- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Laboratory Automation System Market Size, Share | CAGR 9.0%

Global Lab Automation System Market Size, Share Analysis By Type (Total, Modular, Standalone, Robotic, Liquid Handling, ASRS, LIMS, Integrated), By Process (Prep, Handling, Liquid, Assay, Clinical/Molecular Diagnostics, Drug Discovery, Workflow), By Application (Diagnostics, Genomics, Microbiology, Biobanking, Forensics, F&B, Pharma QC), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 8.40 Billion | USD 18.30 Billion | 9.0% | North America, 40.1% |

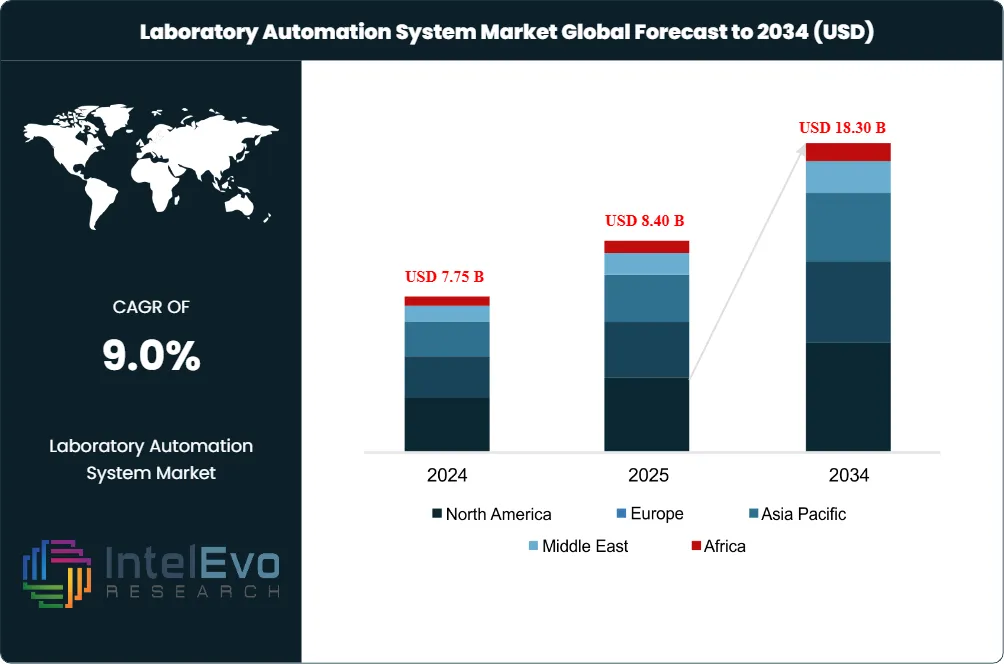

The Laboratory Automation System Market was valued at USD 7.75 Billion in 2024 and USD 8.40 Billion in 2025. The market is projected to reach USD 18.30 Billion by 2034, expanding at a CAGR of 9.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 9.90 Billion over the analysis period. The Laboratory Automation System Market expansion is driven by acute clinical labor shortages, rising diagnostic test volumes, and accelerating integration of robotics with artificial intelligence across pre-analytical, analytical, and post-analytical workflows.

Get More Information about this report -

Request Free Sample ReportDemand-side pressure is the primary growth engine. The CDC reports that approximately 14 billion clinical laboratory tests are ordered annually across more than 266,000 CLIA-certified facilities in the United States, intensifying need for end-to-end automation that compresses turnaround time. Peer-reviewed implementations document up to 86% fewer manual processing steps and turnaround time reductions of 87.3% for HIV testing and 19.3% for COVID-19 testing when total laboratory automation is paired with lean workflow methods. Pharmaceutical and biotechnology companies, which account for roughly 45% of end-user demand, continue to expand high-throughput screening capacity to support GLP-1, oncology, and cell-therapy pipelines.

The regulatory environment is reinforcing adoption. The Centers for Medicare and Medicaid Services finalized phased CLIA modernization rules in 2025 with full digital notification enforcement scheduled by March 1, 2026, raising documentation, traceability, and proficiency-testing standards. The FDA rescinded its laboratory-developed test final rule in September 2025 following a federal court ruling, but FDA QSR design-control expectations and 21 CFR Part 11 electronic records remain binding on automated platforms. EU GMP Annex 1, in force since August 2023, continues to favor robotic isolators and continuous-monitoring automation across European pharmaceutical manufacturing.

Technology dynamics are restructuring the Laboratory Automation System Market through three converging shifts. Vendors including Tecan Group, Hamilton Company, and Beckman Coulter Life Sciences are embedding AI-driven anomaly detection and predictive maintenance into liquid-handling platforms to lift first-pass yield. Modular work cells are gaining ground over fixed total-laboratory-automation lines because they let mid-sized laboratories phase capital expenditure across two-to-three-year cycles. Open-API architectures are displacing closed-vendor stacks, allowing buyers to integrate instruments from multiple vendors under unified scheduling software such as Automata Linq.

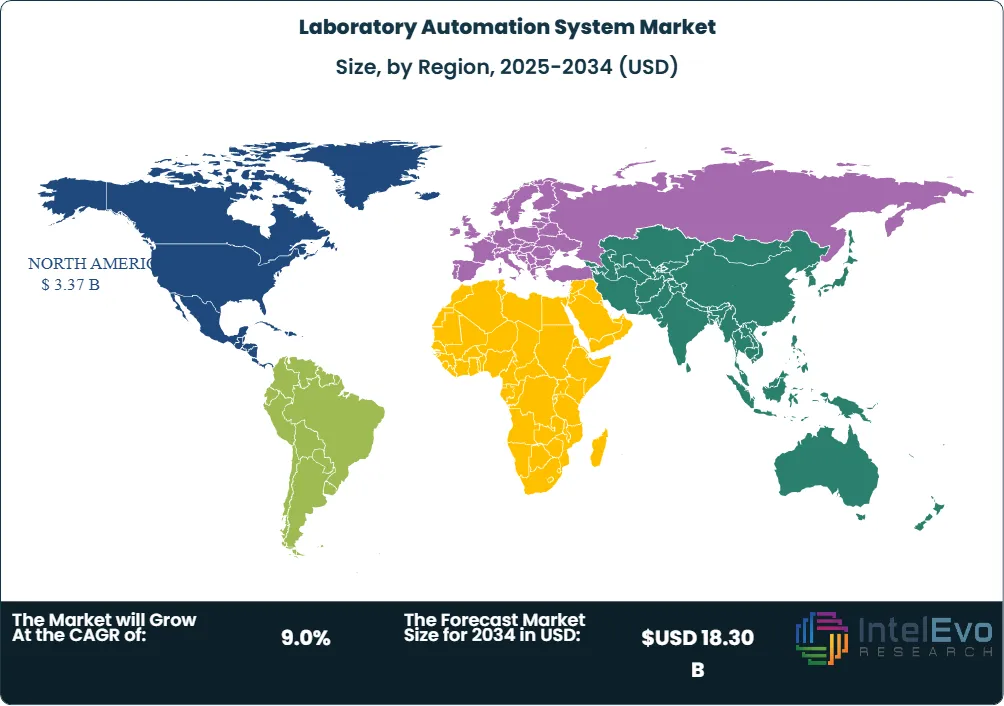

Regional demand is concentrated yet shifting. North America retained the largest share of the Laboratory Automation System Market at 40.1% in 2025, supported by a US installed base valued at approximately USD 3.0 Billion and federal R&D obligations exceeding USD 95 Billion at the National Institutes of Health and related agencies. Asia Pacific is the fastest-growing region, projected to expand at a CAGR of 10.9% through 2034 as China's Made in China 2025 industrial program and India's Production Linked Incentive scheme accelerate domestic biopharmaceutical capacity. By 2034, vendors that combine modular hardware with cloud-native orchestration software are expected to capture a disproportionate share of the USD 9.90 Billion absolute opportunity.

, By Process (Prep, Handling, Liquid, Assay, Clinical/Molecular Diagnostics, Drug Discovery, Workflow), By Application (Diagnostics, Genomics, Microbiology, Biobanking, Forensics, F&B, Pharma QC), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The Laboratory Automation System Market grew from USD 8.40 Billion in 2025 to a projected USD 18.30 Billion by 2034 at a CAGR of 9.0%, an absolute dollar opportunity of USD 9.90 Billion.

- Segment Dominance (Type): Total laboratory automation systems held 62.3% of revenue share in 2025, driven by adoption in high-volume hospital and reference laboratories deploying tracks from Beckman Coulter, Roche, and Inpeco.

- Segment Dominance (Application): Clinical chemistry analysis captured 34.7% of revenue share in 2025, reflecting the routine-test base of approximately 14 billion CLIA-certified tests performed annually in the United States.

- Driver: Clinical staffing shortages and rising sample volume drove 71% of major US clinical laboratories to deploy AI-enhanced automation platforms by April 2024, accelerating CAPEX commitments through 2025.

- Restraint: Total laboratory automation track installations exceed USD 250,000 per system, deferring adoption among small and mid-sized laboratories with annual revenue below USD 10 Million.

- Opportunity: Modular automation systems are projected to grow at an 11.1% CAGR through 2034, opening an addressable opportunity of approximately USD 4.20 Billion within the broader Laboratory Automation System Market.

- Trend: AI-driven workflow orchestration platforms such as Automata Linq, Tecan Introspect, and Beckman Coulter cloud services are displacing closed scheduling software, with vendor partnerships accelerating since the January 2026 Beckman Coulter and Automata agreement.

- Regional: North America led the Laboratory Automation System Market at 40.1% share or roughly USD 3.37 Billion in 2025, while Asia Pacific is projected to grow fastest at a 10.9% CAGR through 2034.

Market Definition & Scope

The Laboratory Automation System Market is defined as the global market for integrated hardware, software, and services that mechanize laboratory workflows from sample receipt through result reporting with minimal human intervention. The market encompasses automated liquid handlers, sample-handling and transport systems, robotic workstations, automated storage and retrieval, total laboratory automation tracks, modular work cells, laboratory information management systems, and middleware that connects instruments to enterprise systems.

This analysis includes total laboratory automation systems, modular automation systems, automation software, robotic plate handlers, microplate readers, and the recurring services and consumables tied to these platforms. The scope explicitly excludes standalone clinical analyzers without conveyor or scheduling integration, manual pipettors, traditional centrifuges sold without robotic loaders, and broader medical-device categories such as point-of-care diagnostics. The Laboratory Automation System Market sits within the parent in vitro diagnostics and life-science instrumentation markets, representing roughly 8% to 10% of that combined parent revenue base in 2025.

Key Insights Summary

- US clinical laboratories run approximately 14 billion lab tests annually across more than 266,000 CLIA-certified facilities, per CDC reporting, sustaining structural demand for total laboratory automation tracks across the Laboratory Automation System Market.

- Total laboratory automation deployments cut manual processing steps by up to 86% and reduce turnaround time by 87.3% on HIV testing and 19.3% on COVID-19 testing, per peer-reviewed clinical implementations.

- Siemens AG closed the USD 5.1 Billion acquisition of Dotmatics on July 1, 2025, expanding its industrial software total addressable market by USD 11 Billion and embedding the Luma scientific intelligence platform into its Siemens Xcelerator portfolio.

- Beckman Coulter Life Sciences and Automata announced a strategic partnership on January 29, 2026, aligned with Automata's USD 45 Million Series C round in which Danaher Ventures secured a board seat to accelerate AI-ready modular work-cell deployments.

- Roche Diagnostics launched the cobas 6800/8800 systems version 2.0 in the United States on December 16, 2025 following FDA 510(k) clearance, increasing throughput and enabling sample prioritization across high-volume molecular laboratories.

- Tecan Group reported 2024 sales of CHF 934 Million (approximately USD 1,062 Million) and launched the Veya multi-omics liquid-handling workstation at the Society for Laboratory Automation and Screening international conference in January 2025.

- Modular automation systems are projected to grow at a CAGR of 11.1% through 2034, outpacing the 9.0% market-wide growth and reflecting laboratory preference for phased capital deployment over single-line total automation.

Competitive Landscape Overview

The Laboratory Automation System Market is moderately consolidated. The top four vendors, Thermo Fisher Scientific, Danaher Corporation through Beckman Coulter, F. Hoffmann-La Roche, and Tecan Group, collectively held an estimated 48% to 52% of global revenue in 2025 based on aggregated company disclosures and published installed-base data. Competition is technology-led rather than price-led, anchored on three vectors: open-API interoperability, AI-driven workflow orchestration, and the depth of recurring consumables and service revenue tied to each automation platform. Entrants such as Automata, Hudson Robotics, and Opentrons are pressuring incumbents on the modular work-cell tier with cloud-native scheduling and lower entry-point pricing.

Competitive evolution accelerated in 2025 and early 2026. Siemens AG closed its USD 5.1 Billion acquisition of Dotmatics on July 1, 2025, embedding scientific intelligence software directly into industrial PLM workflows. Bruker advanced its Project Accelerate 3.0 strategy by integrating Chemspeed laboratory automation and ELITech molecular diagnostics into its measurement-instrument portfolio. Danaher Ventures led the USD 45 Million Series C round in Automata in January 2026, signaling a defensive move by Beckman Coulter to lock in modular AI-ready automation infrastructure before Thermo Fisher or Tecan could acquire the same capability.

Competitive Landscape Matrix

| Company Name | Headquarters | Market Position | Key Product / Solution | Geographic Strength | Recent Strategic Move (Trailing 18 Months) |

|---|---|---|---|---|---|

| Thermo Fisher Scientific | USA | Leader | Vulcan Automated Lab; Orbitrap Astral Zoom; lab consumables portfolio | Global, all regions | Q1 2025 launch of Vulcan Automated Lab integrating robotics, AI, electron microscopy |

| Danaher Corporation (Beckman Coulter) | USA | Leader | DxA 5000 Fit; Power Express; Biomek i3 Liquid Handler | Global, North America strength | December 2025 launch of Biomek i3 Benchtop Liquid Handler |

| F. Hoffmann-La Roche | Switzerland | Leader | cobas 6800/8800 v2.0; cobas i 601; cobas Connection Modules | Global clinical labs | December 2025 US launch of cobas 6800/8800 v2.0 after FDA 510(k) clearance |

| Tecan Group | Switzerland | Leader | Veya multi-omics workstation; Fluent Automation Workstation; Resolvex i300 | Europe, North America, APAC | January 2025 SLAS launch of Veya multi-omics liquid handling workstation |

| Hamilton Company | USA | Challenger | Microlab STAR; Microlab VANTAGE; VENUS software | North America, Europe | Q3 2025 expansion of STAR Line for NGS workflows |

| Agilent Technologies | USA | Challenger | BioTek workstations; Bravo Liquid Handler; OpenLab software | Global pharma and chemical | Partnership with ABB Robotics for SLAS 2026 cell workflow demo |

| Becton, Dickinson and Company | USA | Challenger | BD Kiestra Total Lab Automation; BD Cor | North America, Europe microbiology | FY2025 expansion of Kiestra global installed base |

| Eppendorf AG | Germany | Challenger | epMotion; VisioNize box 2 connectivity hub | Europe, North America research | September 2025 launch of VisioNize box 2 digital hub |

| Siemens Healthineers / Siemens AG | Germany | Challenger | Atellica Process Manager; Dotmatics Luma platform | Europe, North America | July 2025 Siemens close of USD 5.1 billion Dotmatics acquisition |

| Bruker Corporation | USA | Niche Player | Chemspeed automated synthesis platforms; lab automation software | Global research | Project Accelerate 3.0 expansion into AI-ready laboratory automation |

Segmentation Analysis

The Laboratory Automation System Market is segmented across four primary dimensions that buyers use during procurement: by automation type, by process flow, by application, and by end-user. Each dimension captures distinct adoption economics and informs vendor positioning, vendor selection, and ROI calculation for procurement leads building multi-year automation roadmaps.

By Automation Type

Total laboratory automation systems dominated the segment in 2025 with 62.3% of revenue share, equivalent to roughly USD 5.23 Billion. These integrated tracks connect pre-analytical sorting, centrifugation, analytical testing, and post-analytical archiving in a continuous-flow architecture suited to hospital networks running more than two million tests annually. Beckman Coulter's DxA 5000 line, Roche cobas Connection Modules, and Inpeco FlexLab platforms anchor this segment in North America and Europe.

Modular automation systems held the remaining 37.7% of revenue share in 2025 at approximately USD 3.17 Billion, but the segment is forecast to grow at an 11.1% CAGR through 2034 against the 9.0% market-wide rate. Adoption is concentrated in mid-sized clinical laboratories, contract research organizations, and academic genomics core facilities that need configurable work cells from Tecan, Hamilton Company, and Eppendorf. Procurement leads frequently choose modular work cells over total automation lines when capital authorization is capped below USD 1.5 Million per project, because phased deployment delivers faster payback at lower upfront risk.

By Process

Continuous-flow processing accounted for 57.8% of revenue share in 2025, reflecting the architectural preference of high-volume clinical chemistry and immunoassay laboratories for uninterrupted analyzer feeding. Continuous-flow tracks feed Roche cobas, Abbott Alinity, and Siemens Healthineers Atellica analyzers and reduce per-sample reagent waste compared to batch handling. Discrete processing held 42.2% of revenue share and is projected to expand at a CAGR of 10.9% through 2034 as flexible test menus drive demand in molecular diagnostics, mass spectrometry, and NGS workflows where assay heterogeneity penalizes continuous-flow design.

By Application

Clinical chemistry analysis was the largest application segment at 34.7% of revenue share in 2025, driven by routine metabolic, lipid, liver-function, and electrolyte testing performed at scale in hospital and reference laboratories. The segment is projected to grow at a CAGR of 10.8% through 2034 as chronic-disease prevalence and personalized-medicine protocols expand routine-panel volumes. Beckman Coulter, Roche Diagnostics, and Siemens Healthineers anchor this application with high-throughput automated chemistry analyzers integrated into total laboratory automation tracks.

Immunoassay analysis accounted for an estimated 22.0% of revenue share in 2025 and is expanding rapidly on cardiac, infectious-disease, and oncology biomarker testing growth. Other application segments include hematology at 14.5%, molecular diagnostics at 13.5%, and the residual 15.3% allocated across microbiology, drug discovery, genomics, and proteomics. Pharmaceutical R&D applications are accelerating fastest within the modular tier, particularly for high-throughput screening, where Tecan Fluent and Hamilton Microlab STAR platforms dominate procurement decisions.

By End-User

Pharmaceutical and biotechnology companies represented approximately 45.0% of end-user demand in 2025, equivalent to roughly USD 3.78 Billion, driven by sustained R&D spending exceeding USD 290 Billion across the global biopharmaceutical industry. Hospitals and clinical diagnostic laboratories accounted for 30.5% at approximately USD 2.56 Billion, supported by total laboratory automation deployments at networks such as Mayo Clinic, Cleveland Clinic, and Apollo Hospitals. Academic research institutes contributed 14.5%, while environmental, forensic, food and beverage, and contract research organizations together accounted for 10.0% of demand. Procurement checklists across all end-users converge on five evaluation criteria: throughput per square meter, total cost of ownership over seven years, software interoperability, regulatory documentation depth, and vendor service-network density.

Regional Analysis

The Laboratory Automation System Market spans five regions with distinct demand drivers, regulatory anchors, and procurement priorities. Regional revenue shares in 2025 were North America at 40.1%, Europe at 25.4%, Asia Pacific at 24.8%, Latin America at 5.2%, and Middle East and Africa at 4.5%.

North America

North America led the Laboratory Automation System Market at 40.1% share or approximately USD 3.37 Billion in 2025, anchored by the United States, Canada, and Mexico. The US installed base alone is estimated at USD 3.00 Billion and is supported by NIH research obligations exceeding USD 47 Billion in fiscal year 2025 plus state-level investments in clinical-laboratory modernization. The 2025 CLIA modernization rules and FDA 21 CFR Part 11 electronic-records compliance favor automated documentation platforms. Beckman Coulter, Thermo Fisher, and Hamilton Company maintain dominant share, and Roche launched cobas 6800/8800 v2.0 across US laboratories in December 2025 following 510(k) clearance.

Europe

Europe held 25.4% of the Laboratory Automation System Market in 2025, equivalent to approximately USD 2.13 Billion, with Germany, the United Kingdom, France, Switzerland, and Italy as the largest country markets. The EU Horizon Europe research program, which allocates more than EUR 95.5 Billion through 2027, funds laboratory digitalization across academic and clinical research networks. EU GMP Annex 1 has tightened contamination-control requirements since 2023, accelerating procurement of robotic isolators and automated environmental monitoring. Tecan Group, Eppendorf AG, and Siemens Healthineers anchor regional supply, and Siemens completed its USD 5.1 Billion Dotmatics acquisition in July 2025, reinforcing European software leadership.

Asia Pacific

Asia Pacific captured 24.8% of revenue in 2025 at approximately USD 2.08 Billion and is projected to expand at the fastest regional CAGR of 10.9% through 2034. China, Japan, South Korea, and India lead demand, supported by China's Made in China 2025 program, Japan's Society 5.0 framework, and India's Production Linked Incentive scheme for pharmaceuticals. In May 2025, Asian Hospital in Faridabad, India, deployed total laboratory automation in collaboration with QuidelOrtho. Domestic vendors such as Autobio Diagnostics and Sysmex Corporation are gaining share in clinical chemistry and hematology workflows.

Latin America

Latin America accounted for 5.2% of the Laboratory Automation System Market in 2025, approximately USD 0.44 Billion, with Brazil, Mexico, and Argentina as the largest country markets. Brazil's Sistema Unico de Saude reform programs are prioritizing centralized clinical-laboratory automation in tertiary hospitals, while Mexico's Cofepris regulatory alignment with FDA standards is accelerating IVD automation procurement. Roche, Beckman Coulter, and Siemens Healthineers dominate regional supply through distributor networks. Foreign-exchange volatility and import-tariff exposure remain the primary procurement frictions.

Middle East and Africa

Middle East and Africa held 4.5% of the Laboratory Automation System Market in 2025, equivalent to approximately USD 0.38 Billion. Saudi Arabia, the United Arab Emirates, South Africa, and Egypt lead demand, supported by Saudi Vision 2030 healthcare investments and UAE Centennial 2071 digital-health programs. The Saudi Food and Drug Authority and UAE Department of Health have aligned IVD-quality standards with FDA and CE-marking frameworks, simplifying multinational vendor entry. In Q1 2026, regional installations grew across King Faisal Specialist Hospital and Cleveland Clinic Abu Dhabi as both networks expanded total laboratory automation tracks.

Country Analysis

Country-level dynamics within the Laboratory Automation System Market diverge sharply on regulation, reimbursement, and domestic vendor presence. The four most relevant national markets in 2025 are the United States, China, Germany, and Japan, which together account for an estimated 62% of global revenue.

United States

The United States Laboratory Automation System Market was valued at approximately USD 3.00 Billion in 2025 and is projected to grow at a country-specific CAGR of 9.5% through 2034. Federal demand drivers include NIH research obligations exceeding USD 47 Billion in fiscal year 2025 and Medicare clinical-laboratory fee-schedule reforms that pressure laboratories to extract operating efficiency. The 2025 CLIA modernization rules require digital notification systems with full enforcement by March 1, 2026, raising automation procurement priority. State-level initiatives in California, Massachusetts, and North Carolina are funding regional life-sciences automation hubs. Domestic vendors Beckman Coulter, Thermo Fisher, and Hamilton Company together hold an estimated 55% to 60% of US revenue.

China

China's Laboratory Automation System Market reached an estimated USD 1.05 Billion in 2025 and is forecast to grow at a country-specific CAGR of 12.4% through 2034, the fastest among major economies. The Made in China 2025 industrial program and the 14th Five-Year Plan for Bioeconomy prioritize domestic biopharmaceutical capacity and clinical-laboratory modernization. In October 2024, SPT Labtech and ICE Bioscience launched a joint automated drug-screening laboratory in Beijing. Domestic vendors Autobio Diagnostics and Mindray Medical hold growing share in clinical chemistry, while imported equipment from Roche, Beckman Coulter, and Tecan still dominates molecular diagnostics.

Germany

Germany's Laboratory Automation System Market was valued at approximately USD 0.62 Billion in 2025 and is projected to grow at a country-specific CAGR of 7.8% through 2034. The Bundesinstitut fur Arzneimittel und Medizinprodukte aligns automation validation with EU GMP Annex 1 and the EU IVDR transition timeline. German pharmaceutical clusters in Frankfurt, Munich, and Heidelberg drive demand for high-throughput screening systems. Sartorius AG, Eppendorf AG, and Siemens Healthineers are domestic anchors, with Siemens reinforcing software leadership through the July 2025 Dotmatics acquisition close.

Japan

Japan's Laboratory Automation System Market reached approximately USD 0.59 Billion in 2025 and is forecast to grow at a country-specific CAGR of 7.0% through 2034. The Pharmaceuticals and Medical Devices Agency and the Society 5.0 framework are driving clinical-laboratory digitalization. Domestic vendors Sysmex Corporation, Hitachi High-Tech, and Yaskawa Electric anchor the supply base, with Yaskawa launching a precision-handling laboratory robot in March 2026. Hospital-network consolidation under the National Hospital Organization is accelerating total laboratory automation track procurement at flagship sites.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Automation Type

- Total Laboratory Automation (TLA)

- Modular Laboratory Automation

- Standalone Laboratory Automation Systems

- Robotic Laboratory Automation

- Automated Liquid Handling Systems

- Automated Storage and Retrieval Systems (ASRS)

- Laboratory Information Management Systems (LIMS)

- Integrated Laboratory Automation Platforms

- Others

By Process

- Sample Preparation

- Sample Handling and Transport

- Liquid Handling

- Assay Processing

- Clinical Diagnostics

- Molecular Diagnostics

- Drug Discovery and Screening

- Data Management and Analysis

- Quality Control and Assurance

- Laboratory Workflow Management

- Others

By Application

- Clinical Diagnostics

- Drug Discovery and Development

- Genomics and Proteomics Research

- Microbiology Testing

- Biobanking

- Forensic Testing

- Food and Beverage Testing

- Environmental Testing

- Pharmaceutical Quality Control

- Academic and Life Science Research

- Others

By End-User

- Hospitals and Diagnostic Laboratories

- Pharmaceutical and Biotechnology Companies

- Academic and Research Institutes

- Contract Research Organizations (CROs)

- Clinical Research Organizations

- Food and Beverage Testing Laboratories

- Environmental Testing Laboratories

- Forensic Laboratories

- Government and Public Health Laboratories

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.40 B |

| Forecast Revenue (2034) | USD 18.30 B |

| CAGR (2025-2034) | 9.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Automation Type, (Total Laboratory Automation (TLA), Modular Laboratory Automation, Standalone Laboratory Automation Systems, Robotic Laboratory Automation, Automated Liquid Handling Systems, Automated Storage and Retrieval Systems (ASRS), Laboratory Information Management Systems (LIMS), Integrated Laboratory Automation Platforms, Others), By Process, (Sample Preparation, Sample Handling and Transport, Liquid Handling, Assay Processing, Clinical Diagnostics, Molecular Diagnostics, Drug Discovery and Screening, Data Management and Analysis, Quality Control and Assurance, Laboratory Workflow Management, Others), By Application, (Clinical Diagnostics, Drug Discovery and Development, Genomics and Proteomics Research, Microbiology Testing, Biobanking, Forensic Testing, Food and Beverage Testing, Environmental Testing, Pharmaceutical Quality Control, Academic and Life Science Research, Others), By End-User, (Hospitals and Diagnostic Laboratories, Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, Contract Research Organizations (CROs), Clinical Research Organizations, Food and Beverage Testing Laboratories, Environmental Testing Laboratories, Forensic Laboratories, Government and Public Health Laboratories, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THERMO FISHER SCIENTIFIC, DANAHER CORPORATION (BECKMAN COULTER), F. HOFFMANN-LA ROCHE, TECAN GROUP, HAMILTON COMPANY, AGILENT TECHNOLOGIES, BECTON, DICKINSON AND COMPANY, EPPENDORF AG, SIEMENS HEALTHINEERS, BRUKER CORPORATION, BIO-RAD LABORATORIES, SARTORIUS AG, QIAGEN N.V., REVVITY INC., ABBOTT LABORATORIES, HUDSON ROBOTICS, AUTOMATA LABS, ABB LTD., OPENTRONS LABWORKS, Others. |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Process (Prep, Handling, Liquid, Assay, Clinical/Molecular Diagnostics, Drug Discovery, Workflow), By Application (Diagnostics, Genomics, Microbiology, Biobanking, Forensics, F&B, Pharma QC), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Process (Prep, Handling, Liquid, Assay, Clinical/Molecular Diagnostics, Drug Discovery, Workflow), By Application (Diagnostics, Genomics, Microbiology, Biobanking, Forensics, F&B, Pharma QC), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

, By Process (Prep, Handling, Liquid, Assay, Clinical/Molecular Diagnostics, Drug Discovery, Workflow), By Application (Diagnostics, Genomics, Microbiology, Biobanking, Forensics, F&B, Pharma QC), By End-User (Hospitals, Labs, Pharma, Biotech, Academic, CROs) Region & Key Players-Dynamics, Strategies, Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Laboratory Automation System Market?

The Global Laboratory Automation System Market was valued at USD 7.75 Billion in 2024 and USD 8.40 Billion in 2025, and is projected to reach USD 18.30 Billion by 2034, growing at a CAGR of 9.0% from 2026 to 2034. Market growth is driven by laboratory automation, robotics, AI-powered workflows, and increasing demand for high-throughput diagnostics and research.

Who are the major players in the Laboratory Automation System Market?

THERMO FISHER SCIENTIFIC, DANAHER CORPORATION (BECKMAN COULTER), F. HOFFMANN-LA ROCHE, TECAN GROUP, HAMILTON COMPANY, AGILENT TECHNOLOGIES, BECTON, DICKINSON AND COMPANY, EPPENDORF AG, SIEMENS HEALTHINEERS, BRUKER CORPORATION, BIO-RAD LABORATORIES, SARTORIUS AG, QIAGEN N.V., REVVITY INC., ABBOTT LABORATORIES, HUDSON ROBOTICS, AUTOMATA LABS, ABB LTD., OPENTRONS LABWORKS, Others.

Which segments covered the Laboratory Automation System Market?

By Automation Type, (Total Laboratory Automation (TLA), Modular Laboratory Automation, Standalone Laboratory Automation Systems, Robotic Laboratory Automation, Automated Liquid Handling Systems, Automated Storage and Retrieval Systems (ASRS), Laboratory Information Management Systems (LIMS), Integrated Laboratory Automation Platforms, Others), By Process, (Sample Preparation, Sample Handling and Transport, Liquid Handling, Assay Processing, Clinical Diagnostics, Molecular Diagnostics, Drug Discovery and Screening, Data Management and Analysis, Quality Control and Assurance, Laboratory Workflow Management, Others), By Application, (Clinical Diagnostics, Drug Discovery and Development, Genomics and Proteomics Research, Microbiology Testing, Biobanking, Forensic Testing, Food and Beverage Testing, Environmental Testing, Pharmaceutical Quality Control, Academic and Life Science Research, Others), By End-User, (Hospitals and Diagnostic Laboratories, Pharmaceutical and Biotechnology Companies, Academic and Research Institutes, Contract Research Organizations (CROs), Clinical Research Organizations, Food and Beverage Testing Laboratories, Environmental Testing Laboratories, Forensic Laboratories, Government and Public Health Laboratories, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Laboratory Automation System Market

Published Date : 29 Jun 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date