- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Kitchen Sinks Market Size, Share & Forecast 2034 | CAGR 4.8%

Global Kitchen Sinks Market Size, Share, Analysis By Number of Bowls (Single Bowl, Double Bowl, Multi Bowl), By Material (Metallic, Granite, Composite and Others), By Application (Residential Kitchens, Commercial Kitchens, Hospitality and Foodservice), By Distribution Channel (Retail, E-commerce, Specialty Stores), By End-User, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 3.14 Billion | USD 4.8 Billion | 4.8% | Asia Pacific, 35% |

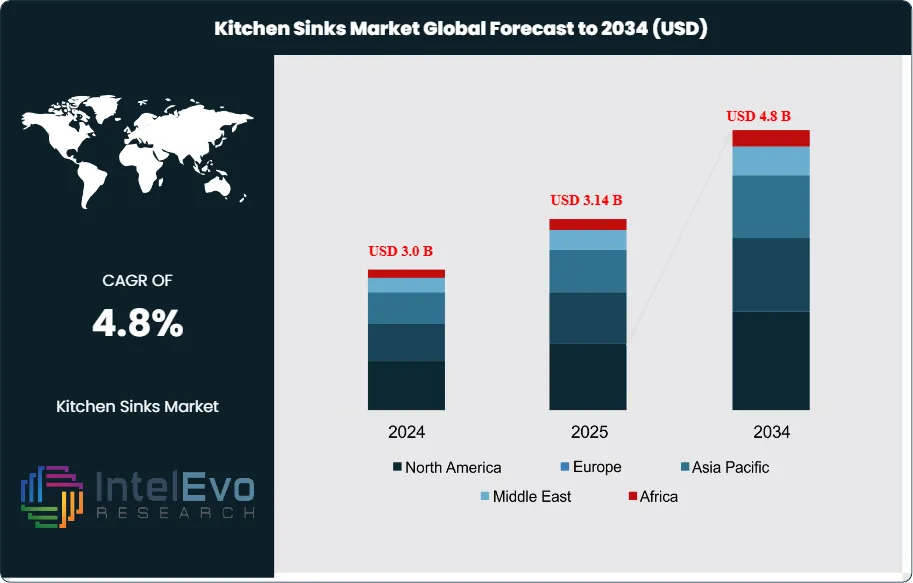

The Kitchen Sinks Market is estimated at USD 3.0 billion in 2024 and is on track to reach roughly USD 4.8 billion by 2034, the market is further estimated to reach approximately USD 3.14 billion in 2025, and is expected to expand at a compound annual growth rate (CAGR) of around 4.8% during the forecast period from 2026 to 2034. Growth is driven by rising residential construction, increasing kitchen remodelling activities, and growing demand for modern, durable, and aesthetically appealing sink designs. Additionally, the expansion of modular kitchens and rising consumer preference for stainless steel and composite materials are further supporting market growth globally.

Get More Information about this report -

Request Free Sample ReportDemand rises with sustained investment in kitchen upgrades and steady new-build housing. Houzz reports that median renovation spending increased by 60% from 2020 to 2023, while typical kitchen remodel budgets often fall between $56,000 and $104,000. In the 2024 Houzz & Home Study, more than half of homeowners reported spending $25,000 or more on renovation projects in 2023. These budgets support premium sink purchases tied to countertop replacement, cabinetry refresh cycles, and higher expectations for fit-and-finish. Urbanization reinforces the trend, with over 56% of the global population living in urban areas and a growing middle class in China and India allocating more spend to home improvement.

The product mix continues to shift, but stainless steel remains the revenue anchor due to price-performance and broad installer familiarity. Stainless steel is estimated to hold about 55% of 2024 revenue, while composite granite and engineered materials approach 20% as consumers prioritize scratch resistance and visual differentiation. Ceramics and fireclay retain a premium niche near 15%, supported by design-led renovation projects. Residential applications account for roughly three-quarters of volume, while foodservice and light commercial segments value deep basins, stain resistance, and faster replacement cycles. E-commerce and direct-to-consumer channels now represent an estimated 30% of unit sales, supported by improved product visualization and standardized cutout templates.

On the supply side, producers face stainless steel price volatility, freight exposure, and regional tariff risk, which can compress margins when pass-through lags. Plumbing codes, material safety rules, and water-efficiency standards shape product development, especially for integrated accessories, coatings, and waste systems. Manufacturers expand automation in forming, welding, and finishing to stabilize quality and reduce labor variability. AI-enabled demand sensing and digital twins improve SKU planning and defect detection, while configuration tools reduce returns in online channels. North America and Western Europe remain the primary premium pools, while India, Southeast Asia, and select Middle East cities emerge as the fastest-growing investment hotspots driven by urban housing and organized retail expansion.

, By Material (Metallic, Granite, Composite and Others), By Application (Residential Kitchens, Commercial Kitchens, Hospitality and Foodservice), By Distribution Channel (Retail, E-commerce, Specialty Stores), By End-User, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

Key Takeaways

- Market Growth: The kitchen sinks market grows from 2.9 billion USD, 2023 to 4.6 billion USD, 2033 at 4.8% CAGR, 2024-2034. It reaches estimated: 3.0 billion USD, 2024 under a steady upgrade-driven demand base.

- Segment Dominance: Single bowl sinks lead with 37.1%, 2023 due to compact layouts and faster installation cycles. The segment expands at estimated: 4.6%, 2024-2034 as urban kitchens favor space efficiency.

- Segment Dominance: Metallic sinks hold 51.0%, 2023 driven by durability and finish consistency. The category sustains estimated: 52.0%, 2024 as steel-led portfolios remain the default choice in mass channels.

- Driver: New housing supply and renovation activity lift volumes, supported by 56.0%, 2024 global urban population share. The market converts this demand into estimated: 0.2 billion USD, 2024 incremental annual revenue uplift across replacement and new-build cycles.

- Restraint: Input-cost volatility pressures margins, with stainless steel pricing risk estimated: 8.0%, 2024 year-over-year variability. Supply-chain lead times add friction at estimated: 6.0 weeks, 2024 for imported SKUs.

- Opportunity: Premium and eco-positioned products open upside, with sustainable-material adoption estimated: 12.0%, 2024 of new launches. Manufacturers capture estimated: 0.7 billion USD, 2033 revenue from composite and designer finishes as consumers trade up.

- Trend: Brands accelerate digital commerce and configuration tools, pushing online channel mix to estimated: 30.0%, 2024 of unit sales. Product teams adopt automation and AI quality inspection at estimated: 18.0%, 2024 of tier-1 plants to reduce defect rates.

- Regional Analysis: Asia Pacific leads with 35.0%, 2023 on rapid urbanization and construction growth. The region delivers estimated: 1.1 billion USD, 2024 market value and sustains estimated: 5.4%, 2024-2034 growth momentum.

Competitive Landscape

The Global Kitchen Sinks Market is moderately fragmented, with the top five manufacturers accounting for an estimated 30.0%–36.0% of 2025 market revenue. Competition is design-driven and brand-oriented, with material innovation, aesthetics, distribution reach, and integration with modular kitchen ecosystems shaping market share more than pure pricing. Competitive intensity increased in 2025–2026 as companies expanded premium product lines, introduced smart and sustainable sinks, and strengthened partnerships with real estate developers and kitchen solution providers.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| FRANKE GROUP | Switzerland | Leader | Stainless steel, granite, and smart kitchen sinks | Europe, North America, Asia | Expanded smart sink solutions and integrated kitchen systems in 2025. |

| BLANCO | Germany | Leader | Premium granite composite and stainless steel sinks | Europe, North America | Strengthened SILGRANIT product line and expanded premium distribution in 2025. |

| KOHLER CO. | US | Leader | Designer kitchen sinks and integrated kitchen fixtures | North America, Global premium markets | Expanded smart kitchen portfolio and luxury product offerings in 2025. |

| ELKAY MANUFACTURING | US | Leader | Stainless steel sinks and commercial kitchen solutions | North America | Invested in commercial and residential hybrid sink solutions in 2025. |

| TOTO LTD. | Japan | Leader | High-end kitchen and sanitary solutions | Asia-Pacific, Global premium | Expanded integrated kitchen and water-efficient solutions in 2025. |

| ROCA SANITARIO | Spain | Challenger | Affordable and mid-range kitchen sink solutions | Europe, Latin America | Strengthened distribution in emerging markets in 2025. |

| HANSGROHE | Germany | Challenger | Premium kitchen fixtures and sink systems | Europe, North America | Expanded designer sink collections and digital retail channels in 2025. |

| DURAVIT AG | Germany | Challenger | Designer kitchen and sanitary products | Europe | Focused on sustainable materials and premium product positioning in 2025. |

| HAFELE | Germany | Niche Player | Modular kitchen solutions including sinks and accessories | Europe, Asia | Expanded modular kitchen partnerships and project-based sales in 2025. |

| ASTRACAST (SCHOCK) | UK/Germany | Niche Player | Composite and granite sinks | Europe | Focused on eco-friendly materials and online retail growth in 2025. |

Summary Insight:

The market is shifting toward premiumization, sustainability, and smart kitchen integration, with increasing importance of modular kitchen ecosystems and e-commerce distribution. Companies with strong brand positioning, innovative materials, and partnerships with developers and kitchen solution providers are gaining competitive advantage, while smaller players compete through price and regional distribution through 2034.

By Type

Single bowl sinks remain the largest configuration in the global kitchen sinks market, accounting for about 37.1 percent of total demand in 2024. Their adoption is driven by compact kitchen layouts and the need to handle oversized cookware efficiently. In urban apartments and mid-sized homes, single bowl designs support better counter utilization, which aligns with ongoing space constraints in new housing developments across Asia Pacific and Europe.

From a functional standpoint, single bowl sinks reduce installation complexity and long-term upkeep. Fewer joints and partitions lower cleaning time and maintenance costs, which appeals to cost-sensitive households and rental properties. This factor supports stable replacement demand, particularly in renovation-led markets such as the United States, Germany, and Japan.

Double and multi-bowl sinks continue to serve differentiated needs. Double bowl units attract users who prioritize task separation, especially in family households and small commercial kitchens. Multi-bowl formats remain limited to high-traffic environments, but steady product upgrades such as integrated drainboards and accessory rails sustain incremental growth through 2030.

By Application

Residential kitchens account for the majority of sink installations, driven by ongoing remodeling activity and steady housing completions. Kitchen upgrades represent one of the highest renovation spending categories globally, with average kitchen remodel costs exceeding USD 55,000 in North America as of 2024. Sink replacement typically coincides with countertop upgrades, supporting recurring demand.

Commercial applications include restaurants, hospitality venues, and institutional kitchens. These buyers emphasize capacity, material strength, and compliance with hygiene standards. Stainless steel sinks dominate this segment due to resistance to corrosion and high usage tolerance. Growth remains moderate but stable, supported by foodservice expansion in urban centers.

Emerging applications include modular kitchens and prefabricated housing projects. These formats favor standardized sink sizes and materials, which supports volume-driven contracts for manufacturers supplying large developers and modular kitchen brands.

By End-Use

Residential buildings represent roughly three-quarters of total market volume in 2025. Rising urban household formation and higher disposable income in emerging economies sustain demand for visually consistent and durable sink products. Homeowners increasingly replace sinks during cosmetic upgrades rather than functional failure, shortening replacement cycles.

Commercial buildings contribute a smaller but stable share. Office cafeterias, hotels, and quick-service restaurants prioritize durability and ease of sanitation. Replacement frequency is higher than residential use, but purchase decisions remain cost-driven and standardized.

Industrial buildings account for a limited share of demand. Usage is confined to employee facilities and light food-processing units, which limits volume but ensures consistent baseline consumption across regions.

By Region

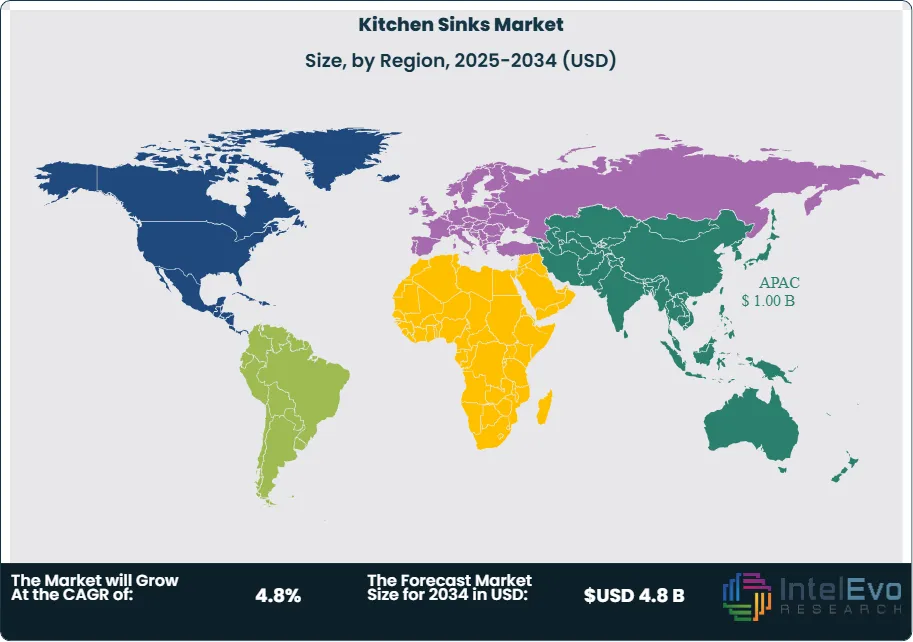

Asia Pacific leads the global kitchen sinks market with around 35 percent share in 2025, equivalent to more than USD 1.0 billion in annual revenue. Rapid urbanization, high residential construction activity, and income growth in China and India underpin this position. Local manufacturing capacity also supports pricing competitiveness and supply reliability.

North America and Europe remain mature but high-value markets. Demand centers on replacement sales, premium materials, and aesthetic alignment with modular kitchen systems. Stainless steel and composite sinks dominate new installations in these regions.

Latin America and the Middle East and Africa represent emerging growth areas. Expanding urban housing, government-backed residential projects, and gradual formalization of retail distribution support long-term demand expansion through the early 2030s.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Number of Bowls

- Single Bowl

- Double Bowl

- Multi Bowl

By Material

- Metallic

- Granite

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.14 B |

| Forecast Revenue (2034) | USD 4.8 B |

| CAGR (2025-2034) | 4.8% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Number of Bowls, (Single Bowl, Double Bowl, Multi Bowl), By Material, (Metallic, Granite, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Kohler Co., Acrysil Limited, Ruvati USA, AGA, Duravit AG, Swanstone, Frigidaire, Zuhne, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Material (Metallic, Granite, Composite and Others), By Application (Residential Kitchens, Commercial Kitchens, Hospitality and Foodservice), By Distribution Channel (Retail, E-commerce, Specialty Stores), By End-User, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

, By Material (Metallic, Granite, Composite and Others), By Application (Residential Kitchens, Commercial Kitchens, Hospitality and Foodservice), By Distribution Channel (Retail, E-commerce, Specialty Stores), By End-User, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

, By Material (Metallic, Granite, Composite and Others), By Application (Residential Kitchens, Commercial Kitchens, Hospitality and Foodservice), By Distribution Channel (Retail, E-commerce, Specialty Stores), By End-User, Industry Trends, Competitive Landscape, Key Players, Regional Insights & Forecast 2026–2034")

Frequently Asked Questions

How big is the Kitchen Sinks Market?

The Global Kitchen Sinks Market was valued at USD 3.14 Billion in 2025, projected to hit USD 4.8 Billion by 2034, growing at a CAGR of 4.8% from 2026–2034, driven by rising home renovation, modular kitchen demand, and durable sink materials.

Who are the major players in the Kitchen Sinks Market?

Kohler Co., Acrysil Limited, Ruvati USA, AGA, Duravit AG, Swanstone, Frigidaire, Zuhne, Other Key Players

Which segments covered the Kitchen Sinks Market?

By Number of Bowls, (Single Bowl, Double Bowl, Multi Bowl), By Material, (Metallic, Granite, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date