- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Liposomal Drug Delivery Market Size, Share & Forecast | CAGR of 8.9%

Global Liposomal Drug Delivery Market Size, Share, Analysis By Product (Doxorubicin, Amphotericin B, Paclitaxel), By Technology (Conventional, PEGylated, Ligand-Targeted, Stimuli-Responsive), By Application (Oncology, Fungal Infections, Pain Management) Region, Key Players – Dynamics, Lipid Nanoparticles, Advanced Nanomedicine & Bioavailability Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 6.08 Billion | USD 13.12 Billion | 8.9% | North America, 41.0% |

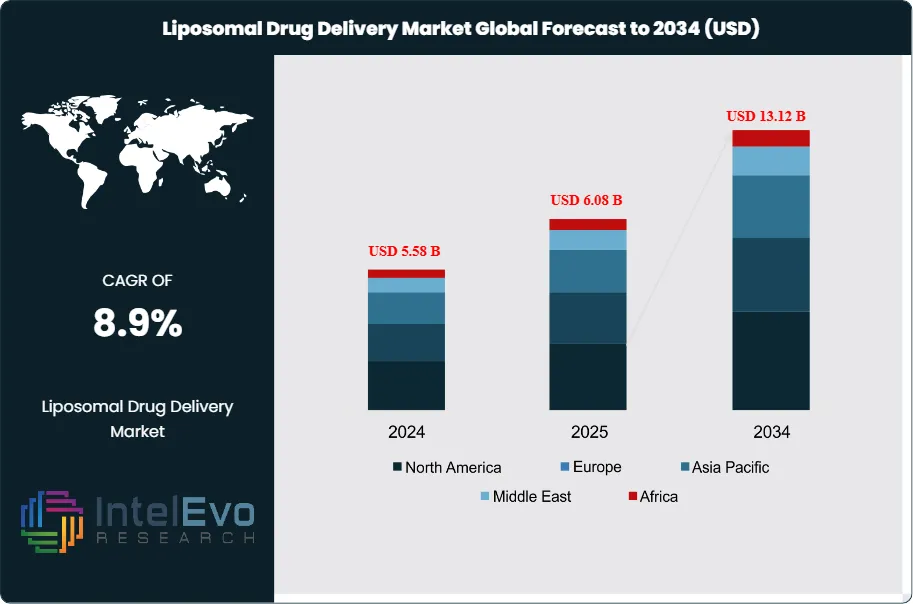

The Liposomal Drug Delivery Market was valued at approximately USD 5.58 billion in 2024 and reached USD 6.08 billion in 2025. The market is projected to grow to USD 13.12 billion by 2034, expanding at a CAGR of 8.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.04 billion over the analysis period, driven by the expanding adoption of liposomal formulations across oncology, infectious disease management, and pain control applications, alongside structural advantages that make lipid-bilayer vesicle encapsulation the reference standard for delivering drugs with unfavorable systemic toxicity profiles or poor aqueous solubility.

Get More Information about this report -

Request Free Sample ReportLiposomes are spherical vesicles composed of phospholipid bilayers measuring 50–300 nanometers in diameter that encapsulate both hydrophilic and hydrophobic active pharmaceutical ingredients. Their unique structural duality—an aqueous core surrounded by lipid bilayer shells—allows simultaneous encapsulation of water-soluble drugs in the core and lipophilic drugs within the membrane, making liposomes the only approved nanocarrier platform capable of delivering both drug classes within a single particle. Since the FDA approved Doxil (PEGylated liposomal doxorubicin) in 1995 as the first liposomal product—initially for Kaposi's sarcoma in AIDS patients—the platform has expanded to encompass over 68 globally approved liposomal formulations spanning antifungal agents, anthracycline chemotherapeutics, local anesthetics, corticosteroids, and cytarabine combinations. In February 2024, Ipsen's Onivyde (irinotecan liposome injection) received FDA approval for first-line treatment of metastatic pancreatic adenocarcinoma as part of the NALIRIFOX regimen—the most recent landmark approval in the sector, expanding Onivyde's addressable patient population from second-line-only to the considerably larger first-line metastatic setting.

Rising global cancer incidence is the market's primary structural demand driver. The American Cancer Society projected approximately 22,010 new acute myeloid leukemia (AML) cases in the U.S. alone in 2025, alongside rising breast, ovarian, and pancreatic cancer diagnoses that collectively expand the eligible patient pool for liposomal oncology products. Liposomal doxorubicin reduces the cardiotoxicity that limits conventional doxorubicin use by reducing peak plasma concentrations through sustained encapsulated release—a pharmacokinetic advantage that translates directly to higher lifetime cumulative doses tolerable by patients and broader treatment applicability across cardiac-compromised cancer populations. Beyond oncology, liposomal bupivacaine (EXPAREL, Pacira BioSciences) has established a distinct commercial franchise in non-opioid post-surgical pain management, driven by growing regulatory and policy pressure to reduce opioid prescribing in the United States. EXPAREL received a new product-specific J-Code effective January 1, 2025, enhancing reimbursement clarity and billing efficiency for hospital and outpatient surgical center users.

Manufacturing technology is advancing in parallel with the commercial franchise expansions. Continuous-flow microfluidic reactors have increased throughput by 35% year-over-year in pilot facilities, reducing formulation development timelines by 22% relative to traditional batch extrusion methods. PEGylation remains the dominant surface modification technology, accounting for 61.23% of liposomal drug delivery revenue in 2024 by enabling extended circulation half-lives through reduced mononuclear phagocyte system uptake. Concurrently, cubosome-based lipid nanoparticle formats—which offer up to 8-fold higher cellular uptake and improved endosomal escape relative to conventional liposomes—are growing at a 10.88% CAGR as next-generation vehicles for gene therapy and mRNA delivery applications validated at commercial scale through COVID-19 mRNA vaccine manufacturing experience.

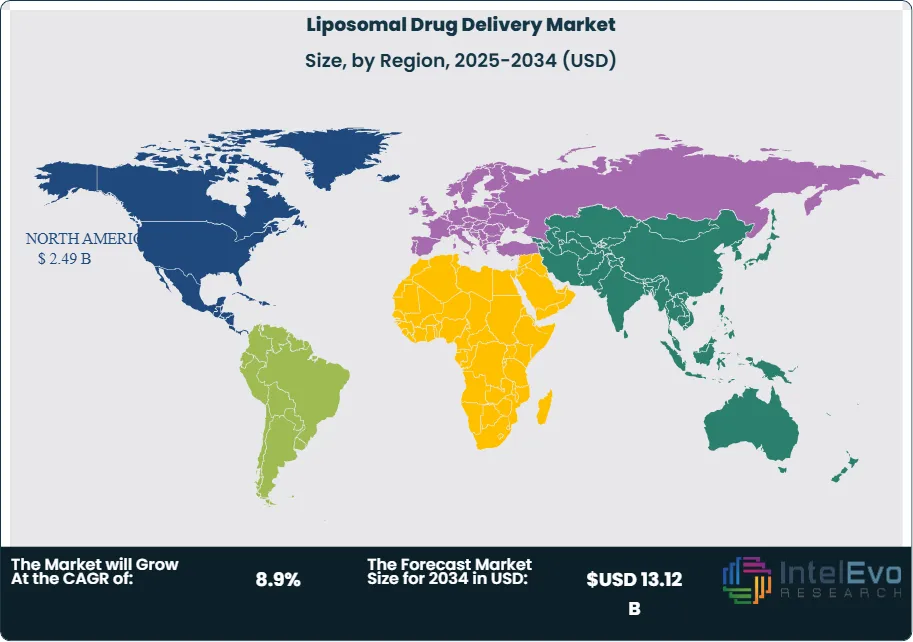

North America dominated the liposomal drug delivery market in 2025 with a 41.0% revenue share valued at approximately USD 2.49 billion, anchored by the United States' robust oncology reimbursement framework, high chronic disease burden, and the presence of Gilead Sciences, Pacira BioSciences, Jazz Pharmaceuticals, and Ipsen's U.S. operations as primary commercial participants. Asia Pacific is the fastest-growing region at an 11.03% CAGR through 2030, driven by rising cancer incidence in China and India, increasing healthcare infrastructure investment, and cost-efficient generic liposomal manufacturing concentrated in Indian and Chinese pharmaceutical manufacturers including Lupin Limited and Sun Pharmaceutical Industries.

Market Definition & Scope

The liposomal drug delivery market is defined as the commercial market for pharmaceutical products formulated using lipid-bilayer vesicle encapsulation technology, in which active pharmaceutical ingredients are entrapped within phospholipid membranes to achieve targeted delivery, controlled release, reduced systemic toxicity, or improved pharmacokinetic profiles relative to conventional free-drug formulations. The market encompasses prescription-grade liposomal drug products across all approved indications, including PEGylated stealth liposomes (such as Doxil/Caelyx and Onivyde), non-PEGylated conventional liposomes (such as the non-PEGylated liposomal doxorubicin Myocet), multivesicular DepoFoam liposomes (such as EXPAREL), lysolipid thermally sensitive liposomes (LTSLs) in clinical development for thermoablation-combined delivery, and immunoliposomes incorporating targeting ligands. Covered drug classes include liposomal anthracyclines (doxorubicin, daunorubicin, vincristine), liposomal antifungals (amphotericin B), liposomal local anesthetics (bupivacaine), liposomal topoisomerase inhibitors (irinotecan), and combination liposomal formulations (Vyxeos containing daunorubicin and cytarabine at a 5:1 molar ratio).

This analysis covers all commercially approved liposomal pharmaceutical products globally, as well as late-stage pipeline candidates in Phase 2 or Phase 3 clinical development and approved generic liposomal formulations. Explicitly excluded are lipid nanoparticles (LNPs) used exclusively for mRNA delivery without lipid bilayer vesicle architecture (such as Onpattro's LNP for siRNA delivery or COVID-19 mRNA vaccine LNPs), lipid complexes that are not classified as liposomes by regulatory agencies including Abelcet and Amphotec (which are lipid complexes, not liposomes), cosmetic lipid carriers, and liposomes used in research-use-only applications without therapeutic intent. The liposomal drug delivery market represents a distinct and established sub-category of the broader nanomedicine and drug delivery platform market, which encompasses liposomes alongside polymeric nanoparticles, dendrimers, solid lipid nanoparticles, and inorganic nanoparticles.

, By Technology (Conventional, PEGylated, Ligand-Targeted, Stimuli-Responsive), By Application (Oncology, Fungal Infections, Pain Management) Region, Key Players – Dynamics, Lipid Nanoparticles, Advanced Nanomedicine & Bioavailability Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global liposomal drug delivery market grew from approximately USD 3.98 billion in 2019 to USD 6.08 billion in 2025 and is forecast to reach USD 13.12 billion by 2034, a 8.9% CAGR over the 2025–2034 period, generating an absolute dollar opportunity of USD 7.04 billion as generic entry, label expansions, and new indication approvals collectively expand commercial volume.

- Segment Dominance (Product): Liposomal doxorubicin held the largest product segment share at 36.0–41.3% in 2024, generating approximately USD 2.2–2.5 billion, because doxorubicin remains the world's most widely used anthracycline chemotherapy agent across breast cancer, ovarian cancer, multiple myeloma, and hematological malignancies—and its liposomal formulation's cardiotoxicity reduction is clinically essential.

- Segment Dominance (Application): Cancer therapy accounted for 49.4–54.0% of the liposomal drug delivery market in 2024 at approximately USD 2.9–3.2 billion, reflecting liposomes' unique capacity to reduce dose-dependent chemotherapy toxicity while maintaining or improving antitumor efficacy through altered biodistribution.

- Driver: The global cancer burden continues to expand—with the World Health Organization projecting 20 million new cancer cases annually by 2030—creating a structurally growing patient pool for liposomal oncology products including Doxil/Caelyx, Onivyde, Vyxeos, Marquibo, and their authorized generics, all of which command premium pricing over conventional drug equivalents.

- Restraint: The high cost of liposomal drug formulation development—estimated at USD 100–200 million per novel liposomal product through Phase 3 including the 20–30 tightly controlled manufacturing process steps—combined with the formulation complexity of achieving consistent particle size distribution (target median 80–120 nm) and encapsulation efficiency above 90%, limits the rate of new branded product entry.

- Opportunity: Generic liposomal doxorubicin entry is accelerating market volume while reducing per-unit prices; Lupin Limited's August 2024 U.S. launch of doxorubicin liposome single-dose vials (Doxorubicin Hydrochloride Liposome Injection) following ANDA approval, and Alembic Pharmaceuticals' June 2025 FDA approval for the same formulation, collectively increase patient access and formulary inclusion rates in hospital systems that previously restricted prescribing to brand-name-only Doxil due to cost.

- Trend: AI-assisted formulation optimization is reducing liposomal drug development timelines by enabling computational selection of lipid composition ratios, PEG chain length, and drug-to-lipid ratios that minimize batch variability, with 63% of lipid nanoparticle batches achieving particle diameters within 10 nm of target in 2025 compared to wider distributions in earlier manufacturing generations.

- Regional: North America led with a 41.0% market share in 2025 valued at approximately USD 2.49 billion, driven by the United States' FDA-approved portfolio of more than 20 liposomal drug products, robust oncology reimbursement through Medicare Part B and D, and Pacira BioSciences' EXPAREL commanding approximately USD 3.15 billion in cumulative sales through 2024 as the leading non-opioid post-surgical pain management liposomal product.

Key Insights Summary

- On February 13, 2024, the FDA expanded the Onivyde (irinotecan liposome injection) indication from second-line gemcitabine-refractory metastatic pancreatic adenocarcinoma to first-line treatment in combination with oxaliplatin, fluorouracil, and leucovorin (the NALIRIFOX regimen), based on the Phase 3 NAPOLI 3 trial (NCT04083235) enrolling 770 patients; the first-line approval triggered a USD 225 million milestone payment from Ipsen to Merrimack Pharmaceuticals and supports Ipsen's projection of EUR 265 million in Onivyde sales for 2025 versus EUR 164 million in 2023.

- In August 2024, Lupin Limited, in partnership with ForDoz Pharma Corporation, introduced Doxorubicin Hydrochloride Liposome Injection 20 mg/10 mL and 50 mg/25 mL single-dose vials in the U.S. market following FDA ANDA approval—expanding generic liposomal doxorubicin access for cancer patients and increasing price competition for Johnson & Johnson's branded Doxil franchise; Alembic Pharmaceuticals subsequently received a separate FDA approval for the same formulation in June 2025.

- Pacira BioSciences received a new product-specific J-Code (Healthcare Common Procedure Coding System code) for EXPAREL (bupivacaine liposome injectable suspension) effective January 1, 2025, enabling more precise reimbursement tracking in hospital and ambulatory settings and reducing the administrative barriers that had previously caused some facilities to underutilize or mis-bill the product; real-world data presented at the Orthopaedic Research Society 2026 Annual Meeting in March 2026 demonstrated EXPAREL's association with lower total cost of care versus ropivacaine and standard non-liposomal bupivacaine in total knee arthroplasty and spinal fusion.

- In February 2025, Innocan Pharma Corporation received an Indian patent covering its LPT-CBD (liposomal prolonged-release cannabidiol) formulation for chronic pain management, validated by a positive FDA pre-IND meeting that confirmed regulatory acceptability of the liposomal cannabinoid delivery approach for the U.S. clinical development pathway—establishing liposomal cannabinoid delivery as a clinically viable segment within the broader pain management pipeline.

- PEGylated stealth liposome technology commanded 61.23% of the liposomal drug delivery market in 2024 by enabling three-to-five-fold longer plasma circulation times versus non-PEGylated equivalents through reduced reticuloendothelial system uptake, a property that underpins the enhanced permeability and retention (EPR) effect exploited by Doxil, Onivyde, and other tumor-targeted liposomal oncologics; however, clinicians are increasingly monitoring hypersensitivity reaction cases and manufacturers are evaluating ganglioside and zwitterionic coating alternatives that reduce complement activation.

- A 2025 review published in Pharmaceutics (Sobol et al., doi: 10.3390/pharmaceutics17070885, July 5, 2025) confirmed that liposomal formulations reduce dose-limiting cardiotoxicity from anthracycline chemotherapy agents by altering biodistribution to decrease myocardial drug exposure—the primary pharmacological rationale supporting the sustained clinical preference for liposomal doxorubicin over conventional doxorubicin in cardiac-compromised oncology patients with breast cancer, ovarian cancer, and multiple myeloma.

Competitive Landscape Overview

The liposomal drug delivery market is moderately consolidated, with the top five manufacturers—Gilead Sciences, Pacira BioSciences, Johnson & Johnson (Janssen), Sun Pharmaceutical Industries, and Luye Pharma Group—collectively holding approximately 60% of total market revenue in 2025. Competitive differentiation occurs across four primary dimensions: proprietary platform technology (PEGylation chemistry, DepoFoam multivesicular architecture, or surface ligand targeting), drug-disease combination specificity (exclusive oncology indication approvals), geographic commercial coverage, and the growing generic liposomal doxorubicin market where Indian and Chinese manufacturers are competing primarily on cost efficiency.

The competitive landscape is bifurcating between innovative branded liposomal products pursuing new indications or combination regimens—exemplified by Onivyde's first-line NALIRIFOX approval in pancreatic cancer and Jazz Pharmaceuticals' Vyxeos pediatric label extension—and a rapidly expanding generic liposomal oncology segment in which FDA ANDA approvals for liposomal doxorubicin are enabling Indian manufacturers including Lupin Limited, Alembic Pharmaceuticals, Sun Pharmaceutical, and Zydus Cadila to compete in the USD 2+ billion annual U.S. liposomal doxorubicin market. The entry of multiple generic manufacturers has reduced brand-name Doxil's market share but expanded the total patient access to liposomal anthracycline therapy, growing overall volume while compressing average selling prices. In January 2024, CHEPLAPHARM Group acquired European commercial rights for Myocet (liposomal doxorubicin, non-PEGylated formulation) from Teva, consolidating European distribution of a clinically meaningful differentiated product—non-PEGylated formulation reduces the pseudo-allergic infusion reactions associated with PEGylated liposomes while maintaining the biodistribution advantage over conventional doxorubicin.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product(s) | Geo Strength | Recent Strategic Move |

| Gilead Sciences, Inc. | USA | Leader | AmBisome® (liposomal amphotericin B); developing long-acting lenacapavir liposomal formulations for HIV | Global | Advancing lenacapavir long-acting injectable liposome for HIV pre-exposure prophylaxis; AmBisome remains standard of care for invasive fungal infections globally |

| Pacira BioSciences, Inc. | USA | Leader | EXPAREL® (bupivacaine liposome DepoFoam); ZILRETTA® (triamcinolone acetonide); PCRX-201 pipeline | N. America | New product-specific J-Code for EXPAREL effective January 1, 2025; joined PROBE Consortium for osteoarthritis research, December 2025 |

| Ipsen Biopharmaceuticals, Inc. | France/USA | Leader | Onivyde® (irinotecan liposome injection) for metastatic pancreatic adenocarcinoma | Global | FDA expanded Onivyde to first-line mPDAC (NALIRIFOX regimen), February 13, 2024; 2025 Onivyde revenue projected at EUR 265 million |

| Jazz Pharmaceuticals plc | Ireland/USA | Challenger | Vyxeos® Liposomal (daunorubicin + cytarabine) for AML with myelodysplasia-related changes | N. America, Europe | Completed observational study on Vyxeos Liposomal in AML treatment, December 2025; pediatric label addition covering patients aged 1 year and older |

| Johnson & Johnson (Janssen) | USA | Challenger | Doxil®/Caelyx® (PEGylated liposomal doxorubicin) for Kaposi’s sarcoma, ovarian cancer, multiple myeloma | Global | Continued Doxil branded and authorized generic maintenance; acquired Ambrx Biopharma to bolster oncology ADC and delivery portfolio, January 2024 |

| Sun Pharmaceutical Industries Ltd. | India | Challenger | Liposomal oncology products including doxorubicin formulations for cancer therapy | Global (emphasis Asia, emerging) | Expanding liposomal oncology portfolio through strategic partnerships; strengthening emerging-market distribution infrastructure, 2024–2025 |

| Lupin Limited | India | Niche Player | Doxorubicin Hydrochloride Liposome Injection (generic Doxil) via ForDoz partnership | N. America | Launched doxorubicin liposome single-dose vials in U.S. market after ForDoz ANDA approval, August 2024; Alembic Pharmaceuticals separately received FDA approval June 2025 |

| Taiwan Liposome Company, Ltd. (TLC) | Taiwan | Niche Player | TLC599 (liposomal dexamethasone for knee OA), TLC178 (liposomal vinorelbine for cancer) | Asia Pacific, N. America | TLC599 advancing in Phase 3 for knee osteoarthritis; partnership with Endo Ventures Limited for U.S. commercialization maintained |

By Product

Liposomal doxorubicin held the largest product segment share at approximately 36.0–41.3% of the liposomal drug delivery market in 2024, generating approximately USD 2.2–2.5 billion in revenue, making it the most commercially significant single liposomal drug product globally. The product's dominance reflects doxorubicin's position as the anchor chemotherapy agent across the three largest liposomal oncology indications: metastatic breast cancer, advanced ovarian cancer, and multiple myeloma. The critical commercial driver is cardiotoxicity reduction: conventional doxorubicin causes irreversible dilated cardiomyopathy at cumulative doses above 400–550 mg/m², while PEGylated liposomal doxorubicin (Doxil/Caelyx) enables higher cumulative lifetime doses by reducing peak plasma concentrations, allowing treatment continuation for patients who would otherwise be forced to discontinue anthracycline therapy due to cardiac risk. Johnson & Johnson's Doxil/Caelyx maintains the dominant branded position, while authorized generics from Zydus Cadila, Sun Pharmaceutical, and now Lupin Limited (August 2024) and Alembic Pharmaceuticals (June 2025) collectively expand the addressable patient base through reduced acquisition cost.

Liposomal amphotericin B (AmBisome, Gilead Sciences) is the second-largest product, addressing the USD 800 million–USD 1 billion fungal infection management segment where it serves as the standard of care for invasive aspergillosis, cryptococcal meningitis, and visceral leishmaniasis in immunocompromised patients. AmBisome reduces the nephrotoxicity that limits conventional amphotericin B deoxycholate use, enabling therapeutic dosing in renal-impaired patients including bone marrow transplant recipients and AIDS patients who constitute the primary at-risk population. Liposomal paclitaxel represents the third major product class, addressing taxane-resistant or hypersensitivity-prone patient populations in breast, lung, and ovarian cancer where the liposomal formulation eliminates the need for the Cremophor EL solvent that causes hypersensitivity reactions in up to 10% of patients receiving conventional paclitaxel. The “others” category encompasses Onivyde (liposomal irinotecan), Vyxeos (liposomal daunorubicin + cytarabine), Marquibo (liposomal vincristine sulfate), DepoCyt (liposomal cytarabine), and EXPAREL (liposomal bupivacaine), each addressing distinct clinical niches with limited substitutability.

By Technology

PEGylated stealth liposome technology held a 43.0–61.2% revenue share in 2024, remaining the commercial workhorse for large-volume oncology liposomal brands. PEGylation—the covalent attachment of polyethylene glycol chains to the liposome surface—creates a hydrophilic steric barrier that inhibits opsonization by plasma proteins and subsequent recognition and clearance by the mononuclear phagocyte system, extending plasma half-life from 2–5 hours for conventional liposomes to 45–55 hours for PEGylated equivalents. This extended circulation enables the EPR effect to drive preferential accumulation in tumor tissue with leaky vasculature and poor lymphatic drainage, achieving 4–8 times higher tumor drug concentrations versus free drug. However, the growing clinical literature on PEG-related hypersensitivity reactions (termed complement activation-related pseudoallergy, CARPA) is stimulating R&D investment in PEG-free alternatives including ganglioside coatings, zwitterionic phosphatidylcholines, and HPMA (hydroxypropylmethacrylamide) polymer conjugates.

Non-PEGylated conventional liposomes represent approximately 30–35% of market revenue, serving clinical situations where standard-rate phagocytic clearance is acceptable or where PEG hypersensitivity risk outweighs the benefit of extended circulation. Myocet (non-PEGylated liposomal doxorubicin) demonstrates an intermediate cardiotoxicity profile between conventional doxorubicin and PEGylated Doxil, providing a clinically useful formulation option for European breast cancer patients managed under national formularies that prefer the non-PEGylated option. DepoFoam multivesicular liposome technology, exclusively deployed by Pacira BioSciences, is a structurally distinct format: instead of a single lipid bilayer, DepoFoam particles contain multiple non-concentric aqueous chambers separated by lipid bilayer membranes, enabling sustained drug release over 72–96 hours from a single injection. EXPAREL's DepoFoam structure provides 72-hour bupivacaine release from a single peri-surgical injection, reducing or eliminating the need for opioid analgesics during the critical 72-hour post-surgical pain window where opioid dependence risk is highest. Lysolipid thermally sensitive liposomes (LTSLs) remain in late-stage clinical investigation for use in combination with regional hyperthermia or thermoablation procedures, releasing drug payloads specifically within tumor tissue heated to 39–42°C—a targeted release mechanism that could enable complete separation of systemic drug exposure from tumor drug exposure.

By Application

Cancer therapy dominated the liposomal drug delivery market with a 49.4–54.0% application share in 2024 at approximately USD 2.9–3.2 billion, because the pharmacological imperative of reducing dose-limiting chemotherapy toxicity while maintaining antitumor efficacy aligns perfectly with liposomes' altered biodistribution capabilities. The oncology pipeline encompasses both approved commercial products and a late-stage clinical portfolio of new liposomal oncology formulations: more than 30 lipid-based platforms were evaluated across late-stage clinical trials for cancer and rare diseases as of 2025. Combination liposomal products represent a particularly innovative segment, with Vyxeos—which entraps daunorubicin and cytarabine at a fixed 5:1 molar ratio inside the same liposome to achieve synergistic cell kill—demonstrating the concept of pharmacologically optimized co-delivery that no oral or free-drug combination can replicate at the cellular level. Ligand-conjugated immunoliposomes with affinity moieties targeting cancer-specific surface antigens reached 24% of liposomal oncology clinical trials in 2025, up from 11% in 2020, reflecting the maturation of the active targeting concept from laboratory proof-of-concept to clinical feasibility.

Fungal infection management represents the second-largest application, driven by AmBisome's entrenched standard-of-care position in invasive fungal infections among immunocompromised patients. The indication benefits from the growing population of hematopoietic stem cell transplant recipients, solid organ transplant patients, and AIDS patients on advanced therapies who face persistent aspergillosis and cryptococcal meningitis risk. Pain management is the third application—and the fastest growing in terms of new indication approvals—with EXPAREL dominating through its DepoFoam platform and benefiting from U.S. healthcare policy supporting opioid prescribing reduction. Real-world data from March 2026 presented by Pacira BioSciences at the Orthopaedic Research Society Annual Meeting demonstrated lower total cost of care with EXPAREL versus standard-of-care alternatives in both total knee arthroplasty and spinal fusion—a health economic argument that aligns hospital cost-containment incentives with clinical adoption. Viral vaccines represent the market's fastest-growing application segment at an 11.42% CAGR through 2030, as lipid nanoparticle technology validated by COVID-19 mRNA vaccine manufacturing now enables rapid development of lipid-formulated vaccines for influenza, RSV, and emerging pathogens.

Regional Analysis

North America held the largest regional share of the liposomal drug delivery market in 2025 at 41.0%, generating approximately USD 2.49 billion, with the United States contributing over 90% of regional revenue. The U.S. market benefits from FDA's established regulatory pathway for liposomal drug approval through the 505(b)(1) and 505(b)(2) pathways for new molecular entity and hybrid liposomal applications respectively, and through the ANDA pathway for generic liposomal doxorubicin formulations. The Centers for Medicare and Medicaid Services (CMS) covers liposomal oncology agents under Medicare Part B (physician-administered) and Medicare Part D (self-administered) depending on route, with relatively favorable reimbursement rates that support branded liposomal product adoption. The policy imperative to reduce opioid prescribing, reinforced by the CDC's Clinical Practice Guideline for Prescribing Opioids (2022) and CMS surgical payment bundling models, creates a systemic commercial tailwind for EXPAREL in elective orthopaedic and general surgical procedures. North America is projected to maintain a CAGR of approximately 8.5% through 2034.

Europe held approximately 28.0% of market revenue in 2025 at approximately USD 1.70 billion, with Germany, France, the United Kingdom, and Italy as the primary demand centers. European Medicines Agency (EMA) guidelines on the quality and equivalence of liposomal drug products (EMA/CHMP/806058/2009) and the Committee for Medicinal Products for Human Use (CHMP) reflection papers on nanomedicine define the regulatory pathway for liposomal product authorization, requiring detailed physicochemical characterization of particle size distribution, zeta potential, encapsulation efficiency, and in vitro drug release profiles. CHEPLAPHARM Group's January 2024 acquisition of European commercial rights for Myocet from Teva expanded the availability of non-PEGylated liposomal doxorubicin for breast cancer patients across EU member states, representing the period's most significant European liposomal product rights transaction. Europe's stringent quality standards and the EMA's guidance on nanotechnology in drug products have also driven investment in European liposomal manufacturing capacity, particularly in Germany, Belgium, and the Netherlands.

Asia Pacific contributed approximately 20.0% of market revenue in 2025 at approximately USD 1.22 billion and is the fastest-growing region at a CAGR of 11.03% through 2030. Rising cancer incidence—China reports over 4.8 million new cancer cases annually and India over 1.4 million—creates expanding patient volumes for liposomal oncology products. India's domestic pharmaceutical industry dominates generic liposomal doxorubicin manufacturing: Lupin Limited's 2024 U.S. ANDA approval and Alembic Pharmaceuticals' 2025 approval both reflect Indian manufacturers' technical capabilities in liposomal formulation that increasingly serve global markets through U.S., European, and Asian distribution. Japan's Pharmaceuticals and Medical Devices Agency (PMDA) regulates liposomal products under the Act on Securing Quality, Efficacy and Safety of Products Including Pharmaceuticals and Medical Devices, with AmBisome and Doxil both holding Japan approvals. South Korea and Taiwan are developing emerging liposomal manufacturing and clinical research capabilities, with Taiwan Liposome Company advancing TLC599 in Phase 3 clinical trials for knee osteoarthritis—an indication that could open a substantial new liposomal therapeutic application if clinical data supports approval.

Latin America and the Middle East & Africa together contributed approximately 11.0% of market revenue in 2025. Brazil and Mexico lead Latin American demand, primarily through public health system procurement of generic liposomal amphotericin B for visceral leishmaniasis treatment under national disease control programs. Saudi Arabia and the UAE drive Middle Eastern demand through advanced oncology center procurement and medical tourism infrastructure that imports branded liposomal products including Doxil and Onivyde at prices reflective of relatively limited generic competition in the Gulf Cooperation Council pharmaceutical market.

Country Analysis

The United States liposomal drug delivery market reached approximately USD 2.22 billion in 2025, growing at a country CAGR of approximately 9.1% through 2034. The U.S. market's breadth is defined by the diversity of its approved liposomal product portfolio: Doxil and its generics, AmBisome, Onivyde and NALIRIFOX, Vyxeos, EXPAREL, Marquibo (liposomal vincristine for Philadelphia chromosome-negative relapsed or refractory ALL), DepoCyt (liposomal cytarabine for lymphomatous meningitis), and Mepact (liposomal mifamurtide, available through expanded access). FDA's Draft Guidance on Liposome Drug Products (2018) and subsequent technical guidelines on chemistry, manufacturing, and controls (CMC) for liposomal drugs define a clear technical submission pathway, with detailed particle size, zeta potential, encapsulation efficiency, and in vitro drug release requirements that collectively protect innovative product developers through the complexity of the regulatory approval process while establishing a high technical bar for generic applicants. The Hatch-Waxman Act's 505(j) ANDA pathway for generic liposomal products requires demonstration of pharmaceutical equivalence through comparative physicochemical characterization and bioequivalence studies, with the FDA's Product Quality Research Institute (PQRI) actively developing standardized dissolution test methods for liposomal products.

Germany's liposomal drug delivery market reached approximately USD 218 million in 2025, growing at an estimated 7.8% CAGR, reflecting the country's position as Western Europe's largest pharmaceutical market and the location of significant liposomal manufacturing infrastructure including facilities operated by CordenPharma and other contract manufacturers serving European and global clients. German hospital procurement for liposomal oncology products is governed by the Social Code Book V (SGB V) and the early benefit assessment (Nutzenbewertung) process under the Pharmaceutical Market Restructuring Act (AMNOG), which determines whether a new drug receives additional benefit designation—a classification that directly affects negotiated reimbursement prices. Liposomal formulations of established drugs (Doxil, Myocet) benefit from comparative effectiveness evidence demonstrating toxicity reduction, which generally supports additional benefit designation in cardiac-compromised patient sub-populations. Japan's liposomal drug delivery market was valued at approximately USD 195 million in 2025, growing at an estimated 8.5% CAGR, with AmBisome and Doxil as the primary commercial products and a pipeline including Taiwan Liposome Company's TLC178 (liposomal vinorelbine) in Japanese clinical evaluation for non-small cell lung cancer.

India's liposomal drug delivery market reached approximately USD 148 million in 2025, growing at an estimated 12.5% CAGR—one of the highest country-level growth rates in the market. India's role is dual: it is simultaneously a significant domestic consumption market for generic liposomal oncology products and the world's leading manufacturing source for exported generic liposomal doxorubicin destined for U.S. and European markets. The Indian government's Department of Pharmaceuticals has designated nanotechnology-based drug delivery as a priority area under the National Pharmaceutical Policy, and the Department of Biotechnology funds university-industry partnerships developing next-generation liposomal formulations for tropical infectious diseases including visceral leishmaniasis (kala-azar) prevalent in Bihar, Jharkhand, and West Bengal—where liposomal amphotericin B is the primary treatment under the National Vector Borne Disease Control Programme. China's liposomal drug delivery market reached approximately USD 244 million in 2025, with several domestically developed liposomal products competing alongside international brands including CSPC Pharmaceutical's liposomal doxorubicin and Shanghai Fudan-Zhangjiang Bio-Pharmaceutical's liposomal daunorubicin, positioning China as the most commercially developed non-U.S. single country market for locally manufactured liposomal oncology drugs.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product

- Liposomal Doxorubicin

- Liposomal Amphotericin B

- Liposomal Paclitaxel

- Others

By Technology

- Conventional Liposomes

- PEGylated Liposomes

- Ligand-Targeted Liposomes

- Stimuli-Responsive Liposomes

By Application

- Oncology

- Fungal Infections

- Pain Management

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.08 B |

| Forecast Revenue (2034) | USD 13.12 B |

| CAGR (2025-2034) | 8.9% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product, (Liposomal Doxorubicin, Liposomal Amphotericin B, Liposomal Paclitaxel, Others), By Technology, (Conventional Liposomes, PEGylated Liposomes, Ligand-Targeted Liposomes, Stimuli-Responsive Liposomes), By Application, (Oncology, Fungal Infections, Pain Management, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | GILEAD SCIENCES, INC., PACIRA BIOSCIENCES, INC., IPSEN BIOPHARMACEUTICALS, INC., JAZZ PHARMACEUTICALS PLC, JOHNSON & JOHNSON (JANSSEN PHARMACEUTICALS, INC.), SUN PHARMACEUTICAL INDUSTRIES LTD., LUYE PHARMA GROUP, ACROTECH BIOPHARMA INC., TAIWAN LIPOSOME COMPANY, LTD., SPECTRUM PHARMACEUTICALS, INC., TAKEDA PHARMACEUTICAL COMPANY LIMITED, TEVA PHARMACEUTICAL INDUSTRIES LTD., LUPIN LIMITED, NOVARTIS AG, CELSION CORPORATION, CHEPLAPHARM ARZNEIMITTEL GMBH, FUJIFILM TOYAMA CHEMICAL CO., LTD., SHANGHAI FUDAN-ZHANGJIANG BIO-PHARMACEUTICAL CO., LTD., INNOCAN PHARMA CORPORATION, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Technology (Conventional, PEGylated, Ligand-Targeted, Stimuli-Responsive), By Application (Oncology, Fungal Infections, Pain Management) Region, Key Players – Dynamics, Lipid Nanoparticles, Advanced Nanomedicine & Bioavailability Trends & Forecast 2026-2034")

, By Technology (Conventional, PEGylated, Ligand-Targeted, Stimuli-Responsive), By Application (Oncology, Fungal Infections, Pain Management) Region, Key Players – Dynamics, Lipid Nanoparticles, Advanced Nanomedicine & Bioavailability Trends & Forecast 2026-2034")

, By Technology (Conventional, PEGylated, Ligand-Targeted, Stimuli-Responsive), By Application (Oncology, Fungal Infections, Pain Management) Region, Key Players – Dynamics, Lipid Nanoparticles, Advanced Nanomedicine & Bioavailability Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Liposomal Drug Delivery Market?

Global Liposomal Drug Delivery Market was valued at USD 5.58 billion in 2024 and is projected to reach USD 13.12 billion by 2034, at a CAGR of 8.9% during 2026–2034.

Who are the major players in the Liposomal Drug Delivery Market?

GILEAD SCIENCES, INC., PACIRA BIOSCIENCES, INC., IPSEN BIOPHARMACEUTICALS, INC., JAZZ PHARMACEUTICALS PLC, JOHNSON & JOHNSON (JANSSEN PHARMACEUTICALS, INC.), SUN PHARMACEUTICAL INDUSTRIES LTD., LUYE PHARMA GROUP, ACROTECH BIOPHARMA INC., TAIWAN LIPOSOME COMPANY, LTD., SPECTRUM PHARMACEUTICALS, INC., TAKEDA PHARMACEUTICAL COMPANY LIMITED, TEVA PHARMACEUTICAL INDUSTRIES LTD., LUPIN LIMITED, NOVARTIS AG, CELSION CORPORATION, CHEPLAPHARM ARZNEIMITTEL GMBH, FUJIFILM TOYAMA CHEMICAL CO., LTD., SHANGHAI FUDAN-ZHANGJIANG BIO-PHARMACEUTICAL CO., LTD., INNOCAN PHARMA CORPORATION, OTHERS

Which segments covered the Liposomal Drug Delivery Market?

By Product, (Liposomal Doxorubicin, Liposomal Amphotericin B, Liposomal Paclitaxel, Others), By Technology, (Conventional Liposomes, PEGylated Liposomes, Ligand-Targeted Liposomes, Stimuli-Responsive Liposomes), By Application, (Oncology, Fungal Infections, Pain Management, Others)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Liposomal Drug Delivery Market

Published Date : 18 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date