- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Invoice Factoring Platform Market Size, Share | CAGR 17.3%

Global Invoice Factoring Platform Market Size, Share, Growth Analysis By Component (Core Factoring Engine, Origination & Underwriting Modules, Compliance & Risk Analytics, Managed Services), By Factoring Type (Recourse, Non-Recourse, Reverse Factoring, Spot Factoring, Confidential Factoring), By End-User (Banks, Fintech Lenders, SMBs, Corporate Treasury), Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

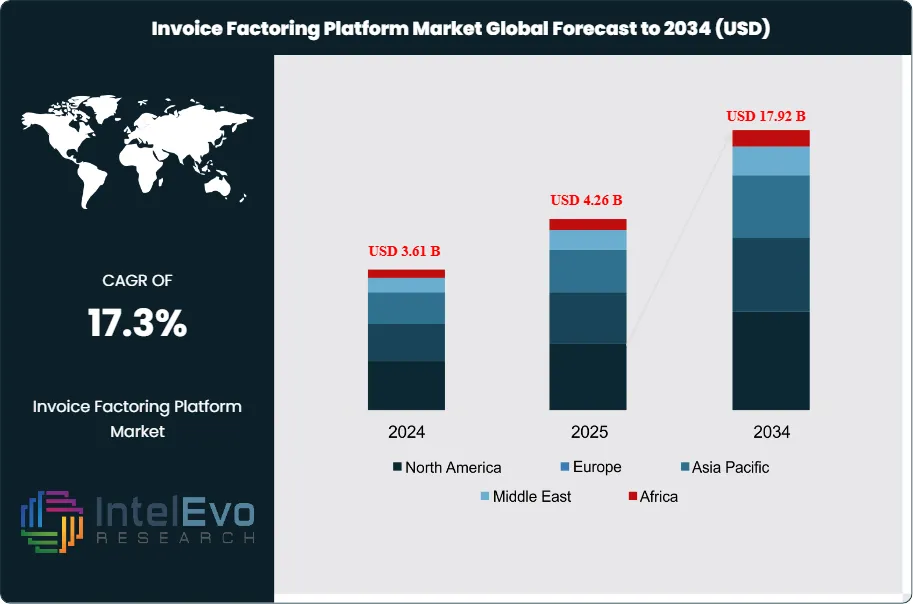

| USD 4.26 Billion | USD 17.92 Billion | 17.3% | Europe, 36.2% |

The Invoice Factoring Platform Market was valued at approximately USD 3.61 Billion in 2024 and reached USD 4.26 Billion in 2025. The market is projected to grow to USD 17.92 Billion by 2034, expanding at a CAGR of 17.3% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 13.66 billion over the analysis period — a trajectory driven by the structural tightening of bank SME lending appetite following the 2023 regional-banking stress, the commercial maturity of API-based accounting and ERP integration that eliminates manual invoice verification, and a policy environment in which both the European Union and the United Kingdom have made late-payment enforcement a material SME protection agenda since 2024.

Get More Information about this report -

Request Free Sample ReportThree specific causal forces explain the invoice factoring platform market's 2025 valuation and distinguish its current trajectory from earlier factoring technology cycles. First, the revised EU Late Payment Regulation — adopted by the European Parliament in April 2025 and replacing Directive 2011/7/EU — imposes a harmonized 30-day maximum payment term on B2B transactions (60 days where expressly agreed in writing and objectively justified), with automatic statutory interest accruing at the ECB reference rate plus 8 percentage points for late invoices. Rather than reducing factoring demand by shortening payment cycles, the regulation expanded the addressable market: late-payment enforcement is uneven across member states, and SMEs increasingly use factoring platforms as a behavioral mechanism to capture guaranteed early payment rather than pursue uncertain statutory recovery. Industry analysis indicates European factoring platform transaction volume increased 22% in the six months following the regulation's adoption. Second, U.S. regional banks retrenched from unsecured SME credit between 2023 and 2025 following the stress events at Silicon Valley Bank, First Republic, and Signature Bank, reducing unsecured SME lending approval rates at banks under USD 50 billion in assets from 56% in 2022 to 33% in 2024 — a contraction that pushed 2.1 million U.S. small businesses toward receivables-backed financing alternatives, with factoring platforms capturing approximately 38% of the displaced demand based on reported origination volumes at leading vendors. Third, the cost of commercial bank time-deposit capital rose to a decade-high of 5.1% average cost at U.S. community banks in Q1 2024 before declining to 4.2% in 2025 — a funding-cost environment that re-rated factoring economics in favor of platform-based models, where capital efficiency, risk-based pricing, and AI-driven buyer credit assessment offset the margin compression that higher funding costs would otherwise impose.

While the invoice factoring platform market's headline growth signals uniform expansion, underlying dynamics reveal a widening divide between embedded-finance-enabled platforms and traditional standalone factoring software vendors. Embedded factoring revenue — where invoice financing is offered natively inside ERP, accounts-payable automation, and B2B marketplace platforms rather than as a separate application SME sellers must seek out — grew at an estimated 31.8% in 2025, nearly double the overall market CAGR. Standalone factoring software, by contrast, is experiencing stagnant new-client growth in mature markets as mid-size banks increasingly prefer ERP-integrated alternatives that distribute factoring directly to their existing SME customers. This pattern closely mirrors the payroll software consolidation of 2017–2021, when embedded payroll inside HR platforms steadily displaced point-solution payroll vendors despite the point vendors' superior standalone functionality — a structural displacement that took six years to fully unfold and that independent factoring platforms appear to be entering in 2025.

AI-driven underwriting and dynamic discounting are restructuring the invoice factoring platform market's value proposition beyond capital access. Factoring platforms deploying buyer-level credit scoring models — trained on payment behavior data across millions of invoices — can price factoring fees with 12-to-18-basis-point greater precision than traditional seller-only underwriting, allowing platforms to approve SMEs that banks and traditional factors reject while maintaining equivalent loss rates. Preliminary Q1 2025 data from platform operators suggests AI-underwritten factoring portfolios achieve net credit losses of 0.7–1.1% versus 1.4–1.9% on portfolios underwritten using legacy seller-financial-statement models — a 60-basis-point risk improvement that, applied to a USD 42-billion annual advance volume at Demica alone, equates to USD 250 million in reduced annual credit losses across the European mid-market factoring platform segment.

, By Factoring Type (Recourse, Non-Recourse, Reverse Factoring, Spot Factoring, Confidential Factoring), By End-User (Banks, Fintech Lenders, SMBs, Corporate Treasury), Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global invoice factoring platform market was valued at USD 4.26 billion in 2025 and is forecast to reach USD 17.92 billion by 2034 at a CAGR of 17.3% (2026–2034), driven by SME credit retrenchment at regional banks, EU late-payment regulation reform, and AI-powered buyer credit assessment that is unlocking previously underwriteable SME segments.

- Segment Dominance: Reverse factoring (supply chain finance) held 39.4% of factoring-type revenue in 2025. Its leadership reflects the structural cost advantage of buyer-led financing: large corporate buyers borrow against their own investment-grade balance sheets at 150–250 bps below the rates their SME suppliers could access independently, creating a savings pool that factoring platforms capture through recurring program management fees averaging 0.3–0.6% of program flow.

- Segment Dominance: Transportation and logistics captured 24.6% of industry-vertical revenue in 2025, the largest vertical in the invoice factoring platform market. Its lead is causally linked to the segment's structural cash-flow timing mismatch — trucking operators pay fuel and driver costs daily but wait 30–60 days for shipper payment — a mismatch that makes factoring a non-discretionary operating utility rather than a discretionary finance option, particularly for the 1.6 million owner-operator and small fleet trucking firms that collectively generated USD 42 billion in factored receivables in 2025.

- Driver: U.S. regional bank SME credit approval rates contracted from 56% (2022) to 33% (2024) following regional banking stress events, pushing 2.1 million small businesses toward receivables-backed financing and driving USD 11.4 billion in incremental invoice factoring platform origination volume in 2024–2025 — the largest bank-credit-displacement migration in U.S. SME finance since the 2008 financial crisis.

- Restraint: Fraud exposure — specifically fabricated or duplicate-financed invoices — constrained 2025 platform margin economics; industry aggregated loss data indicates invoice fraud accounted for 0.9–1.4% of funded volume across independent factoring platforms, compared with 0.3% for bank-operated programs. The gap is narrowing as platforms deploy blockchain-based invoice uniqueness verification and ERP direct-connection validation, but remediation investment added USD 180 million to industry compliance costs in 2025.

- Opportunity: Embedded factoring inside B2B e-commerce, procurement, and accounts-receivable SaaS platforms represents an addressable market of USD 4.3 billion by 2034 as platforms including Shopify B2B, BigCommerce, and SAP Ariba integrate native factoring offers that convert SME sellers into instant-cash recipients at invoice generation — a distribution model that bypasses traditional broker networks and cuts customer acquisition cost by an estimated 78% versus direct-to-SME marketing.

- Trend: Real-time ERP and accounting-software API integrations have reached 62% of new invoice factoring platform client deployments in 2025, up from 24% in 2022. QuickBooks Online, Xero, NetSuite, and SAP Business One connections now enable automatic invoice ingestion and eligibility screening, eliminating manual document upload and reducing time-to-first-funding from an industry average of 5.4 days to under 6 hours at leading platforms.

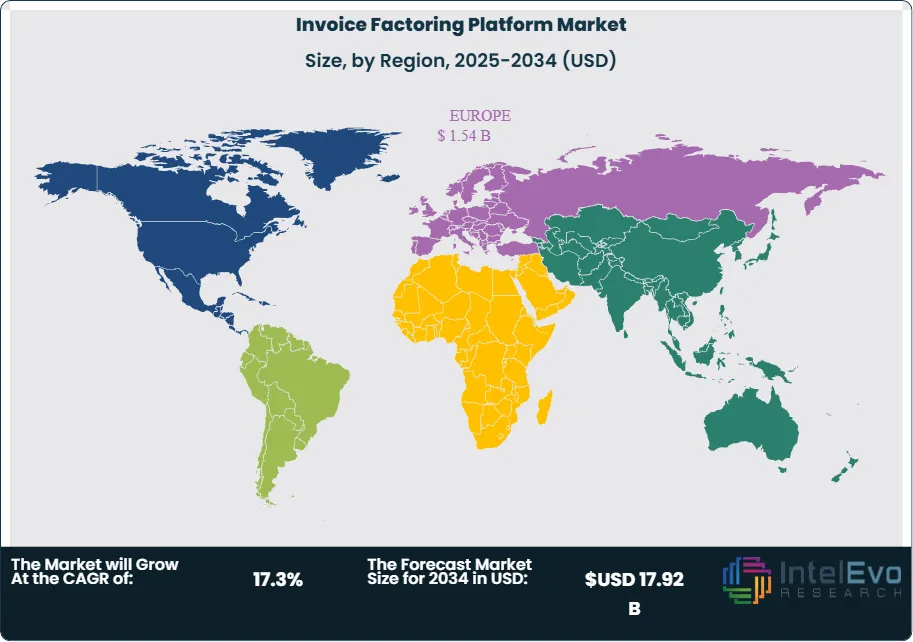

- Regional Analysis: Europe led the global invoice factoring platform market with 36.2% share, equivalent to USD 1.54 billion in 2025, anchored by the revised EU Late Payment Regulation, the EU Factors Chain International (FCI) network connecting 380+ factors across 90 countries, and the highest B2B factoring penetration globally (11.4% of EU GDP flows through factoring arrangements versus 1.8% in the United States).

Competitive Landscape Overview

The global invoice factoring platform market is moderately fragmented, with the top four platforms — BlueVine (Bill.com), Fundbox, C2FO, and Taulia (SAP) — collectively controlling approximately 47% of digital factoring platform revenue in 2025. Competition is multi-dimensional: in the SMB spot-factoring segment, competition is speed- and approval-rate-driven, with platforms differentiating on time-to-funding and AI-powered instant credit decisioning; in the reverse-factoring corporate segment, competition is distribution-driven and based on the depth of ERP partnerships (Taulia's SAP ownership provides an essentially uncontested position within the SAP Ariba ecosystem); and in the bank-operated-platform segment, competition is technology-white-labeling driven, with vendors including Demica and Kyriba licensing their platforms to banks that then deliver factoring to their own SME clients. The competitive environment intensified during 2024–2025 as traditional core banking vendors (Finastra, Temenos) extended into factoring modules, and as payment networks (Mastercard's acquisition of Minna Technologies' factoring arm in 2024) entered via receivables-related acquisitions.

A competitive dynamic actively reshaping the invoice factoring platform market in 2025–2026 is the vertical integration of commercial banks into factoring platform infrastructure ownership. JPMorgan's Q2 2025 announcement of a dedicated digital factoring platform (Chase Working Capital Direct) for SMEs in its Chase Business segment represents the first time a Tier-1 U.S. bank has operated a proprietary factoring platform rather than partnering with third-party vendors. The strategic implication is significant: if the top 10 U.S. banks follow JPMorgan's model, the addressable market for independent factoring platforms shrinks by an estimated USD 1.6 billion in annual revenue by 2028, as bank-direct offerings capture SME customers that would otherwise be served by platform vendors. Independent platforms are responding by deepening vertical-specific product features (freight factoring, healthcare receivables, staffing) where bank generic offerings cannot match the operational specialization that vertical focus provides.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move (2024–2026) |

| BlueVine (Bill.com) | USA | Leader | BlueVine Invoice Factoring | North America | Feb 2025: Integrated AI-powered buyer credit scoring into factoring underwriting, reducing approval time from 24 hours to 12 minutes. |

| Fundbox Inc. | USA | Leader | Fundbox Credit / Pay | North America | Apr 2025: Secured USD 200M warehouse facility from JPMorgan to expand SMB invoice-backed credit lines to USD 150K per client. |

| C2FO | USA | Leader | C2FO Working Capital Platform | Global | Jan 2025: Surpassed USD 2T in cumulative funded receivables across 1.2M buyer-supplier relationships in 175 countries. |

| Taulia (SAP) | USA | Challenger | Taulia Working Capital Finance | North America / Europe | Nov 2024: Deepened SAP Business Network integration, enabling single-click factoring inside SAP Ariba for 6.7M connected suppliers. |

| Kyriba Corp. | USA | Challenger | Kyriba Supplier Finance | Europe / North America | Mar 2025: Launched Kyriba Receivables Finance module integrating ISO 20022 remittance messaging with factoring workflows. |

| Demica Limited | UK | Challenger | Demica Receivables Finance Platform | Europe / Asia Pacific | Jun 2025: Facilitated USD 42B in receivables financing flows for Tier-1 corporates in H1 2025, up 31% year-on-year. |

| MarketFinance (Kriya) | UK | Niche Player | Kriya B2B Pay & Finance | Europe | Aug 2025: Partnered with Lloyds Bank to embed invoice factoring into Lloyds Business Banking for 1.1M SME accounts. |

| Tradeshift | USA/Denmark | Niche Player | Tradeshift Cash | Europe / Asia Pacific | Dec 2024: Completed merger with HSBC's trade finance digital unit, forming a USD 500M joint venture for embedded B2B finance. |

By Component:

Core factoring software platforms constituted the dominant component of the invoice factoring platform market in 2025, capturing 46.7% of revenue at USD 1.99 billion. Their leadership reflects the technical centrality of the factoring engine — which manages invoice ingestion, eligibility determination, advance calculation, collections workflow, and reserve accounting — as the non-discretionary infrastructure underpinning every factoring transaction regardless of product variation. Demica's receivables finance platform, processing USD 42 billion in H1 2025 flows for Tier-1 European corporates, exemplifies how core platform capability translates into program scale: platforms capable of handling multi-currency, multi-jurisdiction, multi-buyer structures command licensing fees 4–6x those of single-market simple-factoring systems, creating a technical-capability-based tiered pricing structure that rewards vendors that have invested in complex deal support.

Origination and underwriting modules accounted for 22.8% of component revenue (USD 971 million, 2025), with a growth rate of 24.1% exceeding the overall market average. The specific event accelerating underwriting module adoption above the market baseline is the commercial availability of AI-powered buyer credit scoring that references aggregated cross-platform payment history — a capability that emerged at production scale in 2024–2025 as data networks (C2FO's 1.2-million-buyer-supplier-relationship dataset, Taulia's 6.7-million-supplier SAP Business Network) reached the training-data volume required for credible machine learning models. The non-obvious competitive dynamic here is the self-reinforcing nature of underwriting data: the larger a platform's invoice volume, the more accurate its buyer-behavior predictions become, which lowers credit losses, which funds more aggressive pricing, which attracts more volume — a flywheel that structurally advantages the top three platforms and creates a widening credit-performance gap relative to sub-scale competitors.

Compliance, KYC and risk analytics modules held 14.6% share (USD 622 million, 2025). The FinCEN Beneficial Ownership Information (BOI) reporting requirements under the Corporate Transparency Act (CTA), effective January 2024 and modified by the March 2025 final rule for smaller reporting companies, created a direct procurement cycle for KYC automation tools that can validate invoice-seller beneficial ownership without manual document review. Integration and professional services contributed 10.4% (USD 443 million), reflecting the complexity of connecting factoring platforms to SME accounting systems, buyer ERP environments, and bank core deposit systems. Managed services and support accounted for the remaining 5.5%, growing at 21.6% as smaller banks without dedicated factoring operations staff outsource platform operations to vendor-managed environments.

By Factoring Type:

Reverse factoring, also known as supply chain finance or supplier finance, commanded 39.4% of factoring-type revenue (USD 1.68 billion, 2025), the largest single sub-segment in the invoice factoring platform market. The specific reason reverse factoring leads is the economic asymmetry it exploits: a buyer-led program allows investment-grade corporate sponsors to provide liquidity to their SME suppliers at the buyer's credit spread (typically 80–160 bps over SOFR for BBB-rated corporates) rather than the supplier's spread (typically 400–900 bps over SOFR for unrated SMEs), creating 200–700 bps of interest-rate arbitrage that the program shares among buyer (through extended payment terms), supplier (through early payment), and platform operator (through program fees). Walmart, Procter & Gamble, and Unilever each operate reverse factoring programs exceeding USD 3 billion in annual supplier-advanced volume, demonstrating that the model is standard operating procedure at global consumer-goods scale, not a niche innovation.

Non-recourse factoring held 21.6% share (USD 920 million, 2025). Its growth accelerated following Basel III final rule implementation timelines that favor balance-sheet treatment of non-recourse receivables purchases over recourse structures for bank sellers. Recourse factoring retained 18.8% (USD 801 million), concentrated among smaller SMEs where credit-risk-sharing with the platform operator enables approval for sellers whose buyer portfolios are too concentrated or sub-investment-grade for non-recourse pricing. Spot/single-invoice factoring accounted for 13.1% of revenue — a share that understates its strategic importance as the entry product through which the majority of first-time SME factoring users enter the market, typically migrating to full-ledger factoring relationships within 12–18 months of initial spot transactions. Confidential (undisclosed) factoring held the remaining 7.1%, primarily in the UK where the product originated and where HMRC enforcement frameworks accommodate the buyer-unnotified structure that most other jurisdictions discourage or prohibit.

By Deployment:

Cloud-native SaaS deployment captured 56.8% of the invoice factoring platform market in 2025 (USD 2.42 billion), with its share accelerating from 38.4% in 2022 as regulatory supervisory guidance (including the OCC's 2024 update to SR 23-4 on third-party technology risk management) explicitly endorsed cloud-hosted lending platforms under appropriate vendor oversight frameworks. Cloud deployment's structural advantage is capital efficiency: factoring platforms experience significant volume variability (seasonal peaks in retail-supplier factoring, quarter-end surges in corporate buyer programs), and elastic cloud infrastructure scales without the capital expenditure required for on-premise capacity planning. Vendors operating on cloud-native architectures, including BlueVine and Fundbox, report infrastructure cost per funded invoice that is 42–58% lower than legacy on-premise-deployed competitors.

Hybrid cloud and on-premise deployment retained 32.6% share (USD 1.39 billion, 2025), primarily among Tier-1 European banks whose factoring operations are integrated with on-premise core banking deposit and commercial lending systems, and among Japanese and German corporate treasuries where data residency preferences exceed cloud deployment's operating cost advantages. Bank-operated private cloud deployment held 10.6%, concentrated among banks operating proprietary factoring platforms (JPMorgan's Chase Working Capital Direct, HSBC's Trade Finance platform) that require data segregation levels available only in dedicated bank-controlled infrastructure.

By End-User:

Banks and specialty finance companies constituted the largest end-user segment of the invoice factoring platform market in 2025, capturing 32.8% of revenue at USD 1.40 billion. The leading position reflects a structural reality: commercial banks originate approximately 71% of global factoring volume by dollar amount, according to Factors Chain International aggregated industry statistics, making banks the dominant category of platform purchaser even as non-bank fintech originators generate disproportionate share-of-voice in market coverage. Santander, BNP Paribas, and HSBC each operate proprietary factoring platforms serving 40,000+ corporate clients, with their technology investment decisions materially affecting the addressable market for independent platform vendors.

Fintech lenders and embedded-finance providers held 24.6% share (USD 1.05 billion, 2025), growing at 23.1%. Independent factoring firms retained 18.4% (USD 784 million) — a declining share as bank-operated platforms and fintech embedded-finance offerings capture SMEs that previously used specialized factoring firms as primary providers. Corporate treasury (reverse factoring sponsors) accounted for 15.8%, reflecting the platform fees corporates pay to operate supplier-finance programs rather than the underlying advance volume, which is generally funded by third-party capital providers. SMB and mid-market sellers constituted the remaining 8.4% — a segment where platforms sell directly to small business owners rather than through intermediaries, with customer acquisition cost remaining the primary economic constraint on broader direct-SME distribution.

By Industry Vertical:

Transportation and logistics captured 24.6% of industry-vertical revenue in 2025 (USD 1.05 billion), the largest vertical segment of the invoice factoring platform market. The segment's leadership stems from structural characteristics unique to the freight industry: owner-operators and small fleets operate with daily cash-out requirements (diesel fuel averaging USD 3.82 per gallon in 2025, driver wages paid weekly) but face shipper payment cycles averaging 32–47 days, creating an unavoidable working capital gap that cannot be managed through retained earnings at the operator's typical scale. The American Trucking Associations reports approximately 1.6 million owner-operator and small-fleet firms in the U.S. alone, and industry data indicates 44–52% of these firms use factoring as primary or sole accounts-receivable management — the highest factoring penetration of any U.S. industry vertical.

Manufacturing and wholesale held 19.4% share (USD 827 million, 2025), primarily through reverse factoring programs sponsored by Tier-1 consumer goods and industrial companies. Staffing and business services accounted for 16.8% — a vertical where the 1-2 week pay cycle to contract workers versus 30-60 day client invoice payment creates a cash-flow gap conceptually similar to trucking but at higher absolute dollar values per staffing firm. Construction and engineering held 13.2%, constrained by the industry's high invoice-dispute rate (liquidated damages, retention holdbacks, change-order disagreements) that makes invoice factoring riskier and therefore more expensive for this vertical than lower-dispute industries. Healthcare and medical receivables accounted for 11.4%, with its growth driven by the Physician Fee Schedule's 2024–2025 reimbursement timing pressures on small medical practices. Retail and e-commerce captured the remaining 9.6%, growing at 26.7% as Amazon Business, Shopify B2B, and similar platforms integrate embedded factoring for their merchant ecosystems.

Regional Analysis

Europe:

Regulatory mandates under the revised EU Late Payment Regulation — adopted April 2025 and replacing Directive 2011/7/EU — combined with Europe's structurally higher factoring penetration (11.4% of GDP versus 1.8% in the United States), positioned Europe as the global leader in the invoice factoring platform market with 36.2% share worth USD 1.54 billion in 2025. The United Kingdom generates approximately 28% of European factoring platform revenue despite its post-Brexit regulatory independence, anchored by London-headquartered Kriya (formerly MarketFinance) and Demica, both of which operate among Europe's most advanced AI-enabled factoring platforms. Germany's Mittelstand manufacturing base — approximately 3.5 million SMEs employing 60% of the country's workforce — represents the single largest national factoring market in continental Europe, with Frankfurt-headquartered Sparkassen-Finanzgruppe and Hamburg Commercial Bank operating competing proprietary factoring platforms that together process an estimated EUR 180 billion in annual advances. France ranks second, where Paris-based BNP Paribas Factor and Credit Agricole Leasing & Factoring generate a combined EUR 110 billion in annual advance volume under the Comite de Reglementation Bancaire framework. Italy's tightly regulated factoring sector, governed by Bank of Italy supervisory guidance on receivables finance, produces a disproportionately strong non-recourse factoring mix (67% of Italian factoring is non-recourse versus 52% EU average) driven by Italian bank preferences for off-balance-sheet receivables treatment.

North America:

Backed by the sharpest SME credit contraction at U.S. regional banks since the 2008 financial crisis and a fintech regulatory environment that has broadly accommodated non-bank factoring platforms, North America's invoice factoring platform market captured 30.4% of global revenue at USD 1.29 billion in 2025. The United States dominates regional activity, with Redwood City-headquartered BlueVine (now part of Bill.com) and San Francisco-based Fundbox collectively serving over 200,000 active SME factoring clients. Dallas-Fort Worth's concentration of freight factoring specialists — including TBS Factoring Service, OTR Capital, and Triumph Business Capital — reflects the geographic correlation between trucking-industry headquarters and factoring infrastructure: Triumph Business Capital alone financed approximately USD 24 billion in trucking invoices in 2024. Chicago's commodity trading ecosystem anchors a distinct specialty factoring segment serving agricultural and metals supply chains. Canadian market activity concentrated in Toronto's Bay Street financial district, where RBC's Business Financial Services segment and Scotia Capital's receivables finance division compete with independent platforms including Greenbox Capital and Merchant Growth Capital. Mexico's nearshoring manufacturing boom — with over USD 40 billion in announced manufacturing investment committed in 2024 alone, concentrated in Monterrey, Saltillo, and the Bajio region — is generating a new demand source for supply-chain-finance-oriented factoring platforms serving the cross-border auto-parts, electronics, and medical-device supply chains.

Asia Pacific:

Manufacturing supply chains concentrated across Guangdong and Jiangsu provinces in China, India's priority-sector lending framework that classifies invoice financing as MSME credit, and Singapore's Networked Trade Platform that digitized cross-border trade documents propelled the Asia Pacific invoice factoring platform market to 20.4% global share, valued at USD 869 million in 2025. Singapore functions as the region's factoring technology hub, hosting headquarters of Demica's Asia Pacific operations, Validus Capital, and the Trade Finance Market platform, while the Infocomm Media Development Authority's Trade Trust blockchain framework provides document-verification infrastructure that reduces invoice fraud risk in cross-border factoring. India's Reserve Bank of India-regulated Trade Receivables Discounting System (TReDS) — with three operational platforms (Receivables Exchange of India, Mynd Solutions' M1xchange, and A.TReDS) — processed approximately INR 5.1 trillion (USD 61 billion) in MSME invoice financing in the fiscal year ending March 2025, making India's regulated receivables exchange the highest-volume structured factoring market in Asia by transaction count. China's rapidly growing e-commerce and B2B platform ecosystems, anchored by Alibaba's Ant Group subsidiary MYbank and JD.com's JD Finance, are embedding factoring directly into their B2B marketplaces — an integration model that is likely to become the dominant Chinese factoring distribution channel by 2028 given the platforms' combined SME reach of over 50 million active business accounts. Australia's 2024 introduction of the Payment Times Reporting Act created late-payment transparency obligations on large businesses, creating indirect demand for factoring platforms as SMEs increasingly monitor and respond to buyer payment behavior.

Latin America:

Chronic working-capital constraints at Latin American SMEs — where the World Bank estimates 51% of small firms cite access to finance as a major operating constraint versus 25% global average — combined with the region's generally short-duration commercial payment cycles (averaging 64 days in Brazil versus 38 days in North America) create unusually strong structural demand for invoice factoring, lifting Latin America's platform market to USD 382 million (9.0% global share) in 2025. Brazil leads regional activity, where Sao Paulo-headquartered Gerencianet, ContaAzul Pay, and Omie operate embedded factoring inside their SME accounting and financial management platforms, reaching an estimated 1.4 million Brazilian SMEs. The Brazilian Securities and Exchange Commission (CVM) Instruction 175, effective January 2024, regulated FIDC (Fundo de Investimento em Direitos Creditorios — investment funds in credit rights) structures that serve as the primary capital source for Brazilian factoring platforms, providing a regulatory framework for institutional capital deployment into factoring that is more developed than in any other Latin American jurisdiction. Mexico's BBVA Mexico and Banorte operate competing supplier finance platforms serving the Monterrey and Mexico City industrial-corridor supply chains, with nearshoring demand driving double-digit annual growth through 2025. Chile's well-developed factoring infrastructure under Superintendencia de Bancos e Instituciones Financieras supervision produces the region's highest factoring-to-GDP penetration (2.8%) outside of Europe, demonstrating that regulatory clarity and supervisory quality are more determinative of factoring market depth than absolute GDP scale. Argentina's severe currency volatility has paradoxically stimulated dollar-denominated factoring platforms that enable exporter SMEs to convert peso-denominated receivables to stable-dollar advances — a niche serving an estimated 18,000 Argentine exporting firms.

Middle East & Africa:

Saudi Arabia's Vision 2030 SME development agenda and the UAE's Federal SME Law (Federal Decree-Law No. 23 of 2022) implementation — which mandates that federal and Emirate-level government entities allocate 10% of procurement to SMEs and pay SME suppliers within 15 working days — created the MEA invoice factoring platform market's growth foundation, supporting a regional market size of USD 171 million (4.0% global share) in 2025. The UAE concentrates roughly 54% of regional factoring platform revenue through the Dubai Multi Commodities Centre (DMCC) and Dubai International Financial Centre (DIFC), both of which host licensed factoring firms and digital platforms serving the Gulf region's commodity trading, construction, and services sectors. Emirates NBD's Business Banking Invoice Finance product and Mashreq's NEOBiz platform compete with specialist fintech factors including Beehive, Lendo (expanded from Saudi Arabia), and Funding Souq to serve the UAE's approximately 557,000 registered SMEs. Saudi Arabia's fintech regulatory sandbox, administered by SAMA, licensed three invoice financing platforms by mid-2025: Raqamyah, Forus Financial, and the Saudi factoring arm of Lendo — collectively financing an estimated USD 1.2 billion in SME invoices since their 2022–2023 commercial launches. South Africa's Johannesburg-based Investec Factoring and Rand Merchant Bank's supplier finance division anchor Sub-Saharan African factoring infrastructure, with Standard Bank's announcement of a pan-African factoring platform in Q2 2025 representing the most significant expansion of intra-African factoring capability since FCI's Africa Chapter formation in 2019.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Component

- Software Platform (Core Factoring Engine)

- Origination & Underwriting Modules

- Compliance, KYC & Risk Analytics

- Integration & Professional Services

- Managed Services & Support

By Factoring Type

- Recourse Factoring

- Non-Recourse Factoring

- Reverse Factoring / Supply Chain Finance

- Spot / Single-Invoice Factoring

- Confidential / Undisclosed Factoring

By Deployment

- Cloud-Native SaaS

- Hybrid Cloud / On-Premise

- Bank-Operated Private Cloud

By End-User

- Banks & Specialty Finance Companies

- Independent Factoring Firms

- Fintech Lenders & Embedded Finance Providers

- Corporate Treasury (Reverse Factoring Sponsors)

- SMB & Mid-Market Sellers

By Industry Vertical

- Manufacturing & Wholesale

- Transportation & Logistics

- Staffing & Business Services

- Construction & Engineering

- Healthcare & Medical Receivables

- Retail & E-Commerce

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 4.26 B |

| Forecast Revenue (2034) | USD 17.92 B |

| CAGR (2025-2034) | 17.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Component, (Software Platform (Core Factoring Engine), Origination & Underwriting Modules, Compliance, KYC & Risk Analytics, Integration & Professional Services, Managed Services & Support), By Factoring Type, (Recourse Factoring, Non-Recourse Factoring, Reverse Factoring / Supply Chain Finance, Spot / Single-Invoice Factoring, Confidential / Undisclosed Factoring), By Deployment, (Cloud-Native SaaS, Hybrid Cloud / On-Premise, Bank-Operated Private Cloud), By End-User, (Banks & Specialty Finance Companies, Independent Factoring Firms, Fintech Lenders & Embedded Finance Providers, Corporate Treasury (Reverse Factoring Sponsors), SMB & Mid-Market Sellers), By Industry Vertical, (Manufacturing & Wholesale, Transportation & Logistics, Staffing & Business Services, Construction & Engineering, Healthcare & Medical Receivables, Retail & E-Commerce) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BLUEVINE (BILL.COM HOLDINGS, INC.), FUNDBOX INC., C2FO LLC, TAULIA LLC (SAP SE), KYRIBA CORPORATION, DEMICA LIMITED, MARKETFINANCE (KRIYA), TRADESHIFT HOLDINGS, INC., TRIUMPH BUSINESS CAPITAL, INC., TBS FACTORING SERVICE, LLC, GREENSILL CAPITAL SUCCESSOR PLATFORMS, INVOICEINTEREST (NOW PRIMEREVENUE, INC.), EFACTOR NETWORK, LENDINGKART FINANCE LIMITED, VALIDUS CAPITAL PTE. LTD., BEEHIVE P2P LIMITED, RAQAMYAH PLATFORM, LENDO, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Factoring Type (Recourse, Non-Recourse, Reverse Factoring, Spot Factoring, Confidential Factoring), By End-User (Banks, Fintech Lenders, SMBs, Corporate Treasury), Industry Trends & Forecast 2026-2034")

, By Factoring Type (Recourse, Non-Recourse, Reverse Factoring, Spot Factoring, Confidential Factoring), By End-User (Banks, Fintech Lenders, SMBs, Corporate Treasury), Industry Trends & Forecast 2026-2034")

, By Factoring Type (Recourse, Non-Recourse, Reverse Factoring, Spot Factoring, Confidential Factoring), By End-User (Banks, Fintech Lenders, SMBs, Corporate Treasury), Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Invoice Factoring Platform Market?

The Global Invoice Factoring Platform Market was valued at USD 3.61 Billion in 2024 and is projected to reach USD 17.92 Billion by 2034, growing at a CAGR of 17.3% from 2026 to 2034, driven by rising demand for alternative working capital financing, increasing adoption of digital invoice financing solutions, AI-powered risk assessment tools, blockchain-based invoice verification, and expanding embedded finance ecosystems across global trade and B2B payment markets.

Who are the major players in the Invoice Factoring Platform Market?

BLUEVINE (BILL.COM HOLDINGS, INC.), FUNDBOX INC., C2FO LLC, TAULIA LLC (SAP SE), KYRIBA CORPORATION, DEMICA LIMITED, MARKETFINANCE (KRIYA), TRADESHIFT HOLDINGS, INC., TRIUMPH BUSINESS CAPITAL, INC., TBS FACTORING SERVICE, LLC, GREENSILL CAPITAL SUCCESSOR PLATFORMS, INVOICEINTEREST (NOW PRIMEREVENUE, INC.), EFACTOR NETWORK, LENDINGKART FINANCE LIMITED, VALIDUS CAPITAL PTE. LTD., BEEHIVE P2P LIMITED, RAQAMYAH PLATFORM, LENDO, OTHERS

Which segments covered the Invoice Factoring Platform Market?

By Component, (Software Platform (Core Factoring Engine), Origination & Underwriting Modules, Compliance, KYC & Risk Analytics, Integration & Professional Services, Managed Services & Support), By Factoring Type, (Recourse Factoring, Non-Recourse Factoring, Reverse Factoring / Supply Chain Finance, Spot / Single-Invoice Factoring, Confidential / Undisclosed Factoring), By Deployment, (Cloud-Native SaaS, Hybrid Cloud / On-Premise, Bank-Operated Private Cloud), By End-User, (Banks & Specialty Finance Companies, Independent Factoring Firms, Fintech Lenders & Embedded Finance Providers, Corporate Treasury (Reverse Factoring Sponsors), SMB & Mid-Market Sellers), By Industry Vertical, (Manufacturing & Wholesale, Transportation & Logistics, Staffing & Business Services, Construction & Engineering, Healthcare & Medical Receivables, Retail & E-Commerce)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Invoice Factoring Platform Market

Published Date : 26 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date