- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Immune Checkpoint Inhibitor Market Size, Share | CAGR of 16.5%

Global Immune Checkpoint Inhibitor Market Size, Share, Analysis By Type (PD-1, PD-L1, CTLA-4 Inhibitors), By Indication (Lung Cancer, Melanoma, Renal Cell Carcinoma), By Route (Intravenous, Subcutaneous) Region, Key Players – Dynamics, Immuno-Oncology Monoclonal Antibodies & Target Tumor Immunotherapy Pipelines, Growth Opportunities Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

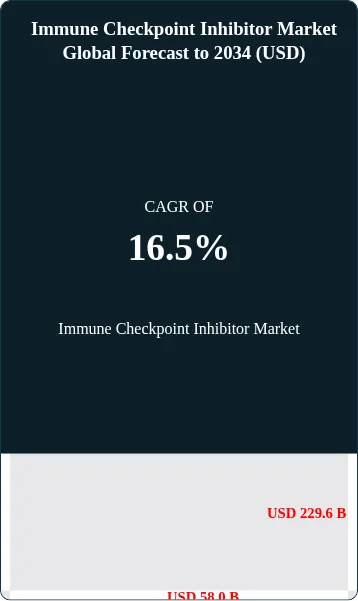

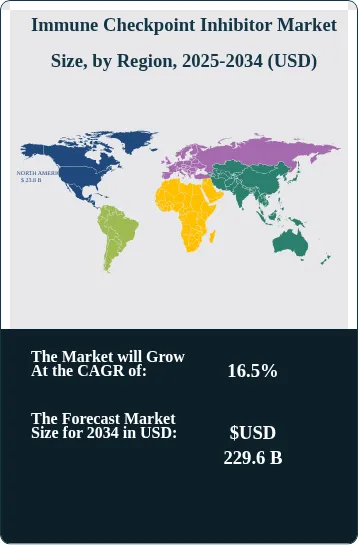

| USD 58.0 Billion | USD 229.6 Billion | 16.5% | North America, 41.0% |

The Immune Checkpoint Inhibitor Market was valued at approximately USD 50.1 billion in 2024 and reached USD 58.0 billion in 2025. The market is projected to grow to USD 229.6 billion by 2034, expanding at a CAGR of 16.5% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 171.6 billion over the analysis period—the largest absolute dollar expansion of any single pharmaceutical product category globally. The market's commercial scale is anchored by Merck & Co.'s KEYTRUDA (pembrolizumab), which alone posted full-year 2024 sales of USD 29.5 billion (18% growth year-over-year), making it the best-selling pharmaceutical drug in the world. Immune checkpoint inhibitors (ICIs) have fundamentally transformed oncology practice since ipilimumab (Yervoy) became the first FDA-approved ICI in 2011, and the sector now encompasses more than a dozen approved monoclonal antibodies targeting PD-1, PD-L1, CTLA-4, and LAG-3 checkpoints across more than 80 cancer indication-drug combinations.

Get More Information about this report -

Request Free Sample ReportImmune checkpoint inhibitors work by blocking inhibitory proteins on T-cells or tumor cells that cancer exploits to evade immune destruction. The programmed death-1 (PD-1) receptor on T-cells and its ligand programmed death-ligand 1 (PD-L1) on tumor cells form the market's dominant target axis: when tumor cells express PD-L1, they suppress T-cell activity by engaging PD-1, effectively cloaking themselves from immune destruction. Anti-PD-1 antibodies (pembrolizumab, nivolumab, cemiplimab, tislelizumab, dostarlimab) and anti-PD-L1 antibodies (atezolizumab, durvalumab, avelumab) disrupt this suppression, restoring T-cell cytotoxic activity against tumor cells. Cytotoxic T-lymphocyte antigen 4 (CTLA-4) inhibitors (ipilimumab, tremelimumab) act earlier in the immune activation cycle, preventing T-cell suppression at the priming stage. In 2022, FDA approved the first LAG-3 blocking antibody combination—Opdualag (nivolumab + relatlimab)—for advanced melanoma, where it more than doubled median progression-free survival versus nivolumab monotherapy in the Phase 2/3 RELATIVITY-047 trial.

Three structural forces sustain the market's 16.5% CAGR. First, indication expansion: the FDA approves 8–12 new or expanded ICI indications per year, with each approval generating a new prescribable patient population. Second, earlier-stage treatment: ICIs are progressively moving from palliative metastatic settings into adjuvant and neoadjuvant perioperative settings where eligible patient populations are substantially larger. In 2025, AstraZeneca received FDA approval for perioperative Imfinzi (durvalumab) combined with FLOT chemotherapy in resectable gastric and gastroesophageal junction cancer—expanding durvalumab's reach from advanced to operable disease. Third, formulation innovation: the December 27, 2024 FDA approval of Opdivo Qvantig (subcutaneous nivolumab + hyaluronidase-nvhy) as the first subcutaneously administered PD-1 inhibitor, followed by the September 19, 2025 approval of subcutaneous pembrolizumab with berahyaluronidase alfa-pmph, enables 3–5 minute injections versus 30-minute IV infusions, expanding delivery to community oncology practices and potentially increasing treatment adherence.

Non-small cell lung cancer (NSCLC) is the market's largest single indication, commanding 25–29% of ICI revenue in 2025, because lung cancer's high global incidence (approximately 2.5 million new cases annually per WHO 2022 data), the PD-L1 expression prevalence across NSCLC histologies, and KEYTRUDA's first-line approval across PD-L1-positive NSCLC patients create the broadest commercially accessible patient population for any single ICI indication. The FDA's Oncology Drugs Advisory Committee voted in September 2024 on the appropriate use of PD-1 inhibitors in NSCLC combination regimens, reflecting regulatory attention to evidence generation standards in this indication. Combination immunotherapy—pairing two checkpoint inhibitors or combining checkpoint inhibitors with chemotherapy, VEGF inhibitors, or PARP inhibitors—is the field's primary clinical development focus, with Merck running more than 30 Phase 3 KEYTRUDA combination trials as of early 2026.

North America dominated the immune checkpoint inhibitor market in 2025 with a 41.0% share at approximately USD 23.8 billion, anchored by U.S. oncology reimbursement under Medicare Part B (covering physician-administered IV immunotherapies) and the United States' contribution to more than 50% of global cancer treatment expenditure. Asia Pacific is the fastest-growing region, with China's domestic ICI market growing at an estimated 19.56% CAGR through 2031 as domestic biotechs including BeiGene (tislelizumab) and Innovent Biologics compete alongside Merck and BMS, and as China's National Reimbursement Drug List progressively includes pembrolizumab and nivolumab following price negotiations under the National Healthcare Security Administration.

Market Definition & Scope

The immune checkpoint inhibitor market is defined as the commercial and clinical-stage market for monoclonal antibodies and bispecific antibody therapies that restore anti-tumor immune responses by blocking inhibitory checkpoint proteins on immune cells or tumor cells, thereby releasing T-cell suppression and enabling immunological recognition and destruction of cancer cells. The market encompasses six approved checkpoint target classes: PD-1 inhibitors (pembrolizumab, nivolumab, cemiplimab, tislelizumab, dostarlimab, balstilimab), PD-L1 inhibitors (atezolizumab, durvalumab, avelumab, cosibelimab), CTLA-4 inhibitors (ipilimumab, tremelimumab), LAG-3 inhibitors (relatlimab, currently approved only as the fixed-dose Opdualag combination), and emerging targets including TIM-3 (hepatitis A virus cellular receptor 2), TIGIT (T-cell immunoreceptor with Ig and ITIM domains), and CD73 in late-stage clinical investigation. Approved combination products—including Opdualag (nivolumab + relatlimab fixed-dose) and the NALIRIFOX regimen anchored by Onivyde—are included where the ICI component is the primary commercial driver. Both intravenous and approved subcutaneous formulations are included.

This analysis covers all commercially approved immune checkpoint inhibitor products globally, including FDA-approved, EMA-approved, and major national market approvals (Japan PMDA, China NMPA). Explicitly excluded are checkpoint inhibitors in pre-clinical or Phase 1 discovery stage without approved indications, antibody-drug conjugates where the ICI component is not the primary payload mechanism, adoptive cell therapies (CAR-T, TIL therapy), cancer vaccines, cytokine therapies (IL-2, interferon), and non-ICI targeted oncology agents. The immune checkpoint inhibitor market represents the largest sub-category of the immuno-oncology market, accounting for approximately 80% of total immuno-oncology revenues and more than 25% of all global oncology drug revenues in 2025.

, By Indication (Lung Cancer, Melanoma, Renal Cell Carcinoma), By Route (Intravenous, Subcutaneous) Region, Key Players – Dynamics, Immuno-Oncology Monoclonal Antibodies & Target Tumor Immunotherapy Pipelines, Growth Opportunities Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global immune checkpoint inhibitor market grew from approximately USD 21.4 billion in 2020 to USD 58.0 billion in 2025, a 22.1% CAGR over the prior 5 years, and is forecast to reach USD 229.6 billion by 2034, generating a 16.5% CAGR and an absolute dollar opportunity of USD 171.6 billion during the 2025–2034 forecast period—the highest absolute dollar growth of any therapeutic class globally.

- Segment Dominance (Type): PD-1 inhibitors held approximately 57.0–70.0% of ICI market revenue in 2025, generating approximately USD 33.1–40.6 billion, because pembrolizumab's 40+ FDA-approved indications across solid tumors and hematological malignancies, combined with nivolumab's comparable multi-tumor label and cemiplimab's accelerating NSCLC franchise, collectively dominate clinical practice across the most prevalent cancer types worldwide.

- Segment Dominance (Indication): Non-small cell lung cancer retained the largest indication share at approximately 26.3% of ICI market revenue in 2025 at approximately USD 15.2 billion, because NSCLC represents the world's highest-burden oncology indication by absolute patient volume and because pembrolizumab achieved first-line standard-of-care status across PD-L1-positive NSCLC in both monotherapy (PD-L1 TPS ≥50%) and combination with chemotherapy settings.

- Driver: The ongoing shift of ICI use from metastatic to earlier disease stages is the market's primary structural volume driver; adjuvant and neoadjuvant ICI approvals create patient populations 3–5 times larger than metastatic populations for the same cancer type, and perioperative ICI treatment in resectable NSCLC, gastric cancer, and bladder cancer is generating substantial new prescription volume above and beyond the established metastatic baseline.

- Restraint: Immune-related adverse events (irAEs) represent the primary clinical restraint on ICI utilization, with Grade 3–4 irAEs including pneumonitis (2–5% incidence), colitis (1–2%), hepatitis (1–3%), and myocarditis (<1% but potentially fatal) requiring treatment discontinuation, corticosteroid management, and specialized monitoring that limits ICI use in patients with pre-existing autoimmune conditions and constrains the ratio of patients who can receive full-course treatment.

- Opportunity: Subcutaneous ICI formulations represent an estimated USD 8–15 billion incremental commercial opportunity through 2034 by expanding delivery into community oncology and primary care settings that lack infusion chair capacity; Opdivo Qvantig (SC nivolumab approved December 27, 2024) and SC pembrolizumab (approved September 19, 2025) together begin a subcutaneous conversion cycle that Mordor Intelligence estimates will drive subcutaneous route growth at a 25.4% CAGR through 2031.

- Trend: Tumor mutational burden (TMB) and microsatellite instability (MSI-H/dMMR) biomarker testing is becoming standard pre-treatment workup for all solid tumor patients, enabling tissue-agnostic ICI prescribing in the approximately 3–5% of metastatic solid tumor patients with high TMB or MSI-H status regardless of primary tumor site; the FDA's 2017 tissue-agnostic pembrolizumab approval for MSI-H solid tumors was the first such approval in oncology history.

- Regional: North America led with 41.0% revenue share in 2025 at approximately USD 23.8 billion, driven by the United States contributing more than 95% of North American ICI revenue through its leadership in ICI price setting (pembrolizumab U.S. list price approximately USD 15,000 per infusion for the 400 mg/6-week dose), first-in-world launches of new ICI approvals, and the highest per-capita cancer treatment expenditure globally.

Key Insights Summary

- On September 19, 2025, the FDA approved subcutaneous pembrolizumab with berahyaluronidase alfa-pmph (sBLA for co-formulation with Halozyme's ENHANZE technology) for all solid tumor indications previously approved for intravenous KEYTRUDA in patients 12 years and older; the approval enables a subcutaneous injection delivery in under 5 minutes versus the standard 30-minute IV infusion, based on the pivotal Phase 3 noninferiority trial demonstrating pharmacokinetic equivalence with IV pembrolizumab in first-line NSCLC in combination with chemotherapy.

- On December 27, 2024, the FDA approved Opdivo Qvantig (nivolumab + hyaluronidase-nvhy) as the first subcutaneously administered PD-1 inhibitor in the United States, co-formulated using Halozyme's ENHANZE drug delivery technology, across all previously approved adult solid tumor nivolumab indications covering renal cell carcinoma, melanoma, NSCLC, head and neck squamous cell carcinoma, urothelial carcinoma, colorectal cancer, hepatocellular carcinoma, and esophageal carcinoma; Opdivo Qvantig was priced at parity with IV Opdivo and launched in early January 2025.

- Merck & Co. reported full-year 2024 KEYTRUDA (pembrolizumab) global sales of USD 29.5 billion, a year-over-year increase of 18% (22% excluding foreign exchange impact), representing approximately 46% of Merck's total 2024 worldwide revenue of USD 64.2 billion and confirming pembrolizumab as the highest-grossing pharmaceutical product globally in 2024; the company maintained more than 30 active Phase 3 combination trials as of Q1 2026 to sustain post-patent indication depth ahead of the anticipated 2028 U.S. patent expiry.

- AstraZeneca's Imfinzi (durvalumab) received FDA approval in 2025 for perioperative use in combination with FLOT chemotherapy (fluorouracil, leucovorin, oxaliplatin, docetaxel) for resectable gastric and gastroesophageal junction cancer at Stages II–IVA, based on the Phase 3 MATTERHORN trial demonstrating statistically significant and clinically meaningful improvement in event-free survival and overall survival versus perioperative chemotherapy alone; results were presented at the 2025 ASCO Annual Meeting Plenary Session and simultaneously published in The New England Journal of Medicine.

- The FDA approved the combination of nivolumab (Opdivo) and ipilimumab (Yervoy) as a first-line treatment for microsatellite instability-high (MSI-H) or mismatch repair-deficient (dMMR) metastatic colorectal cancer in May 2025, based on the Phase 3 CheckMate-8HW trial (>800 patients, 3 arms) demonstrating significantly improved progression-free survival for dual checkpoint inhibition versus chemotherapy, adding Opdivo + Yervoy to pembrolizumab as approved first-line options for the approximately 4% of metastatic colorectal cancer patients with MSI-H tumors.

- In March 2025, Sun Pharmaceutical Industries completed the acquisition of U.S.-based Checkpoint Therapeutics for USD 355 million, obtaining commercial rights to cosibelimab—an anti-PD-L1 monoclonal antibody FDA-approved in December 2024 for metastatic or locally advanced cutaneous squamous cell carcinoma—marking the first major Indian pharmaceutical company's entry into the commercial ICI market and adding an approved ICI to Sun Pharma's U.S. specialty oncology portfolio.

Competitive Landscape Overview

The immune checkpoint inhibitor market is highly consolidated at the top, with Merck & Co., Bristol-Myers Squibb, AstraZeneca, and Roche collectively holding approximately 90% of global ICI revenues in 2025. Merck alone commands approximately 41.2% market share through KEYTRUDA's position as the market-defining product across more than 40 approved indications—a breadth of clinical validation that no single competing product matches. The competitive structure is shaped by the sequential nature of ICI approval economics: each new indication generates a distinct prescribable patient population, and companies that accumulate the most indication breadth create compounding revenue annuities from the same underlying molecule.

The competitive dynamic is bifurcating along two axes. The primary axis is KEYTRUDA lifecycle management versus competitive erosion: Merck's 2028 U.S. patent expiry for pembrolizumab will open the door to biosimilar entry, and the company's more than 30 active Phase 3 trials are explicitly designed to establish combination regimen standards of care that will create clinical hurdles for biosimilar substitution in the combination context even when the pembrolizumab component faces biosimilar competition. The secondary axis is subcutaneous formulation competition: Opdivo Qvantig's December 2024 first-mover advantage as the first approved SC PD-1 inhibitor provided BMS a 9-month head start before subcutaneous pembrolizumab's September 2025 approval. Both formulations use Halozyme Therapeutics' ENHANZE recombinant human hyaluronidase technology and are priced at parity with their IV equivalents, meaning the subcutaneous competition will be driven by clinician and patient preference for administration convenience rather than price.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product(s) | Geo Strength | Recent Strategic Move |

| Merck & Co., Inc. (MSD) | USA (Rahway, NJ) | Leader | KEYTRUDA® (pembrolizumab) PD-1 inhibitor; subcutaneous KEYTRUDA (pembrolizumab + berahyaluronidase alfa-pmph) | Global (>40% market share) | FDA approved subcutaneous pembrolizumab on September 19, 2025; full-year 2024 KEYTRUDA sales reached USD 29.5 billion, 18% year-over-year growth; 30+ Phase 3 combination trials ongoing as of Q1 2026 |

| Bristol-Myers Squibb Company | USA (Princeton, NJ) | Leader | Opdivo® (nivolumab IV); Opdivo Qvantig™ (SC nivolumab + hyaluronidase); Opdualag™ (nivolumab + relatlimab); Yervoy® (ipilimumab) | Global | FDA approved Opdivo Qvantig (first SC PD-1 inhibitor) on December 27, 2024; Q2 2025 Opdivo global sales USD 2.56B (+7% YoY); Opdualag holding ~30% market share in first-line melanoma |

| AstraZeneca PLC | UK (Cambridge) | Challenger | Imfinzi® (durvalumab) PD-L1 inhibitor; Imjudo® (tremelimumab) CTLA-4 inhibitor | Global (strong in lung cancer, SCLC, GI) | FDA approved Imfinzi + FLOT for resectable gastric/GEJ cancer (MATTERHORN trial, 2025); EU approved Imfinzi for resectable NSCLC (AEGEAN trial, 2025); Imfinzi standard of care in Stage III NSCLC globally |

| F. Hoffmann-La Roche Ltd. | Switzerland (Basel) | Challenger | Tecentriq® (atezolizumab) PD-L1 inhibitor; subcutaneous Tecentriq approved September 2021 | Global (strong in NSCLC, SCLC, TNBC) | Focused on maintaining Tecentriq indications following voluntary withdrawal of prior-platinum bladder cancer indication; atezolizumab + bevacizumab combination sustained in hepatocellular carcinoma; SC formulation expanding community oncology access |

| Regeneron Pharmaceuticals + Sanofi | USA/France | Challenger | Libtayo® (cemiplimab-rwlc) PD-1 inhibitor for CSCC, BCC, NSCLC, cervical cancer | USA (Regeneron primary), Europe (Sanofi) | Expanding Libtayo approvals into esophageal squamous cell carcinoma and additional solid tumors; building combination data with REGN4461 in immuno-oncology pipeline |

| GlaxoSmithKline plc (GSK) | UK (London) | Challenger | Jemperli® (dostarlimab-gxly) PD-1 inhibitor for dMMR/MSI-H endometrial cancer and solid tumors | North America, Europe | Dostarlimab expanding into colorectal cancer clinical trials; collaboration with Merck KGaA on cervical cancer; Jemperli plus chemotherapy approved for dMMR/MSI-H endometrial carcinoma in 2021 and confirmed indication |

| BeiGene Ltd. | China/USA | Niche Player | Tevimbra® (tislelizumab) PD-1 inhibitor; approved in China for 14+ indications; FDA approved for esophageal SCC November 2023 | China (dominant), expanding globally | Tislelizumab broadening U.S. label through additional indication submissions; multiple Phase 3 trials in NSCLC, gastric cancer, and NPC; positioned as first major domestic Chinese ICI with U.S. market access |

| Sun Pharmaceutical Industries Ltd. | India (Mumbai) | Niche Player | COSIBELIMAB (PD-L1 inhibitor for CSCC, approved 2024 via Checkpoint Therapeutics acquisition) | USA, India, emerging markets | In March 2025, completed acquisition of Checkpoint Therapeutics for USD 355 million, obtaining cosibelimab (anti-PD-L1) approved by FDA in December 2024 for metastatic or locally advanced CSCC |

By Type

PD-1 inhibitors dominated the immune checkpoint inhibitor market with approximately 57.0–70.0% revenue share in 2025, generating approximately USD 33.1–40.6 billion, because PD-1 represents the final common pathway through which most solid tumor types suppress T-cell cytotoxicity, making PD-1 blockade effective across a wider range of cancer histologies than any other single checkpoint target. Pembrolizumab holds the commercial leadership position with FDA approval across melanoma, NSCLC, head and neck squamous cell carcinoma, urothelial carcinoma, colorectal cancer (MSI-H), gastric and gastroesophageal junction cancer, esophageal cancer, cervical cancer, hepatocellular carcinoma, Merkel cell carcinoma, endometrial carcinoma, biliary tract cancer, triple-negative breast cancer, and multiple myeloma in combination regimens. Nivolumab maintains the second-largest PD-1 position with comparable indication breadth and a strong combination history with ipilimumab (CheckMate series). The subcutaneous formulation transition is occurring fastest in the PD-1 inhibitor class: both SC nivolumab (December 2024) and SC pembrolizumab (September 2025) achieved approval in the trailing 12 months, and Mordor Intelligence estimates the subcutaneous route will grow at a 25.4% CAGR through 2031 as infusion chair availability constraints at community oncology practices resolve through SC adoption.

PD-L1 inhibitors held approximately 20.0–25.0% revenue share in 2025 at approximately USD 11.6–14.5 billion. Durvalumab (Imfinzi, AstraZeneca) is the PD-L1 class leader following KEYTRUDA's PD-1 dominance, with its standard-of-care position in Stage III NSCLC following chemoradiotherapy (PACIFIC trial, establishing the concept of checkpoint consolidation after CRT) and its expanding GI oncology portfolio including cholangiocarcinoma, HCC, gastric cancer, and small cell lung cancer. Atezolizumab (Tecentriq, Roche) is losing ground: while it retains approvals in NSCLC, SCLC, and triple-negative breast cancer, the voluntary withdrawal of its bladder cancer indication and increasing competition from pembrolizumab and durvalumab in its remaining indications have reduced Tecentriq's growth trajectory. Avelumab (Bavencio, Merck KGaA/Pfizer) maintains its first-line maintenance indication in locally advanced or metastatic urothelial carcinoma following platinum-based chemotherapy, a relatively narrow but defensible niche. Cosibelimab (Sun Pharma/Checkpoint Therapeutics), FDA-approved in December 2024 for cutaneous squamous cell carcinoma, adds a new entry-point for PD-L1 inhibitors in dermatological oncology. CTLA-4 inhibitors (ipilimumab, tremelimumab) held approximately 5–8% revenue share, with ipilimumab's value concentrated in combination regimens with nivolumab in renal cell carcinoma, NSCLC, and colorectal cancer, and tremelimumab used in the STRIDE regimen with durvalumab for HCC and metastatic NSCLC.

By Indication

Non-small cell lung cancer accounted for approximately 26.3% of ICI market revenue in 2025 at approximately USD 15.3 billion, reflecting pembrolizumab's position as first-line standard of care in the largest single oncology indication globally. The WHO Global Cancer Observatory recorded approximately 2.21 million new NSCLC cases worldwide in 2022, with approximately 75% presenting at stages III–IV where systemic therapy including immunotherapy is the primary treatment approach. The first-line NSCLC opportunity is bifurcated by PD-L1 expression: patients with tumor proportion score (TPS) of 50% or greater receive pembrolizumab monotherapy, while those with lower PD-L1 expression receive pembrolizumab or atezolizumab in combination with platinum-doublet chemotherapy. The small cell lung cancer (SCLC) indication is the fastest-growing single indication within the ICI market at approximately 22.5% CAGR, driven by durvalumab's first-line extensive-stage SCLC approval and its 2025 ADRIATIC trial results in limited-stage SCLC demonstrating a 27% reduction in risk of death versus placebo, with estimated median overall survival of 55.9 months versus 33.4 months.

Melanoma retains the second-largest indication share at approximately 15–18% of ICI revenue, anchored by the dual checkpoint combination of ipilimumab plus nivolumab (CheckMate-067) which established durable 10-year overall survival rates of approximately 50% in advanced melanoma—the longest published survival data for any immunotherapy regimen in a solid tumor. Opdualag (nivolumab + relatlimab) achieved approximately 30% market share as a standard-of-care in first-line melanoma as of Q1 2025 BMS disclosures, carving share from both PD-1 monotherapy and dual checkpoint nivolumab + ipilimumab regimens with a more favorable safety profile. Renal cell carcinoma represents the third-largest indication, with ICI-based doublets—nivolumab + ipilimumab (CheckMate-214), pembrolizumab + axitinib (KEYNOTE-426), and nivolumab + cabozantinib—supplanting sunitinib as the first-line standard of care. Bladder and urothelial cancers, colorectal cancer (MSI-H subtype), hepatocellular carcinoma, and gastric cancer collectively represent emerging high-growth indications where ICI adoption is still below its potential market penetration rate relative to eligible patient populations.

By Route of Administration

Intravenous infusion generated approximately 67.95% of ICI market revenue in 2025 at approximately USD 39.5 billion, reflecting the historical development pathway of all currently approved ICIs as IV formulations and the infrastructure investment in infusion centers within hospital oncology units and cancer centers. IV administration protocols for ICI agents typically require 30–60 minute infusion sessions every 3–6 weeks, consuming infusion chair time that represents a significant healthcare resource constraint in high-volume oncology centers. The IV segment will continue to dominate through the forecast period in absolute revenue terms, but its percentage share will decline as subcutaneous conversion proceeds across approved PD-1 inhibitors. Subcutaneous administration represented approximately 5–8% of ICI revenue in 2025 following Opdivo Qvantig's December 2024 approval, but is forecast to grow at a 25.4% CAGR through 2031, driven by three structural advantages: a 3–5 minute administration time versus 30 minutes for IV, the possibility of community oncology and primary care delivery, and patient preference for less invasive administration. The device innovation pipeline—including autoinjector-compatible SC ICI formats—could ultimately enable patient self-administration from home settings, representing a paradigm-shifting access expansion for maintenance ICI therapy in adjuvant settings where treatment courses last 12 months or longer.

Regional Analysis

North America held a 41.0% share of the immune checkpoint inhibitor market in 2025 at approximately USD 23.8 billion, with the United States contributing more than 95% of regional revenues. The U.S. market benefits from the world's highest oncology drug pricing environment: KEYTRUDA's U.S. list price for the 400 mg/6-week cycle is approximately USD 15,000, compared to approximately USD 5,000–8,000 in major European markets following AMNOG assessment negotiations and HTA-driven reductions. Medicare Part B covers physician-administered ICI infusions and the new subcutaneous ICI formulations under specific J-Codes, with Opdivo Qvantig receiving a permanent J-Code by July 1, 2025 as BMS disclosed in Q1 2025 investor materials. The FDA's active engagement with ICI regulatory science—including 8–12 new ICI approvals or supplemental approvals per year—ensures a steady cadence of indication expansions that maintain U.S. market dominance. Merck's 2025 annual R&D investment of approximately USD 17.8 billion, directed substantially toward KEYTRUDA lifecycle management and combination development, anchors North America's innovation lead. North America is expected to maintain its position at approximately 40% market share through 2034.

Europe held approximately 26.5% of ICI market revenue in 2025 at approximately USD 15.4 billion, with Germany, France, the United Kingdom, and Italy as the primary demand centers. The European Medicines Agency's (EMA) CHMP reviews ICI marketing authorization applications typically 6–12 months after FDA approvals, with accelerated assessment available for products meeting unmet need criteria. National health technology assessment bodies—Germany's IQWIG under AMNOG, France's HAS, England's NICE, and Italy's AIFA—independently assess ICI comparative effectiveness versus standard of care to determine reimbursement eligibility and negotiated prices, creating market access timelines 12–24 months longer than the U.S. for each new indication. Despite this access delay, European ICI volume is sustained by the EMA's conditional marketing authorization pathway for oncology products meeting unmet need, and by pan-European clinical trial networks (EORTC, ESMO) generating ICI indication-expanding data. AstraZeneca received EU approval for Imfinzi in resectable NSCLC (AEGEAN trial) and a CHMP positive opinion for Imfinzi in limited-stage SCLC (ADRIATIC trial) in 2025, expanding its European ICI franchise.

Asia Pacific represented approximately 24.0% of market revenue in 2025 at approximately USD 13.9 billion and is the fastest-growing region at an estimated 19.56% CAGR through 2031. China is the critical growth engine: rising cancer incidence (China reported approximately 4.82 million new cancer cases in 2022 per the National Cancer Center), increasing ICI inclusion in the National Reimbursement Drug List following price negotiation with the National Healthcare Security Administration, and the proliferation of domestic ICI manufacturers (BeiGene's tislelizumab, Innovent Biologics' sintilimab, Junshi Biosciences' toripalimab) competing on price below Merck and BMS list prices, collectively expanding ICI treatment volumes. Japan's PMDA has approved pembrolizumab and nivolumab across comparable indication portfolios to the FDA, supported by Japanese Cancer Society guidelines recommending ICI-based first-line regimens in multiple tumor types. India and South Korea are the secondary Asia Pacific growth markets, with India's rapidly expanding oncology treatment infrastructure and South Korea's both advanced domestic ICI manufacturers and strong clinical trial participation driving regional momentum.

Latin America contributed approximately 5.8% of market revenue in 2025 at approximately USD 3.4 billion, led by Brazil, Mexico, and Argentina. The Pan American Health Organization (PAHO) data confirm cancer as the second leading cause of death across the region, with breast cancer and cervical cancer—both ICI-addressable indications—among the highest burden tumor types. Regulatory agency ANVISA (Brazil) and COFEPRIS (Mexico) have both approved the major ICIs, but affordability constraints and government procurement negotiation timelines limit access to populations served by private insurance rather than public health systems. The Middle East and Africa region contributed approximately 2.7% of revenue in 2025, primarily through Gulf Cooperation Council countries' advanced oncology centers and South Africa's National Health Insurance pharmaceutical coverage program.

Country Analysis

The United States immune checkpoint inhibitor market reached approximately USD 22.7 billion in 2025, growing at a country-level CAGR of approximately 16.0% through 2034, with the market projected to exceed USD 76.9 billion by 2034 based on the Precedence Research estimate for the U.S. market. The U.S. market's dominance reflects three interconnected structural advantages: pricing power (U.S. payer reimbursement occurs at or near list prices absent mandatory price controls, unlike European HTA-negotiated prices), indication breadth (FDA approves ICI indications 6–18 months before EMA, creating first-to-market commercial windows), and healthcare expenditure scale (U.S. healthcare spending is projected to surpass USD 4.5 trillion by 2024, with oncology representing the largest disease category by spending). The National Cancer Institute estimated approximately 1.9 million new cancer diagnoses in the U.S. for 2024, generating a continuously replenishing eligible patient pool. Merck's FDA filings for 30+ KEYTRUDA combination regimens ensure a pipeline of U.S. indication expansions that will sustain domestic market growth through the 2028 patent expiry inflection point.

Germany's immune checkpoint inhibitor market reached approximately USD 3.9 billion in 2025, growing at an estimated CAGR of approximately 14.5%, making it the largest single European ICI market at approximately 28.9% of regional revenues. Germany's AMNOG early benefit assessment process compares ICIs against the appropriate comparator therapy (standardized care) to determine added benefit classification, which directly determines the price negotiated with the Central Federal Union of Health Insurance Funds (GKV-Spitzenverband). Pembrolizumab has received considerable added benefit designations across its NSCLC and melanoma indications in Germany, supporting above-reference pricing in those settings. AstraZeneca's Imfinzi holds a distinctive German market position through its Stage III NSCLC standard-of-care designation following the PACIFIC trial, which demonstrated overall survival benefit in a setting where no prior systemic therapy had achieved OS improvement. Japan's ICI market reached approximately USD 3.5 billion in 2025, growing at an estimated CAGR of 15.8%, with pembrolizumab and nivolumab as the primary products across gastric cancer (a leading cancer burden in Japan), NSCLC, and MSI-H solid tumors. China's ICI market reached approximately USD 5.8 billion in 2025, growing at approximately 22.5% CAGR—the highest single-country growth rate globally—as National Reimbursement Drug List inclusions for pembrolizumab and nivolumab at significantly negotiated prices increase prescription volumes that offset per-unit price reductions.

The United Kingdom's ICI market reached approximately USD 3.1 billion in 2025, growing at an estimated CAGR of approximately 13.5%, with NICE positive technology appraisals covering pembrolizumab, nivolumab, and atezolizumab across their approved NSCLC, melanoma, and urothelial cancer indications. AstraZeneca's Cambridge base and the UK's Medicines and Healthcare products Regulatory Agency (MHRA)'s independence from EMA post-Brexit have created a distinctive UK regulatory environment where MHRAapprovals for major ICIs follow FDA timelines rather than EMA timelines in some cases, potentially shortening UK market access versus continental Europe. India's ICI market reached approximately USD 780 million in 2025, growing at approximately 20.5% CAGR, driven primarily by private healthcare utilization as KEYTRUDA and Opdivo remain above government health scheme coverage thresholds; India's Cancer Drugs Fund equivalent and hospital-based oncology network expansion are the primary volume drivers.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Type

- PD-1 Inhibitors

- PD-L1 Inhibitors

- CTLA-4 Inhibitors

- Others

By Indication

- Lung Cancer

- Melanoma

- Renal Cell Carcinoma

- Others

By Route of Administration

- Intravenous

- Subcutaneous

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 58.0 B |

| Forecast Revenue (2034) | USD 229.6 B |

| CAGR (2025-2034) | 16.5% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (PD-1 Inhibitors, PD-L1 Inhibitors, CTLA-4 Inhibitors, Others), By Indication, (Lung Cancer, Melanoma, Renal Cell Carcinoma, Others), By Route of Administration, (Intravenous, Subcutaneous, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MERCK & CO., INC. (MSD), BRISTOL-MYERS SQUIBB COMPANY, ASTRAZENECA PLC, F. HOFFMANN-LA ROCHE LTD. (GENENTECH, INC.), REGENERON PHARMACEUTICALS, INC., SANOFI S.A., GLAXOSMITHKLINE PLC (GSK), BEIGENE LTD., SUN PHARMACEUTICAL INDUSTRIES LTD., INNOVENT BIOLOGICS, INC., JUNSHI BIOSCIENCES CO., LTD., MERCK KGAA (EMD SERONO), PFIZER INC., INCYTE CORPORATION, IMMUTEP LIMITED, ELI LILLY AND COMPANY, NOVARTIS AG, ONO PHARMACEUTICAL CO., LTD., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Indication (Lung Cancer, Melanoma, Renal Cell Carcinoma), By Route (Intravenous, Subcutaneous) Region, Key Players – Dynamics, Immuno-Oncology Monoclonal Antibodies & Target Tumor Immunotherapy Pipelines, Growth Opportunities Trends & Forecast 2026-2034")

, By Indication (Lung Cancer, Melanoma, Renal Cell Carcinoma), By Route (Intravenous, Subcutaneous) Region, Key Players – Dynamics, Immuno-Oncology Monoclonal Antibodies & Target Tumor Immunotherapy Pipelines, Growth Opportunities Trends & Forecast 2026-2034")

, By Indication (Lung Cancer, Melanoma, Renal Cell Carcinoma), By Route (Intravenous, Subcutaneous) Region, Key Players – Dynamics, Immuno-Oncology Monoclonal Antibodies & Target Tumor Immunotherapy Pipelines, Growth Opportunities Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Immune Checkpoint Inhibitor Market?

Global Immune Checkpoint Inhibitor Market was valued at USD 50.1 billion in 2024 and is projected to reach USD 229.6 billion by 2034, at a CAGR of 16.5% during 2026–2034.

Who are the major players in the Immune Checkpoint Inhibitor Market?

MERCK & CO., INC. (MSD), BRISTOL-MYERS SQUIBB COMPANY, ASTRAZENECA PLC, F. HOFFMANN-LA ROCHE LTD. (GENENTECH, INC.), REGENERON PHARMACEUTICALS, INC., SANOFI S.A., GLAXOSMITHKLINE PLC (GSK), BEIGENE LTD., SUN PHARMACEUTICAL INDUSTRIES LTD., INNOVENT BIOLOGICS, INC., JUNSHI BIOSCIENCES CO., LTD., MERCK KGAA (EMD SERONO), PFIZER INC., INCYTE CORPORATION, IMMUTEP LIMITED, ELI LILLY AND COMPANY, NOVARTIS AG, ONO PHARMACEUTICAL CO., LTD., OTHERS

Which segments covered the Immune Checkpoint Inhibitor Market?

By Type, (PD-1 Inhibitors, PD-L1 Inhibitors, CTLA-4 Inhibitors, Others), By Indication, (Lung Cancer, Melanoma, Renal Cell Carcinoma, Others), By Route of Administration, (Intravenous, Subcutaneous, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Immune Checkpoint Inhibitor Market

Published Date : 18 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date