- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Intelligent Well Completion Market Size, Share & Growth | CAGR 5.5%

Global Intelligent Well Completion Market Size, Share, Analysis By Component (Downhole Flow-Control Equipment, Sensors & Monitoring Systems, Surface Control and Communication Systems, Packers Isolation & Ancillary Completion Tools), By Technology (Hydraulic Intelligent Completions, Electric & Electro-hydraulic Intelligent Completions, Wireless & Autonomous Inflow-Control Systems), By Application (Production-Rate Control, Water & Gas Control, Reservoir Surveillance & Zonal Monitoring, Injection Control), By Well Architecture (Horizontal Wells, Multilateral Wells, Vertical & Deviated Wells) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 1.6 Billion, 2025 | USD 2.6 Billion, 2034 | 5.5%, 2026–2034 | Middle East and Africa, 27.00%, 2025 |

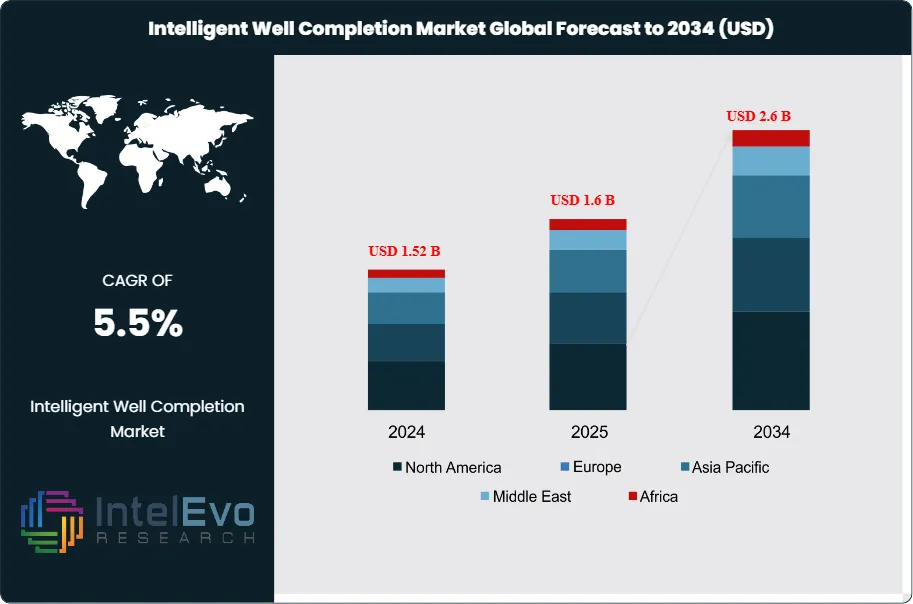

The Intelligent Well Completion Market was valued at approximately USD 1.52 Billion in 2024 and increased to USD 1.6 Billion in 2025. The market is projected to reach nearly USD 2.6 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 5.5% during the forecast period from 2026 to 2034. This estimate reflects current industry positioning in the mid-USD 1.5 billion range and a steady mid-single-digit growth profile across premium completion systems.

Get More Information about this report -

Request Free Sample ReportThe Intelligent Well Completion Market is gaining from a clear shift in upstream spending toward complex wells, deeper reservoirs, and higher recovery from existing fields. Demand is strongest where operators need real-time zonal control, lower intervention frequency, and tighter management of water and gas breakthrough. Offshore Brazil, the North Sea, the Middle East, and selected Asia Pacific gas fields now set the pace for adoption.

Supply conditions remain favorable but not frictionless. The market relies on a concentrated base of global completion-system providers, control-line specialists, flow-control manufacturers, and downhole monitoring vendors. The top tier continues to be led by SLB, Halliburton, Baker Hughes, and Weatherford, while specialists such as TAQA, Expro, Packers Plus, and Tendeka hold targeted positions in inflow control, running tools, and niche completion architectures. Upstream oil and gas project cost inflation continues to slow adoption in marginal onshore projects but has less effect on high-rate offshore and deepwater wells, where production gains can justify higher completion-system spend.

Technology is now the main differentiator in the Intelligent Well Completion Market. Electric and electro-hydraulic systems are gaining share because they reduce hydraulic-line complexity, shorten installation steps, and improve data capture. New product launches across 2025 confirmed that AI, automation, and digitalization are moving into the completion string, the surface control layer, and the production-management workflow.

Regionally, the strongest investment hotspots sit in the Middle East, Brazil, and selected North Sea developments. The main risks remain oil-price volatility, sanctions exposure, longer procurement cycles, and the still-high upfront cost of intelligent systems relative to standard completions. Even so, the market remains on a steady growth path because operators keep prioritizing lower field intervention rates, tighter reservoir control, and higher recovery from fewer wells.

, By Technology (Hydraulic Intelligent Completions, Electric & Electro-hydraulic Intelligent Completions, Wireless & Autonomous Inflow-Control Systems), By Application (Production-Rate Control, Water & Gas Control, Reservoir Surveillance & Zonal Monitoring, Injection Control), By Well Architecture (Horizontal Wells, Multilateral Wells, Vertical & Deviated Wells) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Intelligent Well Completion Market stood at USD 1.6 Billion in 2025 and is projected to reach USD 2.6 Billion by 2034 at a 5.5% CAGR over 2026–2034.

- Segment Dominance: By component, downhole flow-control equipment led the market with a 36.0% share in 2025, equal to about USD 0.58 Billion.

- Segment Dominance: By application, production-rate control led with a 38.0% share in 2025, equal to about USD 0.61 Billion.

- Driver: The main growth driver is the rise in offshore and deepwater field development, especially in Brazil and the Middle East where premium wells require multizone control and lower intervention rates.

- Restraint: The main restraint is system cost and project inflation, which slows conversion from conventional completions in lower-margin onshore projects.

- Opportunity: The largest opportunity sits in electric intelligent completions, which accounted for an estimated 34.0% of the market in 2025, or about USD 0.54 Billion.

- Trend: The defining trend is integration of sensing, automation, and remote control in one completion architecture, with fiber-optic and electric systems gaining wider commercial traction.

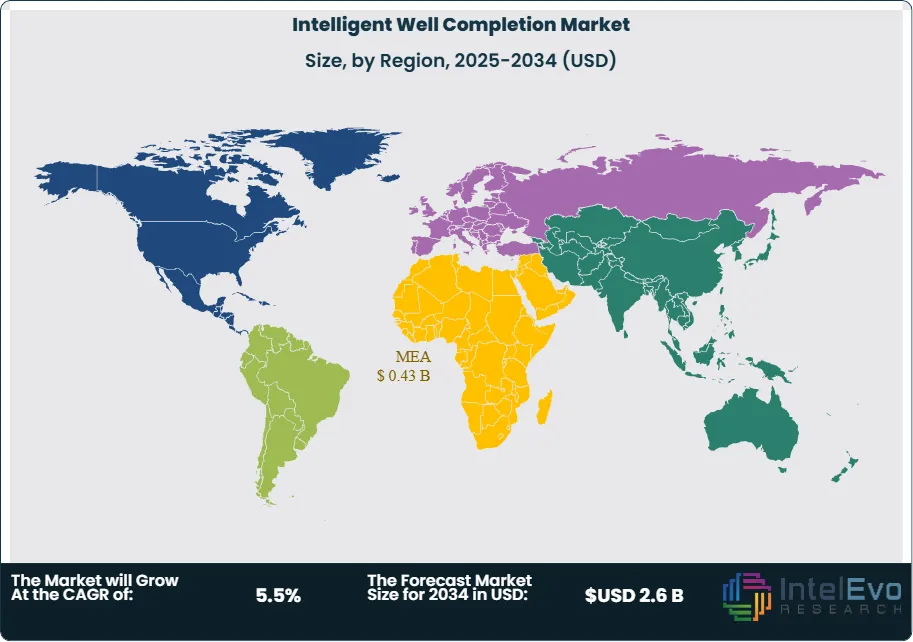

- Regional Analysis: Middle East & Africa led the market with an estimated 27.0% share in 2025, equal to about USD 0.43 Billion.

Competitive Landscape Overview

The Intelligent Well Completion Market is moderately consolidated. The top four players, SLB, Halliburton, Baker Hughes, and Weatherford, controlled an estimated 58.0% of global revenue in 2025. Competition is primarily technology-driven, with electric completions, multizone control, fiber sensing, and digital production management shaping bid success more than simple price. Competitive intensity increased in 2025 as larger offshore operators awarded integrated completion packages and vendors accelerated electric-system launches.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB | US | Leader | Electris electric well completions | Middle East, Latin America | Launched Electris electric completions portfolio in 2025; later won Brazil ultra-deepwater completions work for up to 35 wells. |

| HALLIBURTON | US | Leader | SmartWell intelligent completions | North America, Latin America, Middle East | Launched SmartWell Turing electro-hydraulic control system in 2025 and secured Petrobras deepwater completion contracts. |

| BAKER HUGHES | US | Leader | SureCONTROL intelligent completion systems | Latin America, Middle East | Won a major multi-year fully integrated completions systems contract with Petrobras in 2025. |

| WEATHERFORD | US | Challenger | AMP All-Electric Completions | Middle East, Europe | Advanced AMP all-electric completions with fiber optics in 2025 and won a multi-year Denmark completions contract in 2026. |

| NOV | US | Challenger | Completion Tools portfolio | North America, Middle East | Maintained broad completion-tool presence and focused on tools that reduce non-productive time and improve decisions. |

| EXPRO | UK | Challenger | Hands Free Completion Running System | Europe, MENA, Brazil | Reported new contract wins using advanced completions technologies and launched RCIS in 2025. |

| TAQA | Saudi Arabia | Niche Player | M4 Autonomous Inflow Control System | Middle East | Expanded advanced inflow-control offerings for improved water-control performance. |

| PACKERS PLUS | Canada | Niche Player | ePLUS multi-stage completion systems | North America, Middle East | Field-trialed ePLUS Dart technology across multiple basins in late 2025 and early 2026. |

Segmentation Analysis

By Component

Downhole Flow-Control Equipment held 36.0% of the market in 2025, equal to USD 0.58 Billion. This segment leads because interval control valves, inflow-control devices, sliding sleeves, and multizone flow hardware are the core functional layer of every intelligent completion. Operators buy these systems first when they want direct command over inflow, injection, water-cut management, or zonal shutoff. The 2025 product cycle favored electric and electro-hydraulic valve systems, especially in offshore wells where intervention costs are high and payback periods are faster. The segment should keep the highest pricing power through 2034 because it carries the most direct production impact and the hardest qualification standards.

Sensors and Monitoring Systems held 25.0% of the market in 2025, equal to USD 0.40 Billion. Permanent downhole gauges, fiber-optic monitoring, temperature and pressure sensors, and distributed acoustic or thermal systems now form a standard part of premium intelligent completion packages. Their share is rising because operators no longer view monitoring as optional. Real-time visibility drives zone-level action and reduces uncertainty around water influx, gas coning, and injection response. This category grows faster than the total market through 2034, especially in offshore assets where access is limited and data quality matters.

Surface Control and Communication Systems held 21.0% of the market in 2025, equal to USD 0.34 Billion. This segment covers topside controllers, control lines, power units, telemetry interfaces, and supervisory software that turn downhole hardware into a remotely managed completion system. It is becoming more strategic as operators ask for tighter integration with field automation, SCADA, and production-management platforms. The move toward electric systems improves the outlook because digital control architectures support cleaner data transfer and simpler integration.

Packers, Isolation, and Ancillary Completion Tools held 18.0% of the market in 2025, equal to USD 0.29 Billion. These products include packers, seal assemblies, tubing accessories, control-line protection, and installation-related hardware that enable the intelligent completion system to function under demanding conditions. This category carries lower revenue share because it overlaps with broader completion-tool spend and faces more price competition. Still, it remains essential because poor isolation or unreliable accessory hardware can undermine the data and control value of the entire system.

By Technology

Hydraulic Intelligent Completions held 46.0% of the market in 2025, equal to USD 0.74 Billion. Hydraulic systems still lead because they have the longest field record, broad qualification history, and large installed base in offshore and conventional smart-well developments. Operators continue to favor them in assets where reliability proof matters more than installation simplicity. However, this segment is losing share to electric and electro-hydraulic designs and should grow below the market average through 2034.

Electric and Electro-hydraulic Intelligent Completions held 34.0% of the market in 2025, equal to USD 0.54 Billion. This is the fastest-growing major technology block in the market. Electric architectures reduce hardware count, simplify installation, improve data transmission, and support more responsive zonal control. Adoption is strongest in offshore, subsea, and deepwater wells where every avoided intervention carries high economic value. By 2034, this segment is likely to narrow the gap with hydraulic systems sharply.

Wireless and Autonomous Inflow-Control Systems held 20.0% of the market in 2025, equal to USD 0.32 Billion. This segment includes autonomous inflow-control devices and specialized wireless completion architectures used to manage water or gas breakthrough without continuous surface actuation. It remains smaller because deployment is more selective and project economics depend heavily on reservoir conditions. Yet the strategic value is high in mature fields, heavy-oil environments, and retrofit programs where operators need fluid discrimination rather than full multi-actuated zonal control.

By Application

Production-Rate Control held 38.0% of the market in 2025, equal to USD 0.61 Billion. Operators continue to buy intelligent completions first for direct control over production contribution by zone. When operators can choke, open, or rebalance reservoir sections remotely, they can preserve plateau output, protect drawdown strategy, and react faster to changing reservoir behavior. Because this use case ties most directly to daily cash flow, it captures the biggest share of spend and will remain the anchor application through 2034.

Water and Gas Control held 27.0% of the market in 2025, equal to USD 0.43 Billion. This segment gains from the need to delay water breakthrough, reduce unwanted gas, and limit intervention-heavy remedial work. It is especially relevant in mature offshore fields, heavy-oil reservoirs, and long horizontal wells where coning and early breakthrough can erode project economics. Through 2034, water and gas control should outpace the overall market because it combines production protection with lower field operating cost.

Reservoir Surveillance and Zonal Monitoring held 21.0% of the market in 2025, equal to USD 0.34 Billion. This application includes permanent monitoring packages that capture temperature, pressure, acoustic, and flow behavior across multiple zones. It is becoming more important as operators adopt closed-loop production management rather than periodic well testing alone. The segment benefits from fiber optics, permanent gauges, and digital interpretation systems and is one of the clearest structural growth areas through 2034.

Injection Control held 14.0% of the market in 2025, equal to USD 0.22 Billion. This application includes intelligent management of water injection, gas injection, and other pressure-support functions across reservoir zones. It remains smaller than production-side use cases because many operators still focus intelligent-completion budgets on producing wells first. However, it has clear upside in brownfield redevelopment and large waterflood programs.

By Well Architecture

Horizontal Wells held 44.0% of the market in 2025, equal to USD 0.70 Billion. Horizontal wells dominate because they create the strongest need for distributed inflow management, zonal balancing, and remote control across long reservoir contact. The longer the exposure, the greater the risk of uneven contribution, early water or gas breakthrough, and localized depletion. Intelligent completions directly address those issues, which keeps this segment in the lead.

Multilateral Wells held 31.0% of the market in 2025, equal to USD 0.50 Billion. This segment is strategically important because multilateral designs create some of the most complex completion-control problems in the industry. Operators use intelligent systems in these wells to manage branch-level contribution, isolate problem zones, and reduce intervention frequency. The economic case is strong, but qualification and installation complexity keep share below horizontal wells.

Vertical and Deviated Wells held 25.0% of the market in 2025, equal to USD 0.40 Billion. These wells still account for a meaningful slice of demand, particularly in legacy conventional fields and selected injection programs. The case for intelligent completions is usually weaker here than in long horizontal or multilateral wells, but vertical and deviated wells remain relevant in mature offshore platforms and redevelopment projects where remote monitoring or water-control functions can still improve field performance materially.

Regional Analysis

Middle East & Africa

Middle East & Africa held 27.0% of the global market in 2025, equivalent to USD 0.43 Billion. Saudi Arabia, the UAE, Oman, and key offshore African markets drive the region. The area benefits from large upstream investment, long-life reservoirs, and broad use of smart-well architectures in conventional assets. Saudi Arabia remains the anchor market, while the UAE and Oman support offshore and gas-related demand. The competitive landscape favors vendors with established service infrastructure and smart-well capability. Adoption still skews toward hydraulic systems today, but electric and autonomous inflow-control products are gaining traction as operators target lower intervention cost and cleaner data capture.

North America

North America held 24.0% of the global market in 2025, equivalent to USD 0.38 Billion. The United States dominates the region, followed by Canada and Mexico. The strongest intelligent-completion demand comes from the U.S. Gulf of Mexico, higher-value offshore developments, water-management programs, and selected mature-field applications. The region is a major buyer because it combines deep technical completion capability with strong supplier presence. Growth remains selective in onshore plays due to cost sensitivity, while offshore and specialty brownfield projects drive most intelligent-completion spend.

Asia Pacific

Asia Pacific held 19.0% of the global market in 2025, equivalent to USD 0.30 Billion. China, Australia, India, and Malaysia are the most relevant countries. China drives demand through offshore development and gas-field complexity. Australia contributes through offshore gas and subsea projects where intervention costs are high. India adds gradual demand through offshore redevelopment and selective complex wells. Malaysia is strategically important for inflow-control and water-management solutions. Asia Pacific combines gas-field development, offshore complexity, and rising appetite for remote reservoir management.

Europe

Europe held 18.0% of the global market in 2025, equivalent to USD 0.29 Billion. Norway leads by a wide margin, followed by the UK, Denmark, and the Netherlands. The North Sea remains the region’s core demand center because operators need surveillance-rich, intervention-light completions in offshore fields with aging infrastructure and high operating cost. Europe’s demand pattern favors high-reliability systems, strong permanent monitoring, and lower-intervention designs. That creates good conditions for electric and fiber-assisted architectures, even though overall upstream growth remains slower than in the Middle East and Latin America.

Latin America

Latin America held 12.0% of the global market in 2025, equivalent to USD 0.19 Billion. Brazil dominates the region by a wide margin, followed by Mexico, Guyana, and Argentina. Brazil is the main engine because deepwater developments increasingly use premium intelligent completions. Mexico remains a secondary offshore market with selective demand, while Guyana offers medium-term upside as development intensity rises. Latin America’s growth profile is the strongest among regions from a lower base because Brazil is pushing more multiwell, higher-spec offshore systems into commercial use.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Downhole Flow-Control Equipment

- Sensors and Monitoring Systems

- Surface Control and Communication Systems

- Packers, Isolation, and Ancillary Completion Tools

By Technology

- Hydraulic Intelligent Completions

- Electric and Electro-hydraulic Intelligent Completions

- Wireless and Autonomous Inflow-Control Systems

By Application

- Production-Rate Control

- Water and Gas Control

- Reservoir Surveillance and Zonal Monitoring

- Injection Control

By Well Architecture

- Horizontal Wells

- Multilateral Wells

- Vertical and Deviated Wells

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.6 B |

| Forecast Revenue (2034) | USD 2.6 B |

| CAGR (2025-2034) | 5.5% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component (Downhole Flow-Control Equipment, Sensors and Monitoring Systems, Surface Control and Communication Systems, Packers, Isolation, and Ancillary Completion Tools), By Technology (Hydraulic Intelligent Completions, Electric and Electro-hydraulic Intelligent Completions, Wireless and Autonomous Inflow-Control Systems), By Application (Production-Rate Control, Water and Gas Control, Reservoir Surveillance and Zonal Monitoring, Injection Control), By Well Architecture (Horizontal Wells, Multilateral Wells, Vertical and Deviated Wells) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, NOV, EXPRO, TAQA, PACKERS PLUS, TENDEKA, OMEGA COMPLETION TECHNOLOGY, TAM INTERNATIONAL, WELLTEC, INTELLISERV, INFLOWCONTROL, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Hydraulic Intelligent Completions, Electric & Electro-hydraulic Intelligent Completions, Wireless & Autonomous Inflow-Control Systems), By Application (Production-Rate Control, Water & Gas Control, Reservoir Surveillance & Zonal Monitoring, Injection Control), By Well Architecture (Horizontal Wells, Multilateral Wells, Vertical & Deviated Wells) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

, By Technology (Hydraulic Intelligent Completions, Electric & Electro-hydraulic Intelligent Completions, Wireless & Autonomous Inflow-Control Systems), By Application (Production-Rate Control, Water & Gas Control, Reservoir Surveillance & Zonal Monitoring, Injection Control), By Well Architecture (Horizontal Wells, Multilateral Wells, Vertical & Deviated Wells) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

, By Technology (Hydraulic Intelligent Completions, Electric & Electro-hydraulic Intelligent Completions, Wireless & Autonomous Inflow-Control Systems), By Application (Production-Rate Control, Water & Gas Control, Reservoir Surveillance & Zonal Monitoring, Injection Control), By Well Architecture (Horizontal Wells, Multilateral Wells, Vertical & Deviated Wells) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Intelligent Well Completion Market?

The Global Intelligent Well Completion Market was valued at USD 1.6 Billion in 2025, projected to reach USD 2.6 Billion by 2034 at a CAGR of 5.5% from 2026–2034. Growth is driven by rising adoption of smart well technologies, real-time reservoir monitoring, zonal flow control systems, and increasing offshore oil and gas development activities.

Who are the major players in the Intelligent Well Completion Market?

SLB, HALLIBURTON, BAKER HUGHES, WEATHERFORD, NOV, EXPRO, TAQA, PACKERS PLUS, TENDEKA, OMEGA COMPLETION TECHNOLOGY, TAM INTERNATIONAL, WELLTEC, INTELLISERV, INFLOWCONTROL, Others

Which segments covered the Intelligent Well Completion Market?

By Component (Downhole Flow-Control Equipment, Sensors and Monitoring Systems, Surface Control and Communication Systems, Packers, Isolation, and Ancillary Completion Tools), By Technology (Hydraulic Intelligent Completions, Electric and Electro-hydraulic Intelligent Completions, Wireless and Autonomous Inflow-Control Systems), By Application (Production-Rate Control, Water and Gas Control, Reservoir Surveillance and Zonal Monitoring, Injection Control), By Well Architecture (Horizontal Wells, Multilateral Wells, Vertical and Deviated Wells)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Intelligent Well Completion Market

Published Date : 16 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date