- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global LNG Carrier Vessel Market Size & Forecast 2034 | CAGR 6.0%

Global LNG Carrier Vessel Market Size, Share, Growth & Industry Analysis By Vessel Size (Conventional Large-Scale Carriers, Q-Flex Carriers, Q-Max Carriers, Small-Scale & Coastal LNG Carriers), By Propulsion Type (DFDE & TFDE, ME-GI, X-DF & ME-GA Two-Stroke, Steam Turbine), By Cargo Containment System (Membrane, Moss), By Commercial Model (Long-Term Charter, Spot & Short-Term Charter, Floating Storage & Portfolio Trading) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

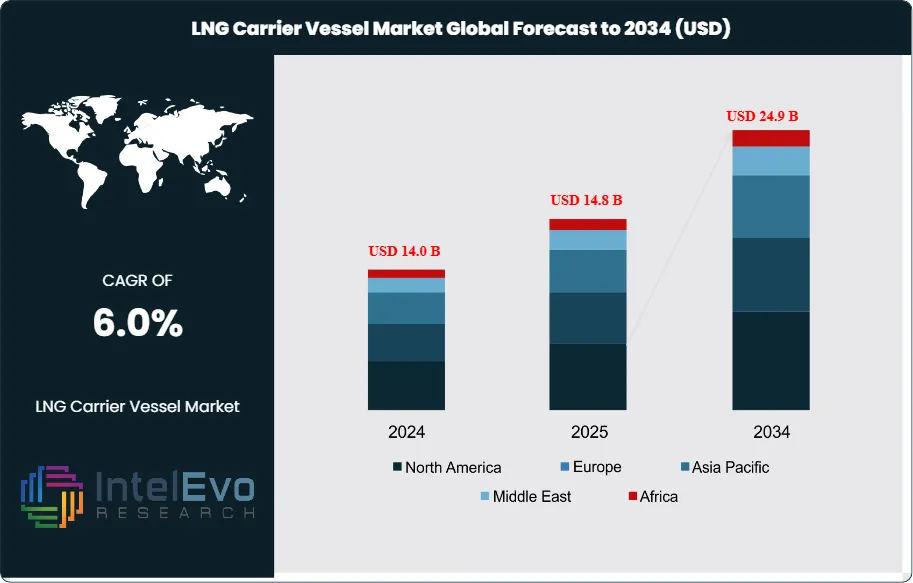

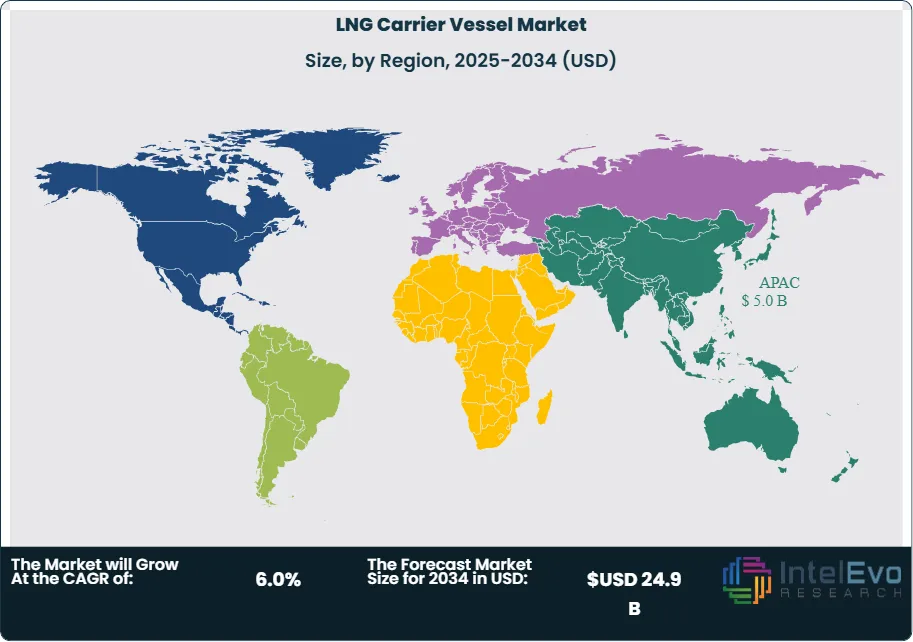

| USD 14.8 Billion | USD 24.9 Billion | 6.0% | Asia Pacific, 34.0% |

The LNG Carrier Vessel Market was valued at approximately USD 14.0 Billion in 2024 and reached USD 14.8 Billion in 2025. The market is projected to grow to USD 24.9 Billion by 2034, expanding at a CAGR of 6.0% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 10.1 Billion over the analysis period. The estimate reflects a market built on 411.24 million tonnes of global LNG trade, a mid-2025 fleet of about 823 LNG carriers, and an orderbook of roughly 343 vessels, which keeps long-term demand for LNG carrier vessel capacity firmly intact even after the freight rate collapse seen in early 2025.

Get More Information about this report -

Request Free Sample ReportThe LNG carrier vessel market in 2025 sits between two opposing forces. One force is structural demand. QatarEnergy is expanding from 77 mtpa toward much higher output through the North Field program, while Asian LNG demand continues to pull vessel demand eastward. The other force is near-term oversupply. Freight rates for standard LNG carriers fell to five-year lows in February 2025 as ship availability increased faster than cargo growth, showing that vessel ordering during the post-2022 energy shock created a temporary capacity surplus. That imbalance does not cancel the long-cycle case for LNG carrier vessels. It changes earnings distribution by vessel age, propulsion type, charter coverage, and route exposure.

Technology is now a hard commercial filter in the LNG carrier vessel market. Newbuild preference has shifted toward 174,000 cbm class carriers with dual-fuel two-stroke propulsion, reliquefaction systems, and digital ship performance platforms. Hanwha Ocean states that its 200th LNG carrier delivered in February 2025 used a low-pressure dual-fuel ME-GA engine and smart ship systems, while QatarEnergy LNG highlighted twin slow-speed gas-burning engines in its new conventional fleet. Owners with modern X-DF, ME-GI, and ME-GA tonnage are securing the strongest charter access because charterers want lower boil-off, better fuel efficiency, and lower methane slip exposure under tightening decarbonization rules.

Regulation also shapes capital allocation in this market. The IMO approved net-zero regulations in April 2025, with formal adoption targeted for October 2025 and entry into force in 2027 for large ocean-going ships over 5,000 gross tonnage. That framework, combined with MARPOL amendments and rising scrutiny on methane emissions, raises compliance pressure on older steam turbine LNG carriers and lifts replacement demand for modern vessels. The result is a two-speed market. Modern carriers with long-term charters hold asset value. Older steam vessels face weaker spot economics, higher retrofit costs, and higher rechartering risk.

Regional capital remains concentrated in Asia Pacific shipbuilding, Middle East export growth, European import security, and North American liquefaction-linked chartering. South Korea and China still dominate construction slots. Qatar continues to anchor multi-year charter demand. Europe remains structurally important because voyage patterns, storage cycles, and energy security planning influence ton-mile demand. These drivers support a steady 2025-2034 LNG carrier vessel market outlook even with short-cycle earnings volatility.

, By Propulsion Type (DFDE & TFDE, ME-GI, X-DF & ME-GA Two-Stroke, Steam Turbine), By Cargo Containment System (Membrane, Moss), By Commercial Model (Long-Term Charter, Spot & Short-Term Charter, Floating Storage & Portfolio Trading) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The LNG Carrier Vessel Market is estimated at USD 14.8 Billion in 2025 and projected to reach USD 24.9 Billion by 2034 at a 6.0% CAGR. The forecast reflects sustained fleet renewal, Qatar-linked chartering, and the buildout of new liquefaction supply.

- Segment Dominance: The LNG Carrier Vessel Market by vessel size is led by conventional large-scale carriers in the 145,000-180,000 cbm class, with an estimated 41.0% share in 2025, because this format remains the standard for new global chartering and portfolio trade. Nakilat’s fleet mix and QatarEnergy’s latest conventional vessel program support that position.

- Segment Dominance: The LNG Carrier Vessel Market by application is led by long-term export project shipping, with an estimated 61.0% share in 2025, driven by QatarEnergy, JERA, PETRONAS-linked chartering, and other contracted supply chains.

- Driver: The main driver is the expansion of global LNG trade and vessel deployment needs. Global LNG trade reached 411.24 MT in 2024, while around 234 new LNG carriers are scheduled for delivery during 2026-2030, showing how supply growth keeps vessel demand elevated.

- Restraint: The main restraint is near-term vessel oversupply. Atlantic spot freight for standard LNG carriers fell to USD 4,250 per day in February 2025, down 82% since the start of 2025, which hurt older vessels most.

- Opportunity: The biggest opportunity sits in fleet renewal and charter coverage for modern dual-fuel tonnage. Hanwha Ocean says it held 23.4% global LNG carrier construction share in February 2025 and can build up to 25 LNG carriers per year, showing strong room for high-spec replacement demand through 2034.

- Trend: The dominant trend is the shift toward modern gas-burning two-stroke carriers and compliance-ready ships. QatarEnergy’s new 174,000 cbm vessels and Flex LNG’s 13 modern two-stroke carriers show the fleet moving toward lower-emission, fuel-efficient assets.

- Regional Analysis: Asia Pacific leads the LNG Carrier Vessel Market with an estimated 34.0% share and about USD 5.0 Billion in 2025, supported by South Korean and Chinese shipyards, Japanese owners, and major importing markets led by China, Japan, and India.

Competitive Landscape Overview

The LNG Carrier Vessel Market is moderately consolidated. The top four participants are estimated to hold about 28.5% of 2025 market revenue, with competition shaped by fleet scale, charter relationships, propulsion technology, and access to Korean and Chinese yard slots. Competitive intensity increased during 2024-2026 as QatarEnergy accelerated vessel awards, Nakilat expanded build programs, and Japanese owners secured more long-term charter exposure. Price matters in spot shipping, but the strongest competitive edge comes from long-term charter coverage and modern dual-fuel fleets.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Nakilat | Qatar | Leader | Q-Flex and Q-Max LNG carrier fleet | Middle East | Began steel cutting for 8 new LNG carriers at Hanwha Ocean in Mar 2025 and 17 more at HHI in May 2025. |

| Mitsui O.S.K. Lines | Japan | Leader | Long-term chartered 174,000 cbm LNG carriers | Asia Pacific | Signed long-term charters with QatarEnergy for six new LNG carriers in Dec 2024 and with JERA for another newbuilding in Jan 2025. |

| NYK Line | Japan | Leader | QatarEnergy newbuild LNG carrier JV fleet | Asia Pacific | Named Al Tuwar in Apr 2025 and later delivered Al Zuwair in Aug 2025 for the QatarEnergy program. |

| Kawasaki Kisen Kaisha | Japan | Leader | LNG carriers under global long-term charter | Asia Pacific | Took part in the delivery and naming of Al Tuwar in Apr 2025 and continued expansion through the QatarEnergy consortium in 2025. |

| MISC Berhad | Malaysia | Challenger | Consortium-operated LNG carriers for QatarEnergy | Asia Pacific | Managed Mihzem and Idd Al Shargi under the QatarEnergy consortium in Oct 2025 and signed two PLL newbuild charter parties in Dec 2024. |

| China LNG Shipping (Holdings) | China | Challenger | QatarEnergy project LNG carrier JV assets | Asia Pacific | Took delivery of Al Mas’habiyyah in Jul 2025 under the QatarEnergy transportation project. |

| GasLog Ltd. | Greece | Challenger | Modern LNG carrier fleet and ship management | Europe | Reported 12 vessel drydockings across 2025 and retained one of the larger modern LNG fleets with two vessels under construction. |

| BW LNG | Singapore | Challenger | LNG carriers and FSRUs | Global | Continued an 11-vessel LNG newbuilding program, including nine 173,400-174,000 cbm ships and two 177,000 cbm ships, in 2025 disclosures. |

| Hanwha Ocean | South Korea | Niche Player | LNG carrier construction platform | Asia Pacific | Delivered its 200th LNG carrier in Feb 2025 and later backed the first U.S.-flagged LNG carrier order in nearly 50 years in Jul 2025. |

| Samsung Heavy Industries | South Korea | Niche Player | Large LNG carrier construction | Asia Pacific | Remained active in LNG carrier construction in 2025 even as it disclosed cancellations tied to Russia-linked icebreaking LNG carrier work in Jun 2025. |

By Vessel

The LNG Carrier Vessel Market by vessel size is led by conventional large-scale carriers of 145,000-180,000 cbm, which account for an estimated 41.0% of 2025 revenue, or about USD 6.1 Billion. This class remains the commercial standard because it balances berth compatibility, cargo economics, and charter flexibility. Q-Flex carriers represent about 34.0%, or USD 5.0 Billion, anchored mainly by Qatar-linked trade. Nakilat alone operates 31 Q-Flex vessels and 14 Q-Max vessels, showing how concentrated the ultra-large segment remains. Q-Max carriers hold an estimated 16.0% share, or USD 2.4 Billion, and stay relevant on high-volume Qatar routes where loading and receiving infrastructure support very large ships. Small-scale and coastal LNG carriers represent the remaining 9.0%, or USD 1.3 Billion, driven by niche distribution, satellite LNG, and regional balancing. Through 2034, conventional 174,000 cbm newbuilds should gain the most share because charterers prefer flexible vessels that can serve both Atlantic and Asia routes without the infrastructure constraints tied to the largest Q-class ships.

By Propulsion Type

The LNG Carrier Vessel Market by propulsion type shows a decisive shift toward modern fuel-efficient propulsion. Dual-fuel electric and tri-fuel diesel electric carriers hold an estimated 46.0% share in 2025, or USD 6.8 Billion, because a large installed fleet still operates with these systems. Two-stroke ME-GI, X-DF, and ME-GA carriers already hold about 39.0%, or USD 5.8 Billion, and this segment is growing fastest because most recent orders and deliveries use lower-emission, lower-boil-off propulsion. Steam turbine ships have fallen to roughly 15.0%, or USD 2.2 Billion, and are now the weakest commercial class in spot trading due to higher fuel consumption and poorer compliance economics. Reuters reported negative returns for older vessels during the February 2025 rate slump, which confirms the widening earnings gap between legacy tonnage and modern ships. The commercial result is clear. Charterers pay for fuel efficiency, regulatory readiness, and methane management, so two-stroke dual-fuel carriers will take most incremental market share through 2034.

By Cargo Containment System

The LNG Carrier Vessel Market by cargo containment system remains heavily concentrated in membrane technology, which accounts for an estimated 82.0% of 2025 revenue, or about USD 12.1 Billion. Membrane systems dominate newbuild contracting because they allow higher volumetric efficiency and better fit the 174,000 cbm conventional class now favored by major charterers. Moss-type spherical containment still holds around 18.0%, or USD 2.7 Billion, mainly in older fleets and specialized route portfolios. The containment split also tracks asset age. Most fresh QatarEnergy-linked orders and new conventional carriers coming from Chinese and South Korean yards are membrane-based, while Moss vessels remain more common in legacy fleets and secondary markets. This part of the LNG carrier vessel market is unlikely to change sharply by 2034 because shipyard design standards, financing preferences, and charterer specifications now lean strongly toward membrane containment. That makes membrane technology the default procurement choice for the next build cycle.

By Commercial Model

The LNG Carrier Vessel Market by commercial model is led by long-term time charter contracts, which account for an estimated 72.0% share in 2025, or USD 10.7 Billion. This reflects how project-backed LNG shipping works. Vessel finance, shipyard slots, and cargo programs are often tied together years before delivery. Spot and short-term chartering represent about 18.0%, or USD 2.7 Billion, while portfolio trading, internal fleet optimization, and floating storage-linked deployment account for about 10.0%, or USD 1.5 Billion. The February 2025 collapse in spot freight rates showed why this split matters. Owners with fixed contracts protected cash flow, while exposed spot fleets saw earnings fall sharply. New charter awards from QatarEnergy, PETRONAS-linked programs, JERA, and other long-horizon LNG buyers show that commercial security still drives asset ordering. By 2034, charter-backed fleets should keep the largest share of market value because lenders, lessors, and owners continue to price long-term coverage above merchant exposure.

Regional Analysis

Asia Pacific

The LNG Carrier Vessel Market in Asia Pacific accounted for an estimated 34.0% share and USD 5.0 Billion in 2025. Asia Pacific leads because the region combines shipbuilding, ownership, and import demand in one system. South Korea remains the core construction base through Hanwha Ocean, HD Hyundai Heavy Industries, and Samsung Heavy Industries. China has increased its role through Hudong-Zhonghua and China LNG Shipping, while Japan remains central on the ownership side through MOL, NYK, and K Line. China, Japan, India, and South Korea are also key LNG demand centers. IGU reported stronger spot LNG imports in China and India during 2024, supported by heatwaves, infrastructure expansion, and gas-for-power demand. This regional structure gives Asia Pacific the deepest industrial base in the LNG carrier vessel market and keeps it ahead through 2034.

Middle East & Africa

The LNG Carrier Vessel Market in Middle East & Africa accounted for an estimated 24.0% share and USD 3.6 Billion in 2025. Qatar is the anchor country by a wide margin because it runs 14 LNG trains with 77 mtpa capacity and continues to underpin the largest vessel expansion cycle in the sector. Nakilat remains the largest LNG carrier owner globally with 69 LNG carriers, including 31 Q-Flex and 14 Q-Max vessels. Qatar-linked demand also explains why so much of the global orderbook is committed to long-term projects rather than open merchant shipping. The UAE and Saudi Arabia matter through energy investment and maritime finance, while South Africa plays a smaller support role in regional shipping and bunkering corridors. The region carries geopolitical risk, which became visible in March 2026 when disrupted Qatari production and vessel positioning outside Hormuz pushed Atlantic LNG freight to USD 264,250 per day and Pacific rates to USD 219,250 per day. That volatility raises insurance and route risk, but it also strengthens the strategic value of Middle East-linked LNG tonnage.

Europe

The LNG Carrier Vessel Market in Europe accounted for an estimated 19.0% share and USD 2.8 Billion in 2025. Europe no longer drives the same emergency restocking cycle seen in 2022-2023, yet it remains vital because LNG import patterns, storage behavior, and Atlantic basin voyage economics heavily affect vessel utilization. IGU reported that European LNG imports fell by 21.22 MT year on year in 2024 to 100.07 MT, driven by high starting inventories, weak demand, and steady pipeline supply. That decline shortened voyage demand for some Atlantic cargoes and increased near-term vessel availability, which helped push spot freight lower in early 2025. Greece remains important through owners such as GasLog and Maran Gas Maritime. The United Kingdom, France, Germany, and Italy stay relevant through receiving terminals and trading activity. Europe’s role in the LNG carrier vessel market will remain influential because ton-mile demand still depends on whether Atlantic cargoes move into Europe or divert to Asia.

North America

The LNG Carrier Vessel Market in North America accounted for an estimated 15.0% share and USD 2.2 Billion in 2025. The United States dominates this region because liquefaction growth and export contract structuring create future charter demand even though the domestic shipbuilding base for LNG carriers remains weak. Reuters reported in May 2025 that U.S. energy companies sought exemption from a plan requiring rising shares of LNG exports to move on U.S.-built ships, noting that the country had only five older LNG ships and none in operation. That gap explains why North American market value comes from cargo origination and charter demand rather than vessel construction leadership. Canada adds importance through West Coast LNG export development, while Mexico is relevant through import infrastructure and transshipment geography. The region’s long-term role improves as U.S. and Canadian liquefaction additions enter service, but vessel ownership and construction will remain tied mainly to Asian and Middle Eastern capital.

Latin America

The LNG Carrier Vessel Market in Latin America accounted for an estimated 8.0% share and USD 1.2 Billion in 2025. Brazil leads regional demand because of gas-to-power swings and import balancing, while Mexico links Latin America to North American cargo flows. Argentina and Chile remain the next most relevant countries due to seasonal LNG use and regasification-linked trade. The region has limited vessel ownership depth compared with Asia Pacific or the Middle East, but it matters for route optionality and seasonal ton-mile demand. Latin America also benefits when Atlantic basin cargoes are rerouted in response to price spreads and weather patterns. The regional market stays smaller because it lacks major LNG carrier manufacturing hubs and does not command the same charter concentration as Qatar or the large Asian buyers. Still, it remains commercially relevant for spot deployment and flexible charter positioning.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Vessel Size

- Conventional Large-Scale Carriers

- Q-Flex Carriers

- Q-Max Carriers

- Small-Scale and Coastal LNG Carriers

By Propulsion Type

- DFDE and TFDE

- ME-GI, X-DF, and ME-GA Two-Stroke

- Steam Turbine

By Cargo Containment System

- Membrane

- Moss

By Commercial Model

- Long-Term Time Charter

- Spot and Short-Term Charter

- Portfolio Trading and Floating Storage-Linked Deployment

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.8 B |

| Forecast Revenue (2034) | USD 24.9 B |

| CAGR (2025-2034) | 6.0% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Vessel Size, (Conventional Large-Scale Carriers, Q-Flex Carriers, Q-Max Carriers, Small-Scale and Coastal LNG Carriers), By Propulsion Type, (DFDE and TFDE, ME-GI, X-DF, and ME-GA Two-Stroke, Steam Turbine), By Cargo Containment System, (Membrane, Moss), By Commercial Model, (Long-Term Time Charter, Spot and Short-Term Charter, Portfolio Trading and Floating Storage-Linked Deployment) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | NAKILAT, MITSUI O.S.K. LINES, NYK LINE, KAWASAKI KISEN KAISHA, MISC BERHAD, BW LNG, GASLOG LTD., FLEX LNG, MARAN GAS MARITIME, CHINA LNG SHIPPING (HOLDINGS), GOLAR LNG, TEEKAY, HYUNDAI GLOVIS, HANWHA OCEAN, SAMSUNG HEAVY INDUSTRIES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Propulsion Type (DFDE & TFDE, ME-GI, X-DF & ME-GA Two-Stroke, Steam Turbine), By Cargo Containment System (Membrane, Moss), By Commercial Model (Long-Term Charter, Spot & Short-Term Charter, Floating Storage & Portfolio Trading) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Propulsion Type (DFDE & TFDE, ME-GI, X-DF & ME-GA Two-Stroke, Steam Turbine), By Cargo Containment System (Membrane, Moss), By Commercial Model (Long-Term Charter, Spot & Short-Term Charter, Floating Storage & Portfolio Trading) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Propulsion Type (DFDE & TFDE, ME-GI, X-DF & ME-GA Two-Stroke, Steam Turbine), By Cargo Containment System (Membrane, Moss), By Commercial Model (Long-Term Charter, Spot & Short-Term Charter, Floating Storage & Portfolio Trading) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the LNG Carrier Vessel Market?

Global LNG carrier vessel market valued at USD 14.0B in 2024, reaching USD 24.9B by 2034, growing at a CAGR of 6.0% from 2026–2034.

Who are the major players in the LNG Carrier Vessel Market?

NAKILAT, MITSUI O.S.K. LINES, NYK LINE, KAWASAKI KISEN KAISHA, MISC BERHAD, BW LNG, GASLOG LTD., FLEX LNG, MARAN GAS MARITIME, CHINA LNG SHIPPING (HOLDINGS), GOLAR LNG, TEEKAY, HYUNDAI GLOVIS, HANWHA OCEAN, SAMSUNG HEAVY INDUSTRIES, Others

Which segments covered the LNG Carrier Vessel Market?

By Vessel Size, (Conventional Large-Scale Carriers, Q-Flex Carriers, Q-Max Carriers, Small-Scale and Coastal LNG Carriers), By Propulsion Type, (DFDE and TFDE, ME-GI, X-DF, and ME-GA Two-Stroke, Steam Turbine), By Cargo Containment System, (Membrane, Moss), By Commercial Model, (Long-Term Time Charter, Spot and Short-Term Charter, Portfolio Trading and Floating Storage-Linked Deployment)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date