Global Hydrogen-Powered Heavy-Duty Trucks Market Size, Share, Analysis Report By Product Type (Heavy-Duty Trucks, Medium-Duty Trucks, Light-Duty Trucks), Range (Above 400 Km, Below 400 Km), Application (Logistics, Municipal), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

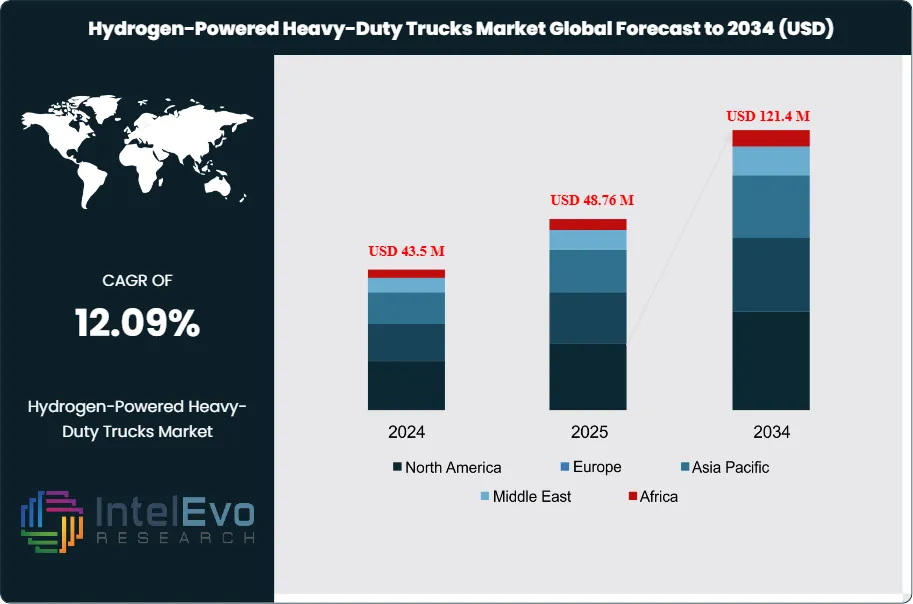

The Global Hydrogen-Powered Heavy-Duty Trucks Market size is projected to reach approximately USD 121.4 Million by 2034, up from USD 43.5 Million in 2024, growing at a CAGR of 12.09% during the forecast period from 2025 to 2034. This growth is driven by increasing environmental regulations, rising demand for low-emission freight solutions, and advancements in hydrogen fuel cell technology. Major logistics and transportation companies are investing in hydrogen-powered trucks to reduce carbon footprints and enhance operational efficiency. As governments and private enterprises push for cleaner and sustainable transport alternatives, hydrogen-powered heavy-duty trucks are poised to play a crucial role in the transition toward zero-emission freight and long-haul transportation globally.

The global hydrogen-powered heavy-duty trucks market refers to the segment of the automotive industry that focuses on trucks powered by hydrogen fuel cells. These vehicles utilize hydrogen as a clean energy source, emitting only water vapor as a byproduct. The current market is characterized by an increasing demand for sustainable transport solutions, driven by rising environmental concerns and government initiatives promoting cleaner alternatives. Major players, including automotive manufacturers and technology firms, are actively investing in research and development to enhance the efficiency and performance of hydrogen trucks, aiming to reduce dependence on fossil fuels.

Several key drivers influence growth dynamics in this market. First, the urgent need to reduce greenhouse gas emissions in the transportation sector is propelling the adoption of hydrogen-powered trucks. Second, advancements in hydrogen fuel cell technology, which have significantly improved the range and efficiency of these vehicles, are making them more appealing to logistics companies. Third, government incentives and subsidies aimed at promoting zero-emission vehicles are further supporting market growth. As logistics and transportation companies strive to meet stringent emission regulations, the transition to hydrogen-powered trucks is becoming increasingly vital.

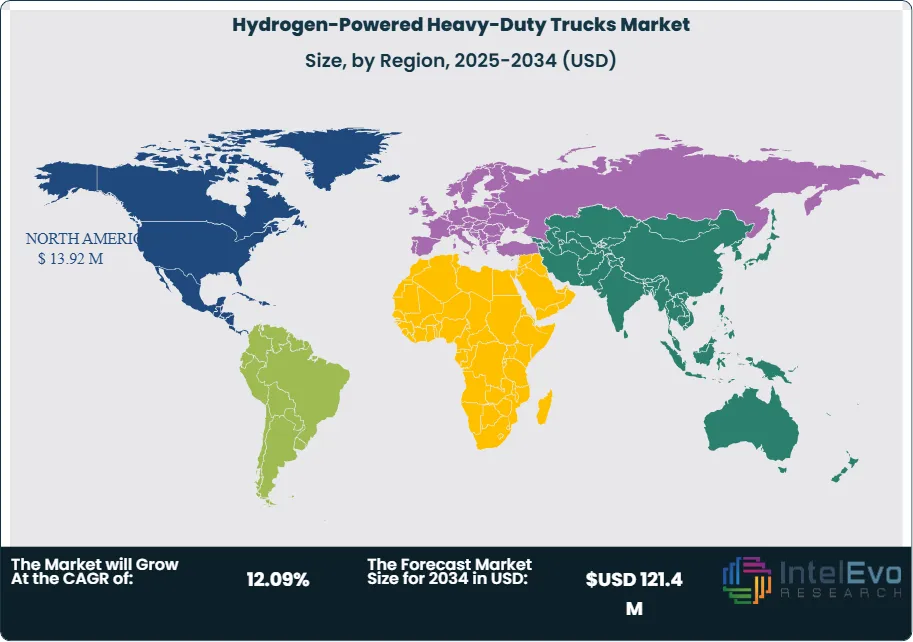

North America is projected to dominate the hydrogen-powered heavy-duty trucks market due to significant investments in hydrogen infrastructure and the presence of major manufacturers. The United States is leading the charge with various initiatives aimed at expanding hydrogen fuel cell technology. In contrast, the Asia-Pacific region is expected to experience the fastest growth rate, driven by the rising demand for advanced transportation solutions and government backing for fuel cell development. Countries like Japan and China are actively pursuing hydrogen as part of their energy strategy, enhancing the market landscape in this region.

The COVID-19 pandemic has had a notable impact on the hydrogen-powered heavy-duty trucks market. Initially, supply chain disruptions and decreased transportation activity led to a slowdown in vehicle production and sales. However, the crisis also accelerated the push for cleaner transportation solutions as governments and companies recognized the importance of resilience and sustainability. This shift in focus is expected to boost the adoption of hydrogen-powered trucks in the post-pandemic recovery phase, as stakeholders prioritize investments in environmentally friendly technologies.

Key Takeaways:

Market Growth: The hydrogen-powered heavy-duty trucks market is expected to reach USD 121.4 million by 2034, growing at a robust CAGR of 12.09%, indicating strong market expansion.

Product Type Analysis: The heavy-duty trucks segment is anticipated to dominate the market, driven by the increasing demand for larger, more efficient vehicles for logistics and freight transportation, which require longer ranges and greater payload capacities.

Range Analysis: The segment for trucks with a range above 400 km is projected to see significant growth due to the need for vehicles that can efficiently cover long distances without frequent refueling, appealing to logistics companies and long-haul transporters.

Driver: The increasing regulatory pressure to reduce greenhouse gas emissions in the transportation sector is driving demand for hydrogen-powered trucks as companies look for sustainable alternatives to fossil fuel-powered vehicles.

Restraint: High initial investment costs for hydrogen infrastructure and fuel cell technology can pose a barrier to market growth, as many logistics companies may hesitate to transition from traditional diesel trucks.

Opportunity: Significant growth potential exists in developing hydrogen infrastructure and partnerships with governments and private entities to create refueling stations, thereby facilitating the widespread adoption of hydrogen-powered trucks.

Trend: There is a growing trend toward integrating advanced fuel cell technology in heavy-duty trucks, enhancing efficiency and performance, which is vital for meeting increasing transportation demands.

Regional Analysis: North America and the Asia-Pacific region are projected to lead the market, driven by substantial investments in hydrogen infrastructure and government initiatives supporting zero-emission vehicles.

Product Type:

The hydrogen-powered heavy-duty trucks market is segmented into heavy-duty, medium-duty, and light-duty trucks. Heavy-duty trucks are expected to dominate the market due to their critical role in freight transportation, requiring higher payload capacities and longer ranges. These vehicles often serve logistics companies that demand efficiency and sustainability in their operations. Medium-duty trucks, while smaller, are gaining traction in urban delivery applications where emissions regulations are stringent. Light-duty trucks are also becoming relevant, especially in last-mile delivery, as companies transition to zero-emission vehicles. As technology advances and infrastructure improves, all segments are likely to see increased adoption, but heavy-duty trucks will remain the backbone of the market.

Range:

The range segment of hydrogen-powered heavy-duty trucks is categorized into those with ranges above and below 400 km. Trucks with a range above 400 km are expected to see significant growth due to their suitability for long-haul transportation. This range allows logistics companies to operate efficiently without frequent refueling stops, thereby enhancing productivity. In contrast, trucks with a range below 400 km are likely to be used for regional or urban deliveries, where shorter distances are the norm. As fuel cell technology advances, the range of hydrogen trucks is expected to improve, making longer-distance transportation more feasible, ultimately catering to diverse logistical needs across different markets.

Application:

The application segment includes logistics and municipal uses. Logistics applications dominate the market, driven by the need for sustainable solutions in freight transportation. As companies aim to meet strict emissions regulations and enhance their sustainability profiles, hydrogen-powered trucks offer an attractive alternative to diesel. Municipal applications, such as waste management and public transport, are also emerging as significant areas for hydrogen truck deployment. Local governments are increasingly adopting these vehicles to reduce urban pollution and comply with environmental targets. Both applications will continue to drive growth, with logistics being the primary focus, while municipal applications provide valuable opportunities for local governments.

Region Analysis:

North America Leads with Significant Market Share in Hydrogen-Powered Heavy-Duty Trucks: North America holds the largest market share in the hydrogen-powered heavy-duty trucks sector, driven primarily by robust investments in hydrogen infrastructure and favorable government policies promoting zero-emission vehicles. The United States is at the forefront, implementing initiatives aimed at enhancing hydrogen refueling stations, which facilitates the adoption of hydrogen trucks among logistics companies. Additionally, major automotive manufacturers in the region are actively developing fuel cell technologies, enhancing performance and efficiency. The combination of stringent emission regulations, a strong emphasis on sustainability, and substantial funding for research and development in hydrogen technologies positions North America as the leading market, fostering further growth in the coming years.

The Asia-Pacific region is emerging as the fastest-growing market for hydrogen-powered heavy-duty trucks, fueled by strong governmental support and increasing awareness of sustainable transportation. Countries like Japan and China are heavily investing in hydrogen technology and infrastructure, making significant strides toward becoming global leaders in hydrogen mobility. The rising demand for clean energy solutions in densely populated urban areas drives growth in municipal applications, while logistics companies are increasingly adopting hydrogen trucks to meet regulatory requirements. Moreover, the ongoing collaboration between private enterprises and government entities fosters innovation and infrastructure development. Other regions, including Europe, Latin America, and the Middle East and Africa, are also witnessing growth; however, they are primarily focused on regulatory frameworks and pilot projects, positioning themselves for future advancements.

By Vehicle Type (Long-Haul Trucks, Medium-Duty Trucks, Specialty Vehicles), By Fuel Type, Hydrogen Fuel Cell, Hydrogen Hybrid Systems), By Range (Above 400 Km, Below 400 Km), By Application (Logistics & Freight Transport, Municipal & Public Transport, Construction & Mining, Others)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Toyota Motor Corporation, Daimler Truck AG (Mercedes-Benz Trucks), Hyundai Motor Company, Nikola Corporation, Volvo Group, MAN Truck & Bus AG, PACCAR Inc. (Kenworth & Peterbilt), Hino Motors, Ltd., Scania AB, BYD Company Ltd., Cummins Inc. (Fuel Cell Division), Ballard Power Systems Inc., Plug Power Inc., Shell Hydrogen, Air Liquide SA, Freightliner (Daimler Trucks North America), Rivian Automotive, Inc., Ashok Leyland, Foton Motor, Isuzu Motors Ltd., ElringKlinger AG, PowerCell Sweden AB, Ørsted A/S

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL HYDROGEN-POWERED HEAVY-DUTY TRUCKS CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Players Analysis:

Nikola Corporation: Nikola focuses on hydrogen fuel cell and battery-electric vehicles, primarily heavy-duty trucks. Their flagship model, the Nikola Two, is designed for long-haul trucking. Headquartered in Phoenix, Arizona, Nikola aims to revolutionize the trucking industry by establishing a network of hydrogen refueling stations, enhancing the feasibility of hydrogen as a transport fuel.

Hyundai Motor Company: Hyundai is a South Korean automotive manufacturer known for its innovation in hydrogen fuel cell technology. The company offers the Xcient Fuel Cell, a heavy-duty truck that operates using hydrogen. Hyundai’s strategy includes expanding its hydrogen ecosystem, from production to distribution, while investing in research and development to enhance fuel cell performance.

Toyota Motor Corporation: Toyota, headquartered in Japan, has been a pioneer in hydrogen fuel cell technology with its Mirai sedan. The company is expanding its offerings to include heavy-duty trucks, focusing on sustainability and low-emission vehicles. Toyota’s strategy involves partnerships for hydrogen infrastructure development and leveraging its extensive experience in fuel cell technology.

Daimler AG: Daimler AG is a global leader in commercial vehicles and has invested heavily in hydrogen fuel cell technology. The Mercedes-Benz GenH2 Truck is an innovative model designed for long-distance transport. Daimler's strategy emphasizes sustainability and achieving carbon neutrality, aiming to integrate hydrogen fuel cells into its existing fleet and infrastructure.

Volvo Group: Based in Sweden, Volvo Group produces trucks, buses, and construction equipment, with a growing focus on hydrogen technology. The Volvo FM Electric and upcoming hydrogen fuel cell trucks exemplify its commitment to sustainable transportation. Volvo aims to achieve climate neutrality by 2040, investing in innovative solutions and partnerships to develop hydrogen infrastructure.

MAN Energy Solutions: MAN Energy Solutions, part of the Volkswagen Group, focuses on engine technology and sustainable energy solutions. They are developing hydrogen-powered engines and related technologies for heavy-duty transport. Based in Germany, MAN's strategy includes transitioning to sustainable fuels and enhancing efficiency in marine and power generation sectors, aligning with global decarbonization goals.

Scania AB: Scania, a Swedish manufacturer of commercial vehicles, offers sustainable transport solutions, including hydrogen trucks. Their R 450 model showcases advanced fuel efficiency and low emissions. Scania’s strategy emphasizes a holistic approach to transport solutions, integrating hydrogen technology into its portfolio to support customers in achieving their sustainability targets.

PACCAR Inc.: PACCAR, headquartered in Bellevue, Washington, manufactures high-quality trucks under the Kenworth and Peterbilt brands. The company is investing in hydrogen fuel cell technology, with plans to introduce hydrogen-powered trucks. PACCAR’s strategy focuses on technological innovation and sustainability, aiming to meet regulatory demands while enhancing fuel efficiency across its product lines.

Hino Motors, Ltd.: Hino, a subsidiary of Toyota, is a Japanese manufacturer specializing in trucks and buses. The company is exploring hydrogen fuel cell technology as part of its strategy to reduce emissions. Hino’s initiatives include collaboration with various partners to develop hydrogen infrastructure and promote the adoption of fuel cell vehicles in commercial applications.

BYD Company Ltd.: BYD, based in China, is a major player in electric vehicles and is expanding its hydrogen fuel cell offerings. The company produces a range of commercial vehicles, including buses and trucks, emphasizing sustainability. BYD’s strategy focuses on vertical integration of its supply chain, enabling the development of comprehensive hydrogen solutions from production to end use.

Market Key Players

Toyota Motor Corporation

Daimler Truck AG (Mercedes-Benz Trucks)

Hyundai Motor Company

Nikola Corporation

Volvo Group

MAN Truck & Bus AG

PACCAR Inc. (Kenworth & Peterbilt)

Hino Motors, Ltd.

Scania AB

BYD Company Ltd.

Cummins Inc. (Fuel Cell Division)

Ballard Power Systems Inc.

Plug Power Inc.

Shell Hydrogen

Air Liquide SA

Freightliner (Daimler Trucks North America)

Rivian Automotive, Inc.

Ashok Leyland

Foton Motor

Isuzu Motors Ltd.

ElringKlinger AG

PowerCell Sweden AB

Ørsted A/S

Driver:

Regulatory Support for Emission Reduction

One of the primary drivers for the hydrogen-powered heavy-duty trucks market is the increasing regulatory support aimed at reducing greenhouse gas emissions. Governments around the world are implementing stricter emission regulations, particularly for the transportation sector, pushing companies to adopt cleaner technologies. Initiatives such as the European Union’s Green Deal and various U.S. state regulations are creating a favorable environment for hydrogen vehicles. These regulations not only encourage manufacturers to invest in hydrogen technology but also incentivize logistics companies to transition away from traditional diesel trucks. The growing emphasis on sustainability and carbon neutrality is likely to drive the demand for hydrogen-powered trucks, positioning them as a viable alternative in the market.

Technological Advancements in Fuel Cells

Technological advancements in fuel cell technology significantly contribute to the growth of the hydrogen-powered heavy-duty trucks market. Innovations in fuel cell efficiency, durability, and cost-effectiveness are making hydrogen trucks more competitive with conventional vehicles. As fuel cells become lighter and more powerful, the overall performance of hydrogen trucks improves, allowing them to meet the demands of logistics and transportation. Furthermore, advancements in hydrogen production and storage technologies, such as electrolysis and high-pressure tanks, are enhancing the feasibility of hydrogen as a fuel source. These improvements not only bolster consumer confidence but also attract investments from manufacturers eager to capitalize on the growing market for clean transportation solutions.

Rising Demand for Sustainable Logistics Solutions

The growing demand for sustainable logistics solutions is another key driver for the hydrogen-powered heavy-duty trucks market. As consumers become more environmentally conscious, businesses are under increasing pressure to adopt eco-friendly practices in their operations. Logistics companies are increasingly seeking alternatives to diesel-powered vehicles to reduce their carbon footprints. Hydrogen-powered trucks offer a sustainable solution, as they emit only water vapor during operation. This shift toward greener logistics is complemented by partnerships between companies and government bodies aimed at establishing hydrogen refueling infrastructure. As sustainability becomes a central tenet of corporate strategy, the adoption of hydrogen trucks is likely to grow, driving market expansion in the coming years.

Restraints:

High Initial Infrastructure Costs

One of the primary restraints hindering the growth of the hydrogen-powered heavy-duty trucks market is the high initial infrastructure costs associated with hydrogen production, storage, and distribution. Developing a network of hydrogen refueling stations requires substantial investment, which can be a barrier for both public and private stakeholders. This infrastructure is critical for the widespread adoption of hydrogen trucks, as the lack of refueling options can deter potential buyers. Additionally, existing logistics companies may be reluctant to invest in new hydrogen trucks without the assurance of adequate refueling infrastructure in their operating regions. Until these challenges are addressed, the market may struggle to realize its full potential.

Limited Range Compared to Diesel Trucks

While hydrogen-powered trucks offer significant environmental benefits, their range can be perceived as a limitation compared to traditional diesel trucks. Although advancements are being made to increase the range of hydrogen trucks, concerns remain about their ability to cover long distances without frequent refueling stops. This limitation is particularly crucial for logistics companies that depend on operational efficiency and timely deliveries. Furthermore, the development of refueling infrastructure is still in its early stages in many regions, adding to the hesitation of companies to transition from diesel. Until the range issues and infrastructure gaps are adequately addressed, the market's growth may be constrained.

Opportunities:

Government Incentives for Clean Technology Adoption

The increasing availability of government incentives for the adoption of clean technologies presents a significant opportunity for the hydrogen-powered heavy-duty trucks market. Many governments are offering subsidies, tax breaks, and grants to companies investing in zero-emission vehicles. These financial incentives can lower the total cost of ownership for hydrogen trucks, making them more attractive to logistics firms. Additionally, the establishment of public-private partnerships can lead to the rapid development of hydrogen infrastructure, further accelerating market adoption. As environmental policies become more favorable, companies can leverage these opportunities to transition to hydrogen-powered fleets, ultimately driving market growth.

Expansion of Hydrogen Infrastructure

Another significant opportunity lies in the expansion of hydrogen infrastructure, including refueling stations and production facilities. As governments and private companies invest in developing this infrastructure, it will facilitate the widespread adoption of hydrogen trucks. The establishment of a robust hydrogen supply chain will enhance the feasibility of hydrogen-powered vehicles, addressing one of the main barriers to market growth. Furthermore, advancements in hydrogen production methods, such as green hydrogen generated from renewable sources, can increase the availability of hydrogen as a fuel. The collaborative efforts between stakeholders to build comprehensive hydrogen networks present a unique opportunity to drive market growth and adoption.

Trend:

Increasing Integration of Smart Technologies

A notable trend in the hydrogen-powered heavy-duty trucks market is the increasing integration of smart technologies, such as telematics and AI-based systems. These technologies enhance vehicle performance and operational efficiency by providing real-time data on fuel consumption, route optimization, and maintenance needs. The use of smart technologies allows logistics companies to manage their fleets more effectively, reducing costs and emissions. As hydrogen trucks become more connected and integrated into broader logistics networks, their appeal will grow, attracting more investments. This trend reflects the overall shift toward digitization and smart transportation solutions in the logistics sector, driving further adoption of hydrogen-powered vehicles.

Recent Development:

In October 2024: Nikola Corporation achieved a significant milestone by wholesaling 88 hydrogen-powered Class 8 trucks in Q3 2024, marking a record sales quarter for the company. Additionally, Nikola introduced its first U.S. dealer-based HYLA modular refueling station, emphasizing its commitment to advancing zero-emission solutions despite market challenges. So far in 2024, Nikola has wholesaled a total of 200 hydrogen fuel cell trucks

In September 2024: Rivian Automotive reported a 76% increase in production year-over-year, reaching 18,948 vehicles produced in Q3 2024. The company aims to build on this momentum with a forecasted total of 20,000 vehicles for the year. Rivian is also expanding its workforce by approximately 1,500 employees to support its production goals.

Frequently Asked Questions

How big is the Hydrogen-Powered Heavy-Duty Trucks Market?

The Hydrogen-Powered Heavy-Duty Trucks Market is projected to reach USD 121.4M by 2034 at 12% CAGR, driven by hydrogen fuel cell adoption and zero-emission freight solutions.

Who are the major players in the Hydrogen-Powered Heavy-Duty Trucks Market?

Toyota Motor Corporation, Daimler Truck AG (Mercedes-Benz Trucks), Hyundai Motor Company, Nikola Corporation, Volvo Group, MAN Truck & Bus AG, PACCAR Inc. (Kenworth & Peterbilt), Hino Motors, Ltd., Scania AB, BYD Company Ltd., Cummins Inc. (Fuel Cell Division), Ballard Power Systems Inc., Plug Power Inc., Shell Hydrogen, Air Liquide SA, Freightliner (Daimler Trucks North America), Rivian Automotive, Inc., Ashok Leyland, Foton Motor, Isuzu Motors Ltd., ElringKlinger AG, PowerCell Sweden AB, Ørsted A/S

Which segments covered the Hydrogen-Powered Heavy-Duty Trucks Market?

By Vehicle Type (Long-Haul Trucks, Medium-Duty Trucks, Specialty Vehicles), By Fuel Type, Hydrogen Fuel Cell, Hydrogen Hybrid Systems), By Range (Above 400 Km, Below 400 Km), By Application (Logistics & Freight Transport, Municipal & Public Transport, Construction & Mining, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, Range (Above 400 Km, Below 400 Km), Application (Logistics, Municipal), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Range (Above 400 Km, Below 400 Km), Application (Logistics, Municipal), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Range (Above 400 Km, Below 400 Km), Application (Logistics, Municipal), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

, Range (Above 400 Km, Below 400 Km), Application (Logistics, Municipal), Region and Key Players - Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")