- Opportunity: Green hydrogen production cost reductions enabled by electrolysis scale-up and renewable energy cost declines are expected to close the total cost of ownership gap between hydrogen fuel cell trucks and diesel by 2028–2030 in key markets, unlocking a fleet replacement opportunity estimated at USD 14.2 Billion by 2034.

- Trend: OEM fuel cell stack vertical integration and strategic alliances with hydrogen producers are the dominant 2025 trend, with Hyundai, Daimler Truck, and Volvo AB each announcing multi-gigawatt stack manufacturing commitments and green hydrogen supply agreements tied to fleet deployment contracts.

- Regional Analysis: Asia Pacific leads the global Hydrogen Fuel Cell Truck market with a 39.4% share in 2025, representing approximately USD 1.23 Billion, driven by China's state-subsidized Fuel Cell Vehicle City Cluster program and South Korea's commercial XCIENT FC truck exports.

Competitive Landscape Overview

The global Hydrogen Fuel Cell Truck market is moderately consolidated at the OEM level, with the top four players, Hyundai Motor Group, Daimler Truck (cellcentric joint venture), Nikola Corporation, and Toyota Motor Corporation, collectively accounting for approximately 44.7% of global market revenue in 2025. Competition is primarily technology-driven, with differentiation centered on fuel cell stack efficiency, system integration quality, hydrogen storage capacity, and total cost of ownership over a 10-year operating horizon. The Chinese domestic market exhibits higher fragmentation, with over 30 state-backed OEMs producing hydrogen fuel cell trucks under the Fuel Cell Vehicle City Cluster subsidy program. M&A activity accelerated in 2024–2025, with fuel cell component suppliers and hydrogen infrastructure operators being acquired by OEM consortia to secure supply chain control. New entrants from battery electric truck manufacturers, including BYD and Arrival, have announced fuel cell variants of existing platforms, intensifying competitive pressure.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Platform | Geographic Strength | Recent Strategic Move (2024–2026) |

| Hyundai Motor Group | South Korea | Leader | XCIENT Fuel Cell (Class 8) | Asia Pacific / Europe | Launched XCIENT FC 2.0 with 190 kW fuel cell stack; secured 1,600-unit order from Swiss logistics consortium (Jan 2025). |

| Daimler Truck (cellcentric) | Germany | Leader | Mercedes-Benz GenH2 Truck | Europe / North America | Cellcentric commenced series production of PEM fuel cell modules at Kuppenheim plant, targeting 10,000 units/year by 2027 (Mar 2025). |

| Nikola Corporation | USA | Leader | Nikola Tre FCEV | North America | Delivered 120 Tre FCEV units to U.S. fleet operators; signed hydrogen supply agreement with Fortescue Future Industries at USD 6/kg (Dec 2024). |

| Toyota Motor Corporation | Japan | Leader | Toyota Fuel Cell System (Class 8) | Asia Pacific / North America | Expanded Project Portal truck trials to 10 Port of Los Angeles operators; launched second-gen 120 kW FC module for Class 8 (Feb 2026). |

| Ballard Power Systems | Canada | Challenger | FCmove-HD+ (300 kW module) | North America / Europe | Secured multi-year supply agreement with Solaris Bus & Coach and Van Hool for heavy-duty FC modules (Sep 2025). |

| Weichai Power | China | Challenger | Weichai HOWO Hydrogen Truck | Asia Pacific | Achieved 60% fuel cell system efficiency milestone; shipped 3,400 units under China FCV City Cluster Phase II (Jun 2025). |

| Volvo AB (TRATON Group) | Sweden | Challenger | Volvo FH Hydrogen (prototype) | Europe | Announced partnership with Vattenfall and SSAB for green hydrogen supply to Volvo FC truck fleet demonstrations across Scandinavia (Apr 2025). |

| Loop Energy | Canada | Niche Player | S1200 fuel cell system | North America / Europe | Signed OEM integration agreement with Terberg Group for terminal tractor fuel cell variant; entered series production (Jan 2026). |

| Plug Power | USA | Niche Player | ProGen fuel cell engine | North America | Delivered ProGen engines to 3 Class 8 truck OEM partners; expanded green hydrogen production at Georgia electrolyzer facility to 45 TPD (Oct 2025). |

By Truck Class:

The Class 8 long-haul segment dominates the global Hydrogen Fuel Cell Truck market with a 58.3% share in 2025, equivalent to approximately USD 1.82 Billion. Class 8 trucks, typically rated above 33,000 lbs gross vehicle weight, are the primary target for hydrogen fuel cell technology because their high daily mileage, consistent route structures, and tight delivery schedules are poorly suited to battery electric alternatives requiring multi-hour recharging. A hydrogen fuel cell Class 8 truck operating at 500,000 km annually generates carbon savings of approximately 135 tonnes CO2 versus a diesel equivalent, providing fleet operators with substantial scope-3 emissions reduction contributions. Gross vehicle weight regulations in the EU, which permit hydrogen tank weight exemptions of up to 1,000 kg under Regulation (EU) 2024/1628, are preserving hydrogen truck payload competitiveness relative to battery variants. Leading Class 8 hydrogen platforms include the Hyundai XCIENT FC 2.0, Daimler GenH2, and Toyota Class 8 pilot at Los Angeles ports.

The Class 6–7 regional haul segment accounted for 27.4% of market revenue in 2025, approximately USD 855 Million. Class 6–7 trucks, used primarily for regional distribution with daily ranges of 300–600 km, represent a growing adoption opportunity as hydrogen refueling infrastructure extends from highway corridors into urban and suburban distribution hubs. Several European postal and parcel delivery operators, including Deutsche Post DHL and La Poste, have committed to hydrogen Class 6 vehicle procurement as part of their 2030 carbon neutrality commitments. The medium-duty Class 4–5 segment held the remaining 14.3% share in 2025, valued at approximately USD 446 Million, primarily concentrated in urban last-mile logistics applications in China and Japan where short-range hydrogen fuel cell systems benefit from favorable municipal subsidy structures.

By End-User:

The logistics and freight transport end-user segment represented 46.2% of the global Hydrogen Fuel Cell Truck market in 2025, approximately USD 1.44 Billion. Major third-party logistics operators are the most economically motivated early adopters because their asset-intensive business models benefit disproportionately from total cost of ownership improvements, and their fixed long-haul routes allow for dedicated hydrogen refueling infrastructure investment. DB Schenker committed to a 100-unit hydrogen truck deployment across its German inter-hub network in 2024, and Amazon Logistics has hydrogen Class 8 trucks in evaluation for its western U.S. linehaul operations. The retail and e-commerce distribution segment held 22.7% in 2025, driven by major retailers' supplier decarbonization requirements and the alignment of hydrogen refueling with distribution center infrastructure investments.

The construction and mining segment accounted for 18.4% of market revenue in 2025, reflecting demand for hydrogen fuel cell heavy equipment and off-road trucks in remote locations where grid access for charging is impractical. Mining operators in Canada, Australia, and South Africa have initiated hydrogen truck pilots for haul truck applications, with Anglo American's hydrogen haul truck demonstrating 290-tonne payload capacity in 2024. Municipal services end-users, including refuse collection, utility service, and street maintenance operators, represented the remaining 12.7% share, primarily concentrated in Japanese and South Korean municipalities with hydrogen infrastructure subsidies.

By Component:

The fuel cell stack component accounted for the largest share of the Hydrogen Fuel Cell Truck by component at 38.6% in 2025, valued at approximately USD 1.20 Billion. PEM fuel cell stacks operating at power outputs of 100–200 kW for Class 8 applications are the highest-value single component in the drivetrain, and stack cost reduction is the central determinant of hydrogen truck total cost of ownership improvement through 2034. Stack durability, currently demonstrated at 25,000–30,000 operating hours by leading suppliers, must reach 500,000 km equivalent lifetimes to match diesel engine replacement economics. Hydrogen storage systems comprised 29.3% of component revenue in 2025, reflecting the cost of Type IV carbon fiber-reinforced composite tanks rated at 350–700 bar operating pressure. Power electronics and drive systems accounted for 22.1%, with the remainder split across ancillary balance-of-plant components including air compressors, humidifiers, and thermal management systems.

By Fuel Type:

Green hydrogen, produced via renewable-powered electrolysis, represented 31.4% of hydrogen consumed by fuel cell trucks in 2025, valued at approximately USD 980 Million in market terms. While green hydrogen production costs remain elevated relative to fossil-derived alternatives, fleet operators with sustainability commitments and regulators in the EU and California are structuring procurement and subsidy programs specifically around certified green hydrogen supply. Blue hydrogen, produced from natural gas with carbon capture and storage, held a 28.9% share in 2025 and serves as a transitional supply solution in North American markets where natural gas infrastructure is extensive. Grey hydrogen, produced from natural gas without CCS, accounted for the largest share at 39.7% in 2025, reflecting current supply realities in China and developing markets. The grey hydrogen share is expected to decline significantly through 2034 as electrolyzer costs fall and green hydrogen certification programs create commercial pull for low-carbon supply.

Regional Analysis

Asia Pacific

Asia Pacific led the global Hydrogen Fuel Cell Truck market with a 39.4% share in 2025, representing approximately USD 1.23 Billion in revenue, positioning the region as both the largest current market and the fastest-growing deployment environment for hydrogen fuel cell trucks. China is the dominant Asia Pacific market, accounting for an estimated 68% of regional revenue, driven by the National Development and Reform Commission's Fuel Cell Vehicle City Cluster initiative, which has designated 17 city cluster groups for accelerated hydrogen vehicle deployment. The program provides direct purchase subsidies of RMB 250,000–RMB 500,000 per vehicle and mandates hydrogen refueling infrastructure co-investment by regional governments. Weichai Power, Yuchai, and SAIC Motor are the leading domestic OEMs, supported by fuel cell stack suppliers including Sinosynergy and Re-Fire Technology. South Korea holds approximately 18% of regional revenue, with Hyundai's XCIENT FC truck exported to Switzerland, Germany, New Zealand, and Saudi Arabia, demonstrating the platform's global commercial readiness. Japan's government has committed JPY 15 Trillion to hydrogen economy infrastructure through 2040, including dedicated hydrogen highway corridor development for freight transport linking Tokyo, Nagoya, and Osaka.

Europe

Europe accounted for 28.7% of the global Hydrogen Fuel Cell Truck market in 2025, approximately USD 896 Million, supported by the world's most comprehensive regulatory framework for heavy-duty vehicle decarbonization. The EU's Heavy-Duty Vehicles CO2 Regulation mandates 45% CO2 reduction for new trucks by 2030 and 90% by 2040 relative to 2019 baselines, making zero-emission powertrain adoption a compliance requirement rather than a voluntary initiative for fleet operators and OEMs. Germany leads European deployment, with the National Hydrogen Strategy committing EUR 9 Billion to hydrogen infrastructure and production through 2030, including dedicated heavy transport refueling corridors along the A2 and A7 autobahn networks. The H2 Accelerate initiative, backed by a consortium of logistics companies including IKEA Supply Chain, DHL, and Schenker, has committed to procuring 100,000 hydrogen trucks across Europe by 2030. The Netherlands is the second-most-active European market, serving as the regional logistics hub for Rhine-Ruhr and North Sea freight flows, with Rotterdam Port Authority integrating hydrogen refueling into its terminal infrastructure. France's national hydrogen plan allocates EUR 9 Billion through 2030, with emphasis on industrial and heavy transport hydrogen applications.

North America

North America represented 22.1% of the global Hydrogen Fuel Cell Truck market in 2025, approximately USD 690 Million, with the United States accounting for approximately 88% of regional revenue. California functions as the North American market catalyst, with the California Air Resources Board's Advanced Clean Trucks regulation requiring zero-emission vehicles to constitute a rising share of OEM truck sales, reaching 40% of Class 2b-8 trucks by 2035. The California Hydrogen Infrastructure Fund has committed USD 1.2 Billion toward heavy-duty hydrogen refueling infrastructure along the I-5 and I-10 freight corridors, providing the route coverage necessary for commercially viable long-haul deployment. The U.S. Department of Energy's Regional Clean Hydrogen Hubs program, funded at USD 7 Billion, is establishing hydrogen production and distribution clusters in the Pacific Northwest, Gulf Coast, and Great Plains regions that will supply truck fleets. Nikola Corporation is the most active North American Class 8 FCEV OEM, with commercial deliveries underway to waste management and logistics operators in California and Texas. Canada's oil sands sector in Alberta is exploring hydrogen fuel cell trucks for haul road applications, with projects from ATCO and Air Products providing hydrogen supply infrastructure.

Latin America

Latin America held a 4.8% share of the global Hydrogen Fuel Cell Truck market in 2025, approximately USD 150 Million, with activity concentrated in Brazil and Chile. Brazil's abundant renewable energy resources, including hydroelectric and wind power, create favorable conditions for green hydrogen production at competitive costs, and the government's National Hydrogen Program launched in 2023 targets the country as a green hydrogen export hub. Petrobras and Embraer have partnered to develop hydrogen production infrastructure that includes truck fueling applications. Chile's National Green Hydrogen Strategy targets 5 GW of electrolysis capacity by 2025 and positions the country as a major green hydrogen exporter, with mining sector truck fleets in the Atacama region under evaluation for hydrogen fuel cell conversion. Colombia and Argentina have hydrogen strategy frameworks at early regulatory stages, with limited near-term commercial deployment expected.

Middle East & Africa

The Middle East and Africa region accounted for 5.0% of the global Hydrogen Fuel Cell Truck market in 2025, approximately USD 156 Million, with activity concentrated in the Gulf Cooperation Council states. Saudi Arabia's NEOM project and the Kingdom's National Hydrogen Strategy target 4 million tonnes of green hydrogen production annually by 2030, with some portion designated for domestic heavy transport applications. NEOM's planned hydrogen-powered logistics fleet for the LINEAR city development has created procurement interest in hydrogen fuel cell trucks from Hyundai and Toyota. The UAE's Masdar hydrogen initiative and Abu Dhabi National Energy Company (TAQA) have invested in electrolysis infrastructure that supports transport decarbonization. South Africa's mining sector, the world's largest platinum producer, has strategic motivation to support hydrogen fuel cell adoption as PGM (platinum group metal) demand from fuel cell cathodes supports domestic mining revenues. Anglo American's hydrogen haul truck demonstrator in South Africa, which completed payload trials in 2024, has attracted government support as a showcase for indigenous hydrogen transport capability.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Truck Class

- Class 8 Long-Haul (Above 33,000 lbs GVW)

- Class 6–7 Regional Haul

- Class 4–5 Medium-Duty

By End-User

- Logistics and Freight Transport

- Retail and E-Commerce Distribution

- Construction and Mining

- Municipal Services

By Component

- Fuel Cell Stack

- Hydrogen Storage System

- Power Electronics and Drive System

- Others (Balance of Plant, Thermal Management)

By Fuel Type

- Green Hydrogen

- Blue Hydrogen

- Grey Hydrogen

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.12 B |

| Forecast Revenue (2034) | USD 22.87 B |

| CAGR (2025-2034) | 24.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Truck Class, (Class 8 Long-Haul (Above 33,000 lbs GVW), Class 6–7 Regional Haul, Class 4–5 Medium-Duty), By End-User, (Logistics and Freight Transport, Retail and E-Commerce Distribution, Construction and Mining, Municipal Services), By Component, (Fuel Cell Stack, Hydrogen Storage System, Power Electronics and Drive System, Others (Balance of Plant, Thermal Management)), By Fuel Type, (Green Hydrogen, Blue Hydrogen, Grey Hydrogen) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HYUNDAI MOTOR GROUP (HTWO), DAIMLER TRUCK (CELLCENTRIC), NIKOLA CORPORATION, TOYOTA MOTOR CORPORATION, BALLARD POWER SYSTEMS, WEICHAI POWER, VOLVO AB (TRATON GROUP), LOOP ENERGY, PLUG POWER, KENWORTH TRUCKS (PACCAR), IVECO GROUP, MAN TRUCK & BUS, SINOSYNERGY, RE-FIRE TECHNOLOGY, YUCHAI HEAVY INDUSTRY, CUMMINS (ACCELERA DIVISION), BOSCH (HYDROGEN POWERTRAIN SOLUTIONS), AIR PRODUCTS AND CHEMICALS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Logistics & Freight, Retail Distribution, Construction & Mining, Municipal Services), By Component (Fuel Cell Stack, Hydrogen Storage System, Power Electronics), By Fuel Type, Industry Trends & Forecast 2026-2034")

, By End-User (Logistics & Freight, Retail Distribution, Construction & Mining, Municipal Services), By Component (Fuel Cell Stack, Hydrogen Storage System, Power Electronics), By Fuel Type, Industry Trends & Forecast 2026-2034")

, By End-User (Logistics & Freight, Retail Distribution, Construction & Mining, Municipal Services), By Component (Fuel Cell Stack, Hydrogen Storage System, Power Electronics), By Fuel Type, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Hydrogen Fuel Cell Truck Market?

The Global Hydrogen Fuel Cell Truck Market was valued at USD 2.50 Billion in 2024 and is projected to reach USD 22.87 Billion by 2034, growing at a CAGR of 24.8% from 2026 to 2034, driven by rising demand for zero-emission heavy-duty transportation, expanding hydrogen refueling infrastructure, advancements in fuel cell technologies, and increasing government support for clean mobility and carbon-neutral logistics worldwide.

Who are the major players in the Hydrogen Fuel Cell Truck Market?

HYUNDAI MOTOR GROUP (HTWO), DAIMLER TRUCK (CELLCENTRIC), NIKOLA CORPORATION, TOYOTA MOTOR CORPORATION, BALLARD POWER SYSTEMS, WEICHAI POWER, VOLVO AB (TRATON GROUP), LOOP ENERGY, PLUG POWER, KENWORTH TRUCKS (PACCAR), IVECO GROUP, MAN TRUCK & BUS, SINOSYNERGY, RE-FIRE TECHNOLOGY, YUCHAI HEAVY INDUSTRY, CUMMINS (ACCELERA DIVISION), BOSCH (HYDROGEN POWERTRAIN SOLUTIONS), AIR PRODUCTS AND CHEMICALS, Others

Which segments covered the Hydrogen Fuel Cell Truck Market?

By Truck Class, (Class 8 Long-Haul (Above 33,000 lbs GVW), Class 6–7 Regional Haul, Class 4–5 Medium-Duty), By End-User, (Logistics and Freight Transport, Retail and E-Commerce Distribution, Construction and Mining, Municipal Services), By Component, (Fuel Cell Stack, Hydrogen Storage System, Power Electronics and Drive System, Others (Balance of Plant, Thermal Management)), By Fuel Type, (Green Hydrogen, Blue Hydrogen, Grey Hydrogen)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Hydrogen Fuel Cell Truck Market

Published Date : 22 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date