- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Leather Handbags Market to Hit $78.5 Bn by 2034 | 6.3% CAGR

Global Leather Handbags Market Size, Share, Analysis Report By Type (Tote Bags & Satchels, Shoulder Bags, Clutches, Backpacks, Others), By Platform (E-commerce & Online Retail, Department Stores & Boutiques, Direct-to-Consumer), By End-User (Women, Men & Unisex) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034

Report Overview

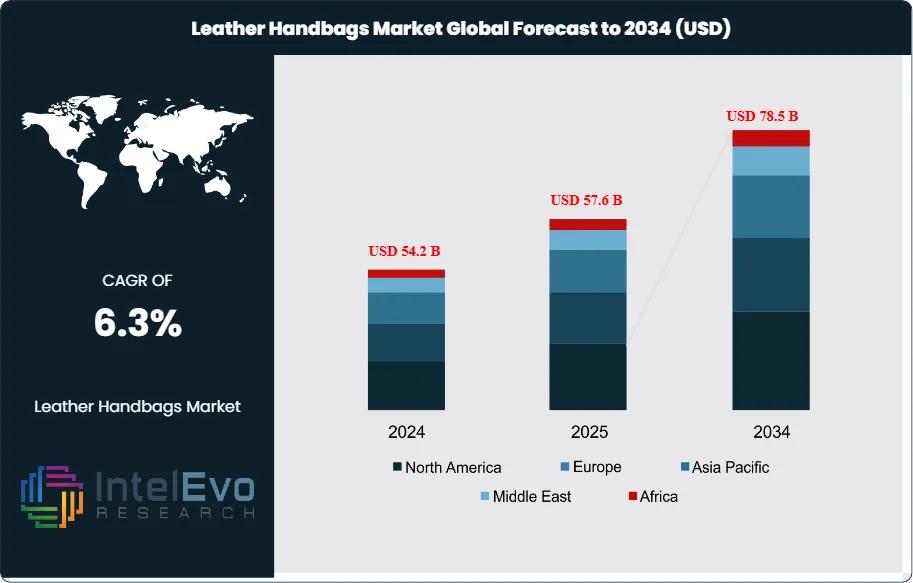

The Global leather handbags market is changing, showing a clear trend toward higher-value purchases and brand differentiation. Valued at USD 54.2 billion in 2024, the market is expected to grow to USD 78.5 billion by 2034, with a compound annual growth rate of 6.3% during this time. The demand remains strong due to increased spending in emerging economies and a lasting interest in traditional craftsmanship in mature markets. By early 2026, the competitive landscape reveals a split strategy. Global luxury brands are strengthening their positions with limited-edition, high-margin items that serve as "investment pieces." In contrast, nimble contemporary brands focus on sustainability, accessibility, and online-first distribution methods.

Get More Information about this report -

Request Free Sample ReportProduct categories are varied and strategically diverse, including Tote Bags, Shoulder Bags, Satchels, Clutches, and Backpacks. This variety helps brands meet both practical and occasion-driven needs. Tote and shoulder bags lead revenue contributions because of their versatility and usefulness, especially for working women in urban settings. At the same time, clutches and mini satchels benefit from purchases driven by events and fashion trends. Premium leather backpacks are becoming popular among younger consumers who want a mix of luxury and practicality. This wide range of products lowers the risk within categories and allows brands to improve their profit margins through seasonal collections and limited releases.

A key theme in the industry is the rise of a "Dual-Track" growth model. Established luxury companies are boosting brand value through scarcity in pricing, artisanal appeal, and controlled distribution. Meanwhile, online-first brands are appealing to Gen Z and millennials with clear sourcing, circular fashion systems, resale options, and plant-based or eco-friendly leather substitutes. Social commerce platforms, especially in China and Southeast Asia, have become vital for accelerating demand. They facilitate product discovery led by influencers and achieve high conversion rates. This integration of digital commerce has shortened product lifecycles and increased competition across both premium and mid-tier markets.

On the supply side, the market faces challenges due to unstable raw hide prices, costs related to environmental regulations, and changing trade rules. Stricter global enforcement against counterfeiting has bolstered brand protection but raised compliance costs. After the pandemic, retail operations have largely stabilized, but geopolitical tensions and shipping delays have prompted near-shoring strategies in Europe and North America. These strategies aim to reduce lead times and manage logistics risks. Looking ahead, operational flexibility, alignment with environmental and social governance, and integrated sales channels will be vital for gaining a competitive edge in a market that increasingly merges traditional luxury with sustainable practices.

, By Platform (E-commerce & Online Retail, Department Stores & Boutiques, Direct-to-Consumer), By End-User (Women, Men & Unisex) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Key Takeaways

- Market Growth: The market is projected to reach USD 78.5 billion by 2034, as consumers increasingly view handbags as both functional accessories and status symbols.

- Type Dominance: Tote bags and satchels account for 38% of the market in 2024, followed by shoulder bags (XX%), clutches (XX%), and backpacks (XX%).

- Platform Dominance: E-commerce and online retail channels represent over 32% of global sales, with department stores and specialty boutiques maintaining a strong presence.

- End-User Dominance: Women represent 82% of the market, with men’s leather handbags and unisex styles gaining traction.

- Driver: Rising disposable incomes, urbanization, and the influence of fashion media are fueling demand.

- Restraint: High prices of premium leather, counterfeit products, and growing competition from synthetic alternatives.

- Opportunity: Sustainable and vegan leather, customization, and expansion into emerging markets.

- Trend: Eco-friendly materials, limited-edition collaborations, and digital marketing campaigns are shaping consumer preferences.

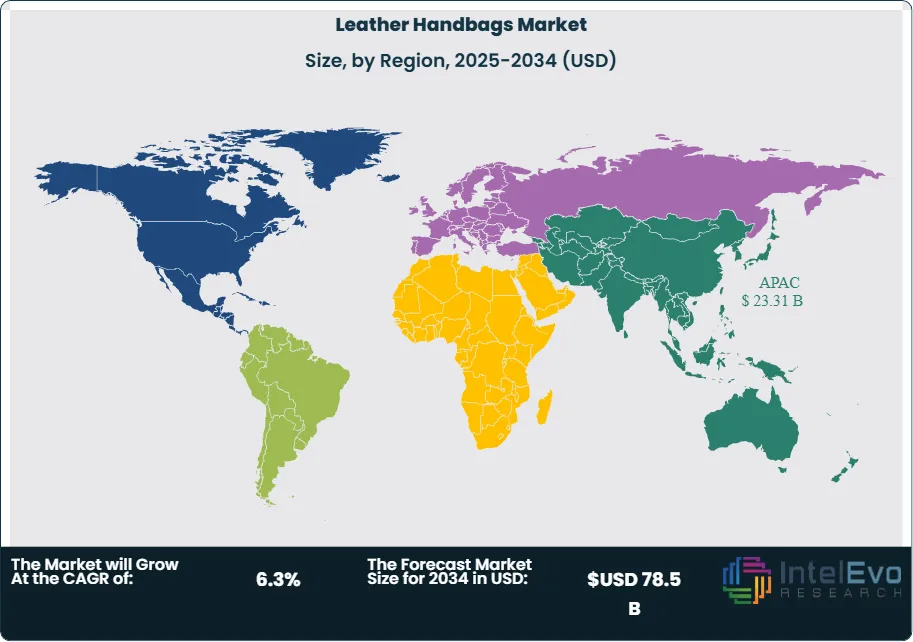

- Regional Analysis: Asia Pacific leads with 36% market share in 2024, followed by Europe (XX%) and North America (XX%). Latin America and the Middle East & Africa are emerging markets with rising luxury consumption.

Type Analysis

Tote and shoulder bags are the functional core of the market, making up over 60% of total volume in 2026. These bags have gained popularity due to the return to office and hybrid work trends. Consumers now need durable, spacious bags that can carry technology and personal items. In the premium segment, designers are creating bags with hidden compartments for devices, using high-quality, vegetable-tanned leathers that develop a unique patina over time. This appeals to consumers who value longevity.

On the other hand, mini bags and clutches are experiencing a resurgence in 2026, thanks to the micro-trend cycle on social media. Although these items are less practical, they are marketed as entry-level luxury or wearable jewelry. Brands like Jacquemus and Prada have introduced these styles to attract a younger customer base. For the 2024-2034 period, the East-West (elongated rectangular) shape is emerging as a popular sub-type, combining the elegance of a clutch with the practicality of a shoulder bag.

Platform Analysis

Offline retail remains the main driver of the leather handbag market, especially for luxury items. In 2026, the in-store experience has transformed into experiential retail. Flagship stores in cities like Paris, Shanghai, and New York now offer customization ateliers and VIP lounges where customers can choose specific leather grains and hardware. This physical experience is vital for assessing the quality and feel of genuine leather, which influences high-value purchases.

Online platforms are the fastest-growing segment and are projected to make up nearly 50% of total sales by 2034. The use of AI-powered virtual try-ons and high-fidelity 3D rendering has built trust in online leather goods. Additionally, social commerce platforms like TikTok Shop and Little Red Book (Xiaohongshu) allow brands to sell directly to consumers, bypassing traditional retailers. In 2026, many brands are offering online-exclusive limited-edition leather colors to increase digital traffic and urgency.

End-User Analysis

The women's segment leads the leather handbag market. In 2026, buying habits are increasingly driven by financial empowerment in emerging economies such as India and Vietnam. Women are shifting from seasonal it-bags to heritage investments, favoring styles like the Hermès Birkin or Chanel Classic Flap, viewed as safeguards against inflation. This move towards investment-grade fashion contributes to a strong CAGR despite economic fluctuations.

The men's segment, though smaller, is the growth wildcard from 2025 to 2034. The bags for men category has expanded beyond briefcases to include crossbody tech pouches, leather backpacks, and oversized totes. Influenced by gorpcore and high-fashion streetwear trends, men are becoming more comfortable with leather accessories. Brands like Louis Vuitton, under Pharrell Williams, are targeting this demographic with bold leather designs that challenge traditional masculine norms, creating a significant revenue opportunity.

Regional Analysis

Asia-Pacific is the global leader of the leather handbag market in 2026, holding over 43% of the market share. While China is the main driver, India is emerging as a key growth region, fueled by a growing middle class and a passion for leather craftsmanship. The region's growth is supported by a large young population, heavily influenced by K-Pop and C-Drama celebrity endorsements, which can lead specific handbag styles to sell out worldwide shortly after a social media post.

Europe and North America focus on quality and value. While volume growth is slower than in Asia-Pacific, the average unit value is higher. European consumers, especially in France and Italy, prefer artisanal, locally-made products and are early adopters of sustainable, circular leather initiatives. In the United States, the market benefits from high disposable income and a vibrant resale market, normalizing the perception of high-end leather bags as both depreciable and liquid assets.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

Type

- Tote Bags & Satchels

- Shoulder Bags

- Clutches

- Backpacks

- Others

Platform

- E-commerce & Online Retail

- Department Stores & Boutiques

- Direct-to-Consumer

End-User

- Women

- Men & Unisex

Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 57.6 B |

| Forecast Revenue (2034) | USD 78.5 B |

| CAGR (2025-2034) | 6.3% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Type (Tote Bags & Satchels, Shoulder Bags, Clutches, Backpacks, Others), By Platform (E-commerce & Online Retail, Department Stores & Boutiques, Direct-to-Consumer), By End-User (Women, Men & Unisex) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LVMH Moët Hennessy Louis Vuitton SE, Kering SA (Gucci, Saint Laurent), Prada Group, Coach (Tapestry, Inc.), Michael Kors (Capri Holdings), Hermès International S.A., Burberry Group PLC, Fossil Group, Inc., Kate Spade, Tory Burch LLC, Longchamp, Furla, Samsonite International S.A., Hidesign, Charles & Keith |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Platform (E-commerce & Online Retail, Department Stores & Boutiques, Direct-to-Consumer), By End-User (Women, Men & Unisex) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, By Platform (E-commerce & Online Retail, Department Stores & Boutiques, Direct-to-Consumer), By End-User (Women, Men & Unisex) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, By Platform (E-commerce & Online Retail, Department Stores & Boutiques, Direct-to-Consumer), By End-User (Women, Men & Unisex) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date