- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Insurance Claims Automation Market Size, Share | CAGR 16.2%

Global Insurance Claims Automation Market Size, Share, Growth Analysis By Component (Software Platforms, Implementation & Managed Services), By Technology (AI & Machine Learning, RPA, OCR & Intelligent Document Processing, Blockchain & Smart Contracts), By Claim Type (Property & Casualty, Health, Life & Annuity, Auto Insurance), By End-User (Insurance Carriers, TPAs, Managed Care Organizations), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

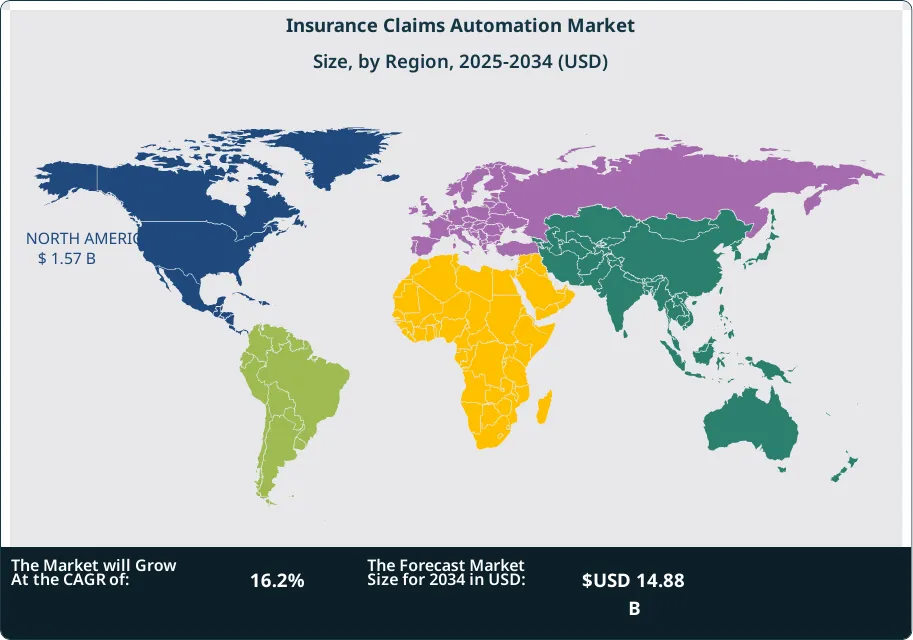

| USD 3.85 Billion | USD 14.88 Billion | 16.2% | North America, 40.8% |

The Insurance Claims Automation Market was valued at approximately USD 3.31 Billion in 2024 and reached USD 3.85 Billion in 2025. The market is projected to grow to USD 14.88 Billion by 2034, expanding at a CAGR of 16.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 11.03 Billion over the analysis period — an expansion anchored by combined ratio deterioration forcing loss adjustment expense reduction, artificial intelligence achieving functional maturity for unstructured insurance document processing, and regulatory frameworks in three major insurance markets introducing timelines that effectively mandate digital claims workflows.

Get More Information about this report -

Request Free Sample ReportThe primary causal trigger behind current market acceleration is the structural deterioration of claims combined ratios across the global property and casualty insurance industry. U.S. P&C insurers recorded an industry-wide combined ratio of 104.7% in 2024, the third consecutive year above 100%, driven by catastrophe loss severity from secondary perils — convective storms, wildfires, and inland flooding — that aggregate loss models consistently underestimated. Loss adjustment expenses represented 12.4% of incurred losses in 2024, up from 10.8% in 2019. This five-year deterioration translates to approximately USD 22 billion in excess annual claims handling costs across U.S. carriers alone, creating a direct financial mandate for automation investment. Chief financial officers at mid-size U.S. regional carriers reported in NAIC working group sessions that a 3–4 percentage point reduction in the loss adjustment expense ratio — achievable through automated triage and straight-through processing for sub-threshold claims — would restore statutory surplus adequacy without premium rate action, elevating automation procurement to a board-level capital priority.

A second specific trigger operates through natural catastrophe volume dynamics. The January 2025 Los Angeles County wildfire events generated an estimated 320,000 residential property claims filed within 72 hours of containment — a claim intake surge that overwhelmed manual adjuster capacity at every carrier active in the California admitted market. Carriers relying on manual photo-submission review required 28–45 days to complete initial contact for complex total-loss claims, creating California Department of Insurance market conduct exposure under regulations requiring acknowledgment within 15 days. Carriers with deployed AI damage assessment platforms completed automated damage scoping within 90 minutes of policyholder photo upload. The resulting competitive and regulatory differentiation accelerated vendor procurement decisions: carriers that had been evaluating automation platforms for 12–18 months compressed decision cycles to 60–90 days following the event.

Technology maturation constitutes the third enabling condition. Large language models trained on insurance-specific document corpora — policy declarations, medical records, repair invoices, and attorney demand letters — achieved benchmark accuracy rates of 91–96% for claims intake data extraction by early 2025, up from 74–81% in 2023. This accuracy threshold crosses the operational viability line for automated adjudication without mandatory human review on straightforward claim types. A relevant parallel: the banking industry's automated loan underwriting adoption accelerated sharply after model accuracy on standard mortgage applications crossed 90% in 2016, triggering vendor consolidation over the subsequent four years. Insurance claims automation sits approximately four years behind banking automation on this adoption curve, implying an acceleration phase concentrated between 2025 and 2029.

A contrarian observation qualifies the growth narrative. While automation adoption rates are accelerating at the platform level, actual straight-through processing rates remain substantially below vendor marketing claims. Independent audits conducted by three European insurance supervisory authorities in 2024 found that self-reported STP rates of 60–80% for automated claims platforms corrected to effective rates of 28–44% for complex multi-coverage claims when actual adjuster override frequency was examined. This gap between platform capability and operational implementation reflects integration complexity with legacy policy administration systems averaging 22 years of age at North American Tier-1 carriers, and the risk aversion of claims management teams whose performance metrics include regulatory penalty avoidance alongside cost efficiency.

, By Technology (AI & Machine Learning, RPA, OCR & Intelligent Document Processing, Blockchain & Smart Contracts), By Claim Type (Property & Casualty, Health, Life & Annuity, Auto Insurance), By End-User (Insurance Carriers, TPAs, Managed Care Organizations), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global insurance claims automation market reached USD 3.85 Billion in 2025 and is forecast to reach USD 14.88 Billion by 2034 at a CAGR of 16.2% over the 2026–2034 forecast period, driven by combined ratio deterioration at P&C carriers and AI document processing accuracy crossing the 90%+ operational viability threshold.

- Segment Dominance (By Component): Software and platform solutions captured 61.4% of component revenue at USD 2.36 Billion in 2025 because SaaS platform deployments generate multi-year recurring revenue at 4–6x the margin of implementation services, with carriers favoring API-first architectures that enable incremental automation without full legacy system replacement.

- Segment Dominance (By Claim Type): Property and casualty claims held 42.6% of claim-type revenue at USD 1.64 Billion in 2025, anchored by catastrophe claims volume from secondary perils and high-frequency homeowners and commercial property claims where automation ROI is most immediately quantifiable, with the January 2025 wildfire claims surge demonstrating a USD 1,248 per-claim cost differential between automated and manual handling.

- Driver: U.S. P&C industry combined ratios averaging 104.7% in 2024 — the third consecutive year above 100% — and loss adjustment expenses rising to 12.4% of incurred losses elevated claims automation to a board-level capital priority, with the Los Angeles wildfire claims surge compressing vendor procurement timelines from 18 months to 60–90 days at directly affected carriers.

- Restraint: Legacy policy administration systems averaging 22 years of age at North American Tier-1 carriers create API integration barriers that inflate implementation timelines by 7.4 months on average versus vendor estimates and suppress effective straight-through processing rates to 28–44% for complex claims — a gap that slows realized ROI and moderates repeat purchase velocity below vendor forecast assumptions.

- Opportunity: The workers' compensation and employer liability claims segment remains fewer than 14% penetrated by AI-assisted processing platforms as of 2025, with jurisdiction-specific medical fee schedule complexity across 46 U.S. state systems creating a specialist vendor opportunity worth USD 800 million–1.3 Billion by 2029 as NCCI electronic data interchange standards and purpose-built WC platforms reduce integration barriers.

- Trend: Generative AI for claims narrative drafting and coverage determination explanation reached 38% penetration among North American claims operations in 2025 versus 12% in Asia Pacific, with early deployments at U.S. regional carriers reporting 34% reductions in claim file documentation time and 19% improvements in post-settlement claimant satisfaction scores.

- Regional Analysis: North America held 40.8% of global insurance claims automation revenue at USD 1.57 Billion in 2025, driven by NAIC market conduct examination standards, catastrophe claims surge differentiation between automated and manual carriers, and the Hartford, Connecticut concentration of Tier-1 mutual P&C insurer technology investment budgets.

Competitive Landscape Overview

The insurance claims automation market exhibits moderate consolidation, with the top four vendors — Guidewire Software, Duck Creek Technologies, Shift Technology, and CCC Intelligent Solutions — collectively accounting for an estimated 46.8% of total market revenue in 2025. Competition bifurcates along two structural axes: full-suite claims management platform vendors (Guidewire, Duck Creek, Sapiens) whose automation capabilities are embedded within comprehensive policy-to-payment insurance operating systems, and best-of-breed AI point-solution vendors (Shift Technology, Tractable, Snapsheet) that integrate via API into existing claims platforms. Full-suite vendors command average contract values of USD 8–25 million for Tier-1 implementations; point-solution vendors achieve faster sales cycles with lower initial commitment thresholds. In 2025, competitive intensity shifted materially as Guidewire and Duck Creek accelerated native AI feature development, compressing the whitespace that standalone AI vendors had previously occupied in adjacency to core platforms. Three India-headquartered technology services firms — Cognizant, Wipro, and Tech Mahindra — entered the mid-market with managed claims automation services priced 25–35% below Western software-plus-implementation bundles, triggering pricing pressure responses from platform incumbents in the USD 2–8 million contract tier.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move (2024–2026) |

| Guidewire Software | USA | Leader | Guidewire ClaimCenter with Kufri GenAI | North America / Europe | Released Kufri platform update in Jan 2025 with embedded generative AI reserve adequacy recommendations; deployed by 17 Tier-1 P&C carriers within six months of release. |

| Duck Creek Technologies | USA | Leader | Duck Creek Claims SaaS Platform | North America | Completed SaaS-only platform transition in Q2 2025; secured a USD 320 million multi-year renewal with a top-10 U.S. P&C insurer in Feb 2026. |

| Shift Technology | France / USA | Leader | Force Claims Fraud Detection & Automation | North America / Europe | Extended Force to auto-adjudicate low-complexity health claims in Mar 2025, reducing average processing time from 18 days to 4.2 days at three European health insurer clients. |

| CCC Intelligent Solutions | USA | Leader | CCC ONE Estimate-STP Auto Claims | North America | Launched CCC Estimate-STP in Oct 2025, achieving 91% auto-adjudication rates for minor collision claims across 35 million annual claim transactions. |

| Pegasystems | USA | Challenger | Pega Claims Management on Pega Infinity | North America / Europe | Released Pega GenAI Blueprint for claims workflow automation in Feb 2025, enabling natural-language adjudication rule configuration without coding expertise. |

| Tractable | UK / USA | Challenger | Tractable AI Auto & Property Damage Assessment | Europe / North America | Extended AI damage assessment to six additional European motor insurer repair networks in Dec 2024, covering 11.4 million vehicles under management in Germany, France, and Benelux. |

| EXL Service | USA | Challenger | EXL XTRAKTO.AI Claims Intelligence Platform | North America / Asia Pacific | Acquired Claimatic claims routing optimization firm in Sep 2025, adding AI-driven adjuster workload management for 28 insurance carrier clients. |

| Sapiens International | Israel | Challenger | Sapiens ClaimsPro | Europe / North America | Launched Sapiens DECISION for automated claim eligibility determination in Q1 2026, covering 40+ coverage types across life, P&C, and workers' compensation. |

| Verisk Analytics | USA | Niche Player | Xactimate Next Property Damage Scoping | North America | Deployed AI-assisted Xactimate Next in Nov 2025 with aerial imagery and LiDAR integration, generating automated repair estimates within 90 minutes of loss notification. |

| Snapsheet | USA | Niche Player | Snapsheet Virtual Claims Management | North America | Raised USD 45 million Series D in Jul 2025 to expand virtual claims handling into the MGA and insurtech carrier segment, targeting 150 new mid-market clients by end of 2026. |

By Component

Software and platform solutions captured 61.4% of insurance claims automation market revenue at USD 2.36 Billion in 2025 — a dominance grounded in the commercial model shift from project-based implementation to subscription-based SaaS licensing completed by the three largest platform vendors between 2022 and 2025. Guidewire achieved 94% SaaS revenue mix by Q4 2024 and Duck Creek completed its SaaS-only transition in Q2 2025, converting previously lumpy implementation revenue into predictable annual recurring contract structures carrying 70–80% gross margins versus 35–45% for professional services. Data network effects amplify the platform segment's advantage: Guidewire's ClaimCenter processes claims across 500+ carrier deployments globally, enabling AI models embedded in reserve adequacy and fraud detection features to improve continuously as the training dataset expands — a compounding moat that smaller point-solution vendors cannot match without equivalent deployment scale. The fastest-growing software sub-segment is API-accessible automated decisioning engines that carriers embed within existing claims workflows rather than replacing them, growing at an estimated 22.4% annually as carriers with 15–25-year-old core systems pursue automation gains without triggering full legacy transformation projects.

Services retained 38.6% of component revenue at USD 1.49 Billion in 2025, sustained by the integration complexity of connecting modern automation platforms to legacy COBOL-based policy administration systems, medical bill review databases, and state-specific regulatory reporting interfaces. Post-implementation reviews at 12 North American carrier deployments found that average implementation timelines exceeded initial vendor estimates by 7.4 months, with legacy system integration accounting for 58% of overrun hours. This complexity sustains demand for specialized implementation partners — Cognizant Insurance, EXL Service, and Majesco Professional Services — that have built repeatable integration accelerators for the 8–12 core legacy platforms accounting for 76% of North American carrier infrastructure. Managed services, representing approximately 31% of total services revenue, grow fastest as carriers with constrained technology staff seek vendor-operated platform management rather than internal deployment.

By Technology

AI and machine learning held 38.7% of technology-segmented revenue at USD 1.49 Billion in 2025. AI dominance over alternative automation technologies reflects a commercial argument specific to claims complexity: insurance claims involve unstructured data inputs — handwritten medical notes, contractor repair estimates in non-standard formats, legal demand letters, and recorded claimant statements — that rule-based robotic process automation cannot interpret without prior human extraction. AI models trained on insurance-specific document types extract structured data from these inputs at 91–96% accuracy, enabling automated coverage determination and reserve calculation on claim types that RPA tools handle only through rigid template matching. The fastest-growing AI sub-application is computer vision for property and auto damage assessment, where deep learning models trained on Tractable's 70 million+ claim training corpus and CCC's 35 million annual auto claim dataset achieve damage severity estimates within 8–12% of manual appraiser assessments on standard damage types — a variance level meeting U.S. state insurance commissioner appraisal fairness tolerances in market conduct examinations.

Robotic process automation contributed 24.3% of technology revenue at USD 0.935 Billion in 2025, concentrated in high-volume repetitive tasks: intake data entry from standard ACORD forms, first-notice-of-loss acknowledgment generation, payment disbursement for settled claims, and regulatory reporting population. RPA's strength is deployment speed — carriers can typically automate a defined workflow task within 4–8 weeks without core system changes — and its weakness is brittleness when source document formats change. OCR and intelligent document processing at 19.8% grows at 21.3% annually, driven by health and medical claims where CMS-1500 and UB-04 forms and prior authorization documents represent high-volume structured extraction targets. Blockchain and smart contract automation at 17.2% remains the segment with the largest gap between projected and realized adoption, concentrated in parametric insurance where weather oracle triggers enable fully automated payouts for flight delay, crop yield, and catastrophe bond instruments without adjuster involvement.

By Claim Type

Property and casualty claims generated 42.6% of claim-type revenue at USD 1.64 Billion in 2025 because the combination of high claim frequency, severe loss cost volatility, and standardized digital damage data inputs creates the most favorable automation ROI equation among all claim types. Commercial property claims average 34 distinct workflow steps from first notice of loss to payment under manual handling; automated platforms reduce this to 11–14 steps for claims below carrier-defined complexity thresholds, translating to loss adjustment expense savings of USD 380–720 per claim. Carriers with deployed automation systems reported average catastrophe claim processing costs of USD 892 versus USD 2,140 for manual-only handling in internal efficiency benchmarking shared with NAIC working groups during 2024 deliberations on electronic claims settlement standards.

Health and medical claims held 31.8% at USD 1.22 Billion in 2025, growing at 18.4% annually — the fastest among claim type segments — driven by the No Surprises Act's independent dispute resolution process generating 490,000+ arbitration submissions in 2024 requiring detailed automated claim data extraction, and by the CMS prior authorization electronic transaction mandate effective January 2026 requiring Medicare Advantage and Medicaid managed care plans to support automated PA decision APIs. Life and annuity at 14.4% and auto and motor at 11.2% complete the distribution, with auto claims distinguished by CCC Intelligent Solutions' near-duopolistic position in U.S. auto damage estimation — an estimated 58% market share in auto appraisal workflow — that limits competitive entry from alternative AI damage assessment vendors.

By End-User

Insurance carriers as direct buyers represented 54.3% of end-user demand at USD 2.09 Billion in 2025, their dominant position reflecting direct P&L accountability for loss adjustment expense ratios — the primary financial metric automation investment must improve. Third-party administrators contributed 24.7% at USD 0.951 Billion, the fastest-growing end-user category at 20.1% annually, driven by the outsourcing trend among small and mid-size carriers that lack technology investment capacity for enterprise automation platforms. Sedgwick, Broadspire, and Gallagher Bassett collectively invested over USD 480 million in claims automation platform development between 2022 and 2025, creating a managed-services delivery model where automation capability is bundled into claims administration contracts rather than sold as a standalone technology purchase. Managed care organizations at 12.6% and other industries at 8.4% complete the end-user distribution.

Regional Analysis

North America

Propelled by NAIC market conduct examination standards mandating 15-day claims acknowledgment timelines, three consecutive years of combined ratio deterioration forcing board-level LAE reduction mandates, and the January 2025 Los Angeles wildfire claims surge that demonstrated in real time the competitive differentiation between automated and manual carriers, North America's insurance claims automation market captured 40.8% of global revenue at USD 1.57 Billion in 2025. The United States accounts for approximately 87% of North American market revenue, concentrated in personal lines property carriers, commercial lines specialty insurers with complex multi-jurisdictional claims, and the workers' compensation insurance segment unique to the U.S. regulatory architecture. Hartford, Connecticut — home to Travelers, Hartford Financial Services, and Aetna's P&C operations — represents the highest absolute claims automation spend concentration per geography globally, as mutual insurer governance structures enable multi-year technology investment cycles insulated from short-term earnings pressure. Canada contributed the regional balance, led by Intact Financial Corporation's USD 14 million claims automation expansion into its RSA Canada subsidiary completed in 2025 following RSA's post-acquisition integration.

Europe

Implementation requirements under the European Insurance and Occupational Pensions Authority's supervisory convergence program for digital claims handling, combined with the EU AI Act's February 2025 categorization of automated claims adjudication as a high-risk AI application requiring conformity assessment documentation, reshaped procurement structures across the European insurance claims automation market, which held 26.3% share worth USD 1.01 Billion in 2025. Germany led European demand through its concentration of large P&C mutual insurers — HUK-Coburg in Coburg and Allianz's Unterföhring Munich campus — following the German Insurance Association's voluntary commitment to sub-48-hour settlement for standard motor claims under EUR 5,000. The United Kingdom contributed the second-largest European sub-market, driven by the Financial Conduct Authority's Consumer Duty implementation review requiring insurers to demonstrate fair and timely claims handling as a measurable customer outcome. France's position as the fourth-largest European demand center reflects AXA's Paris-headquartered group-level automation deployment across 12 country subsidiaries and the Groupama agricultural cooperative's claims automation investment for crop and livestock peril claims.

Asia Pacific

Insurance premium growth exceeding 11% annually in India's non-life sector, combined with Australia's Insurance Council mandating electronic claims lodgment standards for member carriers effective January 2026, drove Asia Pacific's insurance claims automation market to 20.4% global share at USD 0.785 Billion in 2025. China represented the largest APAC sub-market through Ping An Insurance's deployment of AI claims assessment at scale — its Good Doctor platform processed 47 million health claims through automated channels in 2024, a reference deployment whose operational data domestic insurers widely cite in automation ROI justifications. Japan's Financial Services Agency digital transformation guidance for non-life insurers, published in Q2 2025, created a structured roadmap that Tokio Marine, Sompo Japan, and MS&AD Insurance Group are executing through Guidewire ClaimCenter adaptations for Japanese regulatory claim form requirements. India's Insurance Regulatory and Development Authority's BIMA SUGAM digital insurance ecosystem initiative, targeting 1 billion policy registrations by 2027, establishes a digital policy infrastructure layer directly enabling automated claims processing at the scale required by India's 1.4 billion addressable population — including rural agricultural claim volumes where manual adjuster deployment is physically and economically infeasible across Rajasthan and Madhya Pradesh's dispersed farming districts.

Latin America

Structural underinsurance across Latin America — non-life insurance penetration averaging 1.6% of GDP versus 4.1% in North America — constrains absolute market size but creates a growth-by-formalization dynamic as digital distribution expands the insured population into demographics requiring cost-efficient automated claims handling. Latin America's insurance claims automation market reached USD 0.293 Billion (7.6% global share) in 2025, with Brazil accounting for approximately 58% of regional revenue driven by SUSEP's Resolution 407 requirements for electronic first-notice-of-loss handling and automation investments at Bradesco Seguros and Porto Seguro targeting Brazil's growing middle-class auto insurance portfolio. São Paulo-based insurtech carriers including Youse and Pier have deployed AI-first claims models generating loss adjustment expense ratios below 7% — approximately 40% below industry average — attracting reinsurer attention and foreign insurer investment into Brazil's digital insurance segment. Colombia's Superintendencia Financiera published minimum digital claims standards for registered insurers in late 2024, creating a defined compliance timeline that vendor representatives are actively leveraging in procurement conversations across Bogotá-headquartered insurance groups.

Middle East & Africa

Insurance Authority UAE's 2025 digital transformation circular requiring all licensed UAE insurers to implement electronic claims notification and acknowledgment systems by January 2026 created a mandated procurement event affecting 62 licensed carriers in a market where motor and health claims represent 78% of total claim volume, pushing the MEA insurance claims automation market to USD 0.189 Billion (4.9% share) in 2025. Abu Dhabi National Insurance Company and Dubai Insurance Company completed automation platform deployments in Q3 2025 ahead of the regulatory deadline, selecting European point-solution vendors rather than U.S.-headquartered platform incumbents due to data residency requirements under UAE Federal Data Protection Law No. 45 of 2021 that prohibit health claims data processing on non-approved cross-border cloud infrastructure. Saudi Arabia's Vision 2030 insurance sector development target — raising penetration from 1.4% to 4.5% of GDP by 2030 — implies a tripling of insured exposure requiring proportional claims processing capacity increases that manual staffing models cannot support economically. South Africa's Prudential Authority published digital claims standards guidance in Q4 2025 covering the six largest Johannesburg-headquartered short-term insurance groups managing a combined ZAR 86 billion gross written premium market.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software / Platform

- Services (Implementation, Consulting, Managed Services)

By Technology

- AI & Machine Learning

- Robotic Process Automation (RPA)

- OCR & Intelligent Document Processing

- Blockchain & Smart Contracts

By Claim Type

- Property & Casualty (P&C)

- Health & Medical

- Life & Annuity

- Auto / Motor

By End-User

- Insurance Carriers (Direct)

- Third-Party Administrators (TPAs)

- Managed Care Organizations

- Other Industries

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.85 B |

| Forecast Revenue (2034) | USD 14.88 B |

| CAGR (2025-2034) | 16.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software / Platform, Services (Implementation, Consulting, Managed Services)), By Technology, (AI & Machine Learning, Robotic Process Automation (RPA), OCR & Intelligent Document Processing, Blockchain & Smart Contracts), By Claim Type, (Property & Casualty (P&C), Health & Medical, Life & Annuity, Auto / Motor), By End-User, (Insurance Carriers (Direct), Third-Party Administrators (TPAs), Managed Care Organizations, Other Industries) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GUIDEWIRE SOFTWARE, DUCK CREEK TECHNOLOGIES, SHIFT TECHNOLOGY, CCC INTELLIGENT SOLUTIONS, PEGASYSTEMS, TRACTABLE, EXL SERVICE, SAPIENS INTERNATIONAL, VERISK ANALYTICS (XACTIMATE / ISO CLAIMSEARCH), SNAPSHEET, MAJESCO, MITCHELL INTERNATIONAL, COGNIZANT, USHUR, ONE INC., SEDGWICK, GALLAGHER BASSETT, BROADSPIRE, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (AI & Machine Learning, RPA, OCR & Intelligent Document Processing, Blockchain & Smart Contracts), By Claim Type (Property & Casualty, Health, Life & Annuity, Auto Insurance), By End-User (Insurance Carriers, TPAs, Managed Care Organizations), Industry Trends & Forecast 2026-2034")

, By Technology (AI & Machine Learning, RPA, OCR & Intelligent Document Processing, Blockchain & Smart Contracts), By Claim Type (Property & Casualty, Health, Life & Annuity, Auto Insurance), By End-User (Insurance Carriers, TPAs, Managed Care Organizations), Industry Trends & Forecast 2026-2034")

, By Technology (AI & Machine Learning, RPA, OCR & Intelligent Document Processing, Blockchain & Smart Contracts), By Claim Type (Property & Casualty, Health, Life & Annuity, Auto Insurance), By End-User (Insurance Carriers, TPAs, Managed Care Organizations), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Insurance Claims Automation Market?

The Global Insurance Claims Automation Market was valued at USD 3.31 Billion in 2024 and is projected to reach USD 14.88 Billion by 2034, growing at a CAGR of 16.2% from 2026 to 2034, driven by rising adoption of AI-powered claims processing, fraud detection systems, robotic process automation (RPA), computer vision-based damage assessment, and cloud-native insurance technologies across health, life, automotive, property, and commercial insurance sectors worldwide.

Who are the major players in the Insurance Claims Automation Market?

GUIDEWIRE SOFTWARE, DUCK CREEK TECHNOLOGIES, SHIFT TECHNOLOGY, CCC INTELLIGENT SOLUTIONS, PEGASYSTEMS, TRACTABLE, EXL SERVICE, SAPIENS INTERNATIONAL, VERISK ANALYTICS (XACTIMATE / ISO CLAIMSEARCH), SNAPSHEET, MAJESCO, MITCHELL INTERNATIONAL, COGNIZANT, USHUR, ONE INC., SEDGWICK, GALLAGHER BASSETT, BROADSPIRE, Others

Which segments covered the Insurance Claims Automation Market?

By Component, (Software / Platform, Services (Implementation, Consulting, Managed Services)), By Technology, (AI & Machine Learning, Robotic Process Automation (RPA), OCR & Intelligent Document Processing, Blockchain & Smart Contracts), By Claim Type, (Property & Casualty (P&C), Health & Medical, Life & Annuity, Auto / Motor), By End-User, (Insurance Carriers (Direct), Third-Party Administrators (TPAs), Managed Care Organizations, Other Industries)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Insurance Claims Automation Market

Published Date : 27 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date