- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Indoor Farming LED Lighting Market Size, Share | CAGR of 13.8%

Global Indoor Farming LED Lighting Market Size, Share, Growth By Tech (Full Spectrum, Red & Blue, White), By Application (Vertical Farming, Greenhouses, Indoor Cultivation, Research), By Power Rating (Low, Medium, High), By Installation (New, Retrofit) Region, Key Players – Dynamics, Crop Photobiology, Smart Agriculture & Precision Horticulture Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

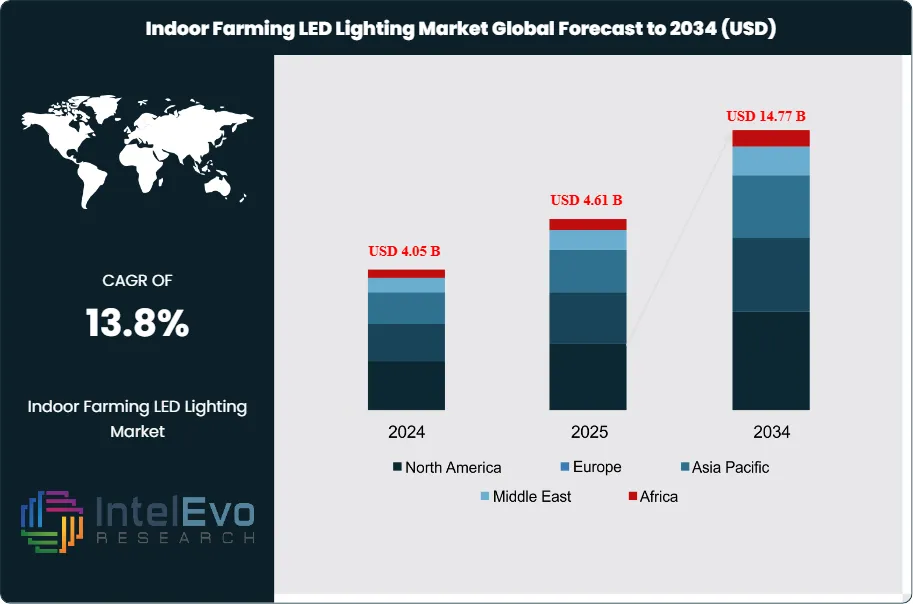

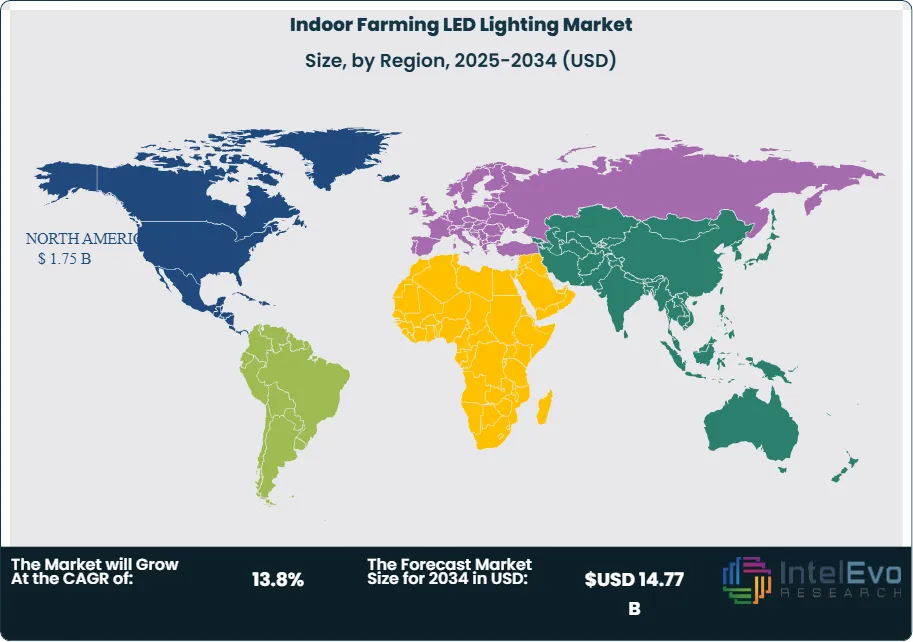

| USD 4.61 Billion | USD 14.77 Billion | 13.8% | North America, 38.0% |

The Indoor Farming LED Lighting Market was valued at approximately USD 4.05 billion in 2024 and reached USD 4.61 billion in 2025. The market is projected to grow to USD 14.77 billion by 2034, expanding at a CAGR of 13.8% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 10.16 billion over the analysis period, reflecting the decisive transition from legacy high-pressure sodium (HPS) systems toward high-efficacy, spectrum-tunable LED technology across vertical farms, indoor grow rooms, and controlled environment agriculture (CEA) facilities worldwide.

Get More Information about this report -

Request Free Sample ReportDemand for indoor farming LED lighting is being driven by three converging forces: the rapid expansion of commercial vertical farming, accelerating cannabis legalization across North America, and government-mandated energy-efficiency upgrades in European greenhouse operations. Photosynthetic photon efficacy (PPE) for commercial LED grow light fixtures now tops 3.1 µmol J⁻¹, a 90% improvement over legacy HPS lamps, enabling operators to reduce electricity costs by 40–60% while achieving crop cycle reductions of 20–25%. LED lighting accounts for 40–60% of total energy consumption in pure indoor farms, meaning each incremental efficiency gain directly improves operating margins and accelerates investment payback periods.

The regulatory environment is reinforcing the market's structural shift toward LEDs. The European Union's revised Energy Performance of Buildings Directive obligates heated glasshouses to transition from mercury-based lamps to connected LED systems as part of 2050 decarbonization targets. The EU's February 2025 enforcement of bans on mercury-containing fluorescent lamps is accelerating fixture replacement across European greenhouse operators. In the United States, the Department of Energy's Solid-State Lighting Program continues to channel R&D investment into horticultural LED innovation, and USDA National Institute of Food and Agriculture grants—including the Specialty Crop Research Initiative—fund university-led efficacy and spectrum optimization trials.

Technology is advancing at a pace that is compressing the hardware replacement cycle. Between 2023 and 2025, more than 45 new horticultural LED products with photosynthetic photon efficacy above 3.5 µmol/J entered commercial availability. Integrated smart-control lighting systems—combining IoT-connected dimming, dynamic spectrum recipes, and cloud-based analytics—expanded by 31% across greenhouse and indoor farming installations over the same period. By 2034, AI-driven spectrum automation, multi-channel LED designs, and close-canopy light deployment strategies are expected to reshape standard operating practice across the indoor farming sector.

North America holds the leading regional share at 38.0% of the indoor farming LED lighting market in 2025, valued at approximately USD 1.75 billion, anchored by cannabis cultivation infrastructure and an established CEA sector. Asia Pacific is the fastest-growing region, expanding at a CAGR of 16.7% through 2030, driven by food-security investments in Japan, South Korea, China, and emerging Gulf Cooperation Council vertical farming programs. Over the 2025–2034 forecast period, the market will be shaped by the convergence of precision agriculture, renewable energy integration, and increasingly standardized spectral data protocols that allow growers to replicate and scale proven light recipes across multi-facility operations.

Market Definition & Scope

The indoor farming LED lighting market is defined as the commercial market for light-emitting diode lighting systems engineered specifically to support plant photosynthesis and morphogenesis in controlled indoor environments, including vertical farms, indoor grow rooms, warehouse farms, and LED-supplemented commercial greenhouses. The market encompasses LED luminaires (toplights, intra-canopy or inter-lighting fixtures, and compact supplemental light bars), LED emitter components for horticultural fixture manufacturing, integrated software and sensor-driven control platforms, and associated services such as spectrum design and light-recipe consulting. Core technologies include full-spectrum, narrow-band, and dynamically tunable multi-channel LED systems, with Fluence Bioengineering, Signify N.V., ams OSRAM AG, Heliospectra AB, P.L. Light Systems, and Valoya Oy among the primary suppliers.

This analysis covers LED-based lighting systems deployed across indoor vertical farms, standalone indoor grow rooms, plant factories, and LED-supplemented commercial greenhouses. Explicitly excluded from this scope are non-LED legacy technologies including high-pressure sodium (HPS) lamps, metal halide (MH) systems, fluorescent grow lights, and plasma lamps, each of which constitutes a separate and declining lighting category. Open-field agricultural lighting, poultry and livestock photoperiod systems, and decorative or general-purpose interior horticultural lighting are also excluded. The indoor farming LED lighting market represents the technology-forward segment of the broader horticulture lighting industry, which was valued at approximately USD 7.51 billion in 2025 when all lighting technologies and all non-indoor applications are included.

, By Application (Vertical Farming, Greenhouses, Indoor Cultivation, Research), By Power Rating (Low, Medium, High), By Installation (New, Retrofit) Region, Key Players – Dynamics, Crop Photobiology, Smart Agriculture & Precision Horticulture Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The indoor farming LED lighting market advanced from an estimated USD 2.5 billion in 2020 to USD 4.61 billion in 2025 and is projected to reach USD 14.77 billion by 2034, a 13.8% CAGR over 2025–2034.

- Segment Dominance (Technology): LED technology commanded 80.3% of the broader horticulture lighting market in 2024, replacing HPS and fluorescent systems in both new installations and retrofit projects due to superior energy efficiency and spectrum control.

- Segment Dominance (Application): Commercial greenhouses held 43.2% of the indoor farming LED lighting market in 2025, while vertical farms represented 41.0% and are growing at a CAGR of 19.6% through 2030, the fastest application segment.

- Driver: Cannabis legalization across 24 U.S. states and Canada's federal legal market created sustained demand for precision LED systems, contributing an estimated 22% of North American indoor farming LED lighting revenue in 2024.

- Restraint: High upfront capital expenditure—LED fixtures for a 1,000 sq ft indoor farm cost USD 10,000–25,000, with payback periods of 2.5–5 years depending on local electricity tariffs—limits adoption among small-scale and emerging-market operators.

- Opportunity: The vertical farming segment represents the largest growth opportunity, with global vertical farming infrastructure investments funding more than 300 large facilities between 2020 and 2025, each requiring thousands of LED fixtures; a single 5,000 square meter facility installs more than 8,000 LED grow lights.

- Trend: Dynamically tunable multi-channel LED systems are emerging as the dominant technology paradigm, with smart control lighting adoption rising 31% between 2023 and 2025 and replacing static full-spectrum designs in new commercial build-outs.

- Regional: North America led the indoor farming LED lighting market in 2025 with a 38.0% share valued at USD 1.75 billion, driven by cannabis legalization, CEA adoption, and USDA-backed innovation programs.

Key Insights Summary

- Photosynthetic photon efficacy for commercial LED horticultural fixtures reached 3.1 µmol J⁻¹ in 2024, a 90% improvement over legacy HPS lamps, enabling a 40–60% reduction in facility energy costs related to illumination in fully indoor farms (DOE Integrated Lighting Campaign data).

- At GreenTech Amsterdam in June 2025, ams OSRAM debuted the OSCONIQ P 3737 GEN 2 hyper-red emitter, achieving 82.4% wall-plug efficiency and a Q90 lifetime of 102,000 operating hours, reducing LED unit counts per fixture while generating estimated annual electricity savings of EUR 11,000 for mid-scale greenhouse operations.

- In November 2025, Fluence Bioengineering introduced the Red Sandwich dual-layer lighting technique at MJBizCon 2025 in Las Vegas, achieving photon efficiency of 3.4 µmol/J and reducing total energy use by up to 26% compared with single-layer top lighting across commercial cannabis operations.

- The EU's enforcement of mercury-fluorescent lamp bans effective February 2025, combined with the revised Energy Performance of Buildings Directive mandating connected LED retrofits in heated glasshouses, is accelerating a multi-billion-dollar replacement cycle across European horticulture; retrofit projects held 58.7% of installation activity in 2024.

- Research published in Frontiers in Plant Science (2023), supported by the USDA Specialty Crop Research Initiative, demonstrated that close-canopy LED placement strategies—reducing light-to-canopy separation from 45 cm to 15 cm—materially improve photon capture efficiency, pointing to a structural design shift in next-generation vertical farm tiers.

- In May 2025, P.L. Light Systems commercialized real-time tunable LED technology allowing growers to shift spectra and intensity by crop growth stage during operation, reducing energy use while lifting yield—signaling a shift from static to dynamic spectrum management as the new commercial baseline.

Competitive Landscape Overview

The indoor farming LED lighting market is moderately consolidated, with Signify N.V., ams OSRAM AG, Heliospectra AB, and P.L. Light Systems collectively holding a meaningful but not dominant combined share of approximately 55–60% of total market revenue in 2025. The competitive landscape features large diversified lighting conglomerates alongside specialist horticultural suppliers, with differentiation occurring across three axes: luminaire hardware efficacy (µmol/J), software-driven spectrum control depth, and geographic service reach. Consolidation gathered pace when Acuity Brands, Inc. acquired Current's Arize horticulture line in 2023, bringing a mainstream U.S. lighting distributor into specialty cultivation and signaling broader industry validation of the CEA lighting segment as a structurally important market.

Competition is shifting from hardware performance benchmarks toward integrated platform propositions combining high-efficacy LED hardware, cloud-connected control systems, crop-specific spectral recipes, and agronomic services. Signify's acquisition and integration of Fluence Bioengineering into its Agricultural Lighting division extended its reach from the European greenhouse market into the North American cannabis and vertical farm sector, creating a dual-geography platform with coverage across vertical farms, commercial greenhouses, and research applications. ams OSRAM competes primarily at the emitter level, supplying LED chips to luminaire manufacturers across the supply chain rather than selling direct-to-grower systems. In Asia Pacific, Everlight Electronics Co., Ltd. (Taiwan) and VANQ Technology leverage geographic proximity to accelerate delivery cycles for regional greenhouse operators in Japan, South Korea, and emerging GCC markets.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Signify N.V. | Netherlands | Leader | GreenPower LED, Philips Horticulture Lighting | Global | Integrated Fluence into Agricultural Lighting division; RAPTR 2 and SPYDR 3 introduced, June 2025 |

| ams OSRAM AG | Austria/Germany | Leader | OSCONIQ P 3737 GEN 2, OSCONIQ P 3737 Batwing | Europe, Asia, N. America | OSCONIQ P 3737 GEN 2 debuted at GreenTech Amsterdam, June 2025, delivering 82.4% Hyper Red efficiency |

| Heliospectra AB | Sweden | Challenger | MITRA X, SIERA light bar, ELIXIA, helioCORE | Europe, N. America, Australia | Dynamic MITRA X multi-channel C3 and C4 fixtures with Spectrum Design Tool rolled out, 2024 |

| P.L. Light Systems | Canada | Challenger | Tunable LED toplights, hybrid LED systems | N. America, Europe | Real-time tunable LED technology with growth-stage spectrum shifting made public, May 2025 |

| Acuity Brands, Inc. | USA | Challenger | Arize horticulture LED line (acquired 2023) | N. America | Folded Current's Arize line into portfolio to gain specialty cultivation segment presence, 2023 |

| Valoya Oy | Finland | Niche Player | AP67, NS1 spectrum LED fixtures | Europe, N. America | Expanded customer base in European vertical farm projects with customized spectral recipes |

| California LightWorks | USA | Niche Player | SolarSystem 550, MegaDrive LED | N. America | Extended product lineup for mid-scale indoor cannabis and produce operations, 2024 |

| Everlight Electronics | Taiwan | Niche Player | LED emitter components for horticultural fixtures | Asia Pacific | Increased emitter production capacity to serve GCC and East Asian indoor farming demand, 2024–2025 |

By Technology

LED technology commands the indoor farming LED lighting market as both the dominant and fastest-growing segment, holding an 80.3% share of the total horticulture lighting market in 2024, with PPE levels now reaching 3.1–3.4 µmol/J across commercial product lines from Signify (Fluence), ams OSRAM, and P.L. Light Systems. The residual share belongs to high-intensity discharge (HID) systems—primarily HPS lamps—which retain relevance in legacy greenhouse installations where radiant heat from the lamp aids root-zone temperature management in cold climates. HPS systems are contracting at an estimated 8–10% annual rate as EU fluorescent bans take effect and energy cost pressures mount.

Within the LED segment, full-spectrum broad-band configurations held 62.0% of revenue in 2024 because of their ability to support diverse crop types across a single facility. Narrow-band red-blue configurations—once the standard for energy-conserving indoor lettuce production—are losing ground to dynamically tunable multi-channel designs such as Fluence's RAPTR 2 and Heliospectra's MITRA X, which adjust spectral composition in real time by crop growth stage. The dynamically tunable segment grew 31% in adoption across greenhouse and indoor farming installations between 2023 and 2025, representing the most technically differentiated and highest-margin product tier. At sub-50W chip level, a separate high-growth segment expands at a projected 18.6% CAGR through 2030, serving vertical farm intra-canopy and supplemental light bars where compact form factor and low heat generation matter more than peak photon flux.

By Application

Commercial greenhouses held the largest application share at 43.2% of market revenue in 2025, generating approximately USD 1.99 billion, because the installed base of large-scale greenhouse operations in the Netherlands, Germany, France, the United States, and Canada provides a continuous retrofit demand stream as legacy HPS fixtures reach end-of-life. In these facilities, Signify's GreenPower LED production modules and ams OSRAM's OSCONIQ P 3737-based luminaires serve as primary toplights, often paired with Heliospectra's helioCORE control software for DLI management and light recipe scheduling. Vegetables and fruits—particularly tomatoes, cucumbers, peppers, and leafy greens—represent 46.9% of cultivation category demand across greenhouses, making them the dominant crop segment and the primary reference case for ROI-driven procurement decisions.

Vertical farms are the fastest-growing application segment, advancing at a 19.6% CAGR through 2030, because entirely indoor operations with zero ambient sunlight require LED lighting as the sole energy input for photosynthesis, making lighting spend proportionally larger than in greenhouse settings. Over 1,500 vertical farming facilities operated globally as of 2025, with more than 85% relying exclusively on LED systems. LED lighting accounts for 25–45% of vertical farm operational expenditure, meaning the business case for efficacy improvements is immediate and measurable. Dubai's GigaFarm project, targeting 3 million kg of annual produce output, and Oasthouse Ventures' 65-acre Virginia greenhouse facility—scheduled for 2026 completion and designed around LEDs from the ground up—demonstrate how both the Middle East food-security agenda and the U.S. CEA build-out are creating large single-order opportunities for LED suppliers. Cannabis and specialty crops represent the third major sub-segment, holding an estimated 17% of indoor farm LED lighting revenue in 2025 and growing at a 17.5% CAGR through 2030, driven by adult-use legalization spreading to additional U.S. states and Germany's 2024 partial legalization.

By Power Rating

Below-300W LED fixtures held the largest power-rating segment share at 56.4–67.0% of market revenue in 2025, driven by their dominance in small-to-mid-scale indoor farms, vertical farm tier lighting, and research applications. These fixtures, represented by products such as Fluence's SPYDR 3 series (available in five wattage configurations up to 2,260 µmol/s output) and Heliospectra's SIERA light bar, are favored for their energy efficiency, heat management characteristics, and compatibility with multi-tier vertical racking systems. Spider Farmer, Mars Hydro, and Vipraspectra lead the commercial small-form-factor sub-segment.

Above-300W high-output fixtures serve large campus-scale greenhouse operations requiring high photon flux densities (PPFD) across wide canopy areas. This tier is dominated by Signify GreenPower LED toplights and ams OSRAM-based commercial luminaires, which deliver output levels above 2,000 µmol/s and sustain 90% photon flux after 102,000+ operating hours. The 300W–1,000W bracket is growing at 8.9% CAGR as commercial produce growers—particularly tomato and cucumber producers in the Netherlands and Canada—standardize on high-output LED toplights to replace aging HPS ceiling fixtures while qualifying for EU energy efficiency incentives and utility rebate programs.

By Installation Type

Retrofit installations commanded 58.7% of the indoor farming LED lighting market in 2024, reflecting a vast installed base of HPS and fluorescent fixtures in operational greenhouses and indoor farms that are approaching scheduled replacement cycles. Retrofit activity is further accelerated by EU mercury-fluorescent bans enforced in February 2025, utility rebate programs in North America that shorten LED payback from five years to as few as two years in favorable tariff zones, and the energy cost shock following electricity price volatility in 2024–2025 that sharpened operators' focus on per-kilowatt-hour returns. Signify and ams OSRAM both provide retrofit-compatible fixture formats that preserve existing mounting infrastructure while delivering 11% or greater energy savings compared with predecessor LED generations.

New installation projects, while representing 41.3% of market revenue in 2024, are set to grow at a 15.2% CAGR through 2030 as purpose-built vertical farms and CEA campuses are commissioned globally. New builds benefit from structural freedom to implement close-canopy lighting architectures, moving-light rigs, and intra-canopy inter-lighting strings that are impractical in retrofitted legacy facilities. Virginia's Oasthouse Ventures 65-acre greenhouse, Qatar's urban food-security investments, and South Korea's government-sponsored vertical farming parks all represent large-format new-build projects where LED specifications are set at the design stage, not the renovation stage—creating higher average order values and longer-term supply agreements for LED manufacturers.

Regional Analysis

North America held the largest regional share of the indoor farming LED lighting market in 2025 at 38.0%, generating approximately USD 1.75 billion. The United States is the primary demand anchor, with 24-state cannabis legalization, a mature CEA sector across California, Colorado, Arizona, and the Northeast, and USDA Specialty Crop Research Initiative funding supporting ongoing LED optimization research. Canada contributes meaningfully through federal cannabis legalization infrastructure and greenhouse expansion programs in Ontario and British Columbia. Utility rebate programs from utilities including Pacific Gas & Electric and Ontario's IESO fund LED retrofits and shorten payback periods, directly stimulating replacement decisions. The North America market is projected to advance at a CAGR of approximately 12.5% through 2034.

Europe accounted for approximately 31.0% of the indoor farming LED lighting market in 2025, valued at USD 1.43 billion, with the Netherlands, Germany, France, and the United Kingdom as primary demand centers. The Netherlands houses the world's largest concentration of commercial greenhouse acreage and has historically been the proving ground for Signify's GreenPower LED platform and Heliospectra's MITRA X system. The EU's revised Energy Performance of Buildings Directive and mercury-fluorescent bans enforce a structural upgrade cycle, while Germany's 2024 partial cannabis legalization opens a new CEA application. Europe's LED retrofit rate is the highest globally, at 58.7% of project activity, reflecting a large legacy HPS install base and strong policy pressure to decarbonize agricultural energy use.

Asia Pacific generated approximately 20.0% of market revenue in 2025, estimated at USD 0.92 billion, and is the fastest-growing region at a CAGR of 16.7% through 2030. Japan leads in plant factory density, with automated facilities producing pesticide-free leafy greens and herbs at scale using Signify Philips GreenPower LED modules; a Innovatus vertical farm in Fuji City produces 12,000 heads of lettuce daily under exclusively LED illumination. South Korea funds government-sponsored vertical farming parks, and China's food-self-sufficiency agenda drives aggressive investment in CEA infrastructure. Everlight Electronics (Taiwan) and VANQ Technology supply regional luminaire manufacturers with tailored emitter components, cutting lead times and reducing import dependency.

Latin America contributed approximately 7.0% of market revenue in 2025, valued at USD 0.32 billion, with growth concentrated in Brazil, Mexico, and Chile. Indoor cannabis cultivation following regulatory changes in Brazil and Mexico drives the primary demand spike, supplemented by high-value specialty produce operations in controlled greenhouse environments. Government modernization programs and increasing private equity interest in agritech are beginning to catalyze CEA investment in urban centers where fresh produce supply chains are unreliable. The Middle East and Africa accounted for approximately 4.0% of market revenue in 2025, valued at USD 0.18 billion, but is gaining strategic importance through GCC urban agriculture grant programs. The UAE's goal to commission 500 vertical farms by 2026—anchored by projects such as Dubai's GigaFarm—and subsidized electricity for indoor farms in Saudi Arabia and Qatar create a disproportionately large opportunity relative to current revenue size.

Country Analysis

The United States indoor farming LED lighting market reached approximately USD 1.42 billion in 2025, advancing at a country-level CAGR of approximately 13.2% through 2034. Federal support through the USDA's Specialty Crop Research Initiative—including the OptimIA research consortium led by Michigan State University with Purdue University, the University of Arizona, and Ohio State University—has quantified close-canopy LED energy savings and is translating laboratory findings into commercial deployment standards. DOE data indicates that converting all U.S. indoor horticultural lighting to LEDs would reduce annual consumption to 6.3 TWh of site electricity, representing a 34% energy saving versus the prior technology baseline. State-level cannabis legalization in California, Colorado, Michigan, Illinois, and Massachusetts maintains a high-density CEA lighting demand footprint, while utility rebate programs from PG&E, Xcel Energy, and Consolidated Edison further subsidize LED adoption across commercial growing operations. In March 2026, Signify introduced an advanced horticultural LED lighting system with integrated spectrum control and smart automation tailored specifically for U.S. indoor farm operators.

The Netherlands indoor farming LED lighting market was valued at approximately USD 0.38 billion in 2025 and is growing at an estimated 14.5% CAGR, reflecting its position as the global greenhouse technology export hub. Signify's GrowWise Center in Eindhoven serves as the primary commercial light-recipe development facility, translating research findings directly into Philips GreenPower product specifications. The revised EU Energy Performance of Buildings Directive and mercury-fluorescent bans drove an acceleration of HPS-to-LED retrofit activity across the Netherlands' 10,000-plus hectares of commercial greenhouse acreage during 2024–2025. Heliospectra collaborated with Tomatoworld and NatureSweet on LED tomato cultivation trials, demonstrating how controlled red-to-far-red ratios improve fruit uniformity and shelf life.

South Korea's indoor farming LED lighting market reached approximately USD 0.19 billion in 2025, growing at an estimated 14.8% CAGR driven by government-sponsored vertical farming initiatives and acute arable land constraints. The Korean Ministry of Agriculture, Food and Rural Affairs funds smart farming programs integrating LED lighting, IoT sensors, and AI-driven crop management. Farm8, a South Korean agriculture company, uses LED technology to reduce plant growth cycles significantly compared with outdoor cultivation, demonstrating the government-sponsored productivity mandate driving commercial adoption. South Korea is also a manufacturing base for mid-tier LED components supplied to regional CEA operators in Southeast Asia. Japan represents a complementary country-level growth story, with its government's "smart agriculture" mandate and dense plant factory network generating approximately USD 0.16 billion in indoor farming LED lighting demand in 2025, growing at approximately 13.5% CAGR through 2034.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Technology

- Full Spectrum LED

- Red & Blue LED

- White LED

- Others

By Application

- Vertical Farming

- Greenhouses

- Indoor Cultivation Facilities

- Research & Laboratories

By Power Rating

- Low Power

- Medium Power

- High Power

By Installation Type

- New Installations

- Retrofit Installations

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.61 B |

| Forecast Revenue (2034) | USD 14.77 B |

| CAGR (2025-2034) | 13.8% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Full Spectrum LED, Red & Blue LED, White LED, Others), By Application, (Vertical Farming, Greenhouses, Indoor Cultivation Facilities, Research & Laboratories), By Power Rating, (Low Power, Medium Power, High Power), By Installation Type, (New Installations, Retrofit Installations) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SIGNIFY N.V., AMS OSRAM AG, HELIOSPECTRA AB, P.L. LIGHT SYSTEMS, ACUITY BRANDS, INC., VALOYA OY, CALIFORNIA LIGHTWORKS, EVERLIGHT ELECTRONICS CO., LTD., GAVITA INTERNATIONAL B.V., LUMIGROW, INC., ILLUMITEX, INC., VANQ TECHNOLOGY, HORTILUX SCHRÉDER, LED iBOND A/S, NATURE'S MIRACLE HOLDINGS, SPIDER FARMER, MARS HYDRO, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Vertical Farming, Greenhouses, Indoor Cultivation, Research), By Power Rating (Low, Medium, High), By Installation (New, Retrofit) Region, Key Players – Dynamics, Crop Photobiology, Smart Agriculture & Precision Horticulture Trends & Forecast 2026-2034")

, By Application (Vertical Farming, Greenhouses, Indoor Cultivation, Research), By Power Rating (Low, Medium, High), By Installation (New, Retrofit) Region, Key Players – Dynamics, Crop Photobiology, Smart Agriculture & Precision Horticulture Trends & Forecast 2026-2034")

, By Application (Vertical Farming, Greenhouses, Indoor Cultivation, Research), By Power Rating (Low, Medium, High), By Installation (New, Retrofit) Region, Key Players – Dynamics, Crop Photobiology, Smart Agriculture & Precision Horticulture Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Indoor Farming LED Lighting Market?

Global Indoor Farming LED Lighting Market was valued at USD 4.05 billion in 2024 and is projected to reach USD 14.77 billion by 2034, at a CAGR of 13.8% (2026–2034).

Who are the major players in the Indoor Farming LED Lighting Market?

SIGNIFY N.V., AMS OSRAM AG, HELIOSPECTRA AB, P.L. LIGHT SYSTEMS, ACUITY BRANDS, INC., VALOYA OY, CALIFORNIA LIGHTWORKS, EVERLIGHT ELECTRONICS CO., LTD., GAVITA INTERNATIONAL B.V., LUMIGROW, INC., ILLUMITEX, INC., VANQ TECHNOLOGY, HORTILUX SCHRÉDER, LED iBOND A/S, NATURE'S MIRACLE HOLDINGS, SPIDER FARMER, MARS HYDRO, OTHERS

Which segments covered the Indoor Farming LED Lighting Market?

By Technology, (Full Spectrum LED, Red & Blue LED, White LED, Others), By Application, (Vertical Farming, Greenhouses, Indoor Cultivation Facilities, Research & Laboratories), By Power Rating, (Low Power, Medium Power, High Power), By Installation Type, (New Installations, Retrofit Installations)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Indoor Farming LED Lighting Market

Published Date : 17 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date