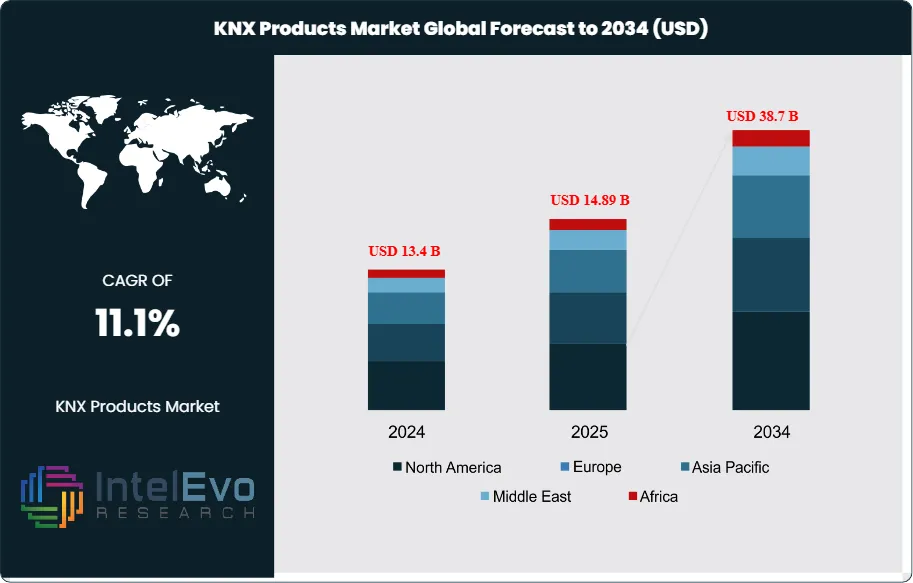

The KNX Products Market is projected to reach approximately USD 38.7 Billion by 2034, up from USD 13.4 Billion in 2024, growing at a CAGR of around 11.1% during 2025–2034. Smart building automation, increasing energy efficiency regulations, and rapid adoption of IoT in commercial and residential spaces are fueling market expansion. KNX is becoming a preferred standard for integrated control systems worldwide, supporting lighting, HVAC, security, and smart metering. As smart cities continue to rise, KNX-based solutions are set to become a core enabler of intelligent infrastructure.

The KNX Products Market encompasses building automation systems based on the KNX open standard protocol, including sensors, actuators, system devices, and software solutions for residential, commercial, and industrial applications. KNX technology enables intelligent control of lighting, HVAC, security, energy management, and other building functions through a standardized communication protocol. The market covers hardware components, software platforms, installation services, and maintenance solutions across global regions.

The market is experiencing robust growth driven by increasing demand for energy-efficient buildings, rising electricity costs, and growing awareness of smart building benefits. Government regulations promoting energy efficiency, such as the EU's Energy Performance of Buildings Directive requiring nearly zero-energy buildings by 2025, are accelerating adoption. The integration of IoT technologies, artificial intelligence, and cloud-based solutions is expanding KNX capabilities and market reach. Additionally, the growing trend toward sustainable construction and green building certifications is creating substantial market opportunities.

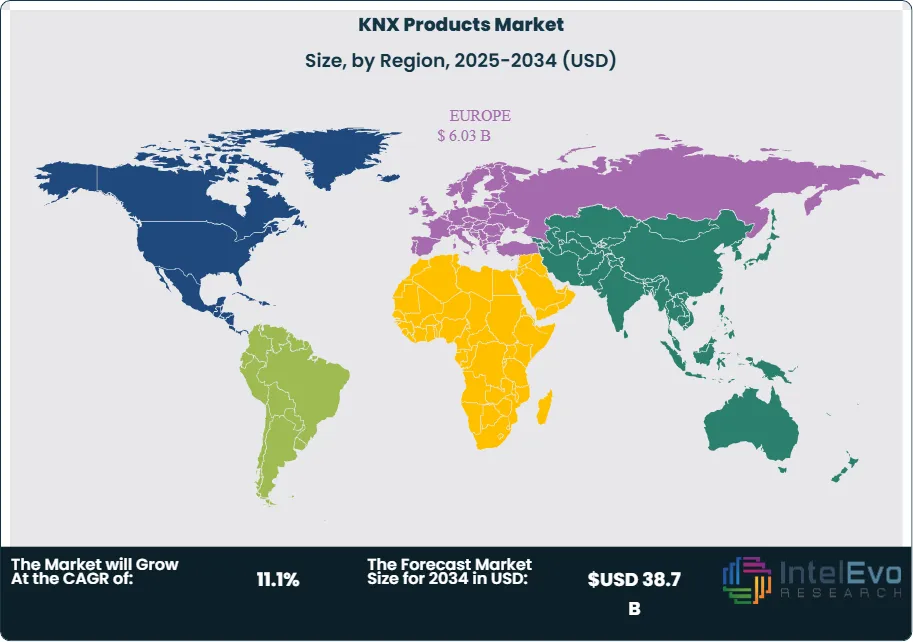

Europe maintains market leadership, accounting for approximately 45-50% of global demand, driven by regulatory support, high energy costs, and advanced building automation adoption. North America represents 20-25% of the market, with strong growth in smart residential applications. The Asia-Pacific region is experiencing the fastest growth at 12-14% CAGR, led by China's urbanization and Japan's technology adoption. China specifically is forecasted to reach $2.4 billion by 2030, growing at 14.1% CAGR, while the US market is valued at $1.7 billion in 2024.

The pandemic initially disrupted supply chains and construction activities, causing temporary market contraction in 2020-2021. However, it accelerated adoption of smart building technologies for health monitoring, contactless controls, and energy management. Increased focus on indoor air quality, occupancy monitoring, and remote building management created new market opportunities. The shift toward hybrid work models and smart homes boosted residential segment demand while commercial projects experienced temporary delays.

The Russia-Ukraine conflict has affected European energy markets, accelerating demand for energy efficient building solutions and KNX technologies. Supply chain disruptions have increased component costs and delivery times, though this has been partially offset by regional sourcing initiatives. Trade tensions between major economies have encouraged companies to diversify manufacturing locations and develop regional supply networks. Semiconductor shortages have impacted production capacity, leading to longer lead times and strategic inventory management.

Key Takeaways

Market Growth: The KNX Products Market is expected to reach USD 38.7 Billion by 2034, driven by increasing adoption of smart home and building automation solutions, rising focus on energy efficiency, and growing demand for IoT integration in building management systems.

Product Type Dominance: Sensors lead market share due to smart building technology adoption.

Application Dominance: Lighting control dominates, driven by energy savings potential and widespread adoption.

End User Dominance: Residential buildings dominate market share, driven by smart home demand.

Driver: Smart building adoption & energy efficiency and IoT integration & building modernization accelerate growth through sustainability requirements and advanced automation capabilities.

Restraint: High implementation costs & system complexity and limited awareness in emerging markets create barriers through significant upfront investments and technical expertise requirements.

Opportunity: Emerging markets expansion and IoT integration & cloud connectivity offer growth potential through untapped regions and enhanced system capabilities.

Trend: Wireless technology adoption and AI-powered building optimization are reshaping the market by enabling flexible installations and intelligent automation.

Regional Analysis: Europe leads owing to established infrastructure and supportive regulatory frameworks promoting energy efficiency. Asia-Pacific and North America show high promise due to rapid urbanization and smart city initiatives driving building automation adoption.

Product Type Analysis:

Sensors Leads With over 60% Market Share In KNX Products Market. The KNX products market exhibits distinct product type segmentation patterns, with sensor technologies establishing commanding market leadership through their fundamental role in intelligent building automation systems. This market dominance reflects the accelerating adoption of smart building infrastructure and the widespread deployment of Internet of Things (IoT)-enabled devices across diverse residential and commercial environments. Sensor technology's market supremacy stems from its position as the critical foundational component within KNX ecosystem architectures, where these devices function as the primary data acquisition interface between physical building environments and automated control systems. This foundational role makes sensors indispensable for virtually all KNX installations, regardless of complexity or application scope.

Application Analysis:

Lighting control remains the most established and widely adopted KNX application, prized for its immediate energy-saving results, enhanced occupant comfort, and relatively simple deployment. Contemporary systems combine daylight harvesting, motion detection, and real-time energy monitoring to deliver dynamic, environment-aware illumination that resonates with both residential and commercial users. The segment’s momentum is reinforced by the rapid transition to LED technology and the growing popularity of smart lighting, both of which demand advanced control functions. Meanwhile, HVAC control is expanding swiftly as organizations prioritize indoor air quality and stringent efficiency mandates, and holistic energy-management solutions are gaining ground through their ability to monitor consumption, integrate renewables, and interact intelligently with the electrical grid.

End User Analysis:

Residential buildings establish market leadership in the KNX products sector through surging consumer recognition of energy efficiency benefits, enhanced home security capabilities, and comprehensive convenience advantages offered by intelligent building automation systems. The residential segment's dominance stems from decreasing technology implementation costs that make sophisticated automation accessible to mainstream homeowners, alongside simplified installation procedures that reduce deployment complexity and professional service requirements. Growing availability of retrofit solutions enables existing homes to integrate advanced KNX systems without extensive renovations, expanding market reach beyond new construction projects. Smart home adoption accelerates particularly within developed markets where elevated energy costs create compelling economic incentives for automated energy management, while strong environmental consciousness drives demand for sustainable building technologies that reduce carbon footprints and optimize resource consumption through intelligent system integration and predictive optimization.

Region Analysis:

Europe Leads With more than 45% Market Share In KNX Products Market. Europe establishes commanding global leadership in the KNX products market through comprehensive regulatory frameworks emphasizing energy efficiency, elevated electricity costs that incentivize automation adoption, and deep-rooted environmental consciousness driving sustainable building practices. The European Union's Energy Performance of Buildings Directive requiring nearly zero-energy buildings creates substantial regulatory momentum supporting KNX system implementation across residential and commercial sectors. Germany spearheads European market development, followed by significant adoption in France, Netherlands, and Nordic regions, benefiting from KNX technology's European heritage and well-established installer networks that ensure comprehensive technical support.

North America represents a substantial secondary market experiencing accelerated growth through expanding smart home adoption, intensified energy management focus, and increased commercial building automation investments, with Canada demonstrating strong potential through climate regulations and green building initiatives.

Asia-Pacific emerges as the fastest-expanding region, propelled by China's extensive urbanization and smart city initiatives, while Japan exhibits robust residential technology adoption and South Korea with Australia advance commercial market development. Emerging markets across Latin America and Middle East/Africa demonstrate early-stage growth driven by urbanization trends, infrastructure development, and growing building automation awareness, representing significant long-term expansion opportunities as economic development and rising energy costs stimulate automation adoption.

Product Type (Actuators, Sensors, System Devices); Application (Lighting Control, HVAC Systems, Energy Management, Blinds & Shutters); End User (Commercial Buildings, Residential Buildings , Industrial)

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Siemens, Schneider Electric, ABB, Albrecht Jung GmbH & Co. KG (JUNG), GIRA, Hager (Berker), Legrand, HDL Automation, GVS, STEINEL, Theben AG, Zennio Avance y Tecnología S.L., MDT Technologies GmbH, Ekinex

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA KNX PRODUCTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA KNX PRODUCTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC KNX PRODUCTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA KNX PRODUCTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA KNX PRODUCTS CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA KNX PRODUCTS CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA KNX PRODUCTS CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL KNX PRODUCTS CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Players Analysis:

Siemens: Siemens maintains a leading market position through its comprehensive building automation portfolio and strong industrial expertise. The company's competitive advantage stems from its extensive experience in industrial automation, robust R&D capabilities, and global service network that supports complex building automation projects. Siemens offers a complete ecosystem of KNX-compatible products including sensors, actuators, system components, and software platforms that enable comprehensive building management solutions. Strategic investments in digitalization, IoT integration, and artificial intelligence enhance the company's KNX offerings with advanced analytics and cloud connectivity capabilities. The company's strong presence in both commercial and industrial markets provides cross-selling opportunities and system integration synergies that reinforce its market leadership position.

Schneider Electric: Schneider Electric holds significant market share with a strong focus on sustainability, energy efficiency, and digital transformation in building automation. The company's competitive strength lies in its comprehensive energy management portfolio that integrates seamlessly with KNX systems to deliver optimized building performance. Schneider's expertise in electrical distribution, power management, and industrial automation provides synergistic opportunities for KNX product deployment across diverse market segments. The company's commitment to sustainability and carbon neutrality aligns with market trends toward green building standards and energy efficiency regulations. Strategic partnerships with technology companies, cloud service providers, and systems integrators enable Schneider to deliver comprehensive digital building solutions that leverage KNX's open standard capabilities.

ABB: ABB maintains competitive market share through its strong industrial automation heritage and technological innovation in building control systems. The company's competitive advantage stems from its expertise in power and automation technologies that complement KNX building automation applications. ABB's global presence, established customer relationships in industrial markets, and comprehensive product portfolio enable cross-selling opportunities and system integration projects. The company's investments in robotics, artificial intelligence, and digital technologies enhance its KNX offerings with advanced automation capabilities. Strategic focus on electrification, renewable energy integration, and smart infrastructure positions ABB to capitalize on emerging trends in sustainable building automation and smart city development.

Albrecht Jung GmbH & Co. KG (JUNG): JUNG specializes in premium KNX solutions with strong emphasis on design, quality, and user experience, particularly in the residential and high-end commercial markets. The company's competitive strength lies in its innovative product designs, superior build quality, and comprehensive range of switches, sensors, and control interfaces that enhance building automation aesthetics and functionality. JUNG's focus on user-friendly interfaces, intuitive operation, and seamless integration appeals to architects, designers, and end-users seeking sophisticated automation solutions. The company's strong European market presence and established distribution network provide solid foundation for international expansion and market share growth in premium segments.

Market Key Players

Siemens

Schneider Electric

ABB

Albrecht Jung GmbH & Co. KG (JUNG)

GIRA

Hager (Berker)

Legrand

HDL Automation

GVS

STEINEL

Theben AG

Zennio Avance y Tecnología S.L.

MDT Technologies GmbH

Ekinex

Driver:

Smart Building Adoption & Energy Efficiency Requirements:

The global shift toward intelligent buildings driven by sustainability goals, energy cost reduction, and occupant comfort optimization is the primary catalyst for KNX market growth. Governments worldwide are implementing stringent energy efficiency regulations and green building standards that mandate advanced building automation systems. The European Union's Energy Performance of Buildings Directive, California's Title 24 energy standards, and similar regulations in Asia-Pacific create compelling demand for KNX solutions. Modern buildings require integrated control of lighting, HVAC, shading, and energy systems to achieve net-zero targets and optimize operational efficiency. KNX's open standard approach enables seamless integration of multiple building functions through a unified communication infrastructure, making it the preferred choice for complex building automation projects. The technology's ability to reduce energy consumption by 30-50% through intelligent control algorithms and occupancy-based automation provides compelling return on investment for building owners and operators.

IoT Integration & Building Modernization:

The convergence of IoT technologies with traditional building automation is creating unprecedented opportunities for KNX product deployment. Legacy buildings require modernization to meet contemporary efficiency and comfort standards, driving retrofit market growth that favors flexible KNX solutions. Cloud connectivity, mobile app control, and remote monitoring capabilities are becoming standard expectations for building occupants and facility managers. KNX's evolution toward IP-based communication enables seamless integration with IoT platforms, artificial intelligence, and predictive analytics that optimize building performance and maintenance. The technology's compatibility with voice assistants, smartphone integration, and cloud-based building management platforms appeals to tech-savvy users seeking comprehensive automation experiences. Government smart city initiatives and infrastructure modernization programs provide additional market stimulus, with public buildings, educational institutions, and healthcare facilities implementing KNX systems to improve operational efficiency and occupant experiences.

Restrain:

High Implementation Costs & System Complexity:

KNX systems require significant upfront investment in both hardware and professional installation services, creating barriers for cost-sensitive market segments. The technology's complexity necessitates specialized training for installers and system integrators, limiting the available talent pool and increasing project costs. The ETS (Engineering Tool Software) programming platform, while powerful, is considered complex by many installers, creating resistance to adoption compared to simpler plug-and-play alternatives. Smaller residential projects and budget-conscious commercial installations often opt for less sophisticated solutions that offer lower initial costs despite reduced functionality. The need for detailed system planning, commissioning, and ongoing maintenance requires specialized expertise that may not be readily available in all geographic markets. Additionally, the perception of KNX as a premium solution limits its penetration in price-sensitive segments where simpler wireless alternatives or proprietary systems provide adequate functionality at lower cost points.

Limited Awareness & Regional Market Penetration:

Despite KNX's technical superiority and open standard advantages, awareness remains limited in many global markets, particularly in North America and developing economies where alternative technologies have established market presence. Competing wireless protocols like Z-Wave, ZigBee, and proprietary systems benefit from aggressive marketing, lower perceived complexity, and established distribution channels that challenge KNX adoption. The technology's European origins and strong European market presence can create perception challenges in markets where local or regional solutions are preferred. Limited availability of trained installers and system integrators in emerging markets restricts market expansion potential, while language barriers and cultural preferences for specific technology approaches can impede adoption. The fragmented nature of building automation markets, with varying regulations, standards, and preferred technologies across regions, requires significant investment in market education and localization efforts that may not generate immediate returns for KNX manufacturers and distributors.

Developing countries in Asia-Pacific, Latin America, and Middle East & Africa present substantial growth opportunities as urbanization accelerates and building standards evolve toward international best practices. Rapid economic development, rising middle-class populations, and government investments in smart city infrastructure create favorable conditions for KNX adoption. These markets often lack entrenched legacy systems, enabling leapfrogging to modern building automation technologies that integrate seamlessly with contemporary IoT and cloud platforms. Government initiatives promoting energy efficiency, sustainable development, and smart infrastructure provide policy support for advanced building automation deployment. The growing hospitality, healthcare, and educational sectors in emerging markets require sophisticated building management capabilities that align with KNX's comprehensive automation approach. Local partnerships with regional systems integrators, adapted product portfolios for specific market requirements, and targeted training programs can accelerate market penetration while building sustainable business relationships in high-growth regions.

IoT Integration & Cloud-Connected Building Ecosystems:

The integration of KNX systems with IoT platforms, artificial intelligence, and cloud-based analytics represents a transformative opportunity for market expansion beyond traditional building automation applications. KNX IoT specifications enable seamless connectivity with modern digital ecosystems, allowing integration with smart city infrastructure, energy grid management, and predictive maintenance platforms. Cloud connectivity enables remote monitoring, optimization algorithms, and data analytics that enhance building performance while reducing operational costs. The convergence with artificial intelligence enables predictive control strategies, occupant behavior learning, and autonomous optimization that delivers superior comfort and efficiency outcomes. Integration with renewable energy systems, electric vehicle charging infrastructure, and energy storage solutions positions KNX as a key enabler for sustainable building ecosystems. These advanced capabilities create new revenue opportunities for manufacturers, system integrators, and service providers while differentiating KNX from simpler automation alternatives in the market.

The KNX market is experiencing a significant shift toward wireless solutions driven by the need for flexible installation options and cost-effective retrofit applications. Wireless KNX products eliminate the need for dedicated bus wiring, reducing installation complexity and costs while enabling automation in existing buildings where rewiring is impractical or expensive. This trend is particularly important in the residential retrofit market and heritage buildings where preservation requirements limit invasive installation methods. Battery-powered wireless sensors and actuators are becoming more sophisticated, offering multi-year operation and reliable communication that matches wired system performance. The integration of energy harvesting technologies and improved wireless protocols enhances reliability while reducing maintenance requirements. Hybrid installations combining wired backbone infrastructure with wireless endpoints provide optimal flexibility and performance for complex building automation projects.

AI-Powered Building Optimization & Predictive Analytics:

Artificial intelligence and machine learning integration is transforming KNX systems from reactive automation platforms to predictive, learning environments that optimize building performance autonomously. AI algorithms analyze occupancy patterns, weather data, energy pricing, and system performance to automatically adjust building operations for optimal efficiency and comfort. Predictive maintenance capabilities identify potential equipment failures before they occur, reducing downtime and maintenance costs while extending system lifespan. Machine learning enables personalized comfort profiles that adapt to individual preferences and usage patterns, enhancing occupant satisfaction and productivity. The integration of external data sources including weather forecasts, utility pricing signals, and grid demand response programs enables buildings to participate in energy markets while optimizing operational costs. These intelligent capabilities position KNX-enabled buildings as active participants in smart city ecosystems and sustainable energy management strategies.

Recent Development

In January 2025: The KNX Association has introduced a comprehensive certification framework specifically designed for Internet of Things (IoT) devices, representing a significant milestone in the evolution of smart building and home automation technology. This certification scheme addresses critical market needs for secure, standardized, and interoperable IoT solutions that can seamlessly integrate with existing KNX infrastructure while maintaining the protocol's renowned reliability and security standards.

In July 2025: The JUNG HOME Gateway extends any KNX installation by linking the bus to IP networks, letting residents manage lighting, climate control, blinds and security devices through smartphones, tablets or voice assistants. Its bidirectional interface enables remote programming, energy-usage visualisation and over-the-air firmware updates while retaining KNX’s real-time reliability. Installers can integrate third-party IoT services via open APIs, making the gateway a flexible bridge that future-proofs both new builds and retrofit smart-home projects.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

Application (Lighting Control, HVAC Systems, Energy Management, Blinds & Shutters) End User (Commercial Buildings, Residential Buildings , Industrial) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Application (Lighting Control, HVAC Systems, Energy Management, Blinds & Shutters) End User (Commercial Buildings, Residential Buildings , Industrial) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Application (Lighting Control, HVAC Systems, Energy Management, Blinds & Shutters) End User (Commercial Buildings, Residential Buildings , Industrial) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Application (Lighting Control, HVAC Systems, Energy Management, Blinds & Shutters) End User (Commercial Buildings, Residential Buildings , Industrial) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")