- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Long Duration Energy Storage Market Size, Share | CAGR 22.6%

Global Long Duration Energy Storage Market Size, Share, Growth Analysis By Technology (Pumped Hydro Storage, Flow Batteries, CAES, Thermal Energy Storage, Hydrogen-Based Storage, Iron-Air & Zinc-Air Systems), By Application (Grid Balancing, Renewable Integration, Microgrids, Ancillary Services), By Duration (4–8 Hours, Multi-Day, Seasonal Storage), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

|---|---|---|---|

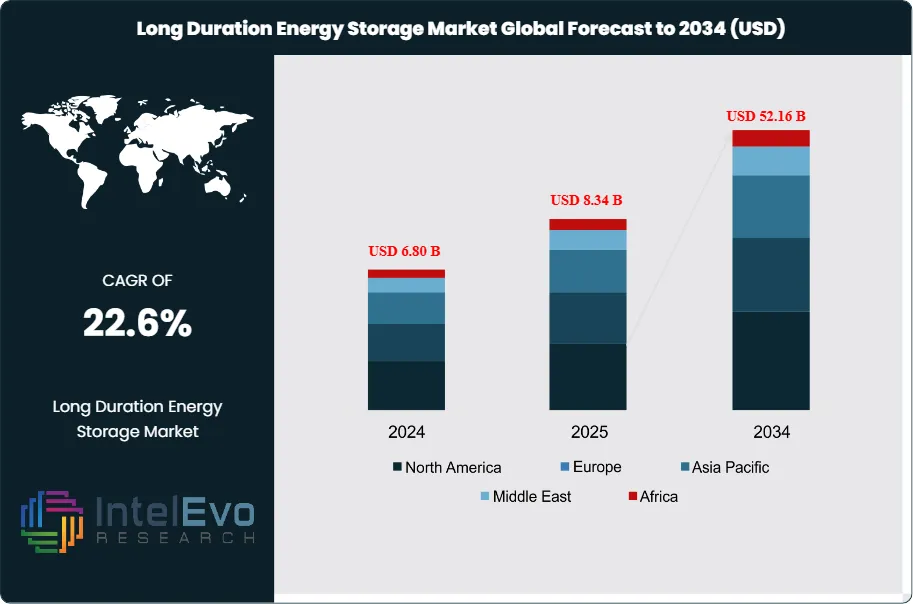

| USD 8.34 Billion | USD 52.16 Billion | 22.6% | Asia Pacific, 38.2% |

The Long Duration Energy Storage Market was valued at approximately USD 6.80 Billion in 2024 and reached USD 8.34 Billion in 2025. The market is projected to grow to USD 52.16 Billion by 2034, expanding at a CAGR of 22.6% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 43.82 Billion over the analysis period, reflecting the mounting urgency with which electricity grid operators, utilities, and energy ministries worldwide are confronting the core limitation of renewable energy: its temporal mismatch between generation and demand.

Get More Information about this report -

Request Free Sample ReportLong duration energy storage (LDES) is defined as storage systems capable of delivering electricity for durations of four hours or more, with the most strategically significant deployments targeting 8 to 24 hours and, for seasonal storage applications, durations of weeks to months. This distinguishes LDES from short-duration lithium-ion battery storage, which predominantly operates at two to four-hour discharge durations and is optimized for frequency regulation and peak shaving rather than the multi-hour grid balancing that LDES addresses. As renewable penetration in major electricity grids approaches and exceeds 50%, the intermittency problem transitions from a marginal balancing challenge to a fundamental grid architecture requirement, and LDES becomes the enabling infrastructure rather than an ancillary service.

The long duration energy storage market encompasses a diverse portfolio of technology platforms including pumped hydro storage, compressed air energy storage, flow batteries using vanadium, iron, zinc, and other chemistries, hydrogen-based storage through electrolysis and fuel cell reconversion, thermal energy storage using molten salt, sand, or other heat retention media, gravity-based mechanical storage, and advanced iron-air and zinc-air electrochemical systems. Each technology occupies a distinct position on the cost, duration, geographic suitability, and commercial maturity spectrum, and no single platform dominates across all application contexts.

Policy frameworks are accelerating LDES deployment at a pace that procurement and regulatory environments were not previously structured to support. The U.S. Inflation Reduction Act introduced a standalone Investment Tax Credit for energy storage of all durations, effective from 2023, eliminating the requirement that storage be co-located with renewable generation to qualify for tax incentives. The U.S. Department of Energy’s LDES Earthshot initiative targets a 90% reduction in the cost of LDES to USD 0.05 per kilowatt-hour of stored energy by 2030. The European Union’s revised Electricity Market Design regulation, adopted in 2024, requires member states to conduct LDES adequacy assessments and develop national storage procurement frameworks. China’s National Development and Reform Commission has mandated that new renewable energy projects above 100 MW include 20% capacity in energy storage with a minimum 4-hour duration, directly creating LDES procurement volume at gigawatt scale.

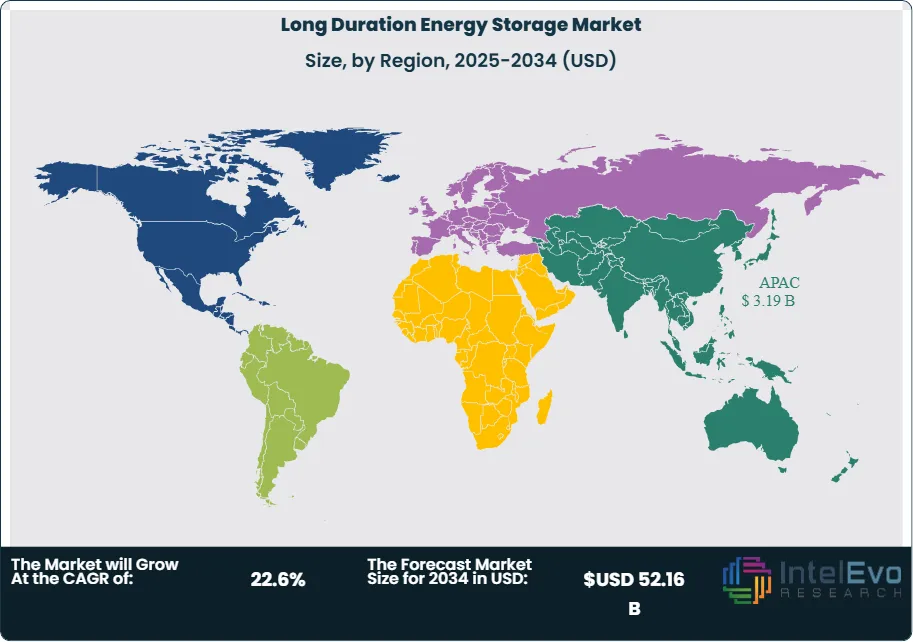

Asia Pacific leads the long duration energy storage market with a 38.2% share in 2025 at USD 3.19 Billion, anchored by China’s mandatory renewable-plus-storage policy and the world’s largest pumped hydro development program. North America accounts for 26.4% of the global market in 2025 at USD 2.20 Billion, with the Inflation Reduction Act’s storage ITC driving flow battery and emerging technology deployments. Europe holds 22.7% of global market share at USD 1.89 Billion, supported by the EU’s Electricity Market Design reform and national capacity market mechanisms incorporating storage.

, By Application (Grid Balancing, Renewable Integration, Microgrids, Ancillary Services), By Duration (4–8 Hours, Multi-Day, Seasonal Storage), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global long duration energy storage market was valued at USD 8.34 Billion in 2025 and is forecast to reach USD 52.16 Billion by 2034, expanding at a CAGR of 22.6% during the 2026–2034 forecast period.

- Segment Dominance: By technology, pumped hydro storage holds the largest share at 41.3% of the long duration energy storage market in 2025, reflecting its established commercial track record, multi-decade asset life, and unmatched capacity scale at sites with suitable topographic and hydrological characteristics.

- Segment Dominance: By application, grid-scale balancing and renewable integration represents the dominant application at 58.6% of the long duration energy storage market in 2025, driven by electricity grid operators’ urgent need to firm variable wind and solar generation output across daily and multi-day weather cycles.

- Driver: The International Energy Agency estimates that achieving net-zero electricity systems by 2050 requires over 10,000 GWh of long duration energy storage capacity globally, compared with approximately 1,400 GWh currently installed, implying a sevenfold capacity expansion that demands sustained annual deployment of 400 to 600 GWh across the 2025–2034 forecast period.

- Restraint: The absence of established long duration energy storage-specific revenue mechanisms in most electricity market structures limits project bankability, as LDES assets cannot reliably capture sufficient revenue from energy arbitrage alone to achieve investment-grade financial returns without capacity payment, ancillary service, or regulated rate-of-return revenue streams.

- Opportunity: Vanadium redox flow batteries, with installed costs projected to decline from approximately USD 400 per kilowatt-hour in 2025 to below USD 180 per kilowatt-hour by 2034 as manufacturing scale increases, represent a USD 9.8 Billion addressable market opportunity for deployments serving 8 to 24-hour grid balancing applications where their cycle life advantage over lithium-ion provides superior total cost of ownership.

- Trend: Iron-air and zinc-air electrochemical storage technologies, targeting cost structures below USD 20 per kilowatt-hour of storage capacity by leveraging earth-abundant materials, are advancing from demonstration to early commercial deployment in 2025, with Form Energy’s iron-air system and EOS Energy’s zinc-air platform securing utility procurement contracts for multi-day storage applications.

- Regional Analysis: Asia Pacific leads the global long duration energy storage market with a 38.2% share in 2025, representing USD 3.19 Billion, driven by China’s mandatory renewable-plus-storage policy framework and the world’s largest active pumped hydro construction program at over 270 GW of projects under development.

Competitive Landscape Overview

The long duration energy storage market is highly fragmented in 2025, with no single company controlling more than 14% of global market revenue across all technology segments. The top four players collectively account for approximately 38% of market share, a figure that rises to 55% within individual technology verticals such as pumped hydro engineering or vanadium flow batteries. Competitive dynamics differ substantially by technology: pumped hydro is dominated by a small number of large engineering and construction firms, flow batteries feature dedicated pure-play developers competing with diversified energy storage companies, and emerging technologies including iron-air, compressed air, and thermal storage are populated by venture-backed startups competing for utility pilot and early commercial contracts. Strategic capital from utilities, sovereign wealth funds, and infrastructure investors is flowing into LDES at an accelerating rate, with global LDES-specific investment exceeding USD 4.2 Billion in 2024 and 2025 combined. The competitive intensity at the project development level is increasing as multiple technology platforms compete for the same grid procurement tenders, with bankability, performance warranty, and levelized cost of storage becoming primary evaluation criteria.

Competitive Landscape Matrix

| Company | HQ | Market Position | Key Technology / Product | Geographic Strength | Recent Strategic Move (2024–2026) |

|---|---|---|---|---|---|

| Form Energy | USA | Leader (Emerging Tech) | Iron-air multi-day storage system | North America | Secured first commercial utility contract with Georgia Power for 15 MW iron-air system in 2024; raised USD 405 Million Series F to fund manufacturing scale-up in West Virginia. |

| Invinity Energy Systems | UK | Challenger | Vanadium flow battery systems | Europe, North America, APAC | Delivered largest UK vanadium flow battery installation in 2025; signed framework agreement with a U.S. utility for 200 MWh multi-project deployment. |

| ESS Inc. | USA | Challenger | Iron Flow Battery (all-iron chemistry) | North America, Europe | Signed 2 GWh long-term supply agreement with a European utility in 2025; achieved UL certification for its Energy Warehouse commercial product line. |

| EOS Energy Enterprises | USA | Challenger | Zinc-air ZNYTH battery | North America | Received USD 398 Million DOE loan guarantee in 2024 for Pennsylvania manufacturing facility; secured 200 MWh utility contract with a Midwest grid operator. |

| Highview Power | UK | Niche Player | CRYOBattery liquid air storage | Europe, North America | Broke ground on 50 MW / 250 MWh liquid air energy storage facility in UK in 2025; secured project financing with National Infrastructure Bank support. |

| Hydrostor | Canada | Niche Player | Advanced compressed air storage | North America, Australia | Reached financial close on 200 MW / 1,600 MWh California CAES project in 2025; secured 25-year offtake agreement with California ISO counterparty. |

| Sumitomo Electric | Japan | Niche Player | Vanadium redox flow battery | Asia Pacific, Europe | Commissioned 51 MWh vanadium flow battery system at Hokkaido grid in 2025; advanced European project pipeline with two grid operator framework agreements. |

| Antora Energy | USA | Niche Player | Thermal carbon block storage | North America | Secured USD 150 Million Series B in 2024; signed first industrial offtake agreement with a U.S. cement manufacturer for thermal energy storage delivering process heat. |

By Technology

The long duration energy storage market by technology is led by pumped hydro storage, which captured 41.3% of global revenue in 2025 at approximately USD 3.44 Billion. Pumped hydro remains the world’s largest and most commercially proven LDES technology, accounting for over 90% of the approximately 1,400 GWh of global installed LDES capacity as of 2025. Its dominance reflects multi-decade asset lives exceeding 50 years, round-trip efficiencies of 70 to 85%, gigawatt-scale capacity achievable at individual sites, and the absence of electrochemical degradation that limits cycle life in battery-based alternatives. China’s National Energy Administration has approved over 270 GW of pumped hydro projects for construction or development, representing the world’s largest single-country infrastructure investment program in any storage technology. Flow batteries, encompassing vanadium redox, iron flow, and zinc-based chemistries, represent the second-largest technology segment at 22.6% of the market in 2025 at USD 1.88 Billion, growing at above-average rates as manufacturing scale increases and cost per kilowatt-hour declines. Compressed air energy storage accounts for 11.4% at USD 951 Million, with advanced adiabatic CAES systems achieving higher round-trip efficiencies than earlier generation diabatic designs. Thermal energy storage, using molten salt, solid media, or phase-change materials, represents 12.8% of the market at USD 1.07 Billion, primarily deployed at concentrating solar power plants and industrial facilities. Hydrogen-based storage, iron-air, zinc-air, and other emerging electrochemical systems collectively account for the remaining 11.9% at USD 992 Million, growing at the highest rates from a small base as pilot and early commercial projects are commissioned.

By Application

The long duration energy storage market by application is dominated by grid-scale balancing and renewable integration, which represents 58.6% of global revenue in 2025 at USD 4.89 Billion. Grid operators deploying increasing proportions of wind and solar generation face multi-hour and multi-day imbalances between variable renewable output and demand patterns that short-duration lithium-ion storage cannot address cost-effectively. LDES systems providing 8 to 24-hour discharge durations fill the critical gap between intraday balancing served by lithium-ion and seasonal storage served by hydrogen or pumped hydro, enabling renewable penetration levels above 70 to 80% without gas peaker backup. Transmission and distribution deferral represents 14.7% of the market at USD 1.23 Billion, as utilities deploy LDES at strategically selected grid nodes to defer capital-intensive transmission infrastructure upgrades by managing peak demand periods. Commercial and industrial behind-the-meter storage accounts for 12.4% of the market at USD 1.03 Billion, with large energy consumers using LDES to manage time-of-use electricity cost structures and provide resilience against extended grid outages. Island and remote microgrid applications represent 9.6% at USD 801 Million, where LDES enables high renewable penetration in isolated grids that cannot rely on interconnected grid backup. Capacity market participation and ancillary services account for the remaining 4.7%.

By Duration

The long duration energy storage market by storage duration reflects the spectrum of grid and commercial needs that LDES technologies address at different timescales. The 4 to 8-hour duration segment represents 38.4% of market revenue in 2025 at USD 3.20 Billion, occupying the boundary between short-duration lithium-ion territory and true LDES applications. Systems in this duration range address the daily solar duck curve, the evening peak demand period when solar generation has ceased but air conditioning and other loads remain high, and are the most commercially active segment with the broadest technology competition. The 8 to 24-hour duration segment represents 34.7% of the market at USD 2.89 Billion, targeting the overnight storage requirement for solar energy generated during peak afternoon hours and the multi-hour wind lull balancing that grid operators increasingly prioritize. Multi-day storage, defined as 24 to 168-hour duration, accounts for 17.6% of the market at USD 1.47 Billion and is the fastest-growing duration segment as iron-air, compressed air, and hydrogen-based systems advance from demonstration to commercial deployment. Seasonal and long-term storage beyond one week represents 9.3% of the market at USD 776 Million, primarily served by pumped hydro facilities with very large reservoir volumes and hydrogen-based storage systems.

By End-User

The long duration energy storage market by end-user is primarily served by utility and grid operators, which account for 64.8% of global revenue in 2025 at USD 5.40 Billion. Vertically integrated utilities, independent power producers, and grid system operators are the primary procurement decision-makers for grid-scale LDES deployments, driven by renewable portfolio standard obligations, capacity market requirements, and system adequacy mandates. Independent power producers and renewable energy developers represent 17.3% of the market at USD 1.44 Billion, deploying LDES as a co-located asset to firm renewable power purchase agreements and improve the dispatchability premium achievable in merchant power markets. Industrial and commercial end-users account for 12.4% of the market at USD 1.03 Billion, primarily large manufacturing facilities, data center operators, and mining operations deploying behind-the-meter LDES for energy cost management and operational resilience. Government and military installations represent the remaining 5.5% at USD 459 Million, with defense agency energy security programs funding LDES deployments at critical facilities to eliminate dependence on grid power during extended outages.

Regional Analysis

Asia Pacific

Asia Pacific accounts for 38.2% of the global long duration energy storage market in 2025, representing USD 3.19 Billion, and is the dominant region by installed capacity, active development pipeline, and government policy ambition. China’s role is decisive: the National Development and Reform Commission’s mandate requiring new renewable energy projects above 100 MW to include storage with a minimum 4-hour duration has created a government-enforced LDES procurement market of approximately 40 to 60 GW annually. China’s pumped hydro development program, with over 270 GW of approved projects, dwarfs the combined pumped hydro pipeline of all other countries combined and will deliver the majority of global new LDES capacity additions through 2030. Chinese flow battery manufacturers including Rongke Power and Dalian Rongke have established the world’s largest vanadium redox flow battery manufacturing capacity, and the commissioning of a 800 MWh vanadium flow battery system in Dalian in 2023 established a benchmark for utility-scale flow battery deployment. Japan’s grid operator JERA and regional utilities are procuring LDES to support the government’s target of 36 to 38% renewable electricity by 2030, with Sumitomo Electric’s vanadium flow battery program and Hokkaido’s grid stabilization storage portfolio representing active deployment programs. Australia’s Snowy 2.0 pumped hydro project, targeting 2,000 MW of generation capacity with 350 GWh of storage, is the largest individual LDES infrastructure project in the Southern Hemisphere and is advancing toward commissioning through 2025 and 2026. India’s Ministry of New and Renewable Energy has issued LDES tenders under its grid-scale storage procurement program, with 4,000 MW of storage capacity targeted for procurement by 2026 to 2027.

North America

North America accounts for 26.4% of the global long duration energy storage market in 2025 at USD 2.20 Billion, and the United States represents the most policy-active LDES market outside China. The Inflation Reduction Act’s standalone Investment Tax Credit for energy storage, providing a 30% base credit rising to 50% with domestic content and energy community bonuses, has transformed the financial feasibility of LDES projects that previously could not achieve bankable returns from energy market revenues alone. The Department of Energy’s LDES Earthshot program and its associated loan guarantee portfolio, which has committed over USD 4.5 Billion in loan guarantees and grants to storage projects between 2022 and 2025, has supported early commercial deployments by Form Energy, EOS Energy, ESS Inc., and Hydrostor that are establishing U.S. commercial reference projects. California’s Long-Duration Storage Program, established under AB 2514 and subsequent legislation, mandates that investor-owned utilities procure 1,000 MW of LDES capacity by 2026, with contracts awarded to pumped hydro, compressed air, and flow battery projects. New York’s six gigawatt storage mandate includes LDES procurement requirements. Texas’ deregulated electricity market, which experienced the February 2021 winter storm grid failure, has prompted ERCOT and the state legislature to develop LDES incentive frameworks to address multi-day cold weather generation shortfalls. Canada contributes approximately 12% of the North American market, with British Columbia Hydro’s pumped storage program and Hydrostor’s Ontario project pipeline representing the primary capacity additions.

Europe

Europe represents 22.7% of the global long duration energy storage market in 2025 at USD 1.89 Billion, driven by the EU’s ambitious renewable energy targets and the Electricity Market Design reform’s storage adequacy provisions. The EU’s revised target of 42.5% renewable energy by 2030, increased from 32%, requires approximately 200 GW of additional renewable capacity additions and supporting grid flexibility infrastructure that LDES is designed to provide. Germany’s grid operator, facing the structural challenge of integrating over 130 GW of installed wind and solar capacity while phasing out nuclear and reducing gas dependence, has issued LDES procurement frameworks and capacity market mechanisms that include multi-hour storage. The United Kingdom’s Capacity Market has been modified to include LDES assets, and National Grid ESO has established a long-duration storage procurement pathway under the Review of Electricity Market Arrangements. Highview Power’s liquid air energy storage facility in the UK represents Europe’s most advanced emerging technology LDES project. France’s pumped hydro fleet, operated by EDF, provides 4.9 GW of LDES capacity, and France is developing compressed air and hydrogen-based storage projects supported by the France 2030 investment plan. The Nordic countries’ large pumped hydro heritage in Norway and Sweden, with over 35 GW of installed capacity, provides a natural flexibility resource that is being commercialized through European power market interconnections.

Latin America

Latin America represents 7.8% of the global long duration energy storage market in 2025 at USD 651 Million, a share anchored by the region’s exceptional pumped hydro natural resource endowment and growing renewable integration requirements. Chile is the leading market, with its northern Atacama Desert hosting one of the world’s highest solar irradiance resources and its Andean geography providing abundant pumped hydro development sites. Chile’s National Energy Commission has integrated LDES requirements into its renewable energy procurement tenders, and the country’s electricity system operator has identified specific grid nodes where LDES deployment would reduce curtailment of solar generation that currently reaches 20 to 30% in peak generation periods. Brazil’s electricity system, already heavily dependent on hydropower, is deploying LDES to manage the increasing variability introduced by wind and solar additions, with the National Electric Energy Agency including storage in its regular energy auction framework. Colombia and Peru have initiated LDES pilot project programs supported by Inter-American Development Bank financing. The region’s abundant renewable resources, combined with growing industrial demand for reliable low-carbon electricity from mining and mineral processing operations, create a compelling structural case for LDES investment that international developers including Hydrostor and infrastructure funds are beginning to target.

Middle East & Africa

Middle East & Africa accounts for 4.9% of the global long duration energy storage market in 2025 at USD 409 Million, with the region’s LDES market shaped by its unique combination of world-class solar resources, water scarcity constraints on pumped hydro, and the energy security imperatives of island and remote grid systems. Saudi Arabia’s NEOM project has specified LDES requirements for its 100% renewable electricity system, with compressed air, hydrogen-based storage, and advanced battery systems among the technologies under evaluation for multi-hour and multi-day storage at gigawatt scale. The UAE’s Masdar has become an active LDES project developer, investing in thermal energy storage and advanced battery projects across the Middle East and internationally. South Africa’s electricity system, facing chronic generation shortfalls and load-shedding, has prioritized LDES in its Integrated Resource Plan update, with the Department of Mineral Resources and Energy issuing storage-specific procurement rounds for 1,500 MW of storage capacity. Africa’s island nations and remote communities represent a distinct LDES market segment where the elimination of diesel generation dependence through high-renewable-plus-storage microgrids provides compelling economics that donors and development finance institutions are actively funding.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technology

- Pumped Hydro Storage

- Flow Batteries (Vanadium, Iron, Zinc)

- Compressed Air Energy Storage (CAES)

- Thermal Energy Storage

- Hydrogen-Based Storage

- Iron-Air and Zinc-Air Electrochemical Systems

By Application

- Grid-Scale Balancing and Renewable Integration

- Transmission and Distribution Deferral

- Commercial and Industrial Behind-the-Meter

- Island and Remote Microgrid

- Capacity Market and Ancillary Services

By Duration

- 4 to 8 Hours

- 8 to 24 Hours

- Multi-Day (24 to 168 Hours)

- Seasonal and Long-Term (Beyond One Week)

By End-User

- Utility and Grid Operators

- Independent Power Producers and Renewable Developers

- Industrial and Commercial End-Users

- Government and Military Installations

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.34 B |

| Forecast Revenue (2034) | USD 52.16 B |

| CAGR (2025-2034) | 22.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Pumped Hydro Storage, Flow Batteries (Vanadium, Iron, Zinc), Compressed Air Energy Storage (CAES), Thermal Energy Storage, Hydrogen-Based Storage, Iron-Air and Zinc-Air Electrochemical Systems), By Application, (Grid-Scale Balancing and Renewable Integration, Transmission and Distribution Deferral, Commercial and Industrial Behind-the-Meter, Island and Remote Microgrid, Capacity Market and Ancillary Services), By Duration, (4 to 8 Hours, 8 to 24 Hours, Multi-Day (24 to 168 Hours), Seasonal and Long-Term (Beyond One Week)), By End-User, (Utility and Grid Operators, Independent Power Producers and Renewable Developers, Industrial and Commercial End-Users, Government and Military Installations) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | FORM ENERGY, INVINITY ENERGY SYSTEMS, HYDROSTOR, EOS ENERGY ENTERPRISES, ESS INC., HIGHVIEW POWER, SUMITOMO ELECTRIC INDUSTRIES, RONGKE POWER, ANTORA ENERGY, ENERGY VAULT, GRAVITRICITY, SALIENT ENERGY, PRIMUS POWER, AMBRI, ENERVENUE, GENERAL ELECTRIC (PUMPED HYDRO DIVISION), ANDRITZ HYDRO, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Grid Balancing, Renewable Integration, Microgrids, Ancillary Services), By Duration (4–8 Hours, Multi-Day, Seasonal Storage), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Grid Balancing, Renewable Integration, Microgrids, Ancillary Services), By Duration (4–8 Hours, Multi-Day, Seasonal Storage), By End-User, Industry Trends & Forecast 2026-2034")

, By Application (Grid Balancing, Renewable Integration, Microgrids, Ancillary Services), By Duration (4–8 Hours, Multi-Day, Seasonal Storage), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Long Duration Energy Storage Market?

The Global Long Duration Energy Storage Market was valued at USD 6.80 Billion in 2024 and is projected to reach USD 52.16 Billion by 2034, growing at a CAGR of 22.6% from 2026 to 2034, driven by rising renewable energy integration, increasing demand for grid stability and energy resilience, advancements in flow battery and hydrogen storage technologies, and growing investments in clean energy infrastructure and decarbonization initiatives worldwide.

Who are the major players in the Long Duration Energy Storage Market?

FORM ENERGY, INVINITY ENERGY SYSTEMS, HYDROSTOR, EOS ENERGY ENTERPRISES, ESS INC., HIGHVIEW POWER, SUMITOMO ELECTRIC INDUSTRIES, RONGKE POWER, ANTORA ENERGY, ENERGY VAULT, GRAVITRICITY, SALIENT ENERGY, PRIMUS POWER, AMBRI, ENERVENUE, GENERAL ELECTRIC (PUMPED HYDRO DIVISION), ANDRITZ HYDRO, Others

Which segments covered the Long Duration Energy Storage Market?

By Technology, (Pumped Hydro Storage, Flow Batteries (Vanadium, Iron, Zinc), Compressed Air Energy Storage (CAES), Thermal Energy Storage, Hydrogen-Based Storage, Iron-Air and Zinc-Air Electrochemical Systems), By Application, (Grid-Scale Balancing and Renewable Integration, Transmission and Distribution Deferral, Commercial and Industrial Behind-the-Meter, Island and Remote Microgrid, Capacity Market and Ancillary Services), By Duration, (4 to 8 Hours, 8 to 24 Hours, Multi-Day (24 to 168 Hours), Seasonal and Long-Term (Beyond One Week)), By End-User, (Utility and Grid Operators, Independent Power Producers and Renewable Developers, Industrial and Commercial End-Users, Government and Military Installations)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Long Duration Energy Storage Market

Published Date : 22 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date