- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Indonesia Joint Pain Injections Market Size, Share & Forecast | CAGR 12.30%

Indonesia Joint Pain Injections Market Size, Share & Growth Analysis By Product Type (Corticosteroid Injections, Hyaluronic Acid Injections, Platelet-Rich Plasma (PRP) Injections, Biologic & Regenerative Therapies), By Joint Type (Knee, Hip, Shoulder, Hand & Wrist, Ankle, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End-User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Sports Medicine Centers), Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2025–2034

Report Overview

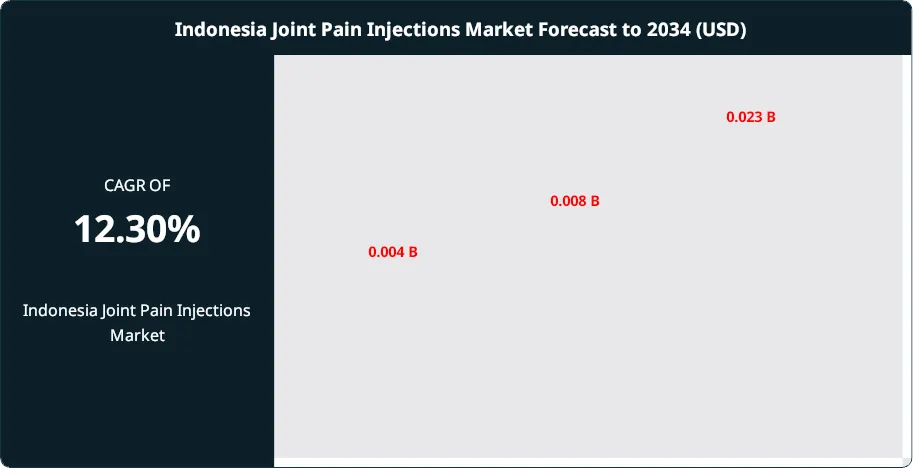

The Indonesia Joint Pain Injections Market was valued at US$ 0.004 Billion in 2024 and is projected to reach approximately US$ 0.023 Billion by 2034. The market is estimated to grow to around US$ 0.008 Billion in 2025. Based on projected growth from 2026 onward, the market is expected to expand at a compound annual growth rate (CAGR) of approximately 12.30% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportExpansion reflects a higher osteoarthritis burden, longer life expectancy, and improved diagnosis as imaging and specialist access widens. Clinicians use intra-articular injections to control pain, preserve mobility, and defer surgery for selected patients. Corticosteroid products contribute about 45% of 2024 revenue because they deliver rapid relief at low cost and align with established coverage rules. Hyaluronic acid products hold roughly 30% as providers target longer effect duration in mild-to-moderate disease. Orthobiologic options, including platelet-rich plasma and other regenerative approaches, represent an estimated 15%, supported by patient willingness to pay and expanding clinical evidence. The remaining share includes local anesthetics and adjunct formulations.

Supply conditions hinge on sterile manufacturing capacity, validated fill–finish lines, and steady access to needles, syringes, and medical-grade excipients. Concentration among compliant sites increases exposure to quality deviations and recalls, which can constrain availability and lift landed costs. Hospital outpatient departments generate about 55% of procedures in 2024, followed by ambulatory centers at roughly 30% and office-based orthopedic clinics near 15%. Providers adopt ultrasound-guided delivery at a faster rate to improve placement accuracy, reduce repeat procedures, and support performance-based contracting. Digitalization raises throughput via e-referrals, e-consent, and automated inventory controls.

Regulators enforce strict sterility assurance and post-market safety reporting, and they scrutinize particulate control and labeling claims. Biologic and combination-product classifications in the United States and Europe raise evidence thresholds and extend development timelines for premium offerings. Reimbursement shapes demand through step therapy and prior authorization, which compresses net prices for viscosupplementation and orthobiologics and rewards suppliers with real-world outcomes data. Risks include infection, flare reactions, variable durability of response, and competitive pressure from oral therapies, physical therapy pathways, and earlier surgical intervention.

North America leads with about 38% of 2024 revenue, supported by procedure volume and payer depth. Europe follows at roughly 27%, driven by aging demographics and specialist density. Asia Pacific reaches around 24% and posts the fastest growth as China and India expand orthopedic capacity, ambulatory infrastructure, and private insurance penetration. Investment hotspots include AI-assisted imaging triage, digitally serialized kits that improve traceability, and automated aseptic production that reduces batch variability and supports cost control.

Injections, Biologic & Regenerative Therapies), By Joint Type (Knee, Hip, Shoulder, Hand & Wrist, Ankle, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End-User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Sports Medicine Centers), Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands from 5.2 billion USD, 2024 to 12.1 billion USD, 2034 at 8.8%, 2024-2034.

- Segment Dominance: Corticosteroid injections lead the product mix at 32.0%, 2024.

- Segment Dominance: Knee joint injections dominate utilization at 35.0%, 2024.

- Driver: Rising knee disorders among elderly and athletic populations increase procedure volume by estimated: 6.0%, 2024.

- Restraint: Reimbursement controls and prior authorization pressure pricing by estimated: 3.0%, 2024.

- Opportunity: Regenerative and premium injectables grow faster, expanding revenue by estimated: 1.1 billion USD, 2030.

- Trend: Hospitals and clinics adopt image-guided delivery and digital workflows, improving accuracy and throughput by estimated: 12.0%, 2026.

- Regional Analysis: North America leads with 40.0% share and 2.0 million USD, 2024.

By Product

Corticosteroid injections remain the largest product category as the market moves into 2025. They account for just over 30 percent of global revenue, supported by fast onset of pain relief and established clinical protocols. You see consistent use across osteoarthritis and inflammatory joint conditions, particularly in hospital and orthopedic clinic settings. Their low unit cost and broad reimbursement coverage sustain high procedure volumes despite growing competition from newer therapies.

Hyaluronic acid injections form the second-largest segment and continue to gain traction among patients seeking longer pain control cycles. Adoption is strongest in patients over 55, where viscosupplementation helps delay surgical intervention. Industry data indicates this segment grows at nearly 9 percent annually through 2030, driven by rising knee and hip procedures and expanded approvals across Asia Pacific and Europe.

Platelet rich plasma injections post faster growth, exceeding a 10 percent CAGR, as you see rising acceptance of autologous therapies. Clinics market PRP as a biologic option with fewer systemic effects. The Others category, including stem cell based formulations and synthetic biomaterials, remains below 10 percent share but attracts investment due to clinical trial activity and private-pay demand.

By Joint Type

The knee segment dominates demand, contributing more than 35 percent of total procedures in 2025. High obesity prevalence, sports injuries, and age-related degeneration drive repeat treatment cycles. You benefit from standardized injection techniques and imaging guidance, which improves outcomes and physician confidence.

Hip joint injections follow, supported by rising osteoarthritis incidence and limited non-surgical alternatives. Growth remains steady as minimally invasive pain management gains preference over early joint replacement. Hand and wrist injections expand faster than the market average due to higher diagnosis rates of carpal tunnel syndrome and inflammatory disorders.

Other joints such as shoulder and ankle account for the remaining share. These procedures increase as ultrasound guidance improves targeting accuracy and reduces complication risk.

By Distribution Channel

Hospital pharmacies lead distribution with over 45 percent share in 2025. You rely on them for immediate availability during outpatient and inpatient procedures. Integration with orthopedic departments ensures consistent volume and compliance with storage standards.

Retail pharmacies maintain strong coverage, especially for follow-up care and chronic management. Their role grows in suburban and rural regions where hospital access is limited. Online pharmacies expand at double-digit rates as patients seek convenience, prescription renewals, and discreet delivery. Regulatory oversight remains strict, which tempers rapid expansion but supports trust.

By Region

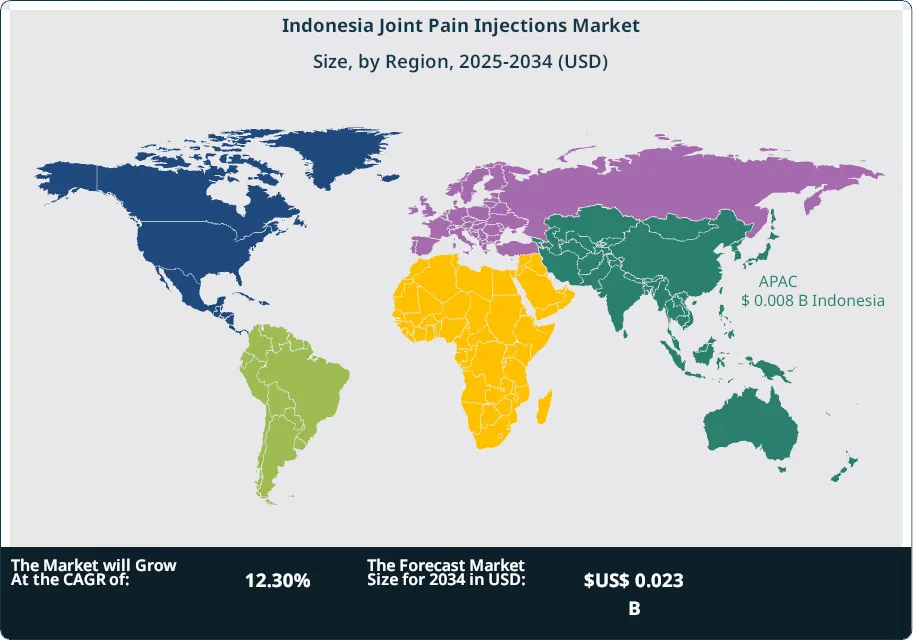

North America leads with over 40 percent market share, supported by high procedure rates and insurance coverage. The United States drives demand through aging demographics and strong adoption of image-guided injections. Europe follows, led by Germany, France, and the United Kingdom, where public healthcare systems support steady volumes.

Asia Pacific records the fastest growth, exceeding 10 percent annually. You see rising investment in orthopedic care across China, India, and South Korea. Latin America and the Middle East and Africa show gradual expansion as private healthcare spending increases and specialist access improves.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product

- Corticosteroid Injections

- Hyaluronic Acid Injections

- Platelet Rich Plasma Injections

- Others

By Joint Type

- Knee

- Hip

- Hand & Wrist

- Others

By Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

By Regions

- JAPAN

| Report Attribute | Details |

| Market size (2025) | US$ 0.008 B |

| Forecast Revenue (2034) | US$ 0.023 B |

| CAGR (2025-2034) | 12.30% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product (Corticosteroid Injections, Hyaluronic Acid Injections, Platelet Rich Plasma Injections, Others), By Joint Type (Knee, Hip, Hand & Wrist, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies) |

| Research Methodology |

|

| Regional scope | Indonesia |

| Competitive Landscape | Bioventus, Dr. Reddy’s Laboratories Ltd., SEIKAGAKU CORPORATION, Pacira BioSciences Inc., Ferring B.V., Zimmer Biomet, Teva Pharmaceutical Industries Ltd., Anika Therapeutics Inc., Sanofi |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Injections, Biologic & Regenerative Therapies), By Joint Type (Knee, Hip, Shoulder, Hand & Wrist, Ankle, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End-User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Sports Medicine Centers), Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2025–2034")

Injections, Biologic & Regenerative Therapies), By Joint Type (Knee, Hip, Shoulder, Hand & Wrist, Ankle, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End-User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Sports Medicine Centers), Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2025–2034")

Injections, Biologic & Regenerative Therapies), By Joint Type (Knee, Hip, Shoulder, Hand & Wrist, Ankle, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies), By End-User (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Sports Medicine Centers), Industry Trends, Competitive Landscape, Regional Outlook & Forecast 2025–2034")

Frequently Asked Questions

How big is the Indonesia Joint Pain Injections Market?

Indonesia Joint Pain Injections Market valued at US$ 0.010 B in 2024, projected to reach US$ 0.023 B by 2034, growing at 12.30% CAGR from 2026–2034.

Who are the major players in the Indonesia Joint Pain Injections Market?

Bioventus, Dr. Reddy’s Laboratories Ltd., SEIKAGAKU CORPORATION, Pacira BioSciences Inc., Ferring B.V., Zimmer Biomet, Teva Pharmaceutical Industries Ltd., Anika Therapeutics Inc., Sanofi

Which segments covered the Indonesia Joint Pain Injections Market?

By Product (Corticosteroid Injections, Hyaluronic Acid Injections, Platelet Rich Plasma Injections, Others), By Joint Type (Knee, Hip, Hand & Wrist, Others), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Indonesia Joint Pain Injections Market

Published Date : 02 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date