- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Large Vision Model Market Size, Share & Forecast | CAGR 20.4%

Global Large Vision Model Market Size, Share, Growth Analysis By Offering (Platform & API Access, Professional Services, On-Premise/Private Cloud Deployment Licenses), By Application (Medical Imaging, Autonomous Robotics, Visual Search, Content Creation, Security & Surveillance, Manufacturing Inspection), By Deployment Mode (Cloud, Hybrid, On-Premise), By End-User Vertical, AI Vision Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

| USD 7.84 Billion | USD 41.56 Billion | 20.4% | North America, 38.5% |

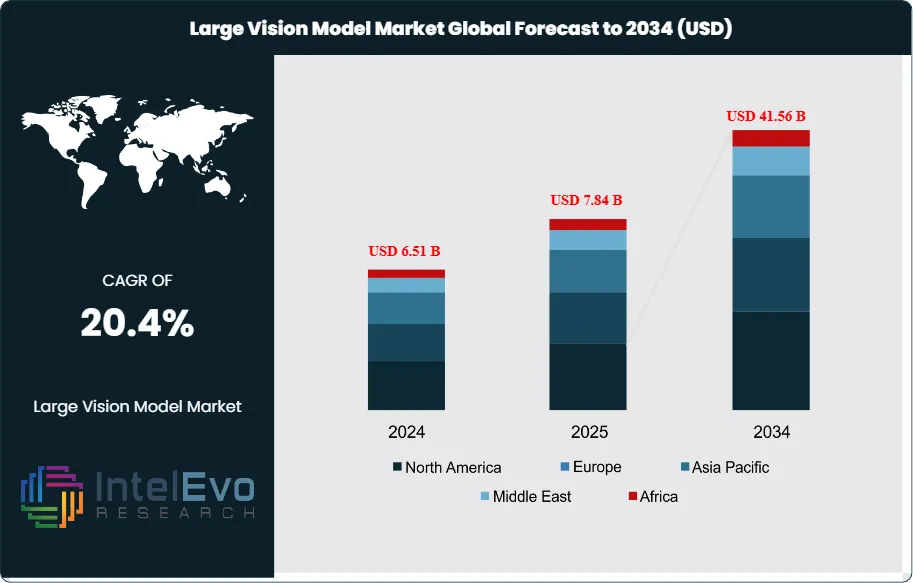

The Large Vision Model Market was valued at approximately USD 6.51 Billion in 2024 and reached USD 7.84 Billion in 2025. The market is projected to grow to USD 41.56 Billion by 2034, expanding at a CAGR of 20.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 33.72 Billion over the analysis period, reflecting the rapid institutional adoption of multimodal AI systems capable of processing and reasoning across images, video, and other visual data modalities at scale.

Get More Information about this report -

Request Free Sample ReportLarge vision models, encompassing multimodal foundation models, vision transformers, and contrastive language-image pre-training architectures, have transitioned from research curiosity to production infrastructure within a compressed five-year window. Enterprise deployment rates for AI-powered visual understanding systems reached approximately 34% among Fortune 500 companies in 2025, up from under 8% in 2022, as inference hardware costs fell by more than 60% following the commoditization of GPU and tensor processing unit capacity. The large vision model market benefits directly from this cost deflation, which has unlocked deployment in verticals previously constrained by compute budgets including retail, logistics, and precision agriculture.

Regulatory signals from the EU AI Act, which entered enforcement phases in 2025, are actively shaping the large vision model market by mandating transparency, bias auditing, and human-oversight requirements for high-risk AI applications. Compliance spending associated with these requirements is estimated to contribute USD 1.2 Billion in additional services revenue to the market by 2028. The NIST AI Risk Management Framework has further accelerated enterprise procurement governance standards in North America, catalyzing demand for auditable, well-documented model offerings from established vendors over unverified open-weight alternatives.

Technology convergence is a defining characteristic of the current large vision model market environment. The integration of vision encoders with large language model reasoning cores, exemplified by the GPT-4o and Gemini 1.5 architectures, has redefined what constitutes a deployable product in this space. Medical imaging remains the single highest-value application segment, with AI-assisted diagnostics generating USD 1.41 Billion in 2025 value within the broader market. Autonomous systems including robotics and industrial inspection represent the fastest-growing application category, projected to expand at a CAGR exceeding 24.1% through 2034 as edge inference capabilities mature.

Asia Pacific, particularly China and Japan, is emerging as a significant production and deployment hub for large vision model infrastructure, supported by sovereign AI investment programs exceeding USD 15 Billion cumulatively announced through 2025. North America retains leadership at 38.5% market share in 2025 by virtue of hyperscaler concentration and enterprise software integration depth. The large vision model market trajectory through 2034 will be shaped by continued architectural innovation, compute democratization, and the maturation of vertical-specific fine-tuned model variants across healthcare, manufacturing, defense, and retail.

, By Application (Medical Imaging, Autonomous Robotics, Visual Search, Content Creation, Security & Surveillance, Manufacturing Inspection), By Deployment Mode (Cloud, Hybrid, On-Premise), By End-User Vertical, AI Vision Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global large vision model market was valued at USD 7.84 Billion in 2025 and is projected to reach USD 41.56 Billion by 2034, expanding at a CAGR of 20.4% during the 2026–2034 forecast period.

- Segment Dominance: By offering, the platform and API access segment leads with approximately 52.3% market share in 2025, driven by hyperscaler distribution and the preference for managed inference endpoints over self-hosted deployments.

- Segment Dominance: By application, medical imaging and diagnostics represents the largest end-use vertical with 18.0% market share in 2025, accounting for USD 1.41 Billion in annual demand, underpinned by FDA clearances for AI-assisted radiology tools.

- Driver: Exponential growth in visual data generation, estimated at 328 Exabytes per day globally in 2025, is compelling enterprises to deploy automated visual understanding at scale, directly driving large vision model market expansion.

- Restraint: High pre-training compute costs, averaging USD 4 Million to USD 100 Million per frontier model run in 2025, restrict new entrant viability and concentrate market power among hyperscalers and well-capitalized labs.

- Opportunity: The autonomous robotics and industrial inspection segment presents an addressable opportunity of USD 6.8 Billion within the large vision model market by 2034, as sub-100ms edge inference and compact vision-language model architectures achieve production readiness.

- Trend: Multimodal unification, wherein a single model processes text, image, video, and audio within one architecture, has reached 41% adoption among enterprise AI procurement decisions in 2025 and will define competitive positioning through 2034.

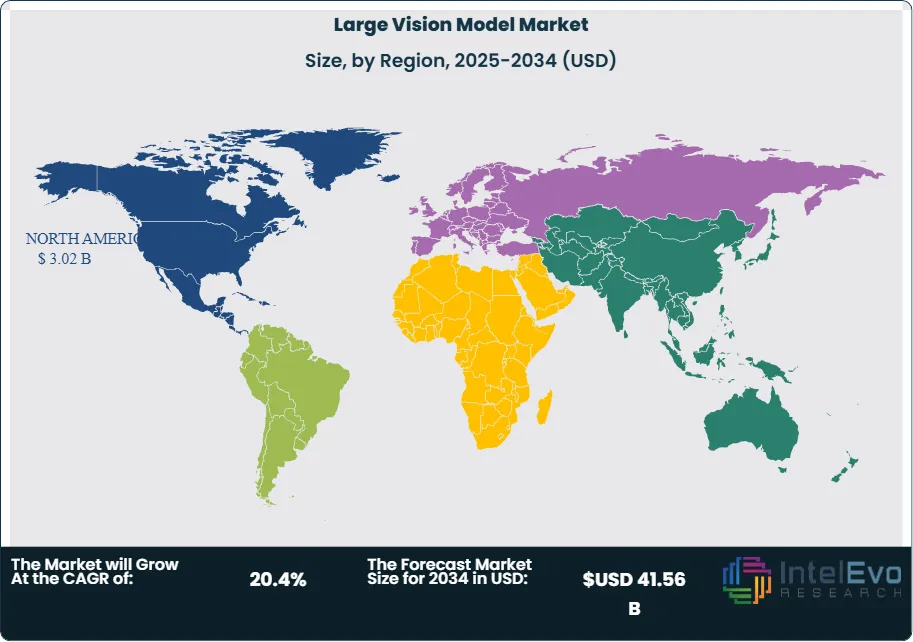

- Regional Analysis: North America leads the large vision model market with 38.5% share in 2025, equivalent to USD 3.02 Billion in annual revenue, driven by hyperscaler infrastructure depth, enterprise software integration, and regulatory framework maturity.

Competitive Landscape Overview

The large vision model market is moderately consolidated at the foundation model layer, where the top four providers, Microsoft (via Azure OpenAI), Google DeepMind, Amazon Web Services, and Meta AI, collectively hold approximately 58% combined market share in 2025. Competition is primarily technology-driven, with architectural performance on multimodal benchmarks such as MMBench and MMMU serving as key procurement decision factors. The competitive intensity has increased materially since 2024 following the open-weight release strategies of Meta and Mistral, which have pressured proprietary API pricing downward by an estimated 35% year-over-year. Vertical-specialist challengers including Stability AI, Cohere, and domain-specific entrants in medical imaging are intensifying competition at the application layer.

Competitive Landscape Matrix

| Company | HQ Country | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| Microsoft (OpenAI) | USA | Leader | GPT-4o Vision API | North America, Europe | Expanded Azure OpenAI Vision to 50+ regions; added real-time video API in Q1 2025 |

| Google DeepMind | USA | Leader | Gemini 1.5 Pro Vision | North America, Asia Pacific | Launched Gemini 2.0 Flash multimodal with native video understanding, Jan 2026 |

| Amazon Web Services | USA | Leader | Bedrock Vision (Claude/Titan) | North America, Global Enterprise | Released Amazon Nova Vision model family on Bedrock platform, Dec 2024 |

| Meta AI | USA | Challenger | Llama 3.2 Vision (11B/90B) | Global (Open Weight) | Released Llama 3.3 with enhanced visual reasoning benchmarks, Feb 2026 |

| Anthropic | USA | Challenger | Claude 3.5 Sonnet Vision | North America, Europe | Deployed Claude 3.7 with extended context vision processing, Mar 2025 |

| Stability AI | UK | Niche Player | Stable Diffusion 3.5 Vision | Europe, North America | Partnership with AWS to distribute SD3.5 via Bedrock marketplace, Jan 2025 |

| Cohere | Canada | Niche Player | Aya Vision (Multilingual) | North America, MEA | Launched Aya Vision 32B with 23-language visual QA capability, Nov 2024 |

| Baidu | China | Challenger | ERNIE Vision 4.0 | Asia Pacific | Integrated ERNIE Vision into Baidu Maps for real-time scene analysis, Apr 2025 |

By Offering

The large vision model market by offering divides primarily into platform and API access, professional services, and on-premise deployment licenses. Platform and API access leads the offering mix with 52.3% share in 2025, generating USD 4.10 Billion in annual revenue. This dominance reflects the architectural reality that frontier model inference requires infrastructure at hyperscaler scale, making managed API endpoints the lowest-friction path for most enterprise buyers. Usage-based pricing models from OpenAI, Google, and Anthropic have further democratized access by eliminating minimum commitment thresholds. The professional services segment accounts for 28.4% share in 2025 at USD 2.23 Billion, covering fine-tuning, custom deployment, integration engineering, and ongoing model governance. Demand for professional services is growing fastest among regulated industries such as healthcare, financial services, and defense, where generic foundation models require domain-specific adaptation before they meet compliance thresholds. On-premise and private cloud deployment licenses represent 19.3% share in 2025 at USD 1.51 Billion, primarily serving government agencies, financial institutions with data sovereignty mandates, and enterprises operating in air-gapped environments. This sub-segment is projected to grow at above-average rates through 2034 as distilled and quantized model variants bring frontier-class vision capability to deployment footprints previously restricted to simpler architectures.

By Application

The large vision model market by application spans medical imaging, autonomous systems, retail and e-commerce, content creation, security and surveillance, manufacturing inspection, and other verticals. Medical imaging and diagnostics leads at 18.0% share in 2025, equivalent to USD 1.41 Billion, underpinned by over 950 FDA-authorized AI-enabled medical devices as of 2025 and accelerating hospital system adoption of AI-assisted radiology workflows. The FDA's Digital Health Center of Excellence has processed a record volume of pre-submissions for large vision model-powered diagnostic tools, signaling continued regulatory pathway maturation. Autonomous systems including robotics, drone navigation, and advanced driver assistance represents 16.2% share in 2025 at USD 1.27 Billion and is the fastest-growing application at a projected 24.1% CAGR through 2034, as vision-language-action model architectures achieve sufficient reliability for industrial deployment. Retail and e-commerce accounts for 14.8% share at USD 1.16 Billion, with visual search, automated product tagging, and AR-assisted shopping driving adoption. Content creation and media accounts for 13.6% share at USD 1.07 Billion, while security and surveillance represents 12.4% at USD 0.97 Billion. Manufacturing quality inspection accounts for 11.5% at USD 0.90 Billion, and all other applications, including precision agriculture, geospatial analysis, and education, account for the remaining 13.5%.

By Deployment Mode

The large vision model market by deployment mode divides into cloud-hosted, hybrid, and on-premise configurations. Cloud-hosted deployment commands 61.4% market share in 2025 at USD 4.81 Billion, reflecting the natural alignment between frontier model compute requirements and hyperscaler infrastructure. AWS, Microsoft Azure, and Google Cloud Platform collectively host the preponderance of production-grade large vision model workloads, and their aggressive pricing competition has lowered cloud inference costs by approximately 40% between 2023 and 2025. Hybrid deployment, combining cloud model hosting with edge preprocessing, holds 24.2% share in 2025 at USD 1.90 Billion. This modality is growing rapidly in manufacturing and logistics contexts where bandwidth constraints or latency requirements preclude full cloud inference but centralized model governance remains commercially essential. On-premise-only deployment represents 14.4% of the market in 2025 at USD 1.13 Billion. This segment is disproportionately concentrated in defense, intelligence community applications, and regulated financial services, where data classification frameworks prohibit external processing. The deployment mode mix is expected to shift modestly toward hybrid by 2034 as edge AI hardware, including NVIDIA Jetson Orin and Qualcomm AI 100 Ultra platforms, achieves broader commercial availability.

By End-User Vertical

The large vision model market by end-user vertical spans healthcare and life sciences, technology and media, manufacturing and industrial, retail and consumer, government and defense, financial services, and other sectors. Healthcare and life sciences leads with 22.1% share in 2025 at USD 1.73 Billion, propelled by clinical imaging AI adoption, drug discovery visualization pipelines, and surgical robotics integration. Technology and media follows at 20.8% share (USD 1.63 Billion), encompassing video platform content moderation, generative media production, and developer tooling ecosystems. Manufacturing and industrial represents 17.3% share at USD 1.36 Billion, with machine vision for quality control and defect detection systems transitioning from traditional computer vision to large vision model architectures due to superior generalization across novel defect categories. Retail and consumer holds 14.2% share at USD 1.11 Billion, while government and defense accounts for 11.8% at USD 0.93 Billion. Financial services represents 8.3% at USD 0.65 Billion, primarily in document processing and fraud detection visual analytics. All remaining verticals account for 5.5% collectively.

Regional Analysis

North America

North America holds the dominant position in the large vision model market with 38.5% share in 2025, equivalent to USD 3.02 Billion in annual revenue. The United States accounts for approximately 91% of the regional total at USD 2.75 Billion, driven by the concentration of hyperscaler cloud infrastructure, leading AI research institutions, and deep enterprise software integration ecosystems. The National AI Initiative Act has sustained federal funding inflows to AI research exceeding USD 3.2 Billion annually, while DARPA and NIH programs have specifically funded large vision model applications in defense and biomedical imaging. Canada contributes approximately USD 0.18 Billion at 6% regional share, with significant activity centered on Montreal and Toronto AI research clusters and growing financial services adoption. Mexico represents a smaller but emerging deployment market at approximately USD 0.09 Billion, with manufacturing sector adoption of visual inspection AI accelerating under nearshoring investment trends. The North American large vision model market benefits from the most mature regulatory infrastructure globally, including FDA Digital Health guidance, NIST AI RMF adoption in federal procurement, and SEC cyber disclosure requirements that create documented demand for auditable AI systems. Enterprise software vendors including Salesforce, SAP, and ServiceNow have embedded large vision model capabilities into commercial platforms, expanding the addressable deployment base beyond direct API customers.

Europe

Europe accounts for 26.2% of the global large vision model market in 2025, generating USD 2.05 Billion in annual revenue. Germany leads the European market at an estimated USD 0.54 Billion, driven by automotive manufacturing AI adoption, Industry 4.0 machine vision deployments, and a strong Mittelstand enterprise base investing in quality assurance automation. The United Kingdom follows at USD 0.47 Billion with concentration in financial services, healthcare AI, and a thriving deep-tech venture ecosystem. France contributes approximately USD 0.33 Billion, supported by the national AI strategy Plan France 2030 and growing defense and aerospace applications. The Netherlands, as a European cloud infrastructure hub, accounts for approximately USD 0.22 Billion. The EU AI Act, which categorized certain large vision model applications as high-risk under Annex III, has created a compliance services sub-market estimated at USD 0.31 Billion within the European large vision model market in 2025. While compliance requirements initially created adoption friction, they have concurrently driven demand for certified, documented model offerings from established vendors over unaudited alternatives. The GDPR data localization requirements maintain pressure on cloud deployment models, sustaining above-average demand for sovereign cloud and on-premise deployment options relative to other regions.

Asia Pacific

Asia Pacific represents 22.8% of the large vision model market in 2025 at USD 1.79 Billion and is the fastest-growing region, projected at a CAGR of 23.6% through 2034. China is the largest country market in the region at an estimated USD 0.72 Billion, supported by state-backed AI investment programs, indigenous model development by Baidu, Alibaba (Qwen-VL), and ByteDance, and mandatory AI integration policies in strategic industrial sectors. China's Ministry of Industry and Information Technology has specifically identified multimodal AI as a priority technology under the 14th Five-Year Plan. Japan contributes approximately USD 0.38 Billion, with application focus on robotics, precision manufacturing, and aging-population healthcare solutions. Japan's government through the Society 5.0 initiative has designated visual AI as critical infrastructure. India is the third-largest country market at approximately USD 0.29 Billion, growing at an estimated 27.4% CAGR as enterprise IT services firms and domestic technology companies build large vision model capabilities. South Korea at approximately USD 0.22 Billion rounds out the top four, with Samsung and LG electronics ecosystems driving consumer device and semiconductor-embedded vision AI demand. Regional infrastructure investment by AWS, Google, and Microsoft in local availability zones is rapidly expanding cloud-hosted large vision model accessibility across Southeast Asian markets including Singapore, Indonesia, and Vietnam.

Latin America

Latin America accounts for 7.4% of the global large vision model market in 2025 at USD 0.58 Billion, representing a nascent but accelerating adoption environment. Brazil leads the region at an estimated USD 0.29 Billion, with the Avenida Paulista technology corridor in São Paulo hosting the highest concentration of AI startup activity in Latin America. Federal investment via the MCTI (Ministry of Science, Technology and Innovation) has designated AI including large vision models as a strategic national priority, with BRL 1.8 Billion in committed research funding through 2026. Mexico contributes approximately USD 0.13 Billion, with manufacturing and logistics applications driving adoption as nearshoring investment elevates automation requirements in Monterrey and Guadalajara industrial corridors. Argentina accounts for approximately USD 0.09 Billion with technology services outsourcing firms developing large vision model integration competencies for export. Connectivity infrastructure limitations and currency volatility in several markets constrain cloud API consumption patterns, creating latent demand that will materialize as infrastructure investment matures. The region is expected to grow at a CAGR of 21.8% through 2034 as cloud penetration, developer ecosystem maturity, and enterprise software localization improve.

Middle East and Africa

The Middle East and Africa region represents 5.1% of the large vision model market in 2025, generating USD 0.40 Billion in annual revenue. The UAE is the dominant market at approximately USD 0.17 Billion, underpinned by the Abu Dhabi AI investment vehicle MGIX and its open-weight model initiative Falcon, which has created a sophisticated local AI infrastructure and positioned the UAE as the region's most advanced AI deployment environment. Saudi Arabia follows at approximately USD 0.13 Billion, with Vision 2030 technology transformation mandates driving government and healthcare sector AI adoption at scale. The Saudi Data and AI Authority (SDAIA) has established procurement frameworks that explicitly include large vision model applications for smart city, surveillance, and industrial use cases. South Africa accounts for approximately USD 0.07 Billion, serving as the primary Sub-Saharan deployment hub with financial services and mining sector applications leading demand. Infrastructure investment from Hyperscalers, including the 2025 Microsoft USD 1 Billion South African data center commitment and AWS Middle East expansion, is progressively reducing latency barriers to cloud-hosted large vision model access across the region. The MEA market is projected to grow at a CAGR of 22.3% through 2034, among the highest across all regions.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Platform and API Access

- Professional Services

- On-Premise / Private Cloud Deployment Licenses

By Application

- Medical Imaging and Diagnostics

- Autonomous Systems and Robotics

- Retail and E-Commerce Visual Search

- Content Creation and Media

- Security and Surveillance

- Manufacturing Quality Inspection

- Other Applications (Agriculture, Geospatial, Education)

By Deployment Mode

- Cloud-Hosted

- Hybrid (Cloud + Edge)

- On-Premise

By End-User Vertical

- Healthcare and Life Sciences

- Technology and Media

- Manufacturing and Industrial

- Retail and Consumer

- Government and Defense

- Financial Services

- Other Verticals

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 7.84 B |

| Forecast Revenue (2034) | USD 41.56 B |

| CAGR (2025-2034) | 20.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering, (Platform and API Access, Professional Services, On-Premise / Private Cloud Deployment Licenses), By Application, (Medical Imaging and Diagnostics, Autonomous Systems and Robotics, Retail and E-Commerce Visual Search, Content Creation and Media, Security and Surveillance, Manufacturing Quality Inspection, Other Applications (Agriculture, Geospatial, Education)), By Deployment Mode, (Cloud-Hosted, Hybrid (Cloud + Edge), On-Premise), By End-User Vertical, (Healthcare and Life Sciences, Technology and Media, Manufacturing and Industrial, Retail and Consumer, Government and Defense, Financial Services, Other Verticals) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MICROSOFT CORPORATION (OPENAI PARTNERSHIP)), GOOGLE DEEPMIND (ALPHABET INC.)), AMAZON WEB SERVICES, INC.), META AI (META PLATFORMS, INC.)), ANTHROPIC PBC), BAIDU, INC.), ALIBABA CLOUD (ALIBABA GROUP)), BYTEDANCE LTD.), STABILITY AI LTD.), COHERE INC.), MISTRAL AI SAS), APPLE INC. (APPLE INTELLIGENCE)), SAMSUNG ELECTRONICS CO., LTD.), NVIDIA CORPORATION), IBM CORPORATION), ORACLE CORPORATION), SALESFORCE, INC.), HUGGING FACE, INC.), TOGETHER AI INC.), ADEPT AI LABS INC.), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Medical Imaging, Autonomous Robotics, Visual Search, Content Creation, Security & Surveillance, Manufacturing Inspection), By Deployment Mode (Cloud, Hybrid, On-Premise), By End-User Vertical, AI Vision Trends & Forecast 2026-2034")

, By Application (Medical Imaging, Autonomous Robotics, Visual Search, Content Creation, Security & Surveillance, Manufacturing Inspection), By Deployment Mode (Cloud, Hybrid, On-Premise), By End-User Vertical, AI Vision Trends & Forecast 2026-2034")

, By Application (Medical Imaging, Autonomous Robotics, Visual Search, Content Creation, Security & Surveillance, Manufacturing Inspection), By Deployment Mode (Cloud, Hybrid, On-Premise), By End-User Vertical, AI Vision Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Large Vision Model Market?

The Global Large Vision Model (LVM) Market was valued at USD 6.51 Billion in 2024 and is projected to reach USD 41.56 Billion by 2034, growing at a CAGR of 20.4% from 2026 to 2034, driven by rapid advancements in generative AI, multimodal learning, computer vision applications, autonomous systems, and increasing enterprise adoption of AI-powered image and video analytics solutions.

Who are the major players in the Large Vision Model Market?

MICROSOFT CORPORATION (OPENAI PARTNERSHIP)), GOOGLE DEEPMIND (ALPHABET INC.)), AMAZON WEB SERVICES, INC.), META AI (META PLATFORMS, INC.)), ANTHROPIC PBC), BAIDU, INC.), ALIBABA CLOUD (ALIBABA GROUP)), BYTEDANCE LTD.), STABILITY AI LTD.), COHERE INC.), MISTRAL AI SAS), APPLE INC. (APPLE INTELLIGENCE)), SAMSUNG ELECTRONICS CO., LTD.), NVIDIA CORPORATION), IBM CORPORATION), ORACLE CORPORATION), SALESFORCE, INC.), HUGGING FACE, INC.), TOGETHER AI INC.), ADEPT AI LABS INC.), Others

Which segments covered the Large Vision Model Market?

By Offering, (Platform and API Access, Professional Services, On-Premise / Private Cloud Deployment Licenses), By Application, (Medical Imaging and Diagnostics, Autonomous Systems and Robotics, Retail and E-Commerce Visual Search, Content Creation and Media, Security and Surveillance, Manufacturing Quality Inspection, Other Applications (Agriculture, Geospatial, Education)), By Deployment Mode, (Cloud-Hosted, Hybrid (Cloud + Edge), On-Premise), By End-User Vertical, (Healthcare and Life Sciences, Technology and Media, Manufacturing and Industrial, Retail and Consumer, Government and Defense, Financial Services, Other Verticals)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date