- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Direct Air Capture Market Size & Forecast | CAGR 27.7%

Global Direct Air Capture Market Size, Share, Growth & Industry Analysis By Capture Technology (Solid Sorbent-Based DAC, Liquid Solvent-Based DAC, Electrochemical DAC, Mineralization-Based DAC), By End-Use CO2 Application (Geological Storage, Synthetic Fuels & E-Fuels, Enhanced Oil Recovery, Construction Materials), By Scale & Facility Type (Large-Scale, Modular, Distributed, DAC Hubs) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

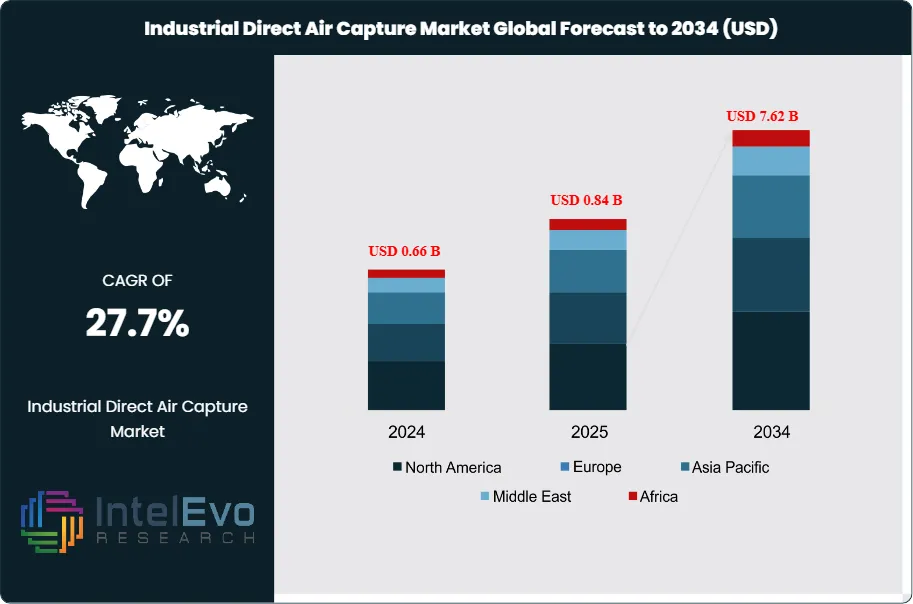

| USD 0.84 Billion | USD 7.62 Billion | 27.7% | North America, 44.0% |

The Industrial Direct Air Capture Market was valued at approximately USD 0.66 Billion in 2024 and reached USD 0.84 Billion in 2025. The market is projected to grow to USD 7.62 Billion by 2034, expanding at a CAGR of 27.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 6.78 Billion over the analysis period, driven by binding corporate net-zero commitments, sovereign climate legislation mandating carbon dioxide removal, rapid commercialization of solid sorbent and liquid solvent DAC technologies, and growing voluntary carbon credit demand from aviation, maritime, and heavy industrial sectors that cannot fully decarbonize through emissions reduction alone.

Get More Information about this report -

Request Free Sample ReportIndustrial direct air capture (DAC) refers to engineered systems that use chemical processes to extract carbon dioxide from ambient atmospheric air at concentrations of approximately 420 parts per million, producing a concentrated CO2 stream suitable for geological storage, utilization in synthetic fuels, or conversion to mineral carbonates. DAC fundamentally differs from point-source carbon capture by operating on ambient air rather than flue gas, enabling carbon removal from any geographic location without dependence on industrial emission source co-location. The industrial direct air capture market encompasses solid sorbent-based systems using amine-functionalized materials or zeolites, liquid solvent systems using potassium hydroxide or amine solutions, electrochemical DAC using membrane processes, and mineralization-based approaches using calcium or magnesium oxide feedstocks.

Several policy and commercial mechanisms are accelerating industrial direct air capture market growth at an unprecedented rate. The US Inflation Reduction Act's 45Q tax credit provides USD 180 per metric ton of CO2 permanently stored from DAC systems, substantially improving the investment economics of commercial-scale facilities and catalyzing over USD 4.5 Billion in committed DAC project capital in the United States through 2025. The European Commission's Carbon Removals Certification Framework, adopted in 2024, establishes a regulatory methodology for quantifying and certifying DAC-based carbon removals for use in EU member state national accounting and voluntary carbon markets. The US Department of Energy's Regional Direct Air Capture Hubs program has allocated USD 3.5 Billion to four regional hub projects, each targeting 1 Million metric tons per year of CO2 removal capacity, providing the capital infrastructure that brings commercial-scale DAC costs within the range of corporate net-zero compliance budgets.

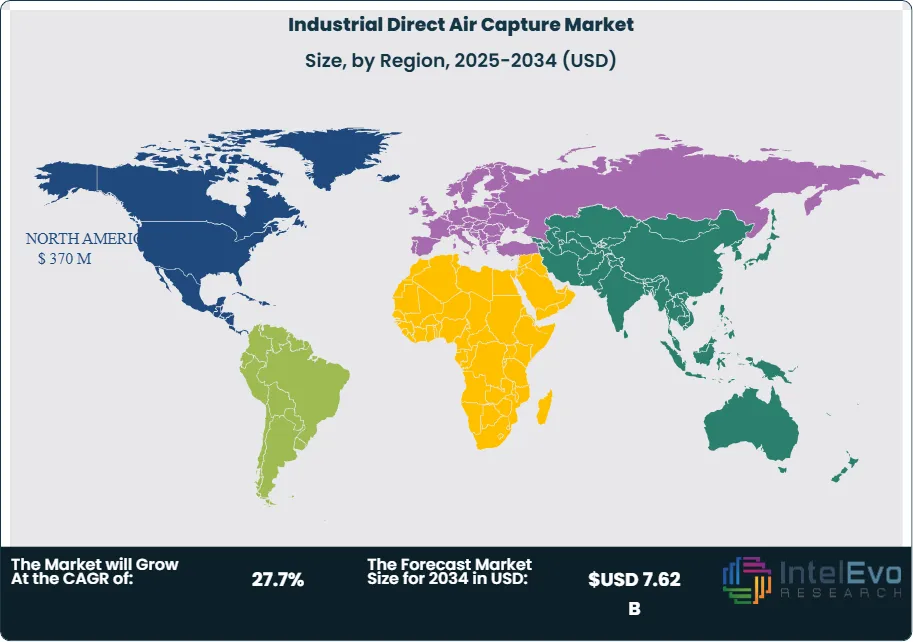

The IEA's Net Zero Emissions by 2050 scenario requires global carbon removal capacity reaching 1 Billion metric tons per year by 2050, with industrial DAC contributing approximately 980 Million metric tons per year. This scale requirement creates a structural, decade-spanning demand signal that differentiates the industrial direct air capture market from other climate technology sectors that face demand uncertainty. North America led the industrial direct air capture market with a 44.0% share in 2025, equivalent to USD 370 Million, driven by the 45Q tax credit mechanism, DOE hub investments, and the commercial scale-up of Occidental Petroleum's 1PointFive DAC program in Texas. Europe is the second-largest region, with Iceland's geothermal energy advantage supporting Climeworks' Mammoth plant as the world's largest DAC installation.

, By End-Use CO2 Application (Geological Storage, Synthetic Fuels & E-Fuels, Enhanced Oil Recovery, Construction Materials), By Scale & Facility Type (Large-Scale, Modular, Distributed, DAC Hubs) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global industrial direct air capture market was valued at USD 0.84 Billion in 2025 and is forecast to reach USD 7.62 Billion by 2034, registering a CAGR of 27.7% during the 2026-2034 forecast period.

- Segment Dominance: By capture technology, solid sorbent-based DAC systems held the largest share at 52.4% of the industrial direct air capture market in 2025, driven by their modular scalability, compatibility with low-temperature heat sources, and the commercial precedent established by Climeworks' amine-functionalized solid sorbent plants in Iceland and Switzerland.

- Segment Dominance: By end-use CO2 application, geological storage and permanent sequestration accounted for 64.8% of the industrial direct air capture market in 2025, reflecting the carbon credit market's preference for permanent removal over utilization pathways that return CO2 to the atmosphere over shorter timeframes.

- Driver: The US Inflation Reduction Act's 45Q tax credit of USD 180 per metric ton of CO2 permanently stored from DAC systems has catalyzed over USD 4.5 Billion in committed US DAC project capital by 2025, making the US the world's largest single-country DAC investment environment and transforming the commercial economics of large-scale DAC facility development.

- Restraint: Industrial direct air capture costs remain in the USD 400-1,000 per metric ton CO2 range at current commercial scale, substantially above the USD 100-200 per metric ton cost target required for broad voluntary carbon market competitiveness and the USD 50-100 range that would enable DAC integration into industrial decarbonization at mass scale.

- Opportunity: The aviation sector's net-zero commitment under ICAO's CORSIA scheme, which requires airlines to offset or remove carbon for international flights above 2019 emission levels, creates a structured demand for permanent carbon removal credits from DAC estimated at 400-600 Million metric tons per year by 2034 under ICAO's progressive CORSIA phase-in.

- Trend: Electrochemical DAC approaches using ion exchange membranes and pH swing processes, which can operate on electricity alone at efficiencies of 200-400 kWh per ton CO2 rather than the 1,500-2,000 kWh per ton CO2 thermal energy requirement of conventional sorbent DAC, grew at approximately 42.6% annual investment rate in 2025, attracting growing venture and government funding.

- Regional Analysis: North America led the industrial direct air capture market with a 44.0% share, equivalent to USD 370 Million in 2025, supported by the US 45Q tax credit, DOE Regional DAC Hub program funding of USD 3.5 Billion, and the concentration of commercial-scale DAC facility development in Texas and Wyoming.

Competitive Landscape Overview

The industrial direct air capture market is highly fragmented, with Climeworks, Carbon Engineering (1PointFive), Heirloom Carbon, and Verdox collectively accounting for approximately 56% of global revenues in 2025. Competition centers on CO2 capture cost per metric ton, energy intensity per unit capture, sorbent material longevity and regeneration cycle durability, and the ability to secure long-term offtake agreements with corporate buyers or government procurement programs. M&A activity intensified with Occidental Petroleum's acquisition of Carbon Engineering in 2023, which provided the scale financing to advance the Stratos commercial DAC plant to operational status in Texas by 2025. New entrants including electrochemical DAC developers and bio-inspired mineralization approaches are increasing technology diversity and attracting DOE and EU innovation grant funding, challenging the near-term commercial dominance of established sorbent-based approaches.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Climeworks AG | Switzerland | Leader | Mammoth DAC Plant (DACCS) | Europe & North America | Commissioned Mammoth DAC plant in Iceland (36,000 tCO2/yr capacity); Q1 2025. |

| Carbon Engineering (1PointFive) | Canada/USA | Leader | AIR TO FUELS DAC + Storage | North America | Opened Stratos DAC commercial plant in Texas (500,000 tCO2/yr target); operational 2025. |

| Heirloom Carbon | USA | Leader | Limestone-Based Low-Cost DAC | North America | Scaled modular limestone calcination DAC to 20,000 tCO2/yr pilot; raised USD 150M Series B; 2025. |

| Verdox Inc. | USA | Leader | Electrochemical DAC Technology | North America | Received USD 80M DOE grant for electrochemical DAC scale-up; progressing to 10,000 tCO2/yr pilot; 2025. |

| Global Thermostat | USA | Challenger | Solid Sorbent Contactor DAC Systems | North America | Signed industrial carbon credit offtake agreement with a US petrochemical company; Q2 2025. |

| Sustaera (formerly BionicLeaf) | USA | Challenger | Monolith Solid Sorbent DAC | North America | Raised USD 12M to advance modular ceramic monolith DAC system toward commercial pilot; 2025. |

| Mission Zero Technologies | UK | Niche Player | ElectroSwing DAC Technology | Europe | Secured UK Research and Innovation Innovate UK funding for first industrial pilot; Q3 2025. |

| Carbyon | Netherlands | Niche Player | Ultra-Thin Sorbent Film DAC | Europe | Reached 1,000 tCO2/yr pilot capacity with ultra-thin rapid-cycling sorbent DAC; 2025. |

| RepAir | Israel | Niche Player | Electrochemical Membrane DAC | Middle East & Europe | Won EUR 2.5M EIC Accelerator grant for membrane-based electrochemical DAC scale-up; Jan 2026. |

| Carbfix (Reykjavik Energy) | Iceland | Niche Player | Basalt CO2 Mineralization Storage | Europe | Expanded CO2 mineralization geological storage capacity to 60,000 tCO2/yr storage rate; 2025. |

By Capture Technology

The industrial direct air capture market by capture technology spans solid sorbent-based DAC, liquid solvent-based DAC, electrochemical DAC, and mineralization-based DAC. Solid sorbent-based DAC held the dominant technology share at 52.4% of the industrial direct air capture market in 2025, equivalent to approximately USD 440 Million. These systems use amine-functionalized porous materials, ion exchange resins, or zeolites to adsorb CO2 from ambient air through a temperature-vacuum swing adsorption (TVSA) or temperature swing adsorption (TSA) cycle. CO2 is captured during the adsorption phase at ambient conditions and released during the regeneration phase at temperatures of 80-120 degrees Celsius, producing a concentrated CO2 stream at approximately 95-99% purity. Climeworks' proprietary amine-impregnated sorbent, Heirloom's calcium hydroxide mineral sorbent, and Sustaera's ceramic monolith sorbent each represent distinct sorbent material approaches within this technology segment. Solid sorbent systems benefit from modular, containerized unit design that enables incremental capacity addition and geographic deployment flexibility, with individual modules typically rated at 1,000-10,000 metric tons CO2 per year.

Liquid solvent-based DAC, which uses aqueous potassium hydroxide or monoethanolamine solutions to absorb CO2 from ambient air in contactor towers and regenerate solvent in high-temperature (approximately 900 degrees Celsius) calcination or steam stripping processes, represented 30.6% of the industrial direct air capture market in 2025. Carbon Engineering's liquid solvent process, now commercialized through Occidental Petroleum's 1PointFive subsidiary at the Stratos facility in Texas, represents the most commercially advanced large-scale liquid solvent DAC system globally, with a design capacity of 500,000 metric tons of CO2 per year at full buildout. Electrochemical DAC, using electrodialysis, membrane processes, or electrochemical pH swing to drive CO2 capture and release without thermal energy requirements, held 10.4% of the market in 2025 and is the fastest-growing technology segment at an estimated CAGR of 38.6% through 2034. Mineralization-based DAC using calcium or magnesium oxide sorbents or enhanced weathering principles represented the remaining 6.6% of the industrial direct air capture market by capture technology in 2025.

By End-Use CO2 Application

The industrial direct air capture market by end-use CO2 application covers geological storage and permanent sequestration, utilization in synthetic fuels and e-fuels, utilization in enhanced oil recovery, and utilization in construction materials and mineralization. Geological storage and permanent sequestration held the dominant end-use share at 64.8% of the industrial direct air capture market in 2025, equivalent to approximately USD 544 Million. Permanent geological storage, where captured CO2 is injected into deep saline aquifers, depleted oil and gas reservoirs, or basalt rock formations for permanent mineral carbonation, generates the highest-value carbon credits under US 45Q tax credit rules (USD 180/tCO2) and the EU Carbon Removals Certification Framework because it provides indefinite carbon removal without risk of re-emission. Climeworks' basalt rock mineralization partnership with Carbfix in Iceland, which converts CO2 to solid carbonate minerals within 2 years of injection, and Occidental's saline aquifer injection in the Texas Permian Basin each demonstrate distinct geological storage pathways. The IEA's Net Zero scenario requires geological storage capacity expansion of 10 Billion metric tons per year globally by 2050, requiring sustained carbon storage infrastructure investment that benefits both geological sequestration specialists and DAC technology providers.

Utilization in synthetic fuels and e-fuels, where DAC-captured CO2 is combined with green hydrogen through Fischer-Tropsch or methanation processes to produce synthetic aviation fuel, synthetic methanol, or synthetic natural gas, represented 18.4% of the industrial direct air capture market in 2025. This application benefits from the EU RefuelEU Aviation regulation, which mandates increasing sustainable aviation fuel blending ratios from 2% in 2025 to 70% by 2050, creating regulatory-driven demand for e-fuel production that requires CO2 feedstock. Utilization in enhanced oil recovery, where CO2 is injected into mature oil reservoirs to improve oil recovery while sequestering a portion of the injected CO2, accounted for 10.2% of the market in 2025, primarily at Carbon Engineering's Stratos facility where Occidental uses captured CO2 for EOR in its Permian Basin operations. Construction materials mineralization and other specialty utilization applications held the remaining 6.6% of the industrial direct air capture market by end-use in 2025.

By Scale and Facility Type

The industrial direct air capture market by scale and facility type covers large-scale centralized DAC plants (above 10,000 metric tons CO2 per year), mid-scale modular DAC systems (1,000-10,000 metric tons CO2 per year), small-scale distributed DAC units (below 1,000 metric tons CO2 per year), and integrated DAC hub facilities co-located with renewable energy or industrial complex. Large-scale centralized DAC plants held the largest revenue share at 44.6% of the industrial direct air capture market in 2025, concentrated at Climeworks' Mammoth plant in Iceland (36,000 tCO2/yr) and Carbon Engineering's Stratos plant in Texas. These facilities generate the highest per-facility revenue through large CO2 capture volumes sold under long-term offtake contracts. Mid-scale modular DAC systems represented 32.4% of the market in 2025, the preferred deployment model for corporate buyers seeking to demonstrate DAC carbon removal for net-zero commitments while building operational experience before committing to gigaton-scale infrastructure investment.

Small-scale distributed DAC units held 14.8% of the industrial direct air capture market in 2025, primarily serving research, development, and demonstration purposes at university research programs, national laboratory facilities, and early-stage corporate sustainability demonstration projects. Integrated DAC hub facilities, co-located with renewable energy generation, geological storage reservoirs, or industrial complexes that provide waste heat or green hydrogen feedstock, represented the remaining 8.2% of the market by facility type in 2025. DOE's Regional DAC Hubs program specifically targets this hub facility model, with four hub projects targeting co-location with geothermal, solar, and wind energy in California, Wyoming, Montana, and Texas, where renewable electricity cost and geological storage reservoir quality combine to minimize DAC operating cost per metric ton.

By Buyer Type

The industrial direct air capture market by buyer type segments into corporate voluntary carbon removal purchasers, government program procurement, aviation and maritime industry buyers, and oil and gas industry integration. Corporate voluntary carbon removal purchasers held the largest buyer type share at 42.6% of the industrial direct air capture market in 2025. Technology companies including Stripe, Microsoft, Google, Shopify, and McKinsey have collectively committed to purchasing over 2 Million metric tons of DAC-based carbon removal credits through advance purchase agreements, establishing a private sector demand signal that has been instrumental in financing early commercial DAC facilities. Government program procurement, through DOE Regional DAC Hub awards, UK Industrial Decarbonisation Challenge grants, and EU Innovation Fund allocations, represented 34.8% of market revenues in 2025. Aviation and maritime industry buyers, purchasing DAC carbon removal credits for ICAO CORSIA compliance and voluntary sustainability commitments, accounted for 14.2%. Oil and gas industry integration for EOR and carbon credit generation held the remaining 8.4%.

Regional Analysis

North America

North America industrial direct air capture market held a 44.0% share in 2025, generating approximately USD 370 Million in revenue. The United States dominates the North American and global industrial DAC market, driven by the IRA's 45Q tax credit of USD 180 per metric ton of CO2 permanently sequestered from DAC, which provides the most financially generous government incentive for DAC deployment of any jurisdiction globally. The DOE's Regional Direct Air Capture Hubs program, which allocated USD 3.5 Billion across four hub projects in 2023-2024, is the largest single government commitment to DAC infrastructure development globally and is attracting private co-investment that multiplies its impact. Carbon Engineering's Stratos plant in Ector County, Texas, operated by Occidental Petroleum's 1PointFive subsidiary, represents the world's most ambitious commercial liquid solvent DAC deployment, targeting 500,000 metric tons of CO2 per year at full scale and demonstrating that large-scale DAC is technically and operationally viable at industrial site conditions without the geothermal energy advantage that Climeworks' Iceland facilities exploit. Heirloom Carbon's limestone calcination DAC system, located in California, received funding from US DOE and is building toward its first commercial-scale deployment targeting 20,000 metric tons per year. Canada contributes through Carbon Engineering's original technology development history and the National Research Council's carbon capture research programs. Wyoming, Montana, and Texas are emerging as preferred DAC hub sites due to their combination of low-cost renewable electricity and high-quality geological CO2 storage reservoirs.

Europe

Europe held approximately 32.4% of the global industrial direct air capture market in 2025, generating approximately USD 272 Million. Iceland is the most commercially significant national location for industrial DAC in Europe, where Climeworks' Mammoth plant benefits from abundant low-cost geothermal electricity (approximately USD 30-50 per MWh) and the Carbfix basalt rock CO2 mineralization storage system that provides permanent, verifiable CO2 storage for high-value carbon credits. Iceland's unique combination of low-cost clean energy and permanent geological CO2 storage makes it the lowest-cost proven location for permanent carbon removal globally, with Climeworks targeting long-term removal costs of USD 300 per metric ton by 2030 and USD 100 by 2035 from Icelandic operations. Switzerland is Climeworks' headquarters and the location of its Orca and earlier DAC pilot plants, where district heating and waste heat from industrial facilities provide regeneration energy for solid sorbent systems. The UK Industrial Decarbonisation Challenge has funded multiple industrial DAC research and demonstration projects, and the UK government's Net Zero Innovation Portfolio includes direct air capture as a priority technology. The EU Innovation Fund and Horizon Europe programs have collectively allocated over USD 400 Million equivalent to DAC-related projects across member states, with Germany, Netherlands, and Norway each advancing domestic DAC pilot programs. The EU Carbon Removals Certification Framework, adopted in 2024, provides the regulatory foundation for DAC-generated carbon removal credits to be used in national climate accounting and compliance carbon markets.

Asia Pacific

Asia Pacific held approximately 14.8% of the global industrial direct air capture market in 2025, generating approximately USD 124 Million. Japan leads the Asia Pacific industrial DAC market, where METI's Green Innovation Fund has allocated approximately USD 900 Million equivalent to carbon capture and utilization technologies including DAC, and major Japanese industrial companies including Mitsubishi Heavy Industries, IHI Corporation, and Toshiba are developing DAC systems for domestic and export markets. Japan's industrial decarbonization strategy specifically references DAC as a technology for addressing residual emissions in hard-to-abate sectors including steel, cement, and chemicals, creating domestic demand for large-scale commercial DAC that Japanese engineering companies are positioning to supply. Australia represents a growing Asia Pacific DAC market, where the government's Safeguard Mechanism reforms for large industrial emitters create compliance demand for carbon removal and where renewable energy resource availability supports low-cost electrolytic hydrogen and renewable electricity for DAC operations. South Korea's national carbon neutrality strategy references carbon capture and removal technologies, with government research funding supporting domestic DAC technology development at Korean universities and research institutes. China's industrial policy includes carbon capture research but has prioritized point-source CCS over atmospheric DAC in near-term deployment programs, making China a smaller near-term DAC market despite its enormous overall emission reduction scale.

Latin America

Latin America held approximately 5.2% of the global industrial direct air capture market in 2025, generating approximately USD 44 Million. Brazil is the dominant regional market, where abundant renewable energy resources including hydropower, solar, and wind at low cost provide favorable energy economics for electrochemical and sorbent-based DAC systems, and where the country's tropical basalt geology offers potential for permanent CO2 mineralization storage analogous to Iceland's basalt rock sequestration. Brazil's role as a major agricultural commodity exporter has positioned it as a potential host for carbon dioxide removal credits certified under emerging tropical land-based removal frameworks, and Brazilian energy companies are beginning to evaluate DAC as a component of net-zero compliance strategies. Chile represents a growing Latin American DAC market, where the Atacama Desert's exceptional solar irradiance of 8-9 kWh per square meter per day provides the lowest-cost solar electricity in the world, making it an attractive location for solar-powered electrochemical DAC at costs potentially competitive with geothermal-powered Icelandic facilities. Mexico's industrial decarbonization programs and growing corporate sustainability requirements from multinational manufacturers operating in Mexico are creating early-stage corporate demand for DAC-based carbon credits to support net-zero commitments. The region's overall DAC market development is constrained by the absence of domestic 45Q-equivalent financial incentives and limited regulatory frameworks for CO2 storage certification.

Middle East & Africa

The Middle East and Africa region held approximately 3.6% of the global industrial direct air capture market in 2025, generating approximately USD 30 Million. The UAE and Saudi Arabia are the primary Middle Eastern DAC markets, where national net-zero commitments by 2050 and 2060 respectively, combined with abundant solar energy resources and national oil company decarbonization programs, are driving investment in DAC feasibility studies and early-scale pilots. Masdar, the Abu Dhabi Future Energy Company, has engaged with DAC technology developers for UAE deployment evaluations, and Saudi Aramco's sustainability program includes carbon capture technology investment as a portfolio component. The region's extreme solar irradiance creates favorable long-term economics for solar-powered DAC, and the availability of depleted hydrocarbon reservoirs for CO2 geological storage at scale provides accessible carbon storage infrastructure. Saudi Arabia's CCUS program under Vision 2030 specifically targets 44 Million metric tons per year of carbon capture and storage capacity by 2035, creating a policy framework that could eventually encompass industrial DAC at commercial scale. South Africa represents the leading African industrial DAC market, where the country's carbon tax system creates a regulatory price signal for carbon removal, and academic research programs at universities including Wits and UCT are advancing DAC material science research.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Capture Technology

- Solid Sorbent-Based DAC

- Liquid Solvent-Based DAC

- Electrochemical DAC

- Mineralization-Based DAC

By End-Use CO2 Application

- Geological Storage & Permanent Sequestration

- Utilization in Synthetic Fuels & E-Fuels

- Enhanced Oil Recovery (EOR)

- Construction Materials Mineralization & Specialty Utilization

By Scale and Facility Type

- Large-Scale Centralized DAC Plants (Above 10,000 tCO2/yr)

- Mid-Scale Modular DAC Systems (1,000-10,000 tCO2/yr)

- Small-Scale Distributed DAC Units (Below 1,000 tCO2/yr)

- Integrated DAC Hub Facilities

By Buyer Type

- Corporate Voluntary Carbon Removal Purchasers

- Government Program Procurement

- Aviation & Maritime Industry Buyers

- Oil & Gas Industry Integration

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 0.84 B |

| Forecast Revenue (2034) | USD 7.62 B |

| CAGR (2025-2034) | 27.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Capture Technology, (Solid Sorbent-Based DAC, Liquid Solvent-Based DAC, Electrochemical DAC, Mineralization-Based DAC), By End-Use CO2 Application, (Geological Storage & Permanent Sequestration, Utilization in Synthetic Fuels & E-Fuels, Enhanced Oil Recovery (EOR), Construction Materials Mineralization & Specialty Utilization), By Scale and Facility Type, (Large-Scale Centralized DAC Plants (Above 10,000 tCO2/yr), Mid-Scale Modular DAC Systems (1,000-10,000 tCO2/yr), Small-Scale Distributed DAC Units (Below 1,000 tCO2/yr), Integrated DAC Hub Facilities), By Buyer Type, (Corporate Voluntary Carbon Removal Purchasers, Government Program Procurement, Aviation & Maritime Industry Buyers, Oil & Gas Industry Integration) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CLIMEWORKS AG, CARBON ENGINEERING (1POINTFIVE/OCCIDENTAL), HEIRLOOM CARBON, VERDOX INC., GLOBAL THERMOSTAT, SUSTAERA, MISSION ZERO TECHNOLOGIES, CARBYON, REPAI, CARBFIX (REYKJAVIK ENERGY), GRAPHYTE (CARBON CASTING DAC), ORIGEN CARBON, AIRHIVE (FORMERLY ATMO CAPTURE), OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use CO2 Application (Geological Storage, Synthetic Fuels & E-Fuels, Enhanced Oil Recovery, Construction Materials), By Scale & Facility Type (Large-Scale, Modular, Distributed, DAC Hubs) Industry Trends & Forecast 2026–2034")

, By End-Use CO2 Application (Geological Storage, Synthetic Fuels & E-Fuels, Enhanced Oil Recovery, Construction Materials), By Scale & Facility Type (Large-Scale, Modular, Distributed, DAC Hubs) Industry Trends & Forecast 2026–2034")

, By End-Use CO2 Application (Geological Storage, Synthetic Fuels & E-Fuels, Enhanced Oil Recovery, Construction Materials), By Scale & Facility Type (Large-Scale, Modular, Distributed, DAC Hubs) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Industrial Direct Air Capture Market?

Global Direct air capture market valued at USD 0.66B in 2024, reaching USD 7.62B by 2034, growing at a CAGR of 27.7% from 2026–2034.

Who are the major players in the Industrial Direct Air Capture Market?

CLIMEWORKS AG, CARBON ENGINEERING (1POINTFIVE/OCCIDENTAL), HEIRLOOM CARBON, VERDOX INC., GLOBAL THERMOSTAT, SUSTAERA, MISSION ZERO TECHNOLOGIES, CARBYON, REPAI, CARBFIX (REYKJAVIK ENERGY), GRAPHYTE (CARBON CASTING DAC), ORIGEN CARBON, AIRHIVE (FORMERLY ATMO CAPTURE), OTHERS

Which segments covered the Industrial Direct Air Capture Market?

By Capture Technology, (Solid Sorbent-Based DAC, Liquid Solvent-Based DAC, Electrochemical DAC, Mineralization-Based DAC), By End-Use CO2 Application, (Geological Storage & Permanent Sequestration, Utilization in Synthetic Fuels & E-Fuels, Enhanced Oil Recovery (EOR), Construction Materials Mineralization & Specialty Utilization), By Scale and Facility Type, (Large-Scale Centralized DAC Plants (Above 10,000 tCO2/yr), Mid-Scale Modular DAC Systems (1,000-10,000 tCO2/yr), Small-Scale Distributed DAC Units (Below 1,000 tCO2/yr), Integrated DAC Hub Facilities), By Buyer Type, (Corporate Voluntary Carbon Removal Purchasers, Government Program Procurement, Aviation & Maritime Industry Buyers, Oil & Gas Industry Integration)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Industrial Direct Air Capture Market

Published Date : 24 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date