- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global In-Memory Computing Market Size, Share & Forecast | CAGR 17.4%

Global In-Memory Computing Market Size, Share Analysis By Component (Solutions, Services), By Deployment (Cloud, On-Premises, Hybrid, Multi-Cloud, Edge), By Application (Analytics, BI, AI/ML, Fraud Detection, Trading, IoT, ERP/CRM), By Vertical (BFSI, IT & Telecom, Retail, Healthcare, Manufacturing, Government), By Memory (DRAM, SRAM, NVM, Persistent, SCM, HBM) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 17.40 Billion | USD 73.50 Billion | 17.4% | North America, 37.0% |

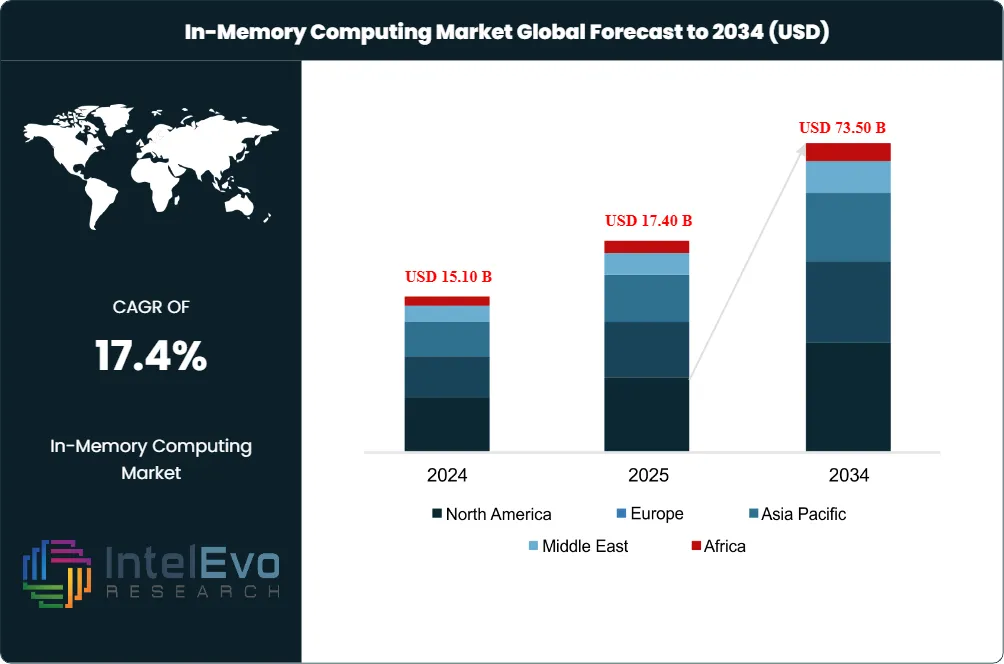

The In-Memory Computing Market was valued at USD 15.10 Billion in 2024 and USD 17.40 Billion in 2025. The market is projected to reach USD 73.50 Billion by 2034, expanding at a CAGR of 17.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 56.10 Billion over the analysis period. Demand is driven by AI workload acceleration, sub-millisecond latency requirements at fraud-detection and personalization engines, and continuous DRAM-and-storage-class-memory price improvements that allow larger datasets to remain in main memory.

Get More Information about this report -

Request Free Sample ReportThe in-memory computing market is anchored by SAP HANA Cloud, Oracle Database In-Memory, IBM Db2 with BLU Acceleration, Redis Enterprise, Hazelcast Platform, and GridGain Platform 9.1 (general availability May 2025). Compute Express Link (CXL) memory disaggregation, ferroelectric HfO2 DRAM+ research, and Storage Class Memory (SCM) pricing trajectories are reshaping the underlying hardware fabric. CXL-enabled disaggregated memory clusters allow capacity additions at near-DRAM bandwidth, while SCM products from Samsung, Micron, and SK hynix narrow the cost gap with NAND.

Cloud and SaaS deployment held the largest 2025 share at approximately 71.5% of revenue, expanding at a 27.6% CAGR through 2030. AWS ElastiCache, Azure Cache for Redis, Google Cloud Memorystore, and Oracle Cloud Infrastructure HeatWave anchor the cloud segment. In-memory data management platforms captured 62% of 2024 revenue, with banks migrating core analytics workloads and reporting query latency cuts of 20 to 40 milliseconds. In-memory application platforms are forecast to grow at 22.4% CAGR through 2030 because digital-native firms design real-time microservices around memory-resident state.

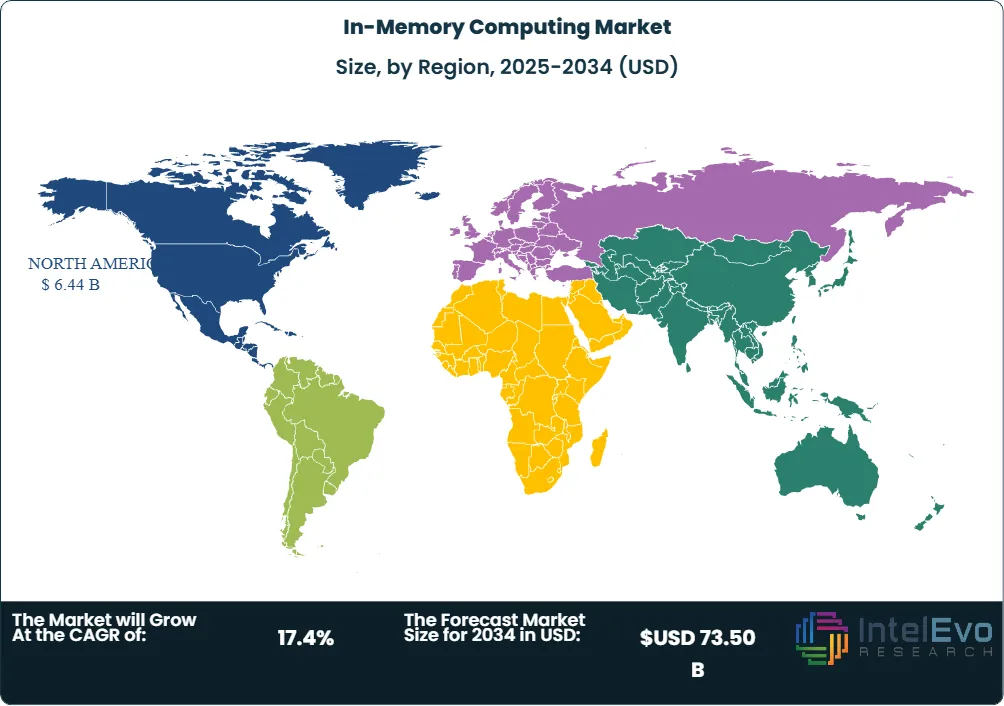

North America led the in-memory computing market with approximately 37.0% revenue share in 2025, equivalent to roughly USD 6.44 Billion in regional revenue, anchored by Oracle (Austin), Microsoft (Redmond), IBM (Armonk), Redis Inc. (Mountain View), and the Banking, Financial Services, and Insurance (BFSI) end-user concentration. Europe held 27% share through SAP SE (Walldorf), Software AG (Darmstadt), and Exasol AG (Nuremberg) headquarters and EUR-denominated enterprise license commitments. Asia Pacific captured 22% share and is forecast as the fastest-growing region at a 20.9% CAGR through 2030. MariaDB's March 2026 agreement to acquire GridGain Systems and Redis's September 2025 acquisition of Decodable redrew the competitive map at year-end 2025 through Q1 2026.

Market Definition & Scope

The in-memory computing market is defined as the global commercial activity covering software platforms, databases, data grids, application servers, and managed services that store and process working datasets in main memory (DRAM, persistent memory, and storage-class memory) rather than disk-based storage. The market includes in-memory databases (SAP HANA, Oracle TimesTen, SingleStore), in-memory data grids (Hazelcast, GridGain, Apache Ignite), distributed caches (Redis, Memcached, AWS ElastiCache), and in-memory application platforms (SAP HANA Cloud, Oracle Coherence).

This analysis includes ACID-compliant in-memory transaction processing, hybrid transactional and analytical processing (HTAP) platforms, and real-time stream-processing engines that maintain materialized state in memory. Excluded are general-purpose RAM hardware sales without in-memory software functionality, traditional disk-based databases without in-memory acceleration features, classical caching libraries embedded inside larger software products, and pure compute-in-memory hardware research before commercialization. The in-memory computing market sits within the broader data management software parent market, capturing real-time and AI-acceleration workloads as the highest-value tier.

, By Deployment (Cloud, On-Premises, Hybrid, Multi-Cloud, Edge), By Application (Analytics, BI, AI/ML, Fraud Detection, Trading, IoT, ERP/CRM), By Vertical (BFSI, IT & Telecom, Retail, Healthcare, Manufacturing, Government), By Memory (DRAM, SRAM, NVM, Persistent, SCM, HBM) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The in-memory computing market grew from USD 17.40 Billion in 2025 toward a forecast value of USD 73.50 Billion by 2034 at a 17.4% CAGR.

- Segment Dominance: In-memory data management platforms captured approximately 62% revenue share in 2024, anchored by SAP HANA, Oracle Database In-Memory, and IBM Db2 with BLU Acceleration.

- Segment Dominance: Cloud and SaaS deployment held 71.5% of 2024 revenue, expanding at a 27.6% CAGR through 2030 versus 8% for on-premises installations.

- Driver: Real-time analytics is the primary driver, capturing 48.3% of 2024 revenue, with 58% of organizations prioritizing sub-second latency per recent enterprise survey data.

- Restraint: DRAM price spikes of 50% in early 2025 raised total cost of ownership for large clusters, delaying refresh cycles for memory-intensive workloads.

- Opportunity: IoT and edge stream processing represents the largest forecast-period opportunity, expanding at a 31% CAGR through 2030 driven by sovereign-AI regulations steering inference to national boundaries.

- Trend: AI agent and vector-search workloads now define new platform requirements, with Redis launching Redis for AI managed semantic caching in September 2025.

- Regional: North America led with 37.0% share in 2025 equivalent to roughly USD 6.44 Billion, while Asia Pacific is the fastest-growing region at a 20.9% forecast CAGR through 2030.

Key Insights Summary

- MariaDB plc agreed to acquire GridGain Systems in March 2026 to combine relational database technology with Apache Ignite-based in-memory computing, targeting AI latency in agentic applications.

- Redis Ltd. acquired Decodable, a real-time data platform, in September 2025 alongside Redis for AI updates including managed semantic caching for AI agents.

- GridGain announced general availability of GridGain Platform 9.1 in May 2025, with enhanced support for real-time hybrid analytical and transactional processing for AI and analytics workloads.

- Exasol AG partnered with MariaDB in October 2025 to deliver MariaDB Exa, a unified analytics offering pairing the Exasol engine with a cloud database platform for generative AI workloads.

- SAP HANA 2.0 reached SPS 08 in early 2026 per SAP product disclosure, continuing biannual support package stack updates since the December 2016 SAP HANA 2.0 release.

- Microsoft and Singtel announced a March 2025 partnership integrating Azure services with Singtel 5G and edge infrastructure across Singapore and broader Asia Pacific markets for ultra-low-latency in-memory analytics.

- BFSI commanded approximately 29.4% of 2024 in-memory computing spending, anchored by fraud-detection, personalization, and risk-engine workloads at JPMorgan Chase, Goldman Sachs, and HSBC.

Competitive Landscape Overview

The in-memory computing market is moderately consolidated, with the top four vendors (SAP SE, Oracle Corporation, Microsoft Corporation, and IBM Corporation) collectively representing an estimated 52 to 58% of 2025 revenue. SAP holds the leading position through SAP HANA installed at over 50,000 customers globally, including most Fortune 500 manufacturers. Oracle anchors transactional in-memory through Oracle Database In-Memory, TimesTen, and the MySQL HeatWave service. Microsoft drives cloud-native in-memory adoption through Azure Cache for Redis and SQL Server In-Memory OLTP. IBM Db2 with BLU Acceleration and Redis on IBM Cloud round out the leadership tier.

Competitive evolution centers on three axes: AI-workload acceleration, hybrid transactional-analytical processing (HTAP) capability, and consumption-based pricing flexibility. Redis Ltd. expanded its competitive position through the September 2025 Decodable acquisition and Redis for AI semantic caching launch, targeting AI-agent context-and-memory workloads. MariaDB plc's March 2026 agreement to acquire GridGain Systems consolidated open-source relational and Apache Ignite-based in-memory technology. Hazelcast Inc., GigaSpaces Technologies, and SingleStore round out the second tier with focused HTAP and stream-processing offerings. Strategic moves through 2025 included Microsoft-Singtel Asia Pacific partnership, Exasol-MariaDB MariaDB Exa launch, and continued IBM-NTT DATA hybrid cloud collaboration in Asia Pacific.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| SAP SE | Germany | Leader | SAP HANA Cloud, SAP HANA 2.0 SPS 08 | Europe, North America | Dec 2024 released SAP HANA Cloud major updates |

| Oracle Corporation | USA | Leader | Oracle Database In-Memory, TimesTen, HeatWave | North America, Europe | 2025 expanded MySQL HeatWave AutoML in OCI |

| Microsoft Corporation | USA | Leader | Azure Cache for Redis, SQL Server In-Memory OLTP | North America, Asia Pacific | Mar 2025 partnered with Singtel for Azure 5G edge |

| IBM Corporation | USA | Leader | IBM Db2 with BLU, Redis on IBM Cloud | North America, Europe | Continued NTT DATA partnership through 2025 |

| Redis Ltd. | USA | Challenger | Redis Enterprise, Redis Cloud, Redis for AI | North America, Europe | Sep 2025 acquired Decodable real-time data platform |

| GridGain Systems Inc. | USA | Challenger | GridGain Platform 9.1, Apache Ignite | North America | Mar 2026 MariaDB agreed to acquire GridGain |

| Hazelcast Inc. | USA | Challenger | Hazelcast Platform, IMDG, Jet stream | North America, Europe | Continued Apache Kafka integration through 2025 |

| Exasol AG | Germany | Niche Player | Exasol analytics database, MariaDB Exa | Europe | Oct 2025 partnered with MariaDB for MariaDB Exa |

| TIBCO Software Inc. | USA | Niche Player | TIBCO Data Virtualization, ActiveSpaces | North America, Europe | Continued Cloud Software Group integration through 2025 |

| Software AG | Germany | Niche Player | Adabas, Terracotta BigMemory | Europe | 2025 continued IBM acquisition integration phase |

Segmentation Analysis

The in-memory computing market is segmented by component, deployment mode, application, end-user vertical, and memory technology, each producing distinct competitive and adoption patterns across the forecast period.

By Component

In-memory data management platforms captured approximately 62% of in-memory computing market revenue in 2024, anchored by ACID-compliant drop-in replacements for entrenched databases at banks and large enterprises. SAP HANA, Oracle Database In-Memory, IBM Db2 with BLU Acceleration, and Microsoft SQL Server In-Memory OLTP dominate this segment with multi-million-dollar annual license commitments. In-memory application platforms held the second-largest share and are forecast to grow at 22.4% CAGR through 2030, the fastest segment, propelled by digital-native firms designing real-time microservices around memory-resident state. Services revenue covering implementation, custom HANA modeling, and managed cloud operations completes the component mix.

By Deployment Mode

Cloud and SaaS deployment captured approximately 71.5% of in-memory computing market revenue in 2024 because hyperscaler economics and consumption-based pricing align with enterprise procurement preferences. AWS ElastiCache, Azure Cache for Redis, Google Cloud Memorystore, and Oracle Cloud Infrastructure HeatWave anchor the cloud segment. Hyperscalers now expose serverless in-memory services that scale instantly. On-premises deployment retains approximately 28.5% revenue share, dominated by financial-services workloads with data-residency constraints and SAP HANA installations on certified hardware. Cloud is forecast to expand at a 27.6% CAGR through 2030 versus single-digit on-premises growth, driven by 35 to 50% lower total cost of ownership over five years.

By Application

Real-time analytics captured 48.3% of in-memory computing market revenue in 2024, the largest application segment, addressing fraud detection, personalization, ad-tech, and telemetry analytics. Risk management and fraud detection accounted for approximately 26.4% of 2025 spending across BFSI, with rising cyberattack frequency requiring proactive threat mitigation. Data processing and management held the third-largest share, anchored by extract-transform-load acceleration and operational reporting. IoT and edge stream processing is forecast to grow at a 31% CAGR through 2030, the fastest application segment, propelled by manufacturing telemetry, smart-city deployments, and autonomous-vehicle data fabrics. Implementation timelines for production in-memory analytics deployments typically run 6 to 12 months.

By End-User Vertical

Banking, Financial Services, and Insurance (BFSI) commanded approximately 29.4% of in-memory computing market spending in 2024, the largest end-user vertical, anchored by JPMorgan Chase, Goldman Sachs, HSBC, Banco Santander, and BNP Paribas fraud-detection and risk-engine workloads. Retail and e-commerce held 18% share, growing at a 14.3% CAGR through forecast period driven by Walmart, Amazon, JD.com, and Target real-time inventory and personalization workloads. IT and telecom captured 16% share, anchored by hyperscaler internal use and 5G core-network telemetry. Healthcare and life sciences represented 11% share and is forecast as the fastest-growing vertical at 23.8% CAGR through 2030 because clinical decision support and genomics workloads benefit from sub-second latency. Manufacturing, government, transportation, and energy round out the remaining 25.6% demand.

By Memory Technology

DRAM accounted for approximately 66.7% of in-memory computing market revenue in 2024, the dominant memory technology, anchored by DDR5 server-grade modules from Samsung Electronics, Micron Technology, and SK hynix. Storage-Class Memory (SCM) including 3D XPoint legacy and successor products captured the second-largest share and is forecast to grow at a 29.5% CAGR through 2030. Compute Express Link (CXL) memory expansion modules represent an emerging share, with CXL 2.0 and CXL 3.0 deployments shipping through 2025 and 2026 from AMD, Intel, Samsung, and Micron. Ferroelectric HfO2 DRAM+ remains in research, targeting near-DRAM speed and non-volatility below 10 nm node geometry. ROI calculations for SCM-augmented deployments typically show 35 to 45% reduction in total cost of ownership versus all-DRAM configurations.

Regional Analysis

The global in-memory computing market shows distinct regional revenue and growth profiles across North America, Europe, Asia Pacific, Latin America, and Middle East and Africa, with North American hyperscaler concentration and European enterprise-license density driving the geographic mix in 2025.

North America

North America led the in-memory computing market with approximately 37.0% share in 2025, equivalent to roughly USD 6.44 Billion in regional revenue. The United States anchors regional demand at JPMorgan Chase, Goldman Sachs, BlackRock, Walmart, Amazon, Microsoft, and Google. Approximately 62% of large U.S. enterprises run in-memory workloads across fraud detection, personalization, and telemetry analytics per industry survey data. Vendor concentration includes Oracle (Austin), Microsoft (Redmond), IBM (Armonk), Redis Inc. (Mountain View), Hazelcast (San Mateo), GridGain (San Francisco Bay Area), and TIBCO (Palo Alto). Canada anchors regional supply through OpenText, while Mexico hosts regional in-memory deployments at FEMSA, BBVA Mexico, and CEMEX.

Europe

Europe held approximately 27% of in-memory computing market revenue in 2025, valued near USD 4.70 Billion. Germany leads regional demand and supply through SAP SE (Walldorf), Software AG (Darmstadt), Exasol AG (Nuremberg), and major industrial deployments at BMW, Volkswagen, Mercedes-Benz, BASF, and Siemens. The United Kingdom anchors financial-services demand at HSBC, Barclays, Lloyds, and Standard Chartered. France contributes through BNP Paribas, Societe Generale, and Atos Eviden enterprise deployments. The European Union General Data Protection Regulation (GDPR), the Digital Operational Resilience Act (DORA), and the EU AI Act collectively drive data-residency and explainability requirements that favor regional in-memory deployments.

Asia Pacific

Asia Pacific captured approximately 22% of in-memory computing market revenue in 2025, valued near USD 3.83 Billion, and is forecast as the fastest-growing region at a 20.9% CAGR through 2030. China leads regional demand through Alibaba Cloud, Tencent Cloud, JD.com, and ICBC fraud-detection workloads, with domestic vendors Huawei GaussDB, Alibaba PolarDB, and Tencent TDSQL providing localized supply. India anchors growing demand at Tata Consultancy Services, Infosys, HDFC Bank, ICICI Bank, and Reliance Jio. Japan supports demand at Toyota, Hitachi, NEC, and Mitsubishi UFJ Financial Group. South Korea contributes through Samsung Electronics, KISTI, and KB Kookmin Bank. Microsoft and Singtel's March 2025 partnership integrating Azure services with Singtel 5G and edge infrastructure across Singapore expanded regional access.

Latin America

Latin America accounted for approximately 7% of in-memory computing market revenue in 2025. Brazil leads regional adoption through Itau Unibanco, Banco do Brasil, Vale, and Petrobras enterprise deployments, with B3 stock exchange driving real-time market-data workloads. Mexico contributes through FEMSA, BBVA Mexico, CEMEX, and Banorte fraud-detection and inventory workloads. Argentina, Chile, and Colombia represent emerging demand pockets supported by mining, energy, and financial-services pilots. Regional growth is constrained by limited Spanish-language enterprise-support capacity and longer hyperscaler latency to U.S. data centers, although AWS Sao Paulo, Azure Brazil South, and Google Cloud Sao Paulo regions accelerate capacity additions through 2027.

Middle East & Africa

Middle East and Africa held approximately 7% of in-memory computing market revenue in 2025. The United Arab Emirates anchors regional demand through Emirates NBD, Etisalat, du, and Dubai Airports real-time-analytics workloads, with Vision 2030 sustainability mandates accelerating capacity additions. Saudi Arabia anchors demand through Saudi Aramco, STC, Al Rajhi Bank, and the Saudi National Bank. Israel contributes through Bank Leumi, Bank Hapoalim, and Teva Pharmaceutical Industries enterprise deployments. South Africa contributes through Standard Bank, ABSA Group, and MTN Group. Egypt and Nigeria represent emerging African demand nodes supported by mobile-banking and telecommunications carriers. The GCC in-memory computing market is forecast to reach USD 0.32 Billion in 2026 per regional analysis.

Country Analysis

United States

The United States in-memory computing market reached approximately USD 5.20 Billion in 2025, with country CAGR tracking near 17.5% through 2034. Demand concentrates at JPMorgan Chase, Goldman Sachs, Walmart, Amazon, Microsoft, Apple, and Procter & Gamble fraud-detection, real-time-analytics, and personalization workloads. Approximately 62% of large U.S. enterprises run in-memory workloads, with 48% reporting double-digit latency reductions after migration. The Federal Financial Institutions Examination Council (FFIEC) and the SEC cyber-disclosure requirements drive financial-services adoption. The CHIPS and Science Act allocated USD 52 Billion through fiscal year 2027 for domestic semiconductor manufacturing, indirectly supporting DRAM and SCM supply chain capacity at Micron and Intel.

Germany

Germany's in-memory computing market reached approximately USD 1.95 Billion in 2025, the largest single-country market within Europe with country CAGR near 16% through 2034. SAP SE (Walldorf) anchors domestic vendor supply alongside Software AG and Exasol AG. BMW, Volkswagen, Mercedes-Benz, BASF, Siemens, and Deutsche Bank drive demand-side adoption through SAP HANA Cloud, Oracle Database In-Memory, and Hazelcast deployments. The Lieferkettensorgfaltspflichtengesetz (LkSG) supply-chain due diligence law and the BAIT (Bankaufsichtliche Anforderungen an die IT) banking IT requirements drive financial-services and industrial in-memory adoption. The Federal Ministry for Economic Affairs and Climate Action funded data-driven manufacturing through GAIA-X initiatives extending through 2027.

China

China's in-memory computing market reached approximately USD 1.65 Billion in 2025, with country CAGR near 22% through 2034, the highest among major economies. Domestic vendors include Huawei GaussDB, Alibaba PolarDB-X, Tencent TDSQL, OceanBase (Ant Group), and TiDB (PingCAP) competing with international SAP HANA and Oracle Database deployments. Demand concentrates at Industrial and Commercial Bank of China, China Construction Bank, Ping An Insurance, Alibaba, Tencent, ByteDance, and JD.com. The Personal Information Protection Law (PIPL) and Data Security Law drive data-residency requirements favoring domestic vendors. China's 14th Five-Year Plan prioritizes domestic database and hardware capacity through Made in China 2025 industrial policy commitments.

Japan

Japan's in-memory computing market reached approximately USD 1.10 Billion in 2025, with country CAGR near 14% through 2034. Toyota Motor Corporation anchors automotive demand through SAP HANA-based connected-vehicle telemetry workloads, while Hitachi, Mitsubishi UFJ Financial Group, NEC, and Sony drive industrial and financial-services demand. Domestic vendors Fujitsu, NEC, and Hitachi compete with international platforms through localized integration services. The Japanese government's Society 5.0 initiative and METI Digital Transformation guidelines drive enterprise modernization budgets. The Act on the Protection of Personal Information (APPI) and the Financial Services Agency cyber-resilience guidelines support data-residency-led on-premises and Japan-region cloud deployments.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Component

- Solutions

- In-Memory Databases

- In-Memory Data Grids

- In-Memory Analytics Platforms

- In-Memory Computing Software

- Data Management and Integration Solutions

- Real-Time Processing Platforms

- Business Intelligence and Visualization Tools

- Others

- Services

- Consulting Services

- Implementation and Integration Services

- Managed Services

- Support and Maintenance Services

- Training and Professional Services

By Deployment Mode

- Cloud-Based Deployment

- On-Premises Deployment

- Hybrid Deployment

- Multi-Cloud Deployment

- Edge Deployment

- Others

By Application

- Real-Time Analytics

- Business Intelligence and Reporting

- Artificial Intelligence and Machine Learning

- Fraud Detection and Risk Management

- Customer Experience Management

- Predictive Analytics

- Financial Trading and Transaction Processing

- Supply Chain and Logistics Optimization

- IoT Data Processing and Analytics

- Database Acceleration

- Enterprise Resource Planning (ERP)

- Customer Relationship Management (CRM)

- Others

By End-User Vertical

- Banking, Financial Services, and Insurance (BFSI)

- Information Technology and Telecommunications

- Retail and E-Commerce

- Healthcare and Life Sciences

- Manufacturing

- Government and Public Sector

- Energy and Utilities

- Transportation and Logistics

- Media and Entertainment

- Automotive

- Education

- Others

By Memory Technology

- Dynamic Random Access Memory (DRAM)

- Static Random Access Memory (SRAM)

- Non-Volatile Memory (NVM)

- Persistent Memory

- Flash Memory

- Storage-Class Memory (SCM)

- High Bandwidth Memory (HBM)

- Hybrid Memory Architectures

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 17.40 B |

| Forecast Revenue (2034) | USD 73.50 B |

| CAGR (2025-2034) | 17.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Solutions, Services), By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment, Multi-Cloud Deployment, Edge Deployment, Others), By Application, (Real-Time Analytics, Business Intelligence and Reporting, Artificial Intelligence and Machine Learning, Fraud Detection and Risk Management, Customer Experience Management, Predictive Analytics, Financial Trading and Transaction Processing, Supply Chain and Logistics Optimization, IoT Data Processing and Analytics, Database Acceleration, Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Others), By End-User Vertical, (Banking, Financial Services, and Insurance (BFSI), Information Technology and Telecommunications, Retail and E-Commerce, Healthcare and Life Sciences, Manufacturing, Government and Public Sector, Energy and Utilities, Transportation and Logistics, Media and Entertainment, Automotive, Education, Others), By Memory Technology, (Dynamic Random Access Memory (DRAM), Static Random Access Memory (SRAM), Non-Volatile Memory (NVM), Persistent Memory, Flash Memory, Storage-Class Memory (SCM), High Bandwidth Memory (HBM), Hybrid Memory Architectures, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SAP SE, ORACLE CORPORATION, MICROSOFT CORPORATION, IBM CORPORATION, REDIS LTD., GRIDGAIN SYSTEMS INC., HAZELCAST INC., EXASOL AG, TIBCO SOFTWARE INC., SOFTWARE AG, GIGASPACES TECHNOLOGIES INC., AMAZON WEB SERVICES INC., GOOGLE LLC (ALPHABET INC.), SAMSUNG ELECTRONICS CO. LTD., MICRON TECHNOLOGY INC., SK HYNIX INC., SINGLESTORE INC., MARIADB PLC, ALTIBASE CORP., FUJITSU LIMITED, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud, On-Premises, Hybrid, Multi-Cloud, Edge), By Application (Analytics, BI, AI/ML, Fraud Detection, Trading, IoT, ERP/CRM), By Vertical (BFSI, IT & Telecom, Retail, Healthcare, Manufacturing, Government), By Memory (DRAM, SRAM, NVM, Persistent, SCM, HBM) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Deployment (Cloud, On-Premises, Hybrid, Multi-Cloud, Edge), By Application (Analytics, BI, AI/ML, Fraud Detection, Trading, IoT, ERP/CRM), By Vertical (BFSI, IT & Telecom, Retail, Healthcare, Manufacturing, Government), By Memory (DRAM, SRAM, NVM, Persistent, SCM, HBM) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Deployment (Cloud, On-Premises, Hybrid, Multi-Cloud, Edge), By Application (Analytics, BI, AI/ML, Fraud Detection, Trading, IoT, ERP/CRM), By Vertical (BFSI, IT & Telecom, Retail, Healthcare, Manufacturing, Government), By Memory (DRAM, SRAM, NVM, Persistent, SCM, HBM) Region & Key Players-Industry Segment Overview, Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the In-Memory Computing Market?

The Global In-Memory Computing Market was valued at USD 15.10 Billion in 2024 and USD 17.40 Billion in 2025, and is projected to reach USD 73.50 Billion by 2034, growing at a CAGR of 17.4% from 2026 to 2034. Market growth is driven by rising demand for real-time analytics, big data processing, and high-performance computing solutions.

Who are the major players in the In-Memory Computing Market?

SAP SE, ORACLE CORPORATION, MICROSOFT CORPORATION, IBM CORPORATION, REDIS LTD., GRIDGAIN SYSTEMS INC., HAZELCAST INC., EXASOL AG, TIBCO SOFTWARE INC., SOFTWARE AG, GIGASPACES TECHNOLOGIES INC., AMAZON WEB SERVICES INC., GOOGLE LLC (ALPHABET INC.), SAMSUNG ELECTRONICS CO. LTD., MICRON TECHNOLOGY INC., SK HYNIX INC., SINGLESTORE INC., MARIADB PLC, ALTIBASE CORP., FUJITSU LIMITED, Others

Which segments covered the In-Memory Computing Market?

By Component, (Solutions, Services), By Deployment Mode, (Cloud-Based Deployment, On-Premises Deployment, Hybrid Deployment, Multi-Cloud Deployment, Edge Deployment, Others), By Application, (Real-Time Analytics, Business Intelligence and Reporting, Artificial Intelligence and Machine Learning, Fraud Detection and Risk Management, Customer Experience Management, Predictive Analytics, Financial Trading and Transaction Processing, Supply Chain and Logistics Optimization, IoT Data Processing and Analytics, Database Acceleration, Enterprise Resource Planning (ERP), Customer Relationship Management (CRM), Others), By End-User Vertical, (Banking, Financial Services, and Insurance (BFSI), Information Technology and Telecommunications, Retail and E-Commerce, Healthcare and Life Sciences, Manufacturing, Government and Public Sector, Energy and Utilities, Transportation and Logistics, Media and Entertainment, Automotive, Education, Others), By Memory Technology, (Dynamic Random Access Memory (DRAM), Static Random Access Memory (SRAM), Non-Volatile Memory (NVM), Persistent Memory, Flash Memory, Storage-Class Memory (SCM), High Bandwidth Memory (HBM), Hybrid Memory Architectures, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date