- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Ingestible Sensor Market Size, Share & Forecast | CAGR 17.6%

Global Ingestible Sensor Market Size, Share, Growth Analysis By Product Type (Capsule Endoscopy Systems, Smart Pills for Medication Adherence, Physiological Monitoring Capsules, Ingestible Biosensor Platforms), By Application (GI Disease Diagnosis, Medication Adherence, Drug Delivery, Clinical Research), By End-User, By Technology (RF, BLE, NFC, Ultrasound Communication), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 1.47 Billion | USD 6.31 Billion | 17.6% | North America, 43.5% |

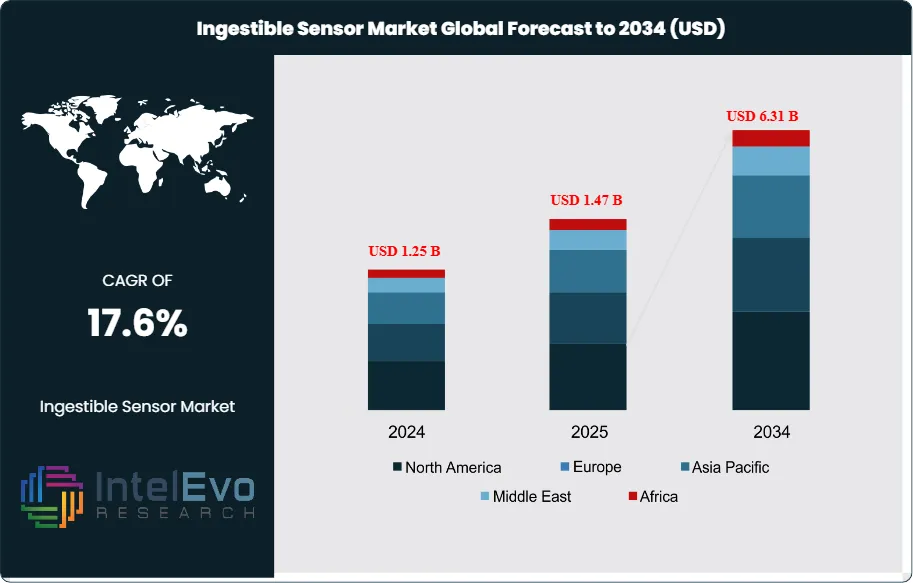

The Ingestible Sensor Market was valued at approximately USD 1.25 Billion in 2024 and reached USD 1.47 Billion in 2025. The market is projected to grow to USD 6.31 Billion by 2034, expanding at a CAGR of 17.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 4.84 Billion over the analysis period, underpinned by convergent advances in miniaturized electronics, biodegradable materials, wireless communication protocols, and clinical demand for continuous, non-invasive physiological monitoring from within the gastrointestinal tract and beyond.

Get More Information about this report -

Request Free Sample ReportIngestible sensors are swallowable electronic devices designed to transmit physiological, biochemical, or medication adherence data from inside the body to external receivers in real time or via stored retrieval. The technology spans capsule endoscopy systems for gastrointestinal imaging, smart pills for medication adherence tracking, physiological monitoring capsules measuring core body temperature and luminal pH, and emerging diagnostic biosensors capable of detecting biomarkers including tumor necrosis factor-alpha, calprotectin, and gastrointestinal microbiome metabolites. The commercial product spectrum extends from well-established FDA-cleared capsule endoscopy platforms generating substantial recurring revenue from disposable capsule sales to early-stage implantable-adjacent ingestible platforms in Phase II and III clinical validation.

The clinical rationale for ingestible sensor adoption is strong and multi-dimensional. Gastrointestinal disorders including colorectal cancer, Crohn’s disease, ulcerative colitis, and obscure gastrointestinal bleeding affect a combined patient population exceeding 100 million in OECD countries. Traditional endoscopy, while the diagnostic gold standard, is invasive, resource-intensive, and inaccessible in underserved geographies. Ingestible sensor platforms provide non-invasive or minimally invasive diagnostic coverage across the small bowel and colon where standard endoscopy is technically limited, reducing the diagnostic gap for obscure GI bleeding, Crohn’s disease monitoring, and colorectal cancer screening in populations unwilling or unable to undergo conventional colonoscopy. The World Gastroenterology Organisation and the American Gastroenterological Association have incorporated capsule endoscopy into clinical practice guidelines for obscure gastrointestinal bleeding and small bowel evaluation, embedding the technology in standard-of-care pathways.

Medication adherence monitoring represents a distinct and high-growth commercial segment. The FDA’s 2017 approval of Abilify MyCite, the first digital medicine incorporating an ingestible sensor for medication ingestion confirmation, opened a regulatory pathway that has subsequently attracted pharmaceutical company interest across psychiatric, cardiovascular, and transplant medicine applications. Non-adherence to prescribed medication regimens is estimated to cost the US healthcare system over USD 300 Billion annually in preventable hospital admissions and disease complications, creating a payer and pharmaceutical industry rationale for ingestible adherence monitoring that extends well beyond niche applications.

The ingestible sensor market intersects materially with the broader digital health, remote patient monitoring, and precision diagnostics sectors. Strategic partnerships between device manufacturers and pharmaceutical companies, telecommunications platforms, and cloud analytics providers are creating integrated data ecosystems that extend value beyond the hardware capsule into subscription-based monitoring services. Asia Pacific is emerging as the highest-growth regional market through the forecast period, supported by high colorectal cancer incidence in East Asia, government-sponsored endoscopy replacement programs in China, and advanced domestic manufacturing capability in China and Japan.

, By Application (GI Disease Diagnosis, Medication Adherence, Drug Delivery, Clinical Research), By End-User, By Technology (RF, BLE, NFC, Ultrasound Communication), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global ingestible sensor market was valued at USD 1.47 Billion in 2025 and is projected to reach USD 6.31 Billion by 2034, growing at a CAGR of 17.6% during the forecast period 2026–2034.

- Segment Dominance: By product type, capsule endoscopy systems account for the largest share at approximately 52.3% of market revenue in 2025, driven by widespread clinical adoption for small bowel evaluation and growing use in colorectal cancer screening programs.

- Segment Dominance: By application, gastrointestinal disease diagnosis and monitoring represents the dominant application segment at approximately 61.4% of market revenue in 2025, reflecting the established clinical utility of ingestible imaging and pH monitoring in GI gastroenterology practice.

- Driver: Rising global prevalence of gastrointestinal disorders, with colorectal cancer incidence exceeding 1.9 million new cases annually per WHO data and Crohn’s disease affecting over 3.4 million patients in North America and Europe combined, sustains strong diagnostic demand that conventional endoscopy capacity cannot fully address.

- Restraint: High per-capsule costs ranging from USD 400 to USD 800 for capsule endoscopy systems, combined with limited reimbursement coverage for next-generation ingestible sensor applications beyond established GI indications, restrict adoption rates in community gastroenterology and emerging market healthcare settings.

- Opportunity: Ingestible biosensors for real-time gastrointestinal biomarker detection, including inflammatory markers such as calprotectin and microbiome metabolites, represent an addressable opportunity exceeding USD 1.1 Billion by 2034, as pharmaceutical companies and gastroenterologists seek non-invasive monitoring tools for biologic therapy response assessment.

- Trend: AI-powered automated image reading for capsule endoscopy videos, adopted in approximately 34% of commercial capsule endoscopy deployments in 2025, is reducing physician reading time per study by 40% to 60% and improving lesion detection sensitivity, fundamentally shifting the economics of capsule endoscopy workflow.

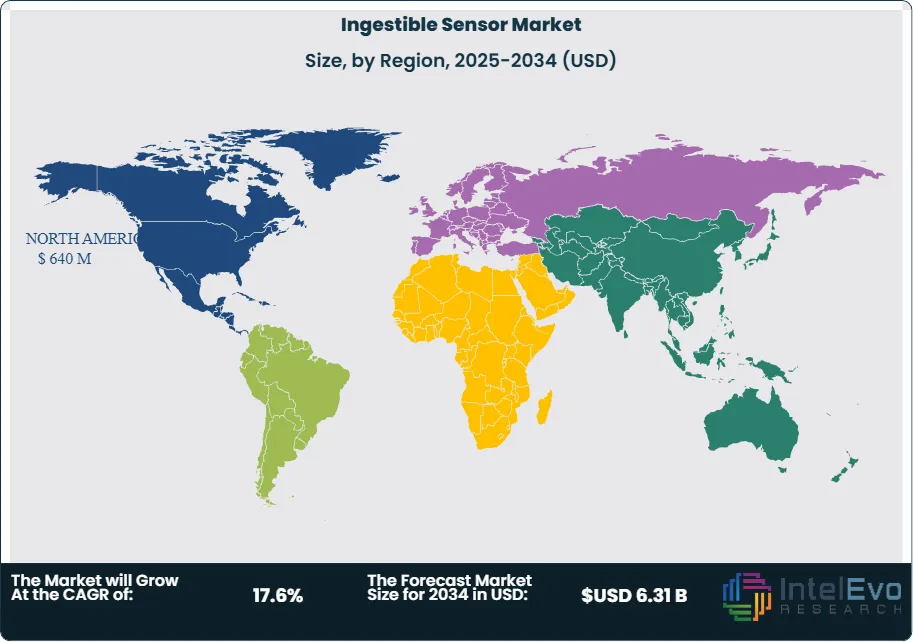

- Regional Analysis: North America leads with a 43.5% regional share, equivalent to approximately USD 640 Million in 2025, supported by FDA clearance pathways for ingestible devices, strong gastroenterology practice density, and reimbursement coverage for capsule endoscopy under Medicare and commercial payers.

Competitive Landscape Overview

The global ingestible sensor market is moderately consolidated in the capsule endoscopy segment, with the top four companies controlling approximately 72% of revenue in 2025. The medication adherence and physiological monitoring segments remain fragmented, with numerous clinical-stage and early-commercial vendors competing on technology differentiation and pharmaceutical partnership alignment. Competition in capsule endoscopy is driven by image resolution, battery life, capsule size, AI-assisted reading software, and gastroenterology practice workflow integration. Acquisition activity has been selective, with large GI device companies acquiring AI reading platform capabilities to defend installed base positions against software-differentiated challengers. Entry barriers are high due to FDA and CE clearance requirements, clinical validation costs, and the capital-intensive nature of building gastroenterology distribution networks.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| Given Imaging (Medtronic) | USA / Israel | Leader | PillCam SB3 / PillCam Colon | Global | Launched PillCam AI-assisted reading module with 94% sensitivity for small bowel lesion detection; expanded reimbursement in 12 European markets (2025) |

| Olympus Corporation | Japan | Leader | EndoCapsule 10 System | Asia Pacific / Europe | Released EndoCapsule 10 with AI polyp detection; partnered with cloud diagnostics platform for remote reading workflow (Mar 2025) |

| Jinshan Science & Technology | China | Leader | OMOM Capsule Endoscopy System | Asia Pacific | Secured NMPA approval for AI-assisted colon capsule; expanded into Southeast Asian hospital networks with government-sponsored colorectal screening program contracts (2025) |

| CapsoVision | USA | Challenger | CapsoCam Plus | North America / Europe | Received CE MDR recertification for CapsoCam Plus; launched 360-degree imaging AI review software update (Q1 2025) |

| Proteus Digital Health | USA | Challenger | Proteus Sensor / Ingestible Event Marker | North America | Secured pharmaceutical co-development agreements for adherence monitoring in transplant and psychiatric medicine; restructured as digital medicine platform (2025) |

| etectRx | USA | Niche Player | ID-Cap Ingestible Sensor System | North America | Completed Phase II clinical validation for transplant medication adherence monitoring; submitted FDA De Novo application (2025) |

| Vibrant Gastro | Israel / USA | Niche Player | Vibrant Capsule (motility therapy) | North America / Europe | Expanded US commercial launch of Vibrant mechanical capsule for chronic constipation to 300+ gastroenterology practices (Jan 2025) |

| Motus GI Holdings | USA | Niche Player | Pure-Vu System (capsule colon prep) | North America | Received expanded FDA clearance for Pure-Vu capsule-assisted colon cleansing; initiated multi-site clinical trial for inpatient use (2025) |

By Product Type

The ingestible sensor market by product type encompasses capsule endoscopy systems, smart pills for medication adherence, physiological monitoring capsules, and emerging ingestible biosensor platforms. Capsule endoscopy systems dominate the product landscape at approximately 52.3% of market revenue in 2025, valued at approximately USD 769 Million. These battery-powered, camera-equipped capsules are swallowed by the patient and capture thousands of images per second as they traverse the gastrointestinal tract, wirelessly transmitting data to an external recorder worn on a belt. Medtronic’s PillCam franchise has dominated this sub-segment since commercialization, though Olympus and Jinshan have meaningfully closed the technology gap in recent years. Capsule endoscopy systems generate high recurring revenue from disposable capsule sales, creating annuity revenue streams that anchor vendor business models. Fourth-generation capsule systems incorporate AI-assisted image review software, pH and temperature sensors, and extended battery life up to 12 hours covering the full GI tract from esophagus to colon.

Smart pills for medication adherence monitoring represent approximately 18.6% of market revenue in 2025 at USD 273 Million. These systems embed ingestible event markers, typically activated carbon or silicon-based microchips of sub-millimeter dimensions, within commercial pharmaceutical tablets or gelatin capsules. Upon dissolution in stomach acid, the sensor transmits a unique signal to a wearable patch that relays confirmed ingestion time and medication identification to a paired mobile application and cloud platform. Following the FDA approval of Abilify MyCite, pharmaceutical companies in psychiatric, transplant, and cardiovascular medicine have pursued ingestible adherence monitoring as a product differentiation strategy for branded medications facing biosimilar or generic competition. The revenue in this segment includes both sensor component licensing fees paid by pharmaceutical manufacturers and software subscription fees paid by healthcare providers and payers for adherence monitoring dashboards.

Physiological monitoring capsules, which measure core body temperature, luminal pH, intestinal motility, and pressure, account for approximately 15.4% of market revenue in 2025 at USD 226 Million. These devices are used primarily in clinical research, pharmaceutical development, and performance physiology applications including athlete core temperature monitoring and GI transit time assessment for clinical trials. The clinical research segment is growing as pharmaceutical companies adopt physiological monitoring capsules to collect pharmacodynamic data in GI drug development programs. Ingestible biosensor platforms, representing the most nascent category and covering real-time detection of biochemical markers within the GI lumen, account for approximately 13.7% of market revenue at USD 201 Million in 2025 and are projected to grow at the highest rate within the product taxonomy through the forecast period.

By Application

Gastrointestinal disease diagnosis and monitoring is the dominant application for ingestible sensors at approximately 61.4% of market revenue in 2025, valued at USD 902 Million. This application encompasses small bowel imaging for obscure gastrointestinal bleeding, Crohn’s disease mucosal assessment, celiac disease evaluation, and colorectal cancer screening. The American Gastroenterological Association practice guidelines include capsule endoscopy as the first-line investigation for obscure GI bleeding and suspected small bowel Crohn’s disease, embedding the technology in standard clinical pathways that generate predictable procedural volume. Colorectal cancer screening represents the fastest-growing indication within GI applications, as colon capsule endoscopy has received reimbursement approval in several European markets as a colonoscopy alternative for patients with failed or incomplete conventional colonoscopy. WHO data indicating 1.9 million new colorectal cancer cases annually creates a structurally large and growing screening demand that will sustain GI application revenue through 2034.

Medication adherence monitoring accounts for approximately 22.1% of market revenue in 2025 at USD 325 Million. This application is driven by pharmaceutical industry investment in digital medicine programs, payer interest in adherence-linked reimbursement models, and clinical evidence linking confirmed adherence monitoring to improved outcomes in transplant, psychiatry, and cardiovascular medicine. The application generates a distinctive commercial model where sensor revenue is closely tied to pharmaceutical licensing arrangements and recurring software subscription fees paid by healthcare systems and managed care organizations. Physiological and performance monitoring accounts for approximately 10.3% of market revenue at USD 151 Million in 2025, while drug delivery and clinical research applications represent approximately 6.2% at USD 91 Million.

By End-User

Hospitals and specialized gastroenterology centers represent the largest end-user segment at approximately 54.8% of market revenue in 2025, valued at USD 805 Million. Academic medical centers and tertiary hospitals are the primary adopters of capsule endoscopy and advanced ingestible monitoring platforms, driven by gastroenterology subspecialty programs, clinical research activity, and reimbursement support from Medicare, commercial payers, and national health systems. Outpatient gastroenterology practices and ambulatory endoscopy centers account for approximately 24.6% of revenue at USD 361 Million. These settings are growing adoption centers as capsule endoscopy technology has matured sufficiently for community gastroenterologist deployment without the specialist support infrastructure required by earlier-generation systems.

Pharmaceutical and clinical research organizations hold approximately 12.3% of market revenue at USD 181 Million in 2025. This segment uses ingestible sensors for pharmacokinetic studies, drug dissolution testing, GI motility characterization in clinical trials, and digital medicine companion diagnostic development. The remaining approximately 8.3% of market revenue, valued at USD 122 Million, comes from consumer wellness, military, and sports performance applications where physiological monitoring capsules and temperature sensors are used in non-clinical settings.

By Technology

Radiofrequency wireless communication technology is the dominant transmission standard in ingestible sensors at approximately 58.6% of market revenue in 2025, valued at USD 861 Million. RF transmission at designated medical telemetry frequencies enables reliable signal penetration through body tissue at sensor power levels consistent with swallowable battery capacity. The RF standard is embedded in all major capsule endoscopy platforms and most medication adherence systems. Bluetooth Low Energy and near-field communication technologies represent approximately 27.4% of market revenue at USD 402 Million, primarily in next-generation medication adherence sensors and physiological monitoring capsules where short-range communication to body-worn receivers is sufficient. Acoustic and ultrasound-based communication technologies, applied in specific research and military-grade body monitoring applications, represent approximately 14.0% of market revenue at USD 206 Million.

Regional Analysis

North America

North America holds the largest share of the global ingestible sensor market at approximately 43.5%, equivalent to USD 640 Million in 2025. The United States accounts for the dominant share of regional revenue, supported by FDA clearance infrastructure for ingestible devices under the 510(k) and De Novo pathways, Medicare coverage of capsule endoscopy for obscure gastrointestinal bleeding and Crohn’s disease indications under CPT codes 91110 and 91111, and a highly concentrated gastroenterology practice network that includes over 16,000 practicing gastroenterologists. Commercial payer coverage for capsule endoscopy is established across all major US insurance networks, providing reimbursement certainty that drives physician adoption. The FDA’s Digital Health Center of Excellence has provided guidance clarity for smart pill medication adherence systems under the Software as a Medical Device framework, opening regulatory pathways that have enabled commercial launches for pharmaceutical-integrated ingestible sensor systems. Canada contributes to regional growth through provincial health system adoption of capsule endoscopy in academic hospitals. The United States accounts for over 90% of North American ingestible sensor revenue in 2025.

Europe

Europe represents approximately 26.2% of global market revenue at USD 385 Million in 2025. Germany leads European adoption through its comprehensive hospital reimbursement for capsule endoscopy procedures under the G-DRG system and active research activity in GI biomarker sensing at university hospital centers. The United Kingdom has established NHS coverage for capsule endoscopy in obscure GI bleeding and Crohn’s disease monitoring, and NHS England has piloted colon capsule programs in bowel cancer screening settings where colonoscopy capacity is constrained. France has steady adoption through its hospital-based gastroenterology network, while Italy, Spain, and the Nordic countries have varying but growing reimbursement frameworks. The European Medical Device Regulation transition has created short-term friction as capsule endoscopy and ingestible sensor manufacturers recertify legacy products under new Class IIb and Class III categorizations, adding 12 to 24 months to product lifecycle timelines and creating an opportunity for MDR-early compliant vendors to capture market share from slower-adapting competitors.

Asia Pacific

Asia Pacific accounts for approximately 22.8% of global market revenue at USD 335 Million in 2025 and is the fastest-growing regional segment. China is the largest Asia Pacific market, driven by one of the world’s highest colorectal cancer incidence rates, government-sponsored early cancer detection programs that have incorporated capsule endoscopy into national screening initiatives, and a domestic manufacturing base anchored by Jinshan Science and Technology that produces competitively priced OMOM capsule systems approved by the NMPA. China’s national 2030 Healthy China initiative includes gastrointestinal cancer early detection as a priority, creating structured public health demand for ingestible imaging platforms. Japan has sophisticated capsule endoscopy adoption across university and community hospitals, with the PMDA approving multiple capsule systems for small bowel and colon indications. South Korea has high penetration in private hospital gastroenterology centers. India represents a growing market, constrained by device pricing relative to out-of-pocket patient costs but benefiting from expanding private hospital infrastructure and medical tourism-driven diagnostic service demand.

Latin America

Latin America represents approximately 4.8% of global market revenue at USD 71 Million in 2025. Brazil leads the region through its concentrated private hospital industry and the Agencia Nacional de Vigilancia Sanitaria registration framework that has cleared major capsule endoscopy systems for commercial use. Brazilian gastroenterology academic centers have driven adoption through clinical research programs, and private health insurance network coverage is expanding for capsule endoscopy procedures in Crohn’s disease and GI bleeding indications. Mexico and Colombia represent secondary markets with active private hospital adoption. The region’s growth through the forecast period will be supported by the expansion of private health insurance coverage and the increasing affordability of capsule technology as Chinese manufacturers introduce competitively priced systems into Latin American distribution networks. Public hospital adoption remains limited by budget constraints in national health systems across the region.

Middle East & Africa

The Middle East and Africa region accounts for approximately 2.7% of global market revenue at USD 40 Million in 2025. The United Arab Emirates and Saudi Arabia lead regional adoption through their advanced tertiary care hospital networks, with capsule endoscopy established in academic hospitals and JCI-accredited private hospitals in Dubai, Abu Dhabi, and Riyadh. The Gulf Cooperation Council’s high GI disease burden, linked in part to dietary patterns associated with type 2 diabetes and metabolic syndrome, creates sustained procedural demand. Israel is a significant contributor to the regional total through its established GI device industry, including the historical headquarters of Given Imaging, and active clinical research in ingestible sensing technologies. South Africa contributes through private hospital group adoption. The wider African continent faces profound access barriers tied to device costs and healthcare infrastructure, though targeted programs for early cancer detection in South Africa and Kenya are beginning to include non-invasive GI diagnostic tools in feasibility frameworks.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Capsule Endoscopy Systems

- Smart Pills for Medication Adherence Monitoring

- Physiological Monitoring Capsules

- Ingestible Biosensor Platforms

By Application

- Gastrointestinal Disease Diagnosis and Monitoring

- Medication Adherence Monitoring

- Physiological and Performance Monitoring

- Drug Delivery and Clinical Research

By End-User

- Hospitals and Gastroenterology Centers

- Outpatient and Ambulatory Endoscopy Practices

- Pharmaceutical and Clinical Research Organizations

- Consumer Wellness and Performance Applications

By Technology

- Radiofrequency (RF) Wireless Communication

- Bluetooth Low Energy (BLE) / Near-Field Communication (NFC)

- Acoustic / Ultrasound Communication

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.47 B |

| Forecast Revenue (2034) | USD 6.31 B |

| CAGR (2025-2034) | 17.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Capsule Endoscopy Systems, Smart Pills for Medication Adherence Monitoring, Physiological Monitoring Capsules, Ingestible Biosensor Platforms), By Application, (Gastrointestinal Disease Diagnosis and Monitoring, Medication Adherence Monitoring, Physiological and Performance Monitoring, Drug Delivery and Clinical Research), By End-User, (Hospitals and Gastroenterology Centers, Outpatient and Ambulatory Endoscopy Practices, Pharmaceutical and Clinical Research Organizations, Consumer Wellness and Performance Applications), By Technology, (Radiofrequency (RF) Wireless Communication, Bluetooth Low Energy (BLE) / Near-Field Communication (NFC), Acoustic / Ultrasound Communication) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GIVEN IMAGING (MEDTRONIC), OLYMPUS CORPORATION, JINSHAN SCIENCE & TECHNOLOGY, PROTEUS DIGITAL HEALTH, CAPSOVISION, ETECTRX, VIBRANT GASTRO, MOTUS GI HOLDINGS, INTROMEDIC, RF SYSTEM LAB, ANKON TECHNOLOGIES, CHECK-CAP, NOVABAY PHARMACEUTICALS (DIGITAL MEDICINE DIVISION), OTSUKA PHARMACEUTICAL (ABILIFY MYCITE PARTNERSHIP), CHUGAI BIOPHARMACEUTICALS (INGESTIBLE BIOSENSOR R&D), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (GI Disease Diagnosis, Medication Adherence, Drug Delivery, Clinical Research), By End-User, By Technology (RF, BLE, NFC, Ultrasound Communication), Industry Trends & Forecast 2026-2034")

, By Application (GI Disease Diagnosis, Medication Adherence, Drug Delivery, Clinical Research), By End-User, By Technology (RF, BLE, NFC, Ultrasound Communication), Industry Trends & Forecast 2026-2034")

, By Application (GI Disease Diagnosis, Medication Adherence, Drug Delivery, Clinical Research), By End-User, By Technology (RF, BLE, NFC, Ultrasound Communication), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Ingestible Sensor Market?

The Global Ingestible Sensor Market was valued at USD 1.25 Billion in 2024 and is projected to reach USD 6.31 Billion by 2034, growing at a CAGR of 17.6% from 2026 to 2034, driven by increasing adoption of digital health technologies, rising demand for real-time patient monitoring, advancements in smart biosensor technologies, and growing applications in medication adherence, chronic disease management, and remote healthcare monitoring solutions worldwide.

Who are the major players in the Ingestible Sensor Market?

GIVEN IMAGING (MEDTRONIC), OLYMPUS CORPORATION, JINSHAN SCIENCE & TECHNOLOGY, PROTEUS DIGITAL HEALTH, CAPSOVISION, ETECTRX, VIBRANT GASTRO, MOTUS GI HOLDINGS, INTROMEDIC, RF SYSTEM LAB, ANKON TECHNOLOGIES, CHECK-CAP, NOVABAY PHARMACEUTICALS (DIGITAL MEDICINE DIVISION), OTSUKA PHARMACEUTICAL (ABILIFY MYCITE PARTNERSHIP), CHUGAI BIOPHARMACEUTICALS (INGESTIBLE BIOSENSOR R&D), Others

Which segments covered the Ingestible Sensor Market?

By Product Type, (Capsule Endoscopy Systems, Smart Pills for Medication Adherence Monitoring, Physiological Monitoring Capsules, Ingestible Biosensor Platforms), By Application, (Gastrointestinal Disease Diagnosis and Monitoring, Medication Adherence Monitoring, Physiological and Performance Monitoring, Drug Delivery and Clinical Research), By End-User, (Hospitals and Gastroenterology Centers, Outpatient and Ambulatory Endoscopy Practices, Pharmaceutical and Clinical Research Organizations, Consumer Wellness and Performance Applications), By Technology, (Radiofrequency (RF) Wireless Communication, Bluetooth Low Energy (BLE) / Near-Field Communication (NFC), Acoustic / Ultrasound Communication)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date