- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Lipid Nanoparticle Drug Delivery Market Size, Share & Growth | CAGR 12.7%

Global Lipid Nanoparticle Drug Delivery Market Size, Share, Analysis By Payload Type (mRNA & saRNA Delivery, siRNA & Oligonucleotide Delivery, Gene Editing & CRISPR Cargo Delivery, Small Molecule and Protein Payloads), By Application (Infectious Disease Vaccines, Genetic & Liver Diseases, Oncology, Rare & Metabolic Diseases), By End User (Pharmaceutical & Biotechnology Companies, CDMOs & Manufacturing Partners, Academic Research Institutes), By Business Model (Commercial LNP Products, Licensed IP Platforms, Development & Manufacturing Services) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 8.4 Billion, 2025 | USD 24.6 Billion, 2034 | 12.7%, 2026–2034 | North America, 44.0%, 2025 |

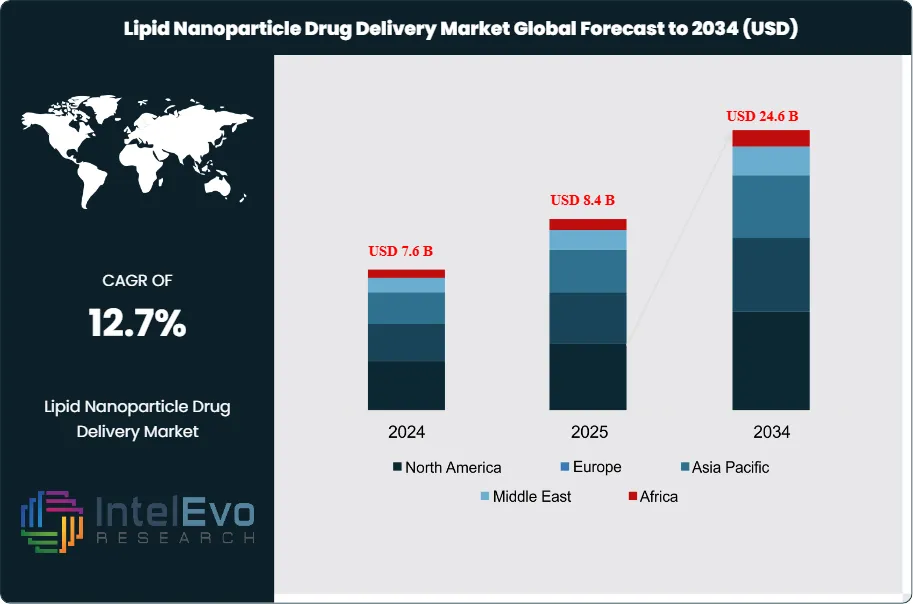

The Lipid Nanoparticle Drug Delivery Market was valued at approximately USD 7.6 Billion in 2024 and increased to USD 8.4 Billion in 2025. The market is projected to reach nearly USD 24.6 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 12.7% during the forecast period from 2026 to 2034. Market growth is primarily driven by the increasing adoption of lipid nanoparticle platforms for mRNA vaccines, gene therapies, and targeted drug delivery applications. Additionally, rising investments in nanomedicine research, expanding clinical pipelines for RNA-based therapeutics, and technological advancements in lipid formulation and delivery systems are expected to further accelerate the adoption of lipid nanoparticle drug delivery technologies across pharmaceutical and biotechnology sectors.

Get More Information about this report -

Request Free Sample ReportThis report defines the Lipid Nanoparticle Drug Delivery Market as the value created by LNP-enabled nucleic acid medicines, platform licensing, and specialized development and manufacturing services tied to LNP delivery. The 2025 market was still anchored by commercial mRNA vaccines, but it was no longer a single-product story. Pfizer reported USD 4.37 Billion in 2025 Comirnaty revenue, while Moderna reported USD 1.94 Billion in 2025 revenue and said it had three marketed products at year-end. Those numbers explain why vaccines still dominate current LNP revenue. They also show why the Lipid Nanoparticle Drug Delivery Market remains commercially meaningful even after the pandemic peak passed.

The market also widened beyond prophylactic vaccines. Alnylam reported USD 173 Million of full-year 2025 ONPATTRO revenue, and the FDA label continues to describe ONPATTRO as a lipid complex injection, keeping it relevant as the first approved systemic RNA-LNP medicine. Acuitas highlighted in 2025 that its LNP technology enabled the first personalized CRISPR therapy dosed in an infant with a urea cycle disorder and also supports the first in-human genome base-editing trial. These signals matter because they show that the Lipid Nanoparticle Drug Delivery Market is moving from a vaccine-heavy commercial base toward broader therapeutic use in gene editing, RNA therapeutics, and personalized medicine.

The supply side is now just as important as the science. Genevant and Arbutus announced in March 2026 a global settlement with Moderna worth up to USD 2.25 Billion, which underlined the commercial value of core LNP intellectual property. Evonik expanded its LNP and nucleic-acid service footprint through a January 2025 partnership with ST Pharm and a September 2025 partnership with Ethris. Cytiva continued to push end-to-end NanoAssemblr systems and LNP kits, while CordenPharma expanded investments in lipids and LNP manufacturing across its global network in 2024 and 2025. The market is therefore being shaped by a combination of product revenue, IP control, and manufacturing scale.

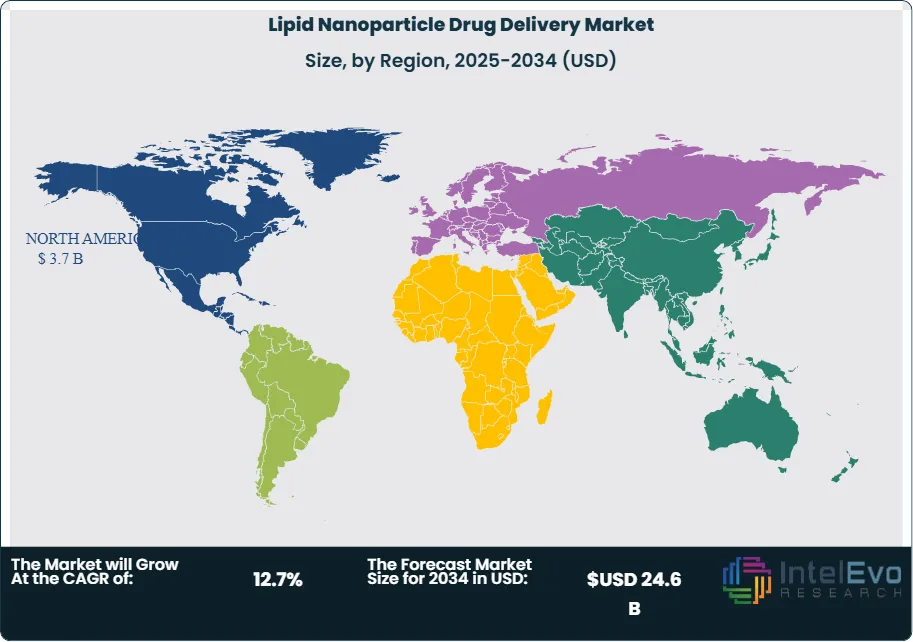

Technology direction in the Lipid Nanoparticle Drug Delivery Market is also shifting. Developers now want repeat dosing, better tolerability, extrahepatic delivery, preformed-vesicle manufacturing, and payload flexibility across mRNA, saRNA, siRNA, and CRISPR cargo. Acuitas presented next-generation LNP data in November 2025 focused on potency, safety, and broader tissue reach. Cytiva positioned its platforms for mRNA, cell therapy, and RNA therapeutics. Regionally, North America held 44.0% of the Lipid Nanoparticle Drug Delivery Market in 2025, equal to USD 3.7 Billion, followed by Europe at 28.0% and Asia Pacific at 19.0%. North America led because it combines the largest approved LNP-enabled product base with the deepest concentration of platform owners, IP holders, and nucleic-acid developers. Europe remained the main platform and CDMO expansion zone, while Asia Pacific gained strategic weight through South Korean API manufacturing and Japan’s growing RNA delivery activity.

, By Application (Infectious Disease Vaccines, Genetic & Liver Diseases, Oncology, Rare & Metabolic Diseases), By End User (Pharmaceutical & Biotechnology Companies, CDMOs & Manufacturing Partners, Academic Research Institutes), By Business Model (Commercial LNP Products, Licensed IP Platforms, Development & Manufacturing Services) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

| Market Growth | The Lipid Nanoparticle Drug Delivery Market stood at USD 8.4 Billion in 2025 and is projected to reach USD 24.6 Billion by 2034 at a 12.7% CAGR. The 2025 base was driven mainly by LNP-enabled mRNA vaccines and a smaller but growing contribution from RNA therapeutics, platform licensing, and CDMO services. |

| Segment Dominance | By payload type, mRNA and saRNA delivery led with 68.0% share in 2025, or USD 5.7 Billion. Pfizer’s USD 4.37 Billion in 2025 Comirnaty revenue and Moderna’s USD 1.94 Billion in 2025 revenue explain why this segment remained dominant. |

| Segment Dominance | By application, infectious disease prophylaxis and respiratory vaccines held the largest share at 54.0% in 2025, equal to USD 4.5 Billion. The segment stayed ahead because approved LNP medicines are still concentrated in commercial mRNA vaccines. |

| Driver | The main driver is the widening use of LNPs across approved products and late-stage pipelines. ONPATTRO produced USD 173 Million in 2025 revenue, while Acuitas showcased repeated dosing of personalized CRISPR therapy with no adverse events in a first-in-human setting. |

| Restraint | The primary restraint is IP complexity and manufacturing dependence. The March 2026 Genevant-Arbutus settlement with Moderna reached up to USD 2.25 Billion, which shows how central core LNP IP remains to market economics. |

| Opportunity | The largest opportunity sits in extrahepatic delivery, gene editing, and personalized RNA therapeutics. Acuitas’ 2025 and 2026 disclosures and Evonik’s 2025 nucleic-acid partnerships suggest more than USD 6.0 Billion of incremental addressable market expansion could emerge between 2025 and 2034. |

| Trend | The dominant trend is vertical integration across RNA payloads, lipids, formulation, and scale-up. Cytiva, Evonik, CordenPharma, and Acuitas all expanded platform depth in 2024–2026, signaling that end-to-end control is becoming a competitive requirement. |

| Regional Analysis | North America led the Lipid Nanoparticle Drug Delivery Market with 44.0% share and USD 3.7 Billion revenue in 2025. The region benefits from the largest LNP-enabled commercial product base and the heaviest concentration of LNP platform companies. |

Competitive Landscape

The Lipid Nanoparticle Drug Delivery Market is moderately consolidated. The top four companies controlled an estimated 63.0% of 2025 market value capture when product-linked revenue, LNP platform licensing, and enabling technology influence are combined. Competition is technology-driven and platform-based rather than purely price-driven. Pfizer remained the largest commercial LNP revenue anchor through Comirnaty. Moderna stayed second through its marketed mRNA portfolio. Genevant and Arbutus proved the economic weight of foundational LNP IP through a settlement worth up to USD 2.25 Billion, while Acuitas kept expanding its role in gene editing and next-generation RNA delivery.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| PFIZER | US | Leader | Comirnaty LNP-enabled vaccine franchise | North America, Europe | Reported USD 4.37 Billion in 2025 Comirnaty revenue in Feb 2026 results. |

| MODERNA | US | Leader | Spikevax / mRNA-LNP platform | North America | Settled global LNP patent litigation with Genevant and Arbutus for up to USD 2.25 Billion in Mar 2026. |

| GENEVANT SCIENCES | US | Leader | LNP patent and licensing platform | North America | Secured up to USD 2.25 Billion in global settlement terms with Moderna in Mar 2026. |

| ACUITAS THERAPEUTICS | Canada | Leader | ALC-0315 / proprietary LNP delivery platform | North America | Took a majority stake in RNA Technologies & Therapeutics in Jan 2026 to integrate RNA construct and LNP capabilities. |

| ARBUTUS BIOPHARMA | Canada | Challenger | Legacy LNP IP portfolio with Genevant | North America | Co-announced the Moderna LNP settlement and global license structure in Mar 2026. |

| ALNYLAM PHARMACEUTICALS | US | Challenger | ONPATTRO | North America, Europe | Reported USD 173 Million in full-year 2025 ONPATTRO revenue in Feb 2026. |

| EVONIK | Germany | Challenger | LNP CDMO and formulation platform | Europe | Partnered with Ethris in Sep 2025 to co-develop LNP offerings for nucleic-acid delivery. |

| CYTIVA | US | Challenger | NanoAssemblr commercial formulation system | North America, Europe | Expanded accessible LNP formulation tools and RNA delivery kits across 2024. |

| CORDENPHARMA | Switzerland | Niche Player | Customized lipid excipients and LNP manufacturing | Europe | Expanded lipids and LNP capacity investments across six technology platforms in Nov 2024 and Mar 2025. |

| ST PHARM | South Korea | Niche Player | SmartCap and nucleic-acid API integration for LNP programs | Asia Pacific | Partnered with Evonik in Jan 2025 to offer integrated RNA and LNP development solutions. |

By Payload Type

mRNA and saRNA delivery led the Lipid Nanoparticle Drug Delivery Market with 68.0% share in 2025, or USD 5.7 Billion. This segment remained dominant because the largest approved LNP-enabled products are still mRNA vaccines. Pfizer’s USD 4.37 Billion of 2025 Comirnaty revenue and Moderna’s USD 1.94 Billion of 2025 revenue explain most of the current scale. The segment also benefits from the broadest manufacturing maturity, the clearest regulatory history, and the most visible installed commercial infrastructure. siRNA and related oligonucleotide delivery represented 18.0%, equal to USD 1.5 Billion, anchored by ONPATTRO and by continuing interest in extrahepatic RNA delivery. Gene editing and CRISPR cargo delivery accounted for 9.0%, or USD 0.8 Billion, and remained strategically important despite smaller current revenue because Acuitas and CHOP demonstrated real-world personalized CRISPR dosing in 2025. Small molecule, protein, and other payloads represented 5.0%, or USD 0.4 Billion, but they remain peripheral compared with nucleic-acid payloads. This mix shows that the Lipid Nanoparticle Drug Delivery Market is still dominated by RNA delivery, yet it is clearly expanding into broader payload diversity as safety, repeat-dosing, and tissue-targeting improve.

By Application

Infectious disease prophylaxis and respiratory vaccines accounted for 54.0% of the Lipid Nanoparticle Drug Delivery Market in 2025, equal to USD 4.5 Billion. This segment led because commercial LNP use is still overwhelmingly tied to COVID-19 and related respiratory vaccination programs. It remains the revenue anchor even after demand normalized from pandemic highs. Genetic and liver-related diseases held 18.0%, or USD 1.5 Billion, reflecting the continued relevance of ONPATTRO and the broader expectation that hepatocyte-directed delivery remains the first scalable non-vaccine therapeutic use case. Oncology represented 17.0%, or USD 1.4 Billion, supported mainly by pipeline investment, personalized cancer vaccine work, and increasing interest in repeat-dosed LNP systems. Rare disease, metabolic disease, and personalized medicine accounted for 11.0%, or USD 0.9 Billion. This smaller segment matters strategically because it is where LNP flexibility, rapid formulation, and individualized manufacturing can command the strongest value per patient. The application split makes one point clear. The Lipid Nanoparticle Drug Delivery Market is still commercially led by vaccines, but future margin expansion will come from therapeutic applications rather than seasonal prophylaxis alone.

By End User

Pharmaceutical and biotechnology companies accounted for 62.0% of the Lipid Nanoparticle Drug Delivery Market in 2025, or USD 5.2 Billion. They led because the largest commercial products and most advanced internal LNP programs still sit inside large vaccine, RNA, and genetic medicine companies. Pfizer, Moderna, Alnylam, and platform-intensive developers remained the main direct users of LNP delivery at scale. CDMOs, formulation service providers, and manufacturing partners held 24.0%, equal to USD 2.0 Billion, and this segment is gaining weight because payload developers increasingly outsource lipid synthesis, nanoparticle formulation, process scale-up, and GMP batch production. Evonik, Cytiva, CordenPharma, and ST Pharm fit this structure. Academic and research institutions represented 14.0%, or USD 1.2 Billion, reflecting the market’s ongoing dependence on translational science and early modality exploration. The end-user mix highlights a central feature of the Lipid Nanoparticle Drug Delivery Market. Commercial revenue still sits with product owners, but enabling value is moving toward specialized service and platform ecosystems that reduce time to clinic and improve scalability. That shift will continue through 2034 as more developers try to move beyond liver-targeted and single-dose applications.

By Business Model

Commercial LNP-enabled products held the largest share at 45.0% in 2025, equal to USD 3.8 Billion. This segment includes approved vaccines and therapeutics whose clinical function depends directly on LNP delivery. It remained dominant because approved-product revenue is still the clearest monetary proof of LNP value creation. Licensed IP and platform access represented 37.0%, or USD 3.1 Billion, and this segment became more visible after the Genevant-Arbutus settlement with Moderna, which reached up to USD 2.25 Billion and underscored the financial weight of foundational LNP patents. Development and manufacturing services accounted for 18.0%, or USD 1.5 Billion, supported by Evonik, Cytiva, CordenPharma, and other specialized providers. This segment is smaller today, but it should grow fastest as more nucleic-acid payload developers need scalable formulation without building full in-house capacity. The business-model split shows that the Lipid Nanoparticle Drug Delivery Market is not just a drug market and not just a tools market. It is a hybrid market where commercial products, licensing economics, and specialized services all generate material value at the same time.

Regional Analysis

North America Analysis

North America held 44.0% of the Lipid Nanoparticle Drug Delivery Market in 2025, equal to USD 3.7 Billion. The United States led the region, followed by Canada and Mexico. The U.S. remained the commercial center because it captured the bulk of Comirnaty and Moderna respiratory product revenue and hosts the most active concentration of LNP-enabled RNA companies, platform licensors, and clinical developers. Pfizer reported USD 4.37 Billion in 2025 Comirnaty revenue, while Moderna reported USD 1.94 Billion in 2025 revenue. Arbutus and Genevant also made North America central to LNP economics through litigation and settlement activity. Canada is strategically important because Acuitas Therapeutics is based there and remains one of the most influential independent LNP platform companies. Mexico is still much smaller in direct LNP platform value, but it benefits from broader North American RNA medicine supply and commercialization ties.

North America’s main strength is its full-stack ecosystem. Product developers, platform owners, litigation centers, specialized clinicians, and venture-backed delivery science are all concentrated in the region. This lowers the distance between discovery, clinical development, and commercial scale-up. It also raises the region’s sensitivity to IP outcomes. The March 2026 Moderna settlement showed that core LNP rights can move billions of dollars in value. North America should remain the largest regional market through 2034 because it combines the strongest current product base with the deepest next-wave therapeutic pipeline.

Europe Analysis

Europe accounted for 28.0% of the Lipid Nanoparticle Drug Delivery Market in 2025, or USD 2.4 Billion. Germany, France, the UK, and Switzerland were the most relevant countries. Germany is especially important because Evonik continues to expand nucleic-acid and LNP services there and because the broader German biotech system remains central to RNA platform development. The UK contributes through large pharmaceutical partnerships and IP-centered commercialization. France matters through multinational life sciences demand and advanced biologics infrastructure. Switzerland became more important in 2025 because CordenPharma announced a more than EUR 500 Million greenfield expansion near Basel and explicitly included lipid excipients and LNPs within its strategic technology platforms. Europe is therefore both a development region and a manufacturing region.

Europe’s main advantage is platform infrastructure. Cytiva’s NanoAssemblr systems, Evonik’s CDMO expansion, and CordenPharma’s investment profile all point to a region built around enabling technology and process scale-up rather than only product commercialization. It is less concentrated than North America in blockbuster product revenue, but it is stronger in cross-company enabling capacity. That should help Europe retain a strong share of the Lipid Nanoparticle Drug Delivery Market through 2034, particularly in services, platform licensing, and development manufacturing.

Asia Pacific Analysis

Asia Pacific held 19.0% of the Lipid Nanoparticle Drug Delivery Market in 2025, equal to USD 1.6 Billion. China, Japan, India, and South Korea were the most strategically relevant countries. Japan remained important because RNA and mRNA delivery are increasingly tied to commercial vaccine and therapeutic development pathways there. South Korea became more visible in 2025 after ST Pharm partnered with Evonik to offer integrated RNA and LNP development solutions, linking nucleic-acid API capability to downstream delivery services. China remains strategically significant because it is a major nucleic-acid innovation and manufacturing region, even though specific public LNP product revenue disclosures are less transparent. India remains an emerging formulation and development market rather than a fully scaled LNP platform leader in 2025.

Asia Pacific’s strength lies in manufacturing economics and growth potential. The region still trails North America and Europe in approved high-value LNP-enabled product revenue, but it is increasingly important in API integration, scale-up, and future therapeutic payload development. As RNA medicine pipelines broaden and regional demand for nucleic-acid delivery grows, Asia Pacific should gain share faster than Europe on a percentage-growth basis through 2034.

Latin America Analysis

Latin America represented 6.0% of the Lipid Nanoparticle Drug Delivery Market in 2025, or USD 0.5 Billion. Brazil led the region, followed by Mexico and Argentina. Commercial scale remained limited compared with North America and Europe because advanced RNA medicine manufacturing, LNP formulation, and specialized IP licensing are still concentrated outside the region. Brazil led because it has the strongest pharmaceutical and biotech base in Latin America and the largest long-term demand potential for complex biologics and nucleic-acid delivery. Mexico followed through regional manufacturing and commercialization ties to North America. Argentina remained smaller and more constrained by capital and industrial scale. The region is still largely an adoption market rather than a platform-origin market in 2025.

The opportunity is real, but it is secondary. Latin America is more likely to capture downstream vaccine and therapeutic adoption first, then a narrower slice of formulation and manufacturing value later. Its main barrier is not scientific capability. It is concentration of capital-intensive LNP infrastructure elsewhere. Even so, as more off-the-shelf RNA medicines move toward broader use, the region should gradually expand from a low base.

Middle East & Africa Analysis

Middle East & Africa held 3.0% of the Lipid Nanoparticle Drug Delivery Market in 2025, equal to USD 0.3 Billion. The UAE, Saudi Arabia, and South Africa were the most relevant countries. The region remained the smallest because LNP value creation still depends heavily on advanced nucleic-acid manufacturing, IP access, and specialized translational infrastructure. The UAE and Saudi Arabia led through stronger life sciences investment and premium healthcare access. South Africa remained the most relevant sub-Saharan market because of its broader scientific base and clinical infrastructure. In 2025, the region’s role was still more about selective adoption and future strategic interest than about large-scale platform ownership or manufacturing.

The main limitation is industrial depth. LNP drug delivery needs lipid chemistry expertise, formulation science, and scalable GMP capability that remain concentrated in North America, Europe, and parts of Asia Pacific. Middle East & Africa should remain the smallest major regional market through 2034, but targeted investment in high-income Gulf healthcare and biotech initiatives can raise its absolute value from a low base.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Payload Type

- mRNA and saRNA Delivery

- siRNA and Related Oligonucleotide Delivery

- Gene Editing and CRISPR Cargo Delivery

- Small Molecule, Protein, and Other Payloads

By Application

- Infectious Disease Prophylaxis and Respiratory Vaccines

- Genetic and Liver-Related Diseases

- Oncology

- Rare Disease, Metabolic Disease, and Personalized Medicine

By End User

- Pharmaceutical and Biotechnology Companies

- CDMOs, Formulation Service Providers, and Manufacturing Partners

- Academic and Research Institutions

By Business Model

- Commercial LNP-Enabled Products

- Licensed IP and Platform Access

- Development and Manufacturing Services

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.4 B |

| Forecast Revenue (2034) | USD 24.6 B |

| CAGR (2025-2034) | 12.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Payload Type, (mRNA and saRNA Delivery, siRNA and Related Oligonucleotide Delivery, Gene Editing and CRISPR Cargo Delivery, Small Molecule, Protein, and Other Payloads), By Application, (Infectious Disease Prophylaxis and Respiratory Vaccines, Genetic and Liver-Related Diseases, Oncology, Rare Disease, Metabolic Disease, and Personalized Medicine), By End User, (Pharmaceutical and Biotechnology Companies, CDMOs, Formulation Service Providers, and Manufacturing Partners, Academic and Research Institutions), By Business Model, (Commercial LNP-Enabled Products, Licensed IP and Platform Access, Development and Manufacturing Services) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PFIZER, MODERNA, GENEVANT SCIENCES, ACUITAS THERAPEUTICS, ARBUTUS BIOPHARMA, BIONTECH, ALNYLAM PHARMACEUTICALS, EVONIK, CYTIVA, CORDENPHARMA, ST PHARM, CUREVAC, ROIVANT SCIENCES, PRECISION NANOSYSTEMS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Infectious Disease Vaccines, Genetic & Liver Diseases, Oncology, Rare & Metabolic Diseases), By End User (Pharmaceutical & Biotechnology Companies, CDMOs & Manufacturing Partners, Academic Research Institutes), By Business Model (Commercial LNP Products, Licensed IP Platforms, Development & Manufacturing Services) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Infectious Disease Vaccines, Genetic & Liver Diseases, Oncology, Rare & Metabolic Diseases), By End User (Pharmaceutical & Biotechnology Companies, CDMOs & Manufacturing Partners, Academic Research Institutes), By Business Model (Commercial LNP Products, Licensed IP Platforms, Development & Manufacturing Services) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Infectious Disease Vaccines, Genetic & Liver Diseases, Oncology, Rare & Metabolic Diseases), By End User (Pharmaceutical & Biotechnology Companies, CDMOs & Manufacturing Partners, Academic Research Institutes), By Business Model (Commercial LNP Products, Licensed IP Platforms, Development & Manufacturing Services) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Lipid Nanoparticle Drug Delivery Market?

The Global Lipid Nanoparticle Drug Delivery Market was valued at USD 8.4 Billion in 2025, projected to reach USD 24.6 Billion by 2034 at a CAGR of 12.7% from 2026–2034. Growth is driven by expanding mRNA vaccine development, RNA-based therapeutics, nanomedicine innovation, and rising demand for targeted drug delivery technologies.

Who are the major players in the Lipid Nanoparticle Drug Delivery Market?

PFIZER, MODERNA, GENEVANT SCIENCES, ACUITAS THERAPEUTICS, ARBUTUS BIOPHARMA, BIONTECH, ALNYLAM PHARMACEUTICALS, EVONIK, CYTIVA, CORDENPHARMA, ST PHARM, CUREVAC, ROIVANT SCIENCES, PRECISION NANOSYSTEMS, Others

Which segments covered the Lipid Nanoparticle Drug Delivery Market?

By Payload Type, (mRNA and saRNA Delivery, siRNA and Related Oligonucleotide Delivery, Gene Editing and CRISPR Cargo Delivery, Small Molecule, Protein, and Other Payloads), By Application, (Infectious Disease Prophylaxis and Respiratory Vaccines, Genetic and Liver-Related Diseases, Oncology, Rare Disease, Metabolic Disease, and Personalized Medicine), By End User, (Pharmaceutical and Biotechnology Companies, CDMOs, Formulation Service Providers, and Manufacturing Partners, Academic and Research Institutions), By Business Model, (Commercial LNP-Enabled Products, Licensed IP and Platform Access, Development and Manufacturing Services)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Lipid Nanoparticle Drug Delivery Market

Published Date : 16 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date