- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Industrial Waste Heat Recovery Market Size, Share | CAGR of 7.2%

Global Industrial Waste Heat Recovery Market Size, Share, Analysis By Application (Steam & Power Generation, Heating, Preheating), By Technology (Heat Exchangers, ORC, Kalina Cycle, Heat Pumps), By Temperature (Low, Medium, High), By End-Use (Oil & Gas, Chemical, Cement, Iron & Steel, Glass, Food & Beverage, Power Gen) Region, Key Players – Dynamics, Strategies, Sustainable Energy & Carbon Reduction Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 68.40 Billion | USD 127.60 Billion | 7.2% | Asia Pacific, 41.3% |

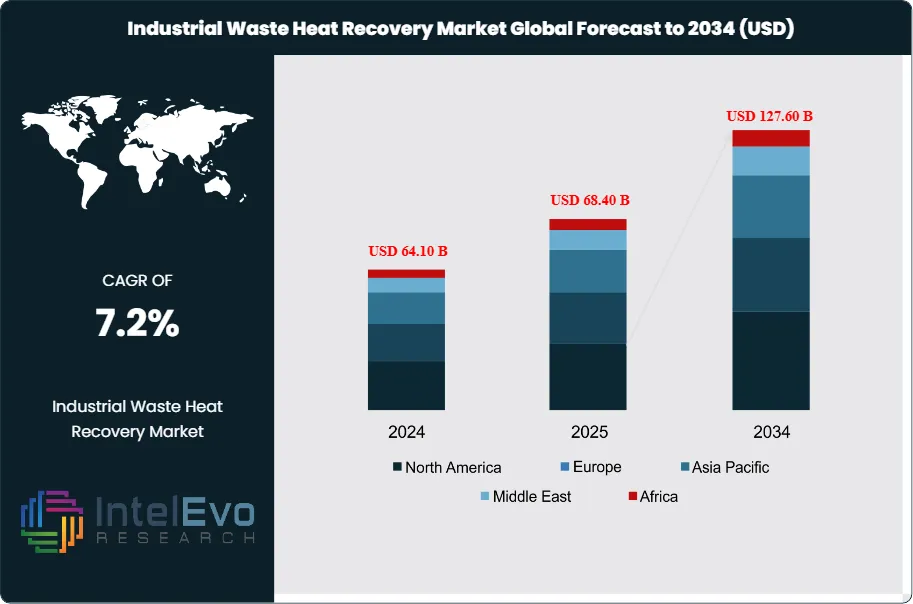

The Industrial Waste Heat Recovery Market was valued at USD 64.10 Billion in 2024 and reached USD 68.40 Billion in 2025. The market is projected to grow to USD 127.60 Billion by 2034, registering a CAGR of 7.2% during the forecast period 2026–2034. This represents an absolute dollar opportunity of USD 59.20 Billion over the analysis period.

Get More Information about this report -

Request Free Sample ReportIndustrial waste heat recovery demand is anchored by energy-intensive production in steel, cement, chemicals, refining, pulp and paper, glass, and food processing. The International Energy Agency reported that industry accounted for nearly 40% of total final energy consumption in 2024, while the U.S. Department of Energy states that 20% to 50% of industrial energy input can leave facilities as exhaust gas, cooling water, hot surfaces, or heated products. That loss pool converts industrial waste heat recovery from a sustainability option into a cost-control system for plants facing power-price volatility.

Regulation is moving procurement from voluntary retrofits toward compliance-linked capital planning. The EU Carbon Border Adjustment Mechanism shifted from the 2023-2025 transitional phase to the definitive 2026 regime, affecting steel, cement, aluminium, fertilisers, electricity, hydrogen, and downstream materials. The revised EU ETS links free allowance treatment to decarbonisation actions from 2026, which improves the payback logic for waste heat boilers, organic Rankine cycle units, high-temperature heat pumps, and economizers in export-oriented plants.

Technology selection is splitting by temperature grade. High-grade flue gas above 400 degrees Celsius supports waste heat recovery boilers, heat recovery steam generators, and ORC power units supplied by Siemens Energy, Thermax, Mitsubishi Heavy Industries, Turboden, and Ormat Technologies. Low-grade heat below 150 degrees Celsius is shifting toward industrial heat pumps, mechanical vapor recompression, and absorption heat pumps supplied by Johnson Controls, MAN Energy Solutions, Alfa Laval, and Mitsubishi Heavy Industries Thermal Systems because heat-to-heat reuse avoids power-conversion losses.

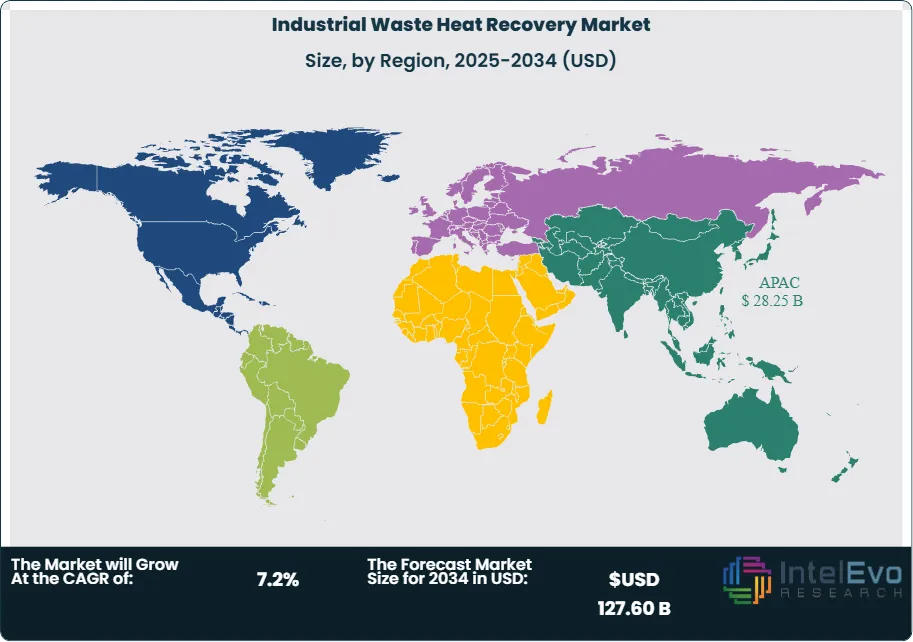

Asia Pacific held 41.3% of the industrial waste heat recovery market in 2025, equal to USD 28.25 Billion, because China and India combine the largest steel, cement, chemicals, and refining capacity additions. North America and Europe remain high-value retrofit regions because the U.S. Department of Energy 48C program, EU ETS, CBAM, and national heat-transition policies make recovered heat bankable. Through 2034, the most attractive projects will be those where recovered heat displaces purchased electricity, reduces fuel input, or monetizes heat through district networks and captive power contracts.

Market Definition & Scope

The industrial waste heat recovery market is defined as the global commercial activity around systems that capture, transfer, upgrade, store, or convert thermal energy that would otherwise be discharged from industrial processes. The market encompasses waste heat recovery boilers, heat recovery steam generators, recuperators, regenerators, economizers, organic Rankine cycle systems, heat exchangers, absorption chillers, industrial heat pumps, mechanical vapor recompression systems, and control software used in manufacturing and process industries.

This analysis includes equipment, engineering services, integration, controls, aftermarket maintenance, and project-specific balance-of-plant supplied to steel, cement, chemicals, refining, glass, pulp and paper, food processing, and industrial power facilities. It excludes residential heat recovery ventilation, automotive exhaust heat recovery, building-only HVAC recovery, municipal wastewater heat recovery without industrial offtake, and general combined heat and power assets that do not recover waste process heat. The industrial waste heat recovery market sits inside the broader industrial energy efficiency and process heat decarbonisation category.

, By Technology (Heat Exchangers, ORC, Kalina Cycle, Heat Pumps), By Temperature (Low, Medium, High), By End-Use (Oil & Gas, Chemical, Cement, Iron & Steel, Glass, Food & Beverage, Power Gen) Region, Key Players – Dynamics, Strategies, Sustainable Energy & Carbon Reduction Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The industrial waste heat recovery market expanded from USD 68.40 Billion in 2025 toward a projected USD 127.60 Billion by 2034 at a 7.2% CAGR, creating USD 59.20 Billion in absolute dollar opportunity.

- Segment Dominance: Steam generation held 38.4% of application revenue in 2025, equal to USD 26.27 Billion, because boilers and HRSG systems convert high-grade exhaust into process steam.

- Segment Dominance: Steel, cement, and metals processing led end-use demand with 34.5% share in 2025, equal to USD 23.60 Billion, due to kiln, furnace, and reheating-line exhaust intensity.

- Driver: Energy-cost exposure is the primary driver, since DOE technical guidance indicates that 20% to 50% of industrial energy input can be lost as waste heat in process plants.

- Restraint: Retrofit complexity limits adoption when heat source and heat sink timing differ, with paybacks extending beyond 5 years in plants lacking continuous operation.

- Opportunity: Asia Pacific represents the largest opportunity at USD 28.25 Billion in 2025 and an estimated USD 57.51 Billion by 2034 as China and India add industrial heat demand.

- Trend: High-temperature industrial heat pumps are moving from pilot projects to plant retrofits, with Mitsubishi Heavy Industries launching a 90 degrees Celsius ETI-W unit in October 2025.

- Regional: Asia Pacific led the industrial waste heat recovery market with 41.3% share and USD 28.25 Billion in 2025, followed by North America at 24.0%.

Key Insights Summary

- The International Energy Agency reported industrial final energy consumption near 40% of global final demand in 2024, making process heat the largest addressable base for industrial energy efficiency systems.

- The U.S. Department of Energy estimates that 20% to 50% of energy input in industrial facilities is lost as waste heat through exhaust gas, cooling water, equipment surfaces, and heated products.

- Industrial heat demand is projected by the International Energy Agency to grow 14%, or about 16 EJ, globally during 2025-2030, with China and India accounting for more than half of incremental demand.

- India's cement industry can replace energy equal to 8.6 million tonnes of coal at full waste heat recovery potential, which would avoid about 12.8 million tonnes of CO2 emissions.

- Turboden stated in April 2026 that it secured six cement-industry ORC projects during 2024-2025 with combined capacity above 35 MW, showing renewed demand for power-from-heat in cement plants.

- Mitsubishi Heavy Industries Thermal Systems introduced the ETI-W centrifugal heat pump in October 2025, supplying hot water up to 90 degrees Celsius from low-temperature industrial waste heat.

- The U.S. Treasury and IRS allocated USD 6.00 Billion in second-round 48C tax credits in January 2025, with roughly USD 2.50 Billion directed to energy-community projects.

Competitive Landscape Overview

The industrial waste heat recovery market is moderately consolidated, with Siemens Energy, ABB Ltd., Alfa Laval AB, and Mitsubishi Heavy Industries together representing an estimated 31% of equipment-led activity in 2025. Competition is technology-based in high-temperature applications and integration-based in low-temperature applications, where heat pumps, automation, and process controls determine operating savings.

Project awards increasingly depend on bankable performance guarantees rather than equipment price alone. Siemens Energy competes through HRSG, compression, turbine, and industrial heat-decarbonisation capability; ABB provides automation, drives, motors, and electrification that reduce auxiliary energy use; Alfa Laval leads in plate heat exchangers and process heat transfer; and Mitsubishi Heavy Industries links Turboden ORC technology with heat pumps and industrial power systems. Apollo's August 2025 agreement to acquire Kelvion indicates investor interest in heat exchanger platforms with exposure to data centres, power, chemicals, and waste heat recovery.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Siemens Energy AG | Germany | Leader | HRSG, steam turbines, industrial heat decarbonisation systems | Europe, North America, Middle East | Reported FY2025 profit before special items of EUR 2.36 Billion and expanded low-carbon industrial heat positioning |

| ABB Ltd. | Switzerland | Leader | Motors, drives, automation, electrification, energy management | Global | Joined Energy Impact Partners in December 2025 to screen energy-transition technologies |

| Alfa Laval AB | Sweden | Leader | Plate heat exchangers, welded heat exchangers, evaporation systems | Europe, North America, Asia Pacific | Expanded process heat and energy-efficiency positioning across industrial and district-energy applications |

| Mitsubishi Heavy Industries, Ltd. | Japan | Leader | Turboden ORC, ETI-W heat pump, industrial power systems | Asia Pacific, Europe, North America | Introduced ETI-W heat pump in October 2025 and advanced Turboden ORC waste-heat projects |

| Turboden S.p.A. | Italy | Challenger | Organic Rankine cycle waste-heat-to-power systems | Europe, Asia Pacific, North America | Started up AGC Thailand ORC unit in April 2026 after Canada SAGD commissioning in October 2025 |

| Ormat Technologies, Inc. | United States | Challenger | Recovered energy generation and binary-cycle equipment | North America, Latin America, Asia | Closed USD 88 Million Blue Mountain acquisition in June 2025, strengthening binary-cycle operating scale |

| Thermax Limited | India | Challenger | Waste heat recovery boilers, absorption chillers, EPC systems | India, Southeast Asia, Middle East, Africa | Expanded industrial decarbonisation offerings for cement, refining, and chemical customers |

| Kelvion Holding GmbH | Germany | Challenger | Heat exchangers, heat recovery and cooling systems | Europe, Americas, Asia Pacific | Apollo agreed to acquire a majority stake in August 2025; Kelvion introduced K°Focus CCS in January 2026 |

| Johnson Controls International plc | Ireland / United States | Challenger | Industrial heat pumps, HVAC heat recovery, district heat systems | Europe, North America | Supported waste-heat heat-pump projects in Zurich and Bavaria during 2025 |

| MAN Energy Solutions SE | Germany | Niche Player | Large-scale industrial heat pumps and CHP integration | Europe, Middle East | Continued deployment of large heat-pump systems for district and industrial heat applications |

Segmentation Analysis

The industrial waste heat recovery market segments by application, technology, temperature grade, and end-use industry, with project economics shaped by operating hours, heat quality, and the ability to reuse heat on site.

By Application

The industrial waste heat recovery market by application is led by steam generation, which held 38.4% share and USD 26.27 Billion in 2025. Waste heat boilers and HRSG units convert kiln exhaust, furnace exhaust, gas turbine exhaust, and process off-gas into steam for refining, chemicals, pulp and paper, and food processing. Siemens Energy, Thermax, Babcock & Wilcox, and Mitsubishi Heavy Industries benefit because steam networks already exist in many plants, reducing integration risk. Steam projects often outrank power-generation projects when natural gas prices are high because recovered steam directly cuts boiler fuel.

Preheating accounted for 28.8% share, equal to USD 19.70 Billion in 2025, across combustion air preheaters, feedwater economizers, charge preheaters, and raw-material drying. ABB, Alfa Laval, Kelvion, and Forbes Marshall compete in this application through heat exchangers, motors, variable-speed drives, and control packages that reduce parasitic losses. Preheating projects usually have shorter implementation timelines than ORC systems because they need fewer grid-interconnection approvals and less rotating equipment.

Power generation captured 21.6% share, equivalent to USD 14.77 Billion in 2025, led by ORC units, steam Rankine systems, and recovered energy generation. Turboden, Ormat Technologies, Dürr, and Kaishan target cement kilns, glass furnaces, compressor stations, SAGD facilities, and steel mills where waste heat is continuous enough to support capacity-factor guarantees. The remaining 11.2% share, or USD 7.66 Billion, includes absorption cooling, district heat export, drying, and hot-water supply.

By Technology

The industrial waste heat recovery market by technology is led by heat exchangers, recuperators, regenerators, and economizers at 36.0% share, equal to USD 24.62 Billion in 2025. Alfa Laval, Kelvion, API Heat Transfer, and Xylem compete through thermal efficiency, fouling tolerance, metallurgy, and serviceability. These systems dominate low- and medium-complexity retrofits because they reuse heat without changing the plant's power architecture.

Waste heat boilers and HRSG systems represented 27.0% share, or USD 18.47 Billion in 2025. Siemens Energy, Thermax, John Cockerill, Babcock & Wilcox, and Mitsubishi Heavy Industries hold stronger positions in refining, petrochemicals, cement, glass, and combined industrial power plants. Organic Rankine cycle systems captured 14.0% share, equal to USD 9.58 Billion, and are used where low-boiling-point working fluids convert medium-temperature heat into electricity. Turboden's 2025-2026 projects in SAGD, glass, and cement illustrate the technology's appeal where water use, maintenance, and variable loads challenge steam-cycle systems.

Industrial heat pumps, absorption heat pumps, and mechanical vapor recompression held 13.0% share, equal to USD 8.89 Billion in 2025, but they are the fastest-moving technology group through 2034. Johnson Controls, MAN Energy Solutions, GEA, MHI Thermal Systems, and Heaten target food, chemicals, paper, district heat, and steel sites where low-grade waste heat can be upgraded into process hot water or steam. Other technologies, including thermal storage and advanced controls, represented 10.0% share.

By Temperature Grade

High-grade waste heat above 400 degrees Celsius accounted for 44.0% of the industrial waste heat recovery market in 2025, equal to USD 30.10 Billion. Cement kilns, glass furnaces, steel reheating furnaces, petrochemical crackers, and refinery heaters provide predictable thermal sources for boilers, preheaters, and power-generation equipment. Procurement teams prioritize refractory durability, fouling management, and shutdown-window planning in this temperature class.

Medium-grade waste heat between 150 and 400 degrees Celsius held 35.0% share, or USD 23.94 Billion, across exhaust streams, dryer exhaust, compressor systems, and process condensate. This grade is attractive for ORC, economizers, absorption chillers, and direct process reuse because it balances usable exergy with manageable materials cost. Low-grade heat below 150 degrees Celsius held 21.0% share, equal to USD 14.36 Billion, and is gaining attention as high-temperature heat pumps, MVR, and district heating connections allow plants to monetize heat that was previously vented.

By End-Use Industry

Steel, cement, and metals led the industrial waste heat recovery market by end-use industry with 34.5% share and USD 23.60 Billion in 2025. Cement kilns and clinker coolers support WHR power plants, while electric arc furnaces, reheating furnaces, and rolling mills offer preheating and steam opportunities. Turboden, Thermax, Siemens Energy, ABB, and Mitsubishi Heavy Industries compete for these projects because energy intensity and carbon exposure make plant owners more willing to finance retrofit capex.

Chemicals, refining, and petrochemicals held 26.5% share, equivalent to USD 18.13 Billion in 2025. Refineries use waste heat boilers, feedwater economizers, steam integration, and heat exchanger networks to reduce fuel gas demand and flaring intensity. Chemicals sites add heat pumps and MVR when evaporation, distillation, and drying create low-grade heat streams. Pulp and paper, food and beverage, glass, and other industries represented the remaining 39.0% share, with higher growth in food processing because electrified heat and hot-water reuse help manufacturers reduce Scope 1 emissions.

Regional Analysis

Asia Pacific led the industrial waste heat recovery market with 41.3% share and USD 28.25 Billion in 2025. China accounted for about USD 14.50 Billion, India for USD 4.00 Billion, Japan for USD 2.35 Billion, and South Korea for USD 1.85 Billion. Demand is driven by steel, cement, chemicals, glass, and electronics supply chains facing electricity-cost pressure and carbon-trade exposure. China's dual-carbon targets and India's Perform, Achieve and Trade framework encourage projects that reduce specific energy consumption. Mitsubishi Heavy Industries' October 2025 ETI-W launch and NEC, Fuji Electric, Thermax, and Forbes Marshall activity keep regional technology supply deep.

North America held 24.0% share of the industrial waste heat recovery market in 2025, equal to USD 16.42 Billion. The United States represented roughly USD 14.00 Billion, with Canada at USD 1.70 Billion and Mexico at USD 0.72 Billion. DOE industrial efficiency resources, the 48C tax credit program, the Industrial Demonstrations Program, and state-level manufacturing decarbonisation incentives support retrofit economics. Turboden commissioned the North American SAGD ORC project at Strathcona's Orion facility in October 2025, proving that oil sands and heavy industrial sites can convert process heat into on-site power.

Europe captured 23.0% share and USD 15.73 Billion in 2025, led by Germany, Italy, France, the United Kingdom, Spain, and the Nordics. EU ETS allowance pressure, CBAM, national district heating policies, and industrial heat electrification programs make the region a high-value retrofit market. Johnson Controls' waste heat projects in Zurich and Bavaria, Heaten's November 2025 selection for the EU HURRICANE project at ArcelorMittal Ghent, and Kelvion's January 2026 carbon capture heat-exchanger platform show how European demand is shifting toward integrated heat reuse rather than equipment-only replacement.

Latin America accounted for 6.5% share, equal to USD 4.45 Billion in 2025. Brazil, Mexico, Chile, and Argentina are the principal markets, with cement, mining, refining, pulp and paper, and food processing driving demand. Electricity-price volatility and hydro-generation swings strengthen the business case for captive power from waste heat. Middle East and Africa held 5.2% share, equal to USD 3.56 Billion, led by Saudi Arabia, the United Arab Emirates, South Africa, Egypt, and Turkey. Refining, petrochemicals, cement, aluminium, and desalination-linked industrial heat applications support regional adoption.

Country Analysis

The United States industrial waste heat recovery market reached approximately USD 14.00 Billion in 2025 and is forecast to grow at a 6.8% country CAGR through 2034. Demand is concentrated in refining, chemicals, steel, food processing, cement, and oil and gas production. The DOE 48C program, industrial efficiency guidance, and state manufacturing grants improve project economics where recovered steam or power displaces purchased energy. Ormat Technologies reported USD 989.6 Million in 2025 revenue and maintained recovered energy generation capabilities, while Turboden's 2025 SAGD project and Tallgrass-linked 2026 waste-heat-to-power selections point to renewed U.S. pipeline and oilfield demand.

China's industrial waste heat recovery market reached approximately USD 14.50 Billion in 2025 and is projected to grow at an 8.2% CAGR through 2034. Steel, cement, chemicals, glass, and aluminium plants anchor demand because China's industrial base has both high heat intensity and policy pressure under dual-carbon targets. Domestic suppliers compete with Siemens Energy, ABB, Alfa Laval, and Mitsubishi Heavy Industries on price and local service. Procurement decisions emphasize payback periods under 3 years, local heat-exchanger fabrication, and compatibility with provincial energy-intensity controls.

Germany's industrial waste heat recovery market reached approximately USD 4.20 Billion in 2025 and is forecast to expand at a 6.5% CAGR through 2034. Chemicals, refining, glass, automotive, paper, and district heating networks drive demand. EU ETS, CBAM, and Germany's industrial transformation funding improve economics for heat pumps, steam integration, and process electrification. Siemens Energy, MAN Energy Solutions, Kelvion, GEA, and Bosch provide domestic engineering depth, while Johnson Controls and Nestle's Bavaria heat-pump example demonstrates food-industry adoption.

India's industrial waste heat recovery market reached approximately USD 4.00 Billion in 2025 and is projected to grow at a 9.0% CAGR through 2034. Cement, steel, aluminium, chemicals, refineries, and pulp and paper plants are priority end-users under the Perform, Achieve and Trade scheme. Indian cement-sector analysis indicates that full WHR potential could replace energy equal to 8.6 million tonnes of coal and avoid 12.8 million tonnes of CO2. Thermax, Forbes Marshall, ABB India, Siemens India, and domestic EPC firms compete on capex discipline, local service, and financing support.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Application

- Steam Generation

- Power Generation

- Process Heating

- Preheating

- Others

By Technology

- Heat Exchangers

- Organic Rankine Cycle (ORC)

- Kalina Cycle

- Heat Pumps

- Thermoelectric Generators

- Others

By Temperature Grade

- Low Temperature (<230°C)

- Medium Temperature (230°C–650°C)

- High Temperature (>650°C)

By End-Use Industry

- Oil & Gas

- Chemical & Petrochemical

- Cement

- Iron & Steel

- Glass

- Pulp & Paper

- Food & Beverage

- Power Generation

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2026) | USD 68.40 B |

| Forecast Revenue (2034) | USD 127.60 B |

| CAGR (2026-2034) | 7.2% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Application, (Steam Generation, Power Generation, Process Heating, Preheating, Others), By Technology, (Heat Exchangers, Organic Rankine Cycle (ORC), Kalina Cycle, Heat Pumps, Thermoelectric Generators, Others), By Temperature Grade, (Low Temperature (<230°C), Medium Temperature (230°C–650°C), High Temperature (>650°C)), By End-Use Industry, (Oil & Gas, Chemical & Petrochemical, Cement, Iron & Steel, Glass, Pulp & Paper, Food & Beverage, Power Generation, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SIEMENS ENERGY AG, ABB LTD., ALFA LAVAL AB, MITSUBISHI HEAVY INDUSTRIES, LTD., TURBODEN S.P.A., ORMAT TECHNOLOGIES, INC., THERMAX LIMITED, KELVION HOLDING GMBH, JOHNSON CONTROLS INTERNATIONAL PLC, MAN ENERGY SOLUTIONS SE, GEA GROUP AG, BABCOCK & WILCOX ENTERPRISES, INC., JOHN COCKERILL, FORBES MARSHALL, DÜRR AG, CLIMEON AB, HEATEN AS, KAISHAN GROUP CO., LTD., OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Heat Exchangers, ORC, Kalina Cycle, Heat Pumps), By Temperature (Low, Medium, High), By End-Use (Oil & Gas, Chemical, Cement, Iron & Steel, Glass, Food & Beverage, Power Gen) Region, Key Players – Dynamics, Strategies, Sustainable Energy & Carbon Reduction Trends & Forecast 2026-2034")

, By Technology (Heat Exchangers, ORC, Kalina Cycle, Heat Pumps), By Temperature (Low, Medium, High), By End-Use (Oil & Gas, Chemical, Cement, Iron & Steel, Glass, Food & Beverage, Power Gen) Region, Key Players – Dynamics, Strategies, Sustainable Energy & Carbon Reduction Trends & Forecast 2026-2034")

, By Technology (Heat Exchangers, ORC, Kalina Cycle, Heat Pumps), By Temperature (Low, Medium, High), By End-Use (Oil & Gas, Chemical, Cement, Iron & Steel, Glass, Food & Beverage, Power Gen) Region, Key Players – Dynamics, Strategies, Sustainable Energy & Carbon Reduction Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Industrial Waste Heat Recovery Market?

The global industrial waste heat recovery market was valued at USD 64.10 Billion in 2024 and USD 68.40 Billion in 2025, reaching USD 127.60 Billion by 2034 at a CAGR of 7.2%. Explore market trends, growth drivers, opportunities, technologies, and industry analysis.

Who are the major players in the Industrial Waste Heat Recovery Market?

SIEMENS ENERGY AG, ABB LTD., ALFA LAVAL AB, MITSUBISHI HEAVY INDUSTRIES, LTD., TURBODEN S.P.A., ORMAT TECHNOLOGIES, INC., THERMAX LIMITED, KELVION HOLDING GMBH, JOHNSON CONTROLS INTERNATIONAL PLC, MAN ENERGY SOLUTIONS SE, GEA GROUP AG, BABCOCK & WILCOX ENTERPRISES, INC., JOHN COCKERILL, FORBES MARSHALL, DÜRR AG, CLIMEON AB, HEATEN AS, KAISHAN GROUP CO., LTD., OTHERS

Which segments covered the Industrial Waste Heat Recovery Market?

By Application, (Steam Generation, Power Generation, Process Heating, Preheating, Others), By Technology, (Heat Exchangers, Organic Rankine Cycle (ORC), Kalina Cycle, Heat Pumps, Thermoelectric Generators, Others), By Temperature Grade, (Low Temperature (<230°C), Medium Temperature (230°C–650°C), High Temperature (>650°C)), By End-Use Industry, (Oil & Gas, Chemical & Petrochemical, Cement, Iron & Steel, Glass, Pulp & Paper, Food & Beverage, Power Generation, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Industrial Waste Heat Recovery Market

Published Date : 13 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date