- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Knee Hyaluronic Acid Injections Market Size | CAGR of 5.6%

Global Knee Hyaluronic Acid Injections Market Size, Share, and In-Depth Analysis By Product Type (Single Injection, Three Injection, Five Injection), By End-Use (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers), By Application (Osteoarthritis, Cartilage Repair, Other Knee Joint Disorders), Industry Region & Key Players, Market Dynamics, Pricing Analysis, Competitive Strategies, Clinical Trends & Forecast 2025–2034

Report Overview

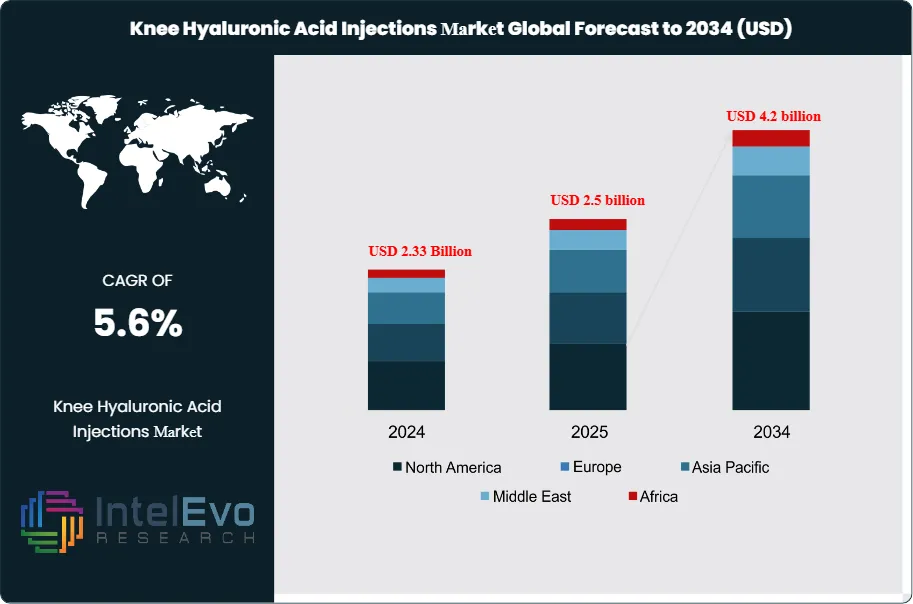

The Knee Hyaluronic Acid Injections Market is estimated to reach approximately USD 2.5 billion in 2025 and is projected to grow steadily to around USD 4.2 billion by 2034. Based on an estimated USD 2.6 billion market size in 2026, the market is expected to register a compound annual growth rate (CAGR) of about 5.6% during the forecast period from 2026 to 2034. This growth is primarily driven by the rising prevalence of knee osteoarthritis, an expanding aging population, and increasing preference for minimally invasive, non-surgical treatment options. In addition, growing awareness among patients and physicians, along with advancements in viscosupplementation formulations that offer longer-lasting pain relief, continue to support sustained market demand and visibility across global healthcare platforms.

Get More Information about this report -

Request Free Sample ReportThis expansion reflects sustained demand for non-surgical interventions for osteoarthritis as health systems seek to delay or reduce the need for total knee replacement. In 2023, the market stood at about USD 2.2 billion, underscoring steady growth momentum into the current forecast period.

Demand rises as osteoarthritis prevalence climbs, particularly in aging populations and among individuals with obesity and joint trauma. More than 32 million adults in the United States live with osteoarthritis, and knee involvement represents a significant share of these cases. Patients and clinicians increasingly prefer viscosupplementation as an intermediate option between oral therapies and invasive surgery, supporting procedure volumes in hospital outpatient departments and orthopedic clinics. Growing awareness of quality-of-life impacts and earlier diagnosis further lift case identification and treatment rates.

On the supply side, global and regional manufacturers compete on formulation performance, injection schedules, and price. Leading companies together account for an estimated 45–50% of global revenue, while a long tail of regional players serves local markets through partnerships and licensing agreements. Vendors expand portfolios from single-injection to multi-injection regimens and explore combinations with corticosteroids to extend symptom relief. Capacity expansions in Asia and contract manufacturing in cost-competitive locations help suppliers manage margin pressure as payers tighten reimbursement.

Regulation shapes market access and development timelines. The U.S. Food and Drug Administration and comparable agencies in Europe and Asia enforce rigorous standards for safety, efficacy, and labeling, which elevate development costs but protect clinical outcomes. Healthcare spending, which represented roughly 17–18% of U.S. GDP in 2020, sustains payer budgets for osteoarthritis care, though reimbursement reviews and pricing negotiations introduce policy risk. Changes in clinical guidelines or safety signals could alter utilization patterns, particularly where payers favor alternative pain therapies.

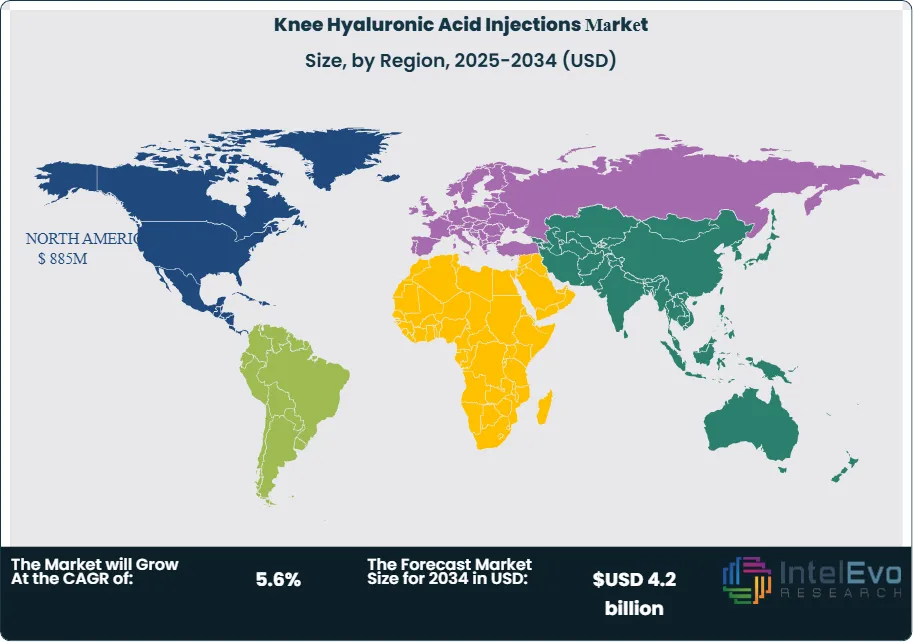

Technology and digitalization begin to influence clinical decision-making and product life-cycle management. Providers adopt imaging-guided injection techniques to improve accuracy, while AI-enabled tools analyze electronic health records to identify candidates likely to respond to viscosupplementation. Automated fill-finish lines and digital quality systems enhance manufacturing efficiency and compliance. Regionally, North America holds around 38% of 2024 revenue, Europe contributes about 30%, and Asia-Pacific delivers the fastest growth, with a projected CAGR above 6.5% as China, India, and Southeast Asia expand access to osteoarthritis care. Emerging opportunities in Latin America and the Middle East and Africa focus on private hospitals, specialty orthopedic centers, and value-segment products.

, By End-Use (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers), By Application (Osteoarthritis, Cartilage Repair, Other Knee Joint Disorders), Industry Region & Key Players, Market Dynamics, Pricing Analysis, Competitive Strategies, Clinical Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market grows from 2.2 billion USD, 2023 to estimated: USD 2.5 billion in 2025 and is projected to reach USD 4.2 billion, 2034, delivering a CAGR of 5.6%, 2026-2034.

- Segment Dominance: The three-injection product segment leads the portfolio, capturing 41.0% of global revenue, 2024, while alternative regimens hold the remaining estimated: 59.0% share, 2024.

- Segment Dominance: Hospitals account for 56.0% of procedure volume, 2024, while orthopedic clinics and ambulatory surgical centers together manage the remaining estimated: 44.0% of cases, 2024. Within indications, osteoarthritis holds 44.0% of market revenue, 2024 and remains the primary clinical focus.

- Driver: Rising osteoarthritis prevalence, with an estimated: 35.0 million patients worldwide, 2024 and a strong preference for non-surgical pain relief drive steady market expansion at a 5.2% CAGR, 2024-2034.

- Restraint: Stringent regulatory review cycles and reimbursement controls limit faster acceleration, with an estimated: 12.0% of claims, 2024 facing coverage restrictions or step-therapy requirements.

- Opportunity: Asia-Pacific presents an attractive expansion runway, with revenue expected to rise from estimated: 0.5 billion USD, 2024 to estimated: 1.0 billion USD, 2034 at a projected CAGR of 6.8%, 2024-2034 as access and diagnosis rates improve.

- Trend: Providers increasingly shift interventions from inpatient theaters to outpatient and day-care settings, where hospitals, clinics, and ambulatory centers already handle over 80.0% of procedures, 2024, reducing cost per case by an estimated: 10.0%, 2024.

- Regional Analysis: North America leads with a 37.8% revenue share, 2024 equating to 0.83 billion USD, 2024, followed by Europe at an estimated: 30.0% share, 2024, while Asia-Pacific grows fastest at an estimated CAGR of 6.8%, 2024-2034 and Latin America plus the Middle East and Africa together approach estimated: 0.6 billion USD, 2034.

By Product

The product mix in the knee hyaluronic acid injections market continues to shift in 2025 as healthcare providers seek treatment formats that reduce patient visits while maintaining clinical outcomes. Single-injection products show strong adoption as they shorten procedure time and appeal to patients who want fewer appointments. Many health systems report rising use of single-dose formats in 2024 and 2025 as outpatient volumes increase. The segment maintains momentum as suppliers improve viscosity profiles and extend durability.

Three-injection products remain the largest segment, accounting for more than 41 percent of global volume in the latest assessment year. Providers continue to rely on this regimen because it balances convenience with sustained symptom control. Clinical data published between 2022 and 2024 strengthened confidence in multi-dose protocols for moderate osteoarthritis, which has helped preserve their leadership position.

Five-injection regimens serve a narrower but clinically important patient group. Specialists often choose this approach for advanced degenerative cases that require longer therapeutic coverage. Although the segment remains smaller than the others, demand is stable. Clinical trials planned for 2025 focus on extending pain-relief intervals, which could influence future adoption. Overall, product innovation and growing osteoarthritis prevalence among adults over 60 continue to support a steady expansion trajectory for all treatment formats.

By Application

Osteoarthritis continues to account for the bulk of procedure demand in 2025, holding more than 44 percent of global market share. Rising diagnosis rates and earlier clinical intervention support ongoing use of viscosupplementation as a preferred non-surgical option. Providers report that patient preference for injectable therapies has increased as awareness of joint-preservation approaches improves.

The cartilage repair segment maintains a meaningful share as specialists integrate hyaluronic acid into broader regenerative treatment plans. Adoption has strengthened in orthopedic centers that combine injections with biologics, physical therapy, or minimally invasive surgery. Studies tracking cartilage health outcomes have expanded interest across Asia and Europe.

Other knee joint disorders, including ligament injury-related degeneration and inflammatory conditions, represent a smaller but steadily growing category. These applications highlight the flexibility of hyaluronic acid formulations in addressing pain and mobility concerns across a varied patient population. Continued research through 2025 is expected to widen clinical indications, gradually increasing the contribution of these secondary segments.

By End-Use

Hospitals remain the primary channel for knee hyaluronic acid injections in 2025, representing more than 56 percent of global utilization. Their dominance reflects broader access to imaging tools, specialist teams, and reimbursement frameworks that support high patient throughput. Systems in North America, Europe, and large Asian metros continue to prioritize outpatient musculoskeletal services, helping maintain high injection volumes.

Orthopedic clinics account for the second-largest share. They attract patients seeking specialized musculoskeletal care and faster scheduling. Clinics in the United States, Japan, Germany, and South Korea report stable year-over-year growth as early-stage osteoarthritis cases shift toward non-surgical management.

Ambulatory surgical centers show rising activity as health systems move routine procedures into cost-efficient outpatient environments. ASCs report steady growth in procedure counts, with adoption highest in the United States and Canada. The “others” category includes rehabilitation centers and multi-specialty outpatient networks, which continue to expand access as payers promote lower-cost care settings.

By Region

North America maintains the largest share in 2025, supported by advanced clinical infrastructure and a high documented prevalence of osteoarthritis. The United States alone reports more than 32 million adults with the condition. These figures, combined with broad insurance coverage, keep the region above 37 percent of global revenue.

Europe follows with strong participation driven by aging populations in Germany, France, Italy, and the United Kingdom. National health systems continue to expand treatment pathways for joint-degeneration conditions, which helps sustain stable demand. Adoption levels remain high in Western Europe as clinicians integrate viscosupplementation into broader pain-management programs.

Asia Pacific is the fastest-growing regional market. China, India, South Korea, and Japan report rising case volumes due to expanding older populations and improved diagnostic access. Health systems are increasing investment in orthopedic care, creating long-term opportunities for suppliers. Latin America and the Middle East & Africa show gradual progress as healthcare spending increases and awareness of non-surgical treatment options improves. Rising use of outpatient centers in Brazil, Mexico, Saudi Arabia, and the UAE supports moderate but steady market expansion.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

Product

- Single Injection

- Three Injection

- Five Injection

End-Use

- Hospitals

- Orthopedic Clinics

- Ambulatory Surgical Centers

- Others

Application

- Osteoarthritis

- Cartilage Repair

- Other Knee Joint Disorders

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.5 billion |

| Forecast Revenue (2034) | USD 4.2 billion |

| CAGR (2025-2034) | 5.6% |

| Historical data | |

| Base Year For Estimation | |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Product (Single Injection, Three Injection, Five Injection), End-Use (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers, Others), Application (Osteoarthritis, Cartilage Repair, Other Knee Joint Disorders) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Haohai Biological Technology, Zimmer Biomet, Fidia Farmaceutici S.p.A, Seikagaku Corporation, Hanmi Pharm Co. Ltd. (Teva Pharmaceuticals Industries Ltd.), Institut Biochimique SA (Bioventus LLC), Sanofi, Chugai Pharmaceuticals Co. Ltd., Meiji Seika Pharma Co. Ltd. (OrthogenRx), Hunan Jingfeng Pharmaceutical Co. Ltd., Anika Therapeutics Inc. (DePuy Synthes Inc.), Ferring B.V., Viatris Inc. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-Use (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers), By Application (Osteoarthritis, Cartilage Repair, Other Knee Joint Disorders), Industry Region & Key Players, Market Dynamics, Pricing Analysis, Competitive Strategies, Clinical Trends & Forecast 2025–2034")

, By End-Use (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers), By Application (Osteoarthritis, Cartilage Repair, Other Knee Joint Disorders), Industry Region & Key Players, Market Dynamics, Pricing Analysis, Competitive Strategies, Clinical Trends & Forecast 2025–2034")

, By End-Use (Hospitals, Orthopedic Clinics, Ambulatory Surgical Centers), By Application (Osteoarthritis, Cartilage Repair, Other Knee Joint Disorders), Industry Region & Key Players, Market Dynamics, Pricing Analysis, Competitive Strategies, Clinical Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Knee Hyaluronic Acid Injections Маrkеt

Published Date : 30 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date