- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global LNG Ship-to-Ship Transfer Equipment Market Forecast 2034 | CAGR 15.4%

Global LNG Ship-to-Ship (STS) Transfer Equipment Market Size, Share, Growth & Industry Analysis By Product Type (Cryogenic Hose Assemblies, Pneumatic & Foam-Filled Fenders, Mooring Systems, Emergency Release Couplings, Manifold Adaptors & Vapour Return Equipment), By Application (FSRU-Linked Operations, FLNG, LNG Bunkering, Transshipment Hubs), By Vessel Type (Q-Flex & Q-Max, Standard LNG Carriers, Small-Scale LNG Vessels), By Service Type Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

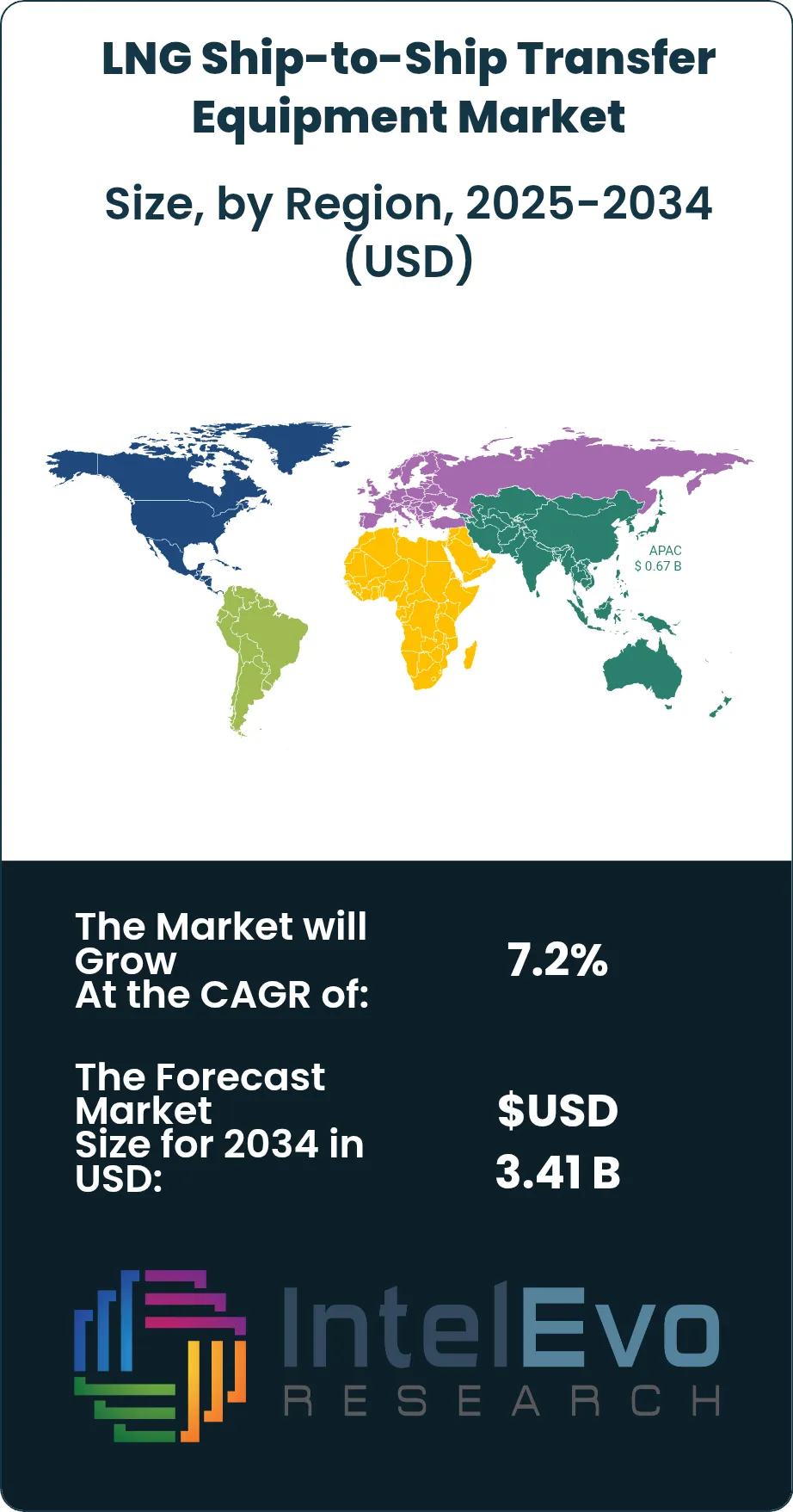

| USD 1.82 Billion | USD 3.41 Billion | 7.2% | Asia Pacific, 36.8% |

The LNG Ship-to-Ship Transfer Equipment Market was valued at approximately USD 1.70 Billion in 2024 and reached USD 1.82 Billion in 2025. The market is projected to grow to USD 3.41 Billion by 2034, expanding at a CAGR of 7.2% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 1.59 Billion over the analysis period, reflecting intensifying demand for flexible offshore LNG transfer infrastructure as the global gas trade accelerates away from fixed terminal-dependent supply chains.

Get More Information about this report -

Request Free Sample ReportLNG ship-to-ship transfer equipment encompasses cryogenic hose assemblies, pneumatic and foam-filled fenders, mooring systems, emergency release couplings, vapour return lines, and manifold adaptor sets used when transferring liquefied natural gas between two vessels at anchorage or in open water. Demand patterns are closely tied to LNG trade volumes, which the International Energy Agency estimates will expand by more than 45% between 2025 and 2034 as importing countries seek to bypass pipeline infrastructure constraints. The market benefits directly from every incremental tonne of LNG transacted through floating storage and regasification units (FSRUs), which require at least one STS operation per cargo cycle.

Regulatory frameworks are tightening around STS safety and environmental protection. The International Maritime Organization (IMO) revised MARPOL Annex I guidelines now extend to LNG STS operations in Emission Control Areas, compelling operators to upgrade legacy equipment to zero-emission or low-leak-rate configurations. The Ship Inspection Report Programme (SIRE) 2.0, implemented across the global tanker industry in 2024, introduced new STS-specific inspection criteria that effectively mandate third-party certified equipment from 2025 onward. These regulatory pressures are driving equipment replacement cycles that would otherwise remain dormant for 15 to 20 years.

Asia Pacific dominated the LNG STS transfer equipment market in 2025 with a 36.8% share, driven by Japan, South Korea, and Australia operating the world's busiest LNG import and export terminals. Middle East & Africa followed at 25.4%, anchored by Qatari offshore loading operations and Nigerian FLNG assets. North America held a 12.6% share in 2025 but is forecast to be the fastest-growing regional market through 2034, propelled by Gulf of Mexico FLNG project startups and Caribbean STS transshipment hubs serving European buyers. Investment in digital monitoring systems, including IoT-based cargo flow sensors and real-time cryogenic pressure telemetry, is reshaping equipment procurement decisions across all regions, with buyers increasingly selecting suppliers that offer integrated hardware-software bundles rather than standalone mechanical components.

Transfer Equipment Market Size, Share, Growth & Industry Analysis By Product Type (Cryogenic Hose Assemblies, Pneumatic & Foam-Filled Fenders, Mooring Systems, Emergency Release Couplings, Manifold Adaptors & Vapour Return Equipment), By Application (FSRU-Linked Operations, FLNG, LNG Bunkering, Transshipment Hubs), By Vessel Type (Q-Flex & Q-Max, Standard LNG Carriers, Small-Scale LNG Vessels), By Service Type Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The LNG ship-to-ship transfer equipment market was valued at USD 1.82 Billion in 2025 and is forecast to reach USD 3.41 Billion by 2034, representing a CAGR of 7.2% over the 2026–2034 forecast period.

- Segment Dominance: Cryogenic hose assemblies held the largest product-type share at 38.4% in 2025, generating USD 0.70 Billion in revenue, driven by their mandatory role in every STS LNG transfer operation.

- Segment Dominance: FSRU-related STS operations accounted for 44.2% of total application demand in 2025, reflecting the global fleet expansion of floating storage and regasification units as countries prioritise energy security.

- Driver: Global LNG trade volume growth, projected to add 180 million tonnes per annum (MTPA) of new supply between 2025 and 2034 per IEA estimates, directly expands the addressable STS equipment service market by an estimated USD 0.9 Billion.

- Restraint: High capital expenditure per STS equipment set, averaging USD 4.2 Million for a complete cryogenic hose and fender package, limits adoption by smaller independent operators and emerging market terminal companies.

- Opportunity: Expansion of Caribbean and West African LNG transshipment hubs represents an estimated USD 380 Million incremental equipment procurement opportunity through 2034, as new FSRU deployments require dedicated STS infrastructure.

- Trend: Adoption of IoT-integrated monitoring systems for cryogenic hose pressure and fender compression reached 28.6% of new equipment orders in 2025, up from 9.4% in 2021, and is forecast to exceed 65% of orders by 2034.

- Regional Analysis: Asia Pacific led global demand with a 36.8% market share in 2025, generating USD 0.67 Billion in revenue, underpinned by Japan and South Korea operating the highest combined FSRU fleet count of any regional bloc.

Competitive Landscape Overview

The LNG ship-to-ship transfer equipment market is moderately consolidated, with the top four suppliers collectively commanding approximately 54% of global revenue in 2025. LMC (Liquid Marine Connectors), Trelleborg Marine & Infrastructure, Yokohama Rubber Co., and Cavotec SA anchor the competitive field through proprietary cryogenic engineering capabilities and classification-society-certified product portfolios. Competition is primarily technology-driven, centred on product safety certification (DNV, Lloyd's Register, Bureau Veritas), operational reliability metrics, and after-sales service network coverage across key LNG trade routes. Competitive intensity increased sharply between 2023 and 2025 as three new entrants from South Korea and China moved to capture APAC FSRU procurement contracts, pressing incumbents to accelerate R&D cycles and formalise regional service agreements.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Solution | Geographic Strength | Recent Strategic Move |

| LMC (Liquid Marine Connectors) | Norway | Leader | KLAW STS Coupler System | Europe / Middle East | Expanded UAE service depot; launched KLAW 16" rapid-connect coupler (Jan 2025) |

| Trelleborg Marine & Infrastructure | Sweden | Leader | TFX STS Fender Systems | North America / Europe | Acquired UK-based Dunlop Oil & Marine fender assets, boosting STS segment capacity (Mar 2025) |

| Yokohama Rubber Co. | Japan | Leader | Super Cone STS Pneumatic Fenders | Asia Pacific | Opened new 40,000 MT/yr fender manufacturing plant in Hiroshima (Jun 2025) |

| Cavotec SA | Switzerland | Challenger | MoorMaster Automated Mooring System | Europe / Asia Pacific | Secured USD 28M contract for LNG STS mooring systems across three Qatari terminals (Sep 2025) |

| BV Valmarine | France | Challenger | STS Hose Loading Arms & Manifolds | Europe / Latin America | Partnered with Petrobras for Santos pre-salt STS equipment supply agreement (Jan 2026) |

| Gall Thomson Environmental | UK | Niche Player | Breakaway Couplings for STS | Europe | Launched enhanced 16-bar rated KBCV coupler line for LNG STS duty (Feb 2025) |

| ITT Bornemann | Germany | Niche Player | Cryogenic Pump Systems | Europe / Middle East | Won supply contract for cryogenic STS transfer pumps at Wilhelmshaven LNG terminal (Apr 2025) |

| Vopak Terminal Services | Netherlands | Niche Player | STS Operations & Equipment Leasing | Global | Extended STS equipment leasing contracts across five Asian LNG hubs (Nov 2025) |

By Product Type

Cryogenic hose assemblies represented the largest product type segment of the LNG ship-to-ship transfer equipment market, commanding a 38.4% share and USD 0.70 Billion in revenue in 2025. These composite hoses, constructed with stainless steel interlock convolutions and multi-layer cryogenic insulation rated for liquid temperatures down to -165°C, are the primary fluid transfer medium in every STS LNG operation. Demand is structurally tied to fleet utilisation and cargo frequency. Japan and South Korea together accounted for nearly 40% of global cryogenic hose procurement in 2025, driven by import terminal density and FSRU fleet expansion. Manufacturers are advancing composite inner layer materials to extend service life from the current industry average of 10 years toward 15 years, which reduces lifecycle cost per operation and increases competitiveness in long-duration fleet supply contracts. The cryogenic hose segment is projected to sustain a 7.5% CAGR through 2034 as FSRU deployments continue outpacing fixed terminal construction in emerging import markets.

Pneumatic and foam-filled fender systems held a 27.1% share of the LNG STS transfer equipment market in 2025, generating approximately USD 0.49 Billion. Fenders absorb kinetic energy during vessel approach and maintain safe separation throughout the transfer, making them safety-critical components subject to OCIMF Equipment Guidelines and ISO 17357 standards. The 4.0-metre and 4.5-metre diameter product grades dominated procurement volumes, reflecting the beam widths of standard Q-Flex and Q-Max LNG carriers operating out of Qatar and Australia. Foam-filled variants are gaining share over pneumatic models in weather-exposed anchorage locations given their lower maintenance burden and immunity to deflation risk. The fender segment is projected to grow at 6.8% CAGR through 2034, supported by fleet expansion and periodic replacement demand estimated at USD 18 Million per year industry-wide.

Mooring systems, emergency release couplings (ERCs), and manifold adaptors collectively accounted for the remaining 34.5% of product-type revenue in 2025. Mooring systems held 18.3% share, as automated mooring technology from suppliers such as Cavotec reduces crew exposure during STS operations and is increasingly mandated by SIRE 2.0 inspection frameworks. Emergency release couplings commanded a 9.8% share, driven by regulatory requirements that every LNG STS operation must have a dry-break ERC rated to full operating pressure. Manifold adaptors and vapour return equipment made up the balance at 6.4%, with growth driven by compatibility requirements as fleet vessel specifications diversify across different builder generations.

By Application

FSRU-linked STS transfer operations constituted the dominant application segment, representing 44.2% of total LNG STS equipment demand and USD 0.80 Billion in market revenue in 2025. The global FSRU fleet reached 52 operational units in 2025, with an additional 18 units under construction per vessel tracking data compiled from Lloyd's List Intelligence, and each new unit requires a complete set of STS transfer equipment worth USD 3.5 Million to USD 5.0 Million at initial commissioning. The FSRU application segment is forecast to grow at 8.1% CAGR through 2034 as emerging import nations in Southeast Asia, South Asia, and East Africa adopt FSRUs as the fastest path to LNG import infrastructure, bypassing decade-long fixed terminal construction timelines.

Floating LNG (FLNG) production vessel applications held a 22.7% share in 2025. FLNG vessels such as Shell's Prelude and PETRONAS' PFLNG Dua require STS equipment capable of operating in open-ocean swell conditions, imposing higher specification requirements on fender systems and cryogenic hoses than sheltered anchorage FSRU transfers. Equipment for FLNG duty commands a 15% to 25% price premium over standard FSRU-grade products. New FLNG projects awarded between 2023 and 2025 in the Mozambique, Tanzanian, and North American deepwater basins will generate an estimated USD 210 Million in STS equipment procurement through 2030.

Ship-to-ship LNG bunkering applications accounted for 18.9% of equipment demand in 2025, a share that has grown from 8.3% in 2020, reflecting the rapid adoption of LNG as a marine fuel following the IMO 2020 sulphur cap. LNG bunkering STS equipment operates at smaller transfer volumes and lower manifold pressures than production transfer duty, enabling lighter and more standardised product specifications. Singapore, Rotterdam, and Zeebrugge collectively processed over 60% of global LNG bunkering STS volumes in 2025. Transshipment hub STS operations made up the remaining 14.2%, concentrated in the Caribbean and Mediterranean trade lanes where mid-size LNG carriers offload to smaller shuttle vessels for final delivery to terminals with draught or throughput constraints.

By Vessel Type Compatibility

Q-Flex and Q-Max carrier-compatible equipment represented 36.5% of the market in 2025, the highest single vessel-compatibility category, reflecting the dominant role of Qatari LNG supply in global trade. Equipment certified for these large-beam vessels requires fender diameters of 4.0 metres or greater and hose inner diameters of 12 to 16 inches to handle transfer rates above 10,000 cubic metres per hour. Standard LNG carrier-compatible equipment (145,000 to 165,000 cbm class) held 41.8% share in 2025, forming the broadest base of demand given its applicability across the majority of operating vessels. Small-scale LNG and bunkering vessel equipment held the remaining 21.7%, the fastest-growing sub-segment at an estimated 9.4% CAGR through 2034, driven by LNG bunkering fleet growth and coastal short-sea trade electrification programmes in Europe and Asia.

Regional Analysis

| Region | Share (2025) | Revenue (USD B) | Key Countries |

| Asia Pacific | 36.8% | 0.67 | Japan, South Korea, China, Australia |

| Middle East & Africa | 25.4% | 0.46 | Qatar, UAE, Saudi Arabia, Nigeria |

| Europe | 20.1% | 0.37 | Norway, UK, Netherlands, Belgium |

| North America | 12.6% | 0.23 | United States, Canada, Mexico |

| Latin America | 5.1% | 0.09 | Brazil, Argentina, Trinidad & Tobago |

Asia Pacific

Asia Pacific dominated the LNG ship-to-ship transfer equipment market with a 36.8% share and USD 0.67 Billion in revenue in 2025. Japan remains the world's second-largest LNG importer and its FSRU and floating storage unit fleet is the most dense of any single country outside Qatar, creating sustained replacement and expansion equipment demand. South Korea, the third-largest LNG importer globally, hosts an FSRU leasing industry servicing Southeast Asian buyers that generates recurring STS equipment procurement cycles. China's LNG imports rose 12.4% year-on-year in 2024 per General Administration of Customs data, expanding the demand base for both fixed-terminal-linked and offshore STS operations. Australia, as the world's largest or second-largest LNG exporter depending on the year, relies on STS capability at Darwin and near-field Prelude operations, sustaining fender and hose replacement demand. Regional governments, particularly in Vietnam, the Philippines, and Bangladesh, are financing new FSRU import terminals under energy security frameworks, adding 8 to 12 new FSRU deployments expected between 2025 and 2028 that will each require full STS equipment packages.

Middle East & Africa

The Middle East & Africa region held a 25.4% share of the LNG STS transfer equipment market in 2025, generating USD 0.46 Billion. Qatar is the anchor market, operating the world's largest LNG export infrastructure and conducting the highest volume of offshore STS lightering operations among any single producer. QatarEnergy's North Field expansion programme, targeting output growth from 77 MTPA to 142 MTPA by 2030, requires extensive STS equipment procurement across its offshore transfer fleet. The UAE's Jebel Ali and Fujairah terminals serve as regional LNG transshipment hubs, adding incremental equipment demand from hub STS activities. Nigeria's FLNG assets, including the ENI-operated Coral Sul, generate ongoing STS equipment procurement given their open-ocean transfer profiles. South Africa's FSRU tender at Richards Bay, awarded in 2024, represents an emerging procurement centre. Equipment investment across the region is supported by NOC capital expenditure commitments from Saudi Aramco, ADNOC, and SONATRACH for gas infrastructure expansion through 2030.

Europe

Europe accounted for 20.1% of global LNG STS transfer equipment market revenue in 2025, generating USD 0.37 Billion. The region's LNG import infrastructure expanded dramatically between 2022 and 2025 as European buyers redirected supply from pipeline Russian gas to Atlantic Basin and Middle Eastern LNG cargoes. Norway, as both a leading equipment manufacturer base and a growing LNG exporter, anchors the regional supplier community. The UK's Isle of Grain and South Hook terminals handle STS-linked FSRU operations in the Thames Estuary and Milford Haven waters respectively, driving equipment procurement from UK-flag vessel operators. The Netherlands' Gate terminal at Rotterdam and Belgium's Zeebrugge terminal together processed approximately 22% of European LNG import volumes in 2025, sustaining high STS equipment utilisation rates. Regulatory activity from the European Maritime Safety Agency (EMSA) on STS best practice guidelines for LNG, updated in 2024, is harmonising specification standards across EU member state operators, creating predictable procurement cycles for certified equipment suppliers with EMSA-recognised test reports.

North America

North America held a 12.6% share and USD 0.23 Billion in LNG STS transfer equipment market revenue in 2025, but the region is forecast to record the highest growth rate of any market through 2034, driven by Gulf of Mexico FLNG project startups and Caribbean transshipment hub development. The United States is now the world's largest LNG exporter after Sabine Pass, Corpus Christi, and Freeport LNG plant expansions, and new offshore FLNG permits issued by BSEE between 2023 and 2025 anticipate 3 to 5 new floating production vessels entering service before 2030. Each offshore FLNG vessel requires STS-capable transfer infrastructure for shuttle tanker loading, generating USD 4 Million to USD 6 Million in initial equipment investment per unit. Trinidad and Tobago's Atlantic LNG facility uses STS operations as a routine logistical tool for partial cargo consolidation, while Mexico's Pacific Coast LNG development projects anticipate STS transfer as the primary export mechanism given terminal draught limitations. Canada's LNG Canada export terminal in British Columbia, which commenced operations in 2025, adds a further procurement anchor in the Western Canadian basin.

Latin America

Latin America held a 5.1% share of the LNG STS transfer equipment market in 2025, generating USD 0.09 Billion, but represents a high-growth frontier market through 2034. Brazil anchors regional demand through Petrobras offshore operations and the country's six operational FSRU terminals, each requiring periodic STS equipment maintenance and replacement. Argentina's floating regasification infrastructure, operated through the national gas utility, added two new FSRU contracts in 2024 and 2025, increasing equipment procurement demand in the region by an estimated 18%. Trinidad and Tobago, classified within the Latin America coverage for this report, generates above-regional-average equipment utilisation rates at the Point Fortin export terminal. The Caribbean LNG transshipment hub concept, with multiple sites under evaluation between Puerto Rico and the Dominican Republic, could transform the region into a major STS equipment demand centre by 2030 if commercial agreements are finalised with Atlantic Basin LNG exporters targeting non-traditional markets.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Cryogenic Hose Assemblies

- Pneumatic & Foam-Filled Fenders

- Mooring Systems

- Emergency Release Couplings (ERCs)

- Manifold Adaptors & Vapour Return Equipment

By Application

- FSRU-Linked STS Operations

- FLNG Production Vessel Operations

- LNG Ship-to-Ship Bunkering

- Transshipment Hub STS Operations

By Vessel Type Compatibility

- Q-Flex & Q-Max LNG Carriers

- Standard LNG Carriers (145,000–165,000 cbm)

- Small-Scale LNG & Bunkering Vessels

By Service Type

- Equipment Supply & Manufacturing

- Equipment Leasing & Charter

- After-Sales Maintenance & Inspection

- Training & Certification Services

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.82 B |

| Forecast Revenue (2034) | USD 3.41 B |

| CAGR (2025-2034) | 7.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Cryogenic Hose Assemblies, Pneumatic & Foam-Filled Fenders, Mooring Systems, Emergency Release Couplings (ERCs), Manifold Adaptors & Vapour Return Equipment), By Application, (FSRU-Linked STS Operations, FLNG Production Vessel Operations, LNG Ship-to-Ship Bunkering, Transshipment Hub STS Operations), By Vessel Type Compatibility, (Q-Flex & Q-Max LNG Carriers, Standard LNG Carriers (145,000–165,000 cbm), Small-Scale LNG & Bunkering Vessels), By Service Type, (Equipment Supply & Manufacturing, Equipment Leasing & Charter, After-Sales Maintenance & Inspection, Training & Certification Services) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LMC (LIQUID MARINE CONNECTORS), TRELLEBORG MARINE & INFRASTRUCTURE, YOKOHAMA RUBBER CO., CAVOTEC SA, BV VALMARINE, GALL THOMSON ENVIRONMENTAL, ITT BORNEMANN, VOPAK TERMINAL SERVICES, ELAFLEX HIBY, EMCO WHEATON, CRYOFAB, WIRETECHNIK, SIRIUS MARINE SERVICES, TORGY LNG, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

Transfer Equipment Market Size, Share, Growth & Industry Analysis By Product Type (Cryogenic Hose Assemblies, Pneumatic & Foam-Filled Fenders, Mooring Systems, Emergency Release Couplings, Manifold Adaptors & Vapour Return Equipment), By Application (FSRU-Linked Operations, FLNG, LNG Bunkering, Transshipment Hubs), By Vessel Type (Q-Flex & Q-Max, Standard LNG Carriers, Small-Scale LNG Vessels), By Service Type Industry Trends & Forecast 2026–2034")

Transfer Equipment Market Size, Share, Growth & Industry Analysis By Product Type (Cryogenic Hose Assemblies, Pneumatic & Foam-Filled Fenders, Mooring Systems, Emergency Release Couplings, Manifold Adaptors & Vapour Return Equipment), By Application (FSRU-Linked Operations, FLNG, LNG Bunkering, Transshipment Hubs), By Vessel Type (Q-Flex & Q-Max, Standard LNG Carriers, Small-Scale LNG Vessels), By Service Type Industry Trends & Forecast 2026–2034")

Transfer Equipment Market Size, Share, Growth & Industry Analysis By Product Type (Cryogenic Hose Assemblies, Pneumatic & Foam-Filled Fenders, Mooring Systems, Emergency Release Couplings, Manifold Adaptors & Vapour Return Equipment), By Application (FSRU-Linked Operations, FLNG, LNG Bunkering, Transshipment Hubs), By Vessel Type (Q-Flex & Q-Max, Standard LNG Carriers, Small-Scale LNG Vessels), By Service Type Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the LNG Ship-to-Ship Transfer Equipment Market?

Global LNG STS transfer equipment market valued at USD 1.70B in 2024, reaching USD 3.41B by 2034, growing at a CAGR of 7.2% from 2026–2034.

Who are the major players in the LNG Ship-to-Ship Transfer Equipment Market?

LMC (LIQUID MARINE CONNECTORS), TRELLEBORG MARINE & INFRASTRUCTURE, YOKOHAMA RUBBER CO., CAVOTEC SA, BV VALMARINE, GALL THOMSON ENVIRONMENTAL, ITT BORNEMANN, VOPAK TERMINAL SERVICES, ELAFLEX HIBY, EMCO WHEATON, CRYOFAB, WIRETECHNIK, SIRIUS MARINE SERVICES, TORGY LNG, OTHERS

Which segments covered the LNG Ship-to-Ship Transfer Equipment Market?

By Product Type, (Cryogenic Hose Assemblies, Pneumatic & Foam-Filled Fenders, Mooring Systems, Emergency Release Couplings (ERCs), Manifold Adaptors & Vapour Return Equipment), By Application, (FSRU-Linked STS Operations, FLNG Production Vessel Operations, LNG Ship-to-Ship Bunkering, Transshipment Hub STS Operations), By Vessel Type Compatibility, (Q-Flex & Q-Max LNG Carriers, Standard LNG Carriers (145,000–165,000 cbm), Small-Scale LNG & Bunkering Vessels), By Service Type, (Equipment Supply & Manufacturing, Equipment Leasing & Charter, After-Sales Maintenance & Inspection, Training & Certification Services)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

LNG Ship-to-Ship Transfer Equipment Market

Published Date : 14 Apr 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date