- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Language Translation Device Market Size & Forecast 2024–2034 | 10.6% CAGR

Global Language Translation Device Market Size, Share, Analysis By Product (Handheld Translation Devices, Wearable Translation Devices), By Type (Online Translation, Offline Translation), By Application (Consumer Use, Commercial & Enterprise Use), By Distribution Channel (Online Platforms, Retail Stores), Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Technology Innovation, Competitive Strategies, Trends & Forecast 2025–2034

Report Overview

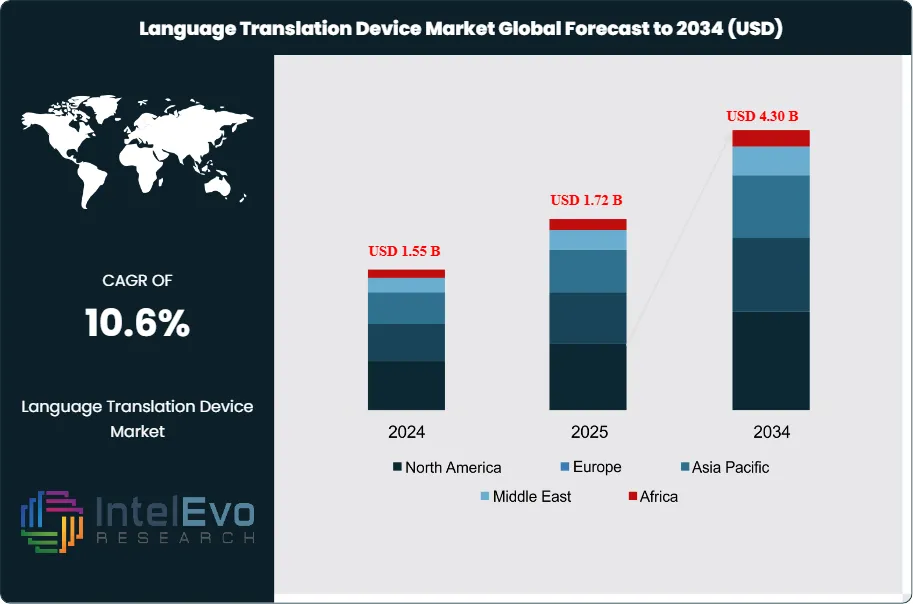

The Language Translation Device Market was valued at USD 1.55 Billion in 2024 and is projected to reach approximately USD 4.30 Billion by 2034. The market is estimated to grow to around USD 1.72 Billion in 2025. Based on projected expansion from 2026 onward, the industry is expected to register a compound annual growth rate (CAGR) of approximately 10.6% during 2026–2034.

Get More Information about this report -

Request Free Sample ReportLanguage translation devices enable near real-time conversion of speech or text across languages via handheld units, wearables, and software applications that run on smartphones and other connected endpoints. Demand is rising as cross-border commerce expands and multilingual interactions become routine in sales, service, and field operations. Enterprises use these tools to reduce handling time in contact centers, support frontline staff, and improve consistency in customer communications across markets. Travel and hospitality also support consumer adoption, while education and training providers deploy translation to support diverse student populations and cross-language collaboration.

On the supply side, performance gains come from AI, machine learning, and natural language processing that improve intent capture, context handling, and translation latency. Vendors compete on quality in noisy environments, offline operation, battery efficiency, and privacy-by-design controls. Hybrid architectures are becoming standard, with more processing retained on-device to limit data exposure and enable offline use, while cloud services deliver model updates and broader language coverage. In February 2024, Microsoft advanced AI-driven translation with an emphasis on embedding real-time capabilities into Microsoft Teams and related productivity tools, reinforcing a shift toward integrated translation inside daily workflows.

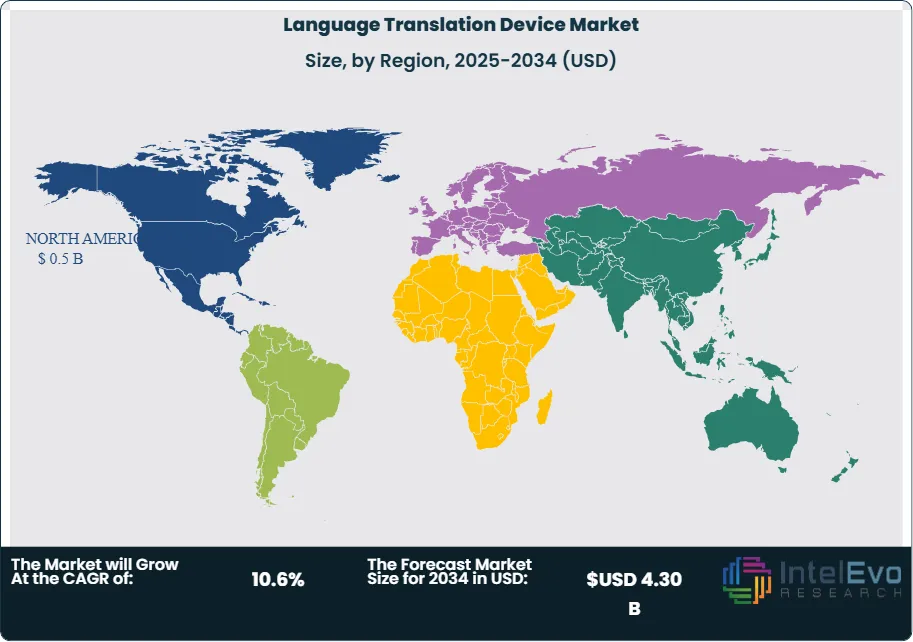

Regionally, North America remains the largest revenue pool, supported by higher enterprise spend and early deployment at scale. The region accounted for over 35.3% of global revenue in 2023, or about USD 0.5 billion, and is estimated near USD 0.55 billion in 2024. Europe is assessed at roughly 25% share in 2024, shaped by GDPR compliance and tightening AI governance that raises requirements for auditability and data retention controls. Asia Pacific is positioned for the fastest growth, supported by cross-border e-commerce and mobile-first adoption; India and Southeast Asia are emerging investment hotspots, alongside the Gulf states where tourism and multilingual services drive demand.

Key risks include uneven accuracy across dialects, liability exposure from mistranslations in regulated settings, and cybersecurity threats tied to voice data and device connectivity. Privacy rules, biometric-data constraints, and cross-border transfer requirements can increase compliance cost and extend procurement cycles, especially in public-sector programs. Even so, improving model quality, expanding language coverage, and an estimated 3–5% annual decline in average device pricing should sustain adoption through 2034.

, By Type (Online Translation, Offline Translation), By Application (Consumer Use, Commercial & Enterprise Use), By Distribution Channel (Online Platforms, Retail Stores), Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Technology Innovation, Competitive Strategies, Trends & Forecast 2025–2034")

Key Takeaways

• Market Growth: The market expands from 1.4 billion USD, 2024 to 3.9 billion USD, 2034 at 10.8%, 2024-2034. Revenue growth sustains scale-up across enterprise and consumer use cases at 10.8%, 2024-2034.

• Segment Dominance : Handheld devices lead demand with 75.4%, 2024. The format retains dominance due to portability and immediate use in field scenarios at 75.4%, 2024.

• Segment Dominance: Online translation captures 72.5%, 2024, reflecting preference for connected, continuously updated language models. Online platforms also lead distribution with 68.8%, 2024.

• Driver: Commercial deployments drive adoption with 63.1%, 2024 as firms prioritize faster multilingual interactions and service consistency. Enterprise budgets support rollout across customer-facing operations at 63.1%, 2024.

• Restraint: Data privacy and compliance risk constrains adoption in regulated environments at estimated: 0.2 billion USD, 2024. Accuracy variance across dialects and noisy settings raises operational risk at estimated: 3.0%, 2024.

• Opportunity: Expanding underserved languages and dialect coverage creates whitespace at estimated: 1.1 billion USD, 2034. Integrating devices into wearables and mobile ecosystems broadens addressable demand at estimated: 28.0%, 2034.

• Trend: AI-led model upgrades improve speed and contextual accuracy, lifting premium feature attach rates at estimated: 35.0%, 2024. Vendors shift more inference on-device to reduce latency and exposure at estimated: 45.0%, 2024.

• Regional Analysis: North America leads with 35.3%, 2024 and generates 0.5 billion USD, 2024. Regional scale accelerates enterprise penetration at 35.3%, 2024.

By Type

Handheld language translation devices continue to account for the largest share of global demand as the market moves through 2025 and beyond. In 2023, handheld models represented more than 75.4 percent of total shipments, and this share remains structurally high due to their functional depth and reliability. These devices offer larger displays, tactile controls, and expanded configuration options, which support complex multilingual exchanges in business, education, and institutional settings.

Compared with wearable formats, handheld devices support stronger processors and extended battery life, enabling faster response times and higher accuracy during continuous use. This capability is critical for professional environments such as conferences, training sessions, and field operations, where uninterrupted translation is required. Most leading handheld devices now support more than 100 languages, with offline packs covering 40 to 60 languages, which further strengthens adoption across global markets.

Wearable and other form factors are expanding, but they remain complementary rather than substitutive. Adoption remains concentrated in consumer and travel use cases, while enterprise buyers continue to prioritize handheld solutions for reliability, security controls, and translation depth.

By Application

Online translation remains the dominant operating mode within language translation devices. In 2023, online-enabled solutions accounted for over 72.5 percent of market revenue, supported by widespread broadband access and mobile connectivity. This share is expected to remain above 70 percent through 2030 as real-time cloud processing delivers higher contextual accuracy and faster updates.

Online translation enables direct integration with emails, messaging platforms, browsers, and enterprise collaboration tools. This functionality has become essential for globally distributed teams and service operations. Continuous model updates also allow vendors to improve accuracy without hardware replacement, reducing total cost of ownership for organizations.

Offline translation continues to serve regulated and remote environments where connectivity is limited or restricted. Growth remains steady rather than rapid, with adoption concentrated in defense, emergency services, and travel to low-connectivity regions.

By End-Use

Commercial use cases represent the largest end-use category in the market. In 2023, commercial deployments accounted for more than 63.1 percent of total demand. Multinational enterprises rely on translation devices to support cross-border sales, customer service, and operational coordination. Hospitality, aviation, and tourism have also emerged as major adopters as international travel volumes normalize.

Translation accuracy for industry-specific terminology has improved materially since 2022, driven by advances in domain-trained language models. This progress has increased adoption in healthcare, legal services, and technical maintenance, where precision directly affects outcomes and compliance.

Residential use continues to grow at a slower pace, largely driven by travel and personal learning. Industrial use remains niche but stable, focused on safety briefings, equipment manuals, and multinational workforce coordination.

By Region

North America remains the largest regional market. In 2023, the region accounted for over 35.3 percent of global revenue, equivalent to approximately USD 0.5 billion. Demand is concentrated in healthcare, legal services, public safety, and enterprise collaboration, supported by high technology spending and diverse language requirements.

Europe follows with strong adoption across government services, cross-border trade, and education. Regulatory focus on data privacy has increased demand for secure, device-based translation solutions. Asia Pacific is the fastest-growing region, supported by outbound travel, cross-border e-commerce, and rising enterprise digitization in China, India, Japan, and Southeast Asia.

Latin America and the Middle East and Africa represent emerging growth pockets. Increasing tourism, infrastructure projects, and international partnerships are driving steady adoption, particularly in commercial and public service applications.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product

- Handheld

- Wearable

By Type

- Online Translation

- Offline Translation

By Application

- Consumer

- Commercial

By Distribution Channel

- Online Platforms

- Retail Stores

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.72 B |

| Forecast Revenue (2034) | USD 4.30 B |

| CAGR (2025-2034) | 10.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product (Handheld, Wearable), By Type (Online Translation, Offline Translation), By Application (Consumer, Commercial, By Distribution Channel, Online Platforms, Retail Stores) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Timekettle, Vasco Electronics, Google LLC, Pocketalk, iFLYTEK Co., Ltd., Waverly Labs, ECTACO, Inc., Langogo, Cheetah Mobile Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Type (Online Translation, Offline Translation), By Application (Consumer Use, Commercial & Enterprise Use), By Distribution Channel (Online Platforms, Retail Stores), Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Technology Innovation, Competitive Strategies, Trends & Forecast 2025–2034")

, By Type (Online Translation, Offline Translation), By Application (Consumer Use, Commercial & Enterprise Use), By Distribution Channel (Online Platforms, Retail Stores), Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Technology Innovation, Competitive Strategies, Trends & Forecast 2025–2034")

, By Type (Online Translation, Offline Translation), By Application (Consumer Use, Commercial & Enterprise Use), By Distribution Channel (Online Platforms, Retail Stores), Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Technology Innovation, Competitive Strategies, Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Language Translation Device Market?

Global Language Translation Device Market valued at USD 1.55B in 2024, projected to reach USD 4.30B by 2034, growing at 10.6% CAGR from 2026–2034 with rising travel demand.

Who are the major players in the Language Translation Device Market?

Timekettle, Vasco Electronics, Google LLC, Pocketalk, iFLYTEK Co., Ltd., Waverly Labs, ECTACO, Inc., Langogo, Cheetah Mobile Inc., Other Key Players

Which segments covered the Language Translation Device Market?

By Product (Handheld, Wearable), By Type (Online Translation, Offline Translation), By Application (Consumer, Commercial, By Distribution Channel, Online Platforms, Retail Stores)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Language Translation Device Market

Published Date : 04 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date