- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Livestock Wearable Sensor Market Size, Share | CAGR of 12.0%

Global Livestock Wearable Sensor Market Size, Share, Analysis By Product (RFID Tags, GPS Tracking, Health & Activity Monitoring, Smart Collars), By Animal (Cattle, Poultry, Swine, Sheep & Goats), By Application (Health Monitoring, Behavior, Reproduction, Location, Feeding Management), By End-User Region, Key Players – Dynamics, Precision Livestock Farming (PLF) & AgTech IoT Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 2.18 Billion | USD 6.04 Billion | 12.0% | North America, 36.2% |

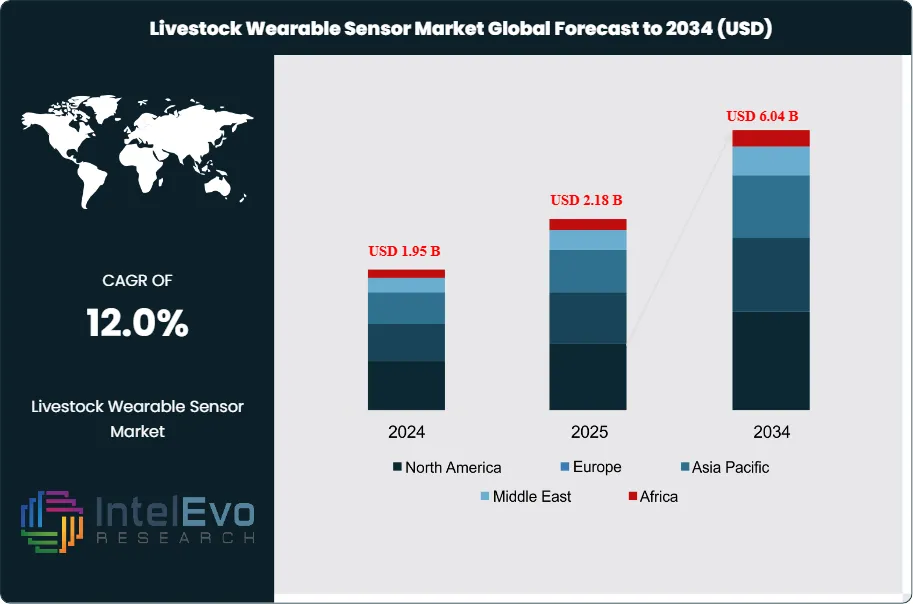

The Livestock Wearable Sensor Market was valued at USD 1.95 Billion in 2024 and is estimated to reach USD 2.18 Billion in 2025. The market is projected to grow to USD 6.04 Billion by 2034, expanding at a CAGR of 12.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.86 Billion over the analysis period, equivalent to roughly 2.8 times the 2025 base value. Adoption is concentrating around four product families: smart collars, smart ear tags, rumen boluses, and leg-mounted activity bands, each tied to distinct husbandry workflows in dairy, beef, swine, and poultry operations.

Get More Information about this report -

Request Free Sample ReportDemand is driven by precision livestock farming economics that link continuous behavioral data to measurable production gains. Field studies cited by Connecterra B.V. and CowManager B.V. show estrus detection sensitivity above 92% and lameness alerts three to five days before clinical signs, translating into conception-rate improvements above 15% and avoided losses around USD 370 per affected dairy cow. With the average dairy cow generating an estimated USD 15,000 in lifetime gross revenue, even single-digit gains in detection accuracy justify per-head sensor spend, which is why penetration is climbing fastest on commercial herds above 200 animals.

Regulatory tailwinds are accelerating shipments of electronic ear tags. The U.S. Department of Agriculture's APHIS rule on electronic identification, which became enforceable on November 5, 2024, requires interstate-moved dairy cattle and sexually intact beef cattle 18 months and older to carry visually and electronically readable 840 EID tags. The European Union's mandatory electronic identification framework for cattle, sheep, and goats remains in force across all 27 member states, while the United Kingdom's Livestock Information Service is rolling out a multi-species traceability backbone through 2026. These mandates create installed-base anchors that wearable health-sensor vendors are layering onto.

Technology shifts are widening the addressable market. Halter's solar-powered virtual-fencing collar passed 1 million units sold by March 2026, and the company's satellite-connected version removes the on-farm tower dependency that previously locked out remote ranches. SmaXtec animal care GmbH has extended bolus service life beyond 6 years and added a progesterone biosensor module, opening continuous reproductive endocrine monitoring as a new product category. AI-driven baseline learning, demonstrated commercially by Ori Cattle's pilot tag in early 2026, is pushing per-animal alert accuracy higher while collapsing the cost structure relative to subscription-heavy incumbents.

North America led the market with 36.2% share in 2025, supported by USDA traceability funding and a commercial dairy base of roughly 9.4 million milking cows. Europe followed at 28.7%, anchored by the Netherlands, Germany, France, and the United Kingdom. Asia Pacific is the fastest-growing region with a CAGR projected near 14.5%, reflecting Chinese dairy modernization, India's 230.58 million tonnes of milk production reported by the Press Information Bureau for 2022-2023, and Australia's tightening biosecurity regime. Looking through 2034, market structure is expected to consolidate around four global platforms while specialist start-ups capture niche performance categories such as poultry environmental sensors and equine biosensors.

Market Definition & Scope

The livestock wearable sensor market covers electronic devices physically attached to or ingested by farm animals that capture continuous physiological, behavioral, or location data and transmit it to farm-management software. The market encompasses smart collars, electronic ear tags, rumen boluses, leg-mounted pedometers, halter-based sensors, tail tags, and injectable transponders deployed across cattle, swine, poultry, equine, and small ruminant operations.

This analysis includes hardware sales, embedded firmware, and the per-animal subscription fees bundled with sensor deployment. Excluded are non-wearable sensors mounted on barn infrastructure (parlor cameras, ammonia probes, weight scales), companion-animal wearables for dogs and cats, conventional non-electronic visual ear tags, and standalone livestock management software without an associated wearable component. The wearable sensor segment accounts for an estimated 38% of the parent precision livestock farming hardware market, which is itself a sub-segment of the broader animal health and agtech industry valued above USD 1.4 trillion in 2025 by global production output.

, By Animal (Cattle, Poultry, Swine, Sheep & Goats), By Application (Health Monitoring, Behavior, Reproduction, Location, Feeding Management), By End-User Region, Key Players – Dynamics, Precision Livestock Farming (PLF) & AgTech IoT Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The livestock wearable sensor market expanded from USD 2.18 Billion in 2025 toward a projected USD 6.04 Billion by 2034, representing a 12.0% CAGR over the nine-year forecast horizon.

- Segment Dominance by Product Type: Smart collars held the largest revenue share at 32.0% in 2025, driven by virtual-fencing adoption on extensive grazing operations across the United States, Australia, and New Zealand.

- Segment Dominance by Animal Type: Cattle, including dairy and beef, captured 52.1% revenue share in 2025 because of high per-animal economic value and longer productive lifespans relative to swine and poultry.

- Driver: Federal traceability mandates including the USDA APHIS 840 EID rule effective November 5, 2024 are pushing electronic ear tag attach rates above 70% on interstate-moved dairy cattle.

- Restraint: Average sensor system payback periods of 18 to 30 months and per-collar costs ranging from USD 100 to USD 350 limit penetration on herds smaller than 100 animals, particularly across Latin America and Africa.

- Opportunity: The trailing 12-month venture funding total reached approximately USD 320 Million, with Halter alone closing USD 320 Million across two rounds, signaling investor consensus on a multibillion-dollar virtual-fencing category.

- Trend: AI-driven baseline learning is replacing rule-based threshold alerts, with platforms from Connecterra and Smartbow (Zoetis) achieving 92 to 94% sensitivity for early disease and estrus detection.

- Regional: North America accounted for 36.2% of global revenue, equivalent to USD 0.79 Billion in 2025, supported by approximately 9.4 million U.S. dairy cows and 87.2 million beef cattle in inventory.

Key Insights Summary

- Behavioral deviations recorded by accelerometer-based wearables typically appear four to six days before clinical signs of bovine respiratory disease, according to peer-reviewed work cited in the Animals journal published by MDPI in 2021.

- Per the USDA APHIS final rule that took effect November 5, 2024, every official ear tag applied to interstate-moved dairy cattle and sexually intact beef cattle 18 months and older must carry both visual and electronic readability, with EID tags priced at roughly USD 3 each through state veterinarian channels.

- Halter disclosed in November 2025 that ranchers in 22 U.S. states had installed roughly 11,000 miles of virtual fencing using its solar-powered collars, an installation footprint the company estimates avoided about USD 220 Million in conventional fence construction expenditure.

- A multicenter clinical validation study from 2024 reported a 93.7% estrus detection sensitivity for ear-mounted sensors deployed by CowManager B.V., across more than 1.2 million monitored cow-days, with a false-positive rate near 4%.

- SmaXtec animal care GmbH closed a strategic growth investment from KKR in January 2025 alongside Highland Europe, accelerating a product roadmap that includes a continuous progesterone biosensor module integrated into its rumen bolus platform.

- Hardware costs for RFID and GPS modules used in livestock wearables have been declining at roughly 7 to 9% per year through 2025 as semiconductor miniaturization and IoT-component economies of scale compress bill-of-materials.

- On March 24, 2026, Halter banked a USD 220 Million Series E round led by Founders Fund at a USD 2 Billion valuation, doubling its prior valuation inside nine months and placing virtual fencing among the most-capitalized agtech sub-categories of the cycle.

Competitive Landscape Overview

The livestock wearable sensor market is moderately consolidated, with the four largest vendors (Merck Animal Health, DeLaval, GEA Group, and Nedap N.V.) collectively holding an estimated 41 to 45% of 2025 revenue. Competition is shifting from hardware specifications toward platform breadth: vendors are bundling collars or ear tags with cloud analytics, herd management dashboards, and integration with milking robots or feed automation. Halter's USD 2 Billion valuation reflects how a connectivity-and-data play, rather than a pure device sale, is now the strategic prize.

Consolidation has progressed through acquisitions such as GEA Group taking ownership of CattleEye in March 2024 to add AI lameness detection, and Merck Animal Health bringing Vence into its portfolio in 2022 for virtual fencing reach. New entrants from outside conventional agtech, including Saskatchewan-based Ori Cattle which launched its first pilot in early 2026, are pursuing subscription-free models priced for cow-calf operators rather than commercial dairies.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product | Geographic Strength | Recent Strategic Move |

|---|---|---|---|---|---|

| Merck Animal Health | USA | Leader | Allflex SenseHub, Vence collars | North America, Europe, Australia | Brought Vence virtual-fencing portfolio onto Allflex distribution rails through 2025 |

| DeLaval | Sweden | Leader | DelPro herd management, RTLS tags | Global dairy footprint | Rolled out the VMS V310 milking system with integrated heat and pregnancy sensing |

| GEA Group | Germany | Leader | DairyNet, CattleEye AI module | Europe, North America | Closed CattleEye purchase in March 2024 to embed video-AI lameness detection |

| Nedap N.V. | Netherlands | Leader | SmartTag Neck, Leg, and Ear | Europe, North America | Broadened the SmartTag platform with cloud analytics for mid-sized dairy cooperatives |

| Afimilk Ltd. | Israel | Challenger | AfiAct II leg pedometer, AfiCollar | Global dairy | Pushed AfiFarm 5 deployments across Latin America during 2025 |

| smaXtec animal care GmbH | Austria | Challenger | Rumen bolus with pH and temp | Europe, North America | Banked KKR-led growth round in January 2025 and named Charlie Sheppy CEO in November 2025 |

| CowManager B.V. | Netherlands | Challenger | SensOor ear sensor | Europe, North America | Tied SensOor data into Lely Vector feeding system across a 120-farm pilot in the Netherlands |

| Halter | New Zealand / USA | Challenger | Solar-powered smart collar | USA, NZ, Australia | Banked USD 220 Million in March 2026 from Founders Fund at a USD 2 Billion valuation |

| Connecterra B.V. | Netherlands | Niche | Ida AI platform with neckband | Europe | Sharpened Ida deep-learning models with federated-learning across multi-farm datasets |

| Datamars (Allflex/HerdInsights) | Switzerland | Niche | Z Tags, RFID readers, HerdInsights | Global | Widened HerdInsights collar deployments through Datamars Livestock distribution channels |

Segmentation Analysis

The livestock wearable sensor market segments along four primary axes: product type, animal type, application, and end-user. Cross-referencing these axes shows that smart collars on dairy cattle for health monitoring through dairy farms remains the single largest revenue cell, accounting for roughly 21% of 2025 global revenue.

By Product Type

Smart collars led the product type split with 32.0% revenue share in 2025, equal to roughly USD 0.70 Billion. Solar-powered collars from Halter and Vence have captured beef and grazing markets that the smaller form-factors of dairy ear tags cannot serve, and per-collar pricing now ranges from USD 200 on subscription models to USD 350 outright. Smart ear tags followed at 28.0% share, reflecting their compatibility with USDA 840 EID rules and CowManager-style behavioral monitoring at lower per-animal capex.

Rumen boluses captured 15.0% revenue share, anchored by smaXtec's continuous in-rumen platform and an installed base across Austria, Germany, and the United States. Boluses deliver core body temperature, rumination, and pH data over service lives that now exceed 6 years, displacing manual thermometer checks across 800-cow-plus dairies. Leg-mounted activity bands and pedometers represented 14.0% of the market, with Afimilk's AfiAct II and Nedap's SmartTag Leg widely deployed for heat detection on freestall dairies. Other formats including halters, tail tags, and injectable transponders accounted for the remaining 11.0% in 2025.

By Animal Type

Cattle held a commanding 52.1% revenue share in 2025, equal to approximately USD 1.14 Billion. Dairy cows alone represent the bulk of this segment because per-animal lifetime gross revenue around USD 15,000 makes even modest production gains profitable to instrument. Beef cattle adoption is climbing fastest within the cattle category as virtual fencing collars from Halter and Vence reach extensive grazing operations. The segment's CAGR through 2034 is projected at 11.4%.

Poultry took 18.0% share and is the fastest-growing animal category at a forecast 14.6% CAGR, fueled by Asia Pacific commercial broiler and layer expansion. Swine accounted for 15.0% on the back of African swine fever risk management across Germany, Spain, and China; biosensors that detect early respiratory and behavioral changes are valued at USD 25 to USD 40 per animal at scale. Equine wearables held 9.0% share concentrated in racing and sport horse markets across the United States, United Kingdom, and Gulf Cooperation Council states. Sheep, goats, and other small ruminants comprised the remaining 5.9%.

By Application

Health and disease detection led applications with 35.0% revenue share, reflecting the economic case anchored by USDA data that places average dairy disease cost above USD 400 per affected cow. Sensor-driven mastitis and ketosis prediction now reaches 92% accuracy on AI-augmented platforms, prompting integration with veterinary protocols on 7,000-plus farms across more than 60 countries deploying CowManager SensOor.

Reproductive management and heat detection captured 25.0% share, with conception-rate improvements of 15 to 16% versus visual observation reported across CowManager and Nedap deployments. Behavior and activity monitoring took 20.0%, location and GPS tracking 15.0%, and feed intake monitoring 5.0%. Heat-detection accuracy is now the primary purchase criterion on 200-plus-cow dairies because each missed estrus event costs an estimated USD 250 in extended days open.

By End-User

Dairy farms dominated the end-user breakdown with 45.0% revenue share, equivalent to roughly USD 0.98 Billion in 2025. Adoption is most advanced on robotic-milking herds because sensor-driven heat detection and rumination data feed directly into automated drafting gates. Beef operations and feedlots followed at 30.0%, with U.S. cow-calf adoption climbing fastest as Halter and Vence deployments expand.

Poultry farms accounted for 12.0%, swine farms 9.0%, and research institutes plus veterinary practices the remaining 4.0%. Mid-sized dairies (200 to 2,000 milking head) are the fastest-growing end-user cohort because hardware cost compression has pushed payback periods below 24 months on this herd-size band, opening a customer base previously priced out of the technology.

Regional Analysis

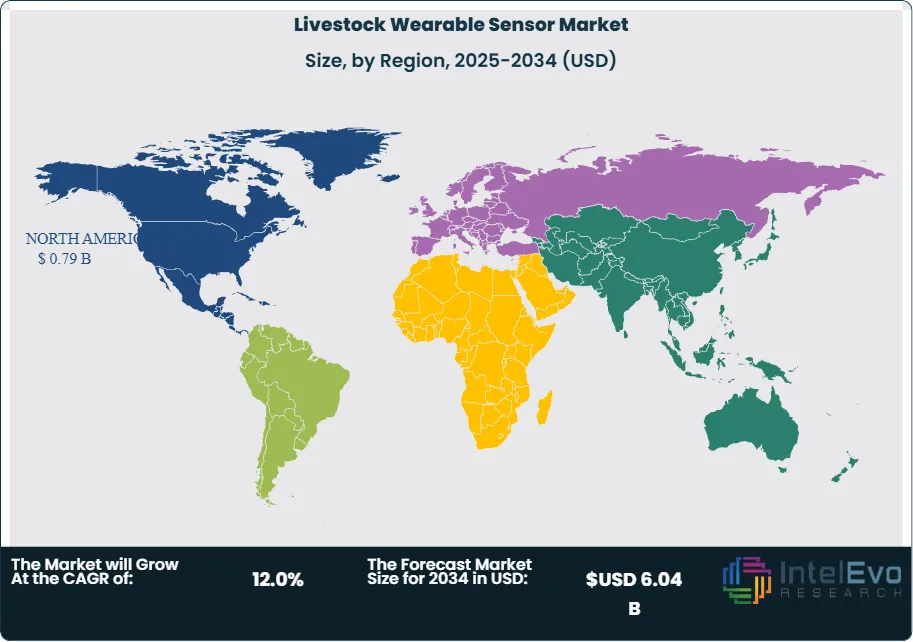

The global livestock wearable sensor market splits across five regions, with revenue concentration tracking commercial dairy density and traceability regulation. North America led with 36.2% share, Europe followed at 28.7%, Asia Pacific captured 22.0%, Latin America 7.5%, and Middle East and Africa 5.6%, summing to 100% of 2025 revenue.

North America

North America generated USD 0.79 Billion in 2025 revenue, holding 36.2% global share. The United States accounted for the bulk, supported by 9.4 million dairy cows and 87.2 million beef cattle in inventory. The USDA APHIS 840 EID rule that took effect on November 5, 2024 is the primary regulatory accelerant, requiring electronic identification on interstate-moved dairy cattle and breeding-age beef cattle. Canada contributed roughly USD 0.072 Billion, with Alberta-led feedlot adoption and federal Automated Livestock Monitoring research grants. Halter's U.S. customer base reached 200-plus ranchers across 22 states by November 2025, illustrating accelerating beef-side penetration.

Europe

Europe contributed USD 0.626 Billion in 2025, equal to 28.7% global share, with the Netherlands, Germany, France, and the United Kingdom as anchor markets. EU mandatory electronic identification rules for cattle, sheep, and goats remain in force across all 27 member states, while the Farm to Fork strategy reinforces precision-livestock investment. The Netherlands hosts a dense ecosystem of vendors including CowManager B.V., Connecterra B.V., Nedap N.V., and Lely International N.V. Germany's swine industry is the largest European wearable swine market, with roughly 21 million pigs deployed under behavioral monitoring tied to African Swine Fever vigilance.

Asia Pacific

Asia Pacific posted USD 0.480 Billion in 2025 with 22.0% share and is the fastest-growing region at a 14.5% forecast CAGR through 2034. China leads regional value through industrial-scale dairy modernization across Inner Mongolia, Hebei, and Heilongjiang provinces. India follows on the strength of milk production at 230.58 million tonnes for 2022-2023 reported by the Press Information Bureau, with state-level deployments such as the JioGauSamriddhi smart neck-tag system launched by Jio Things Limited in August 2025. Australia and New Zealand are anchor virtual-fencing markets, where Halter has deployed collars across roughly 400,000 head as of mid-2025.

Latin America

Latin America accounted for USD 0.164 Billion in 2025 (7.5% share). Brazil, with the world's largest commercial cattle herd above 230 million head, is the regional anchor, though wearable penetration remains below 2% of the herd because of price sensitivity on extensive ranches. Argentina and Mexico follow, with adoption concentrated on dairy operations in the Pampas and Jalisco. Vence has run pilots across the region to extend virtual fencing into rotational grazing programs aligned with regenerative-agriculture incentive payments.

Middle East & Africa

Middle East and Africa generated USD 0.122 Billion in 2025, holding 5.6% share. Saudi Arabia and the United Arab Emirates anchor regional dairy investment through Almarai and Al Ain Farms, both of which use Allflex and Afimilk wearables on confined herds. South Africa is the largest sub-Saharan market, with HerdInsights deployments expanding through 2025. Adoption headwinds include limited cellular coverage on extensive grazing land, which Halter's satellite-connected collar variant is positioned to address as it rolls out through 2026.

Country Analysis

United States

The U.S. livestock wearable sensor market reached USD 0.654 Billion in 2025 and is forecast to grow at an 11.5% CAGR through 2034. The USDA APHIS rule on electronic identification, enforceable from November 5, 2024, channels approximately 1.6 million interstate-moved dairy and breeding cattle annually into mandatory 840 EID tagging, with USD 15 Million in federal funding allocated under the Consolidated Appropriations Act of 2024 for free EID tag distribution. Beef-side adoption is being shaped by Halter, which closed an 11,000-mile virtual-fencing milestone with U.S. customers in November 2025, and by Merck Animal Health's Vence platform, which operates without cellular coverage and now serves cow-calf operations across the Mountain West. State initiatives including Wisconsin, Texas, and California precision-dairy programs add roughly USD 35 Million in cumulative subsidy availability for 2025-2026.

Germany

Germany's market reached USD 0.153 Billion in 2025, growing at a 12.4% CAGR through 2034. Adoption is concentrated on the country's 3.7 million dairy cows and 21 million pigs, with regulatory drivers including the EU mandatory electronic identification framework and stricter Tierschutz-Nutztierhaltungsverordnung welfare standards. SmaXtec animal care GmbH and CowManager B.V. command notable installed bases on Bavarian and North Rhine-Westphalia dairies, while domestic engineering champion GEA Group integrates CattleEye's AI lameness module into its DairyNet platform. African Swine Fever vigilance has accelerated swine biosensor deployment across the country's largest finishing operations.

Netherlands

The Netherlands generated USD 0.109 Billion in 2025 at a 13.8% CAGR through 2034, the highest among European country markets. Dutch dairy operates on roughly 1.6 million milking cows under intensive housing, where wearables yield the highest economic return per animal. Domestic vendors CowManager B.V., Connecterra B.V., Nedap N.V., and Lely International N.V. control more than 60% of the local installed base. The expanded CowManager-Lely SensOor-Vector integration deployed across 120 Dutch farms produced a 7.3% lift in energy-corrected milk yield per cow per day, reinforcing the country's status as the global testbed for sensor-driven dairy automation.

China

China's livestock wearable sensor market reached USD 0.196 Billion in 2025 at a 15.2% CAGR through 2034, the fastest among major country markets. Demand is driven by commercial dairy consolidation across Inner Mongolia and Heilongjiang where 10,000-cow units are increasingly the norm and where wearable attach rates exceed 65% on new builds. State-affiliated agricultural research institutes have piloted multi-parameter biosensor patches for metabolic monitoring on dairy cattle, while NB-IoT and 5G coverage rollouts under the Ministry of Industry and Information Technology have removed connectivity bottlenecks on large-scale poultry farms. African Swine Fever recovery investment continues to push behavioral-monitoring deployments across the country's pork sector.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product Type

- RFID Tags & Sensors

- GPS Tracking Devices

- Health Monitoring Sensors

- Activity Monitoring Devices

- Smart Collars

- Others

By Animal Type

- Cattle

- Poultry

- Swine

- Sheep & Goats

- Others

By Application

- Health Monitoring & Disease Detection

- Behavior Monitoring

- Reproduction Management

- Location & Tracking

- Feeding Management

- Others

By End-User

- Dairy Farms

- Livestock Farms

- Poultry Farms

- Veterinary Clinics

- Research Institutes

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.18 B |

| Forecast Revenue (2034) | USD 6.04 B |

| CAGR (2025-2034) | 12.0% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (RFID Tags & Sensors, GPS Tracking Devices, Health Monitoring Sensors, Activity Monitoring Devices, Smart Collars, Others), By Animal Type, (Cattle, Poultry, Swine, Sheep & Goats, Others), By Application, (Health Monitoring & Disease Detection, Behavior Monitoring, Reproduction Management, Location & Tracking, Feeding Management, Others), By End-User, (Dairy Farms, Livestock Farms, Poultry Farms, Veterinary Clinics, Research Institutes, Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | MERCK ANIMAL HEALTH, DELAVAL, GEA GROUP, NEDAP N.V., AFIMILK LTD., SMAXTEC ANIMAL CARE GMBH, COWMANAGER B.V., HALTER, CONNECTERRA B.V., DATAMARS, MOOCALL LTD., BOUMATIC LLC, DAIRYMASTER, LELY INTERNATIONAL N.V., FULLWOOD JOZ, HOKOFARM GROUP, GALLAGHER GROUP LIMITED, CERES TAG, STELLAPPS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Animal (Cattle, Poultry, Swine, Sheep & Goats), By Application (Health Monitoring, Behavior, Reproduction, Location, Feeding Management), By End-User Region, Key Players – Dynamics, Precision Livestock Farming (PLF) & AgTech IoT Trends & Forecast 2026-2034")

, By Animal (Cattle, Poultry, Swine, Sheep & Goats), By Application (Health Monitoring, Behavior, Reproduction, Location, Feeding Management), By End-User Region, Key Players – Dynamics, Precision Livestock Farming (PLF) & AgTech IoT Trends & Forecast 2026-2034")

, By Animal (Cattle, Poultry, Swine, Sheep & Goats), By Application (Health Monitoring, Behavior, Reproduction, Location, Feeding Management), By End-User Region, Key Players – Dynamics, Precision Livestock Farming (PLF) & AgTech IoT Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Livestock Wearable Sensor Market?

Global Livestock Wearable Sensor Market was valued at USD 2.18 Billion in 2025 and is projected to reach USD 6.04 Billion by 2034, growing at a CAGR of 12.0% during 2026–2034. Explore market trends, drivers, opportunities, segmentation, and industry insights.

Who are the major players in the Livestock Wearable Sensor Market?

MERCK ANIMAL HEALTH, DELAVAL, GEA GROUP, NEDAP N.V., AFIMILK LTD., SMAXTEC ANIMAL CARE GMBH, COWMANAGER B.V., HALTER, CONNECTERRA B.V., DATAMARS, MOOCALL LTD., BOUMATIC LLC, DAIRYMASTER, LELY INTERNATIONAL N.V., FULLWOOD JOZ, HOKOFARM GROUP, GALLAGHER GROUP LIMITED, CERES TAG, STELLAPPS, Others

Which segments covered the Livestock Wearable Sensor Market?

By Product Type, (RFID Tags & Sensors, GPS Tracking Devices, Health Monitoring Sensors, Activity Monitoring Devices, Smart Collars, Others), By Animal Type, (Cattle, Poultry, Swine, Sheep & Goats, Others), By Application, (Health Monitoring & Disease Detection, Behavior Monitoring, Reproduction Management, Location & Tracking, Feeding Management, Others), By End-User, (Dairy Farms, Livestock Farms, Poultry Farms, Veterinary Clinics, Research Institutes, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Livestock Wearable Sensor Market

Published Date : 15 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date