- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Luminescent Nanoparticle Market Size, Share & Forecast | CAGR 11.9%

Global Luminescent Nanoparticle Market Size, Share, Growth Analysis By Product Type (Quantum Dots, Carbon Quantum Dots, Upconversion Nanoparticles, Fluorescent Silica Nanoparticles, Perovskite Nanocrystals), By Application (Biomedical Imaging, Diagnostics, Display & Lighting, Solar Energy, Security & Anti-Counterfeiting, Drug Delivery, Environmental Monitoring), By End-Use Industry, Competitive Landscape, Technology Trends, Regional Outlook & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

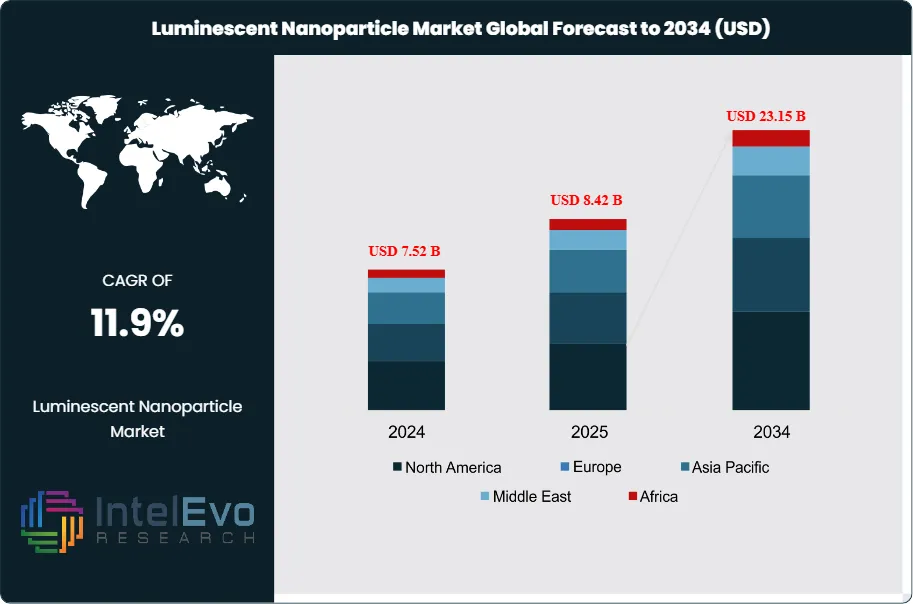

| USD 8.42 Billion | USD 23.15 Billion | 11.9% | North America, 36.2% |

The Luminescent Nanoparticle Market was valued at approximately USD 7.52 Billion in 2024 and reached USD 8.42 Billion in 2025. The market is projected to grow to USD 23.15 Billion by 2034, expanding at a CAGR of 11.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 14.73 Billion over the analysis period, underscoring the accelerating commercial adoption of luminescent nanoparticles across diagnostics, display technology, photovoltaics, and bioimaging applications.

Get More Information about this report -

Request Free Sample ReportLuminescent nanoparticles — including quantum dots (QDs), carbon quantum dots, upconversion nanoparticles (UCNPs), fluorescent silica nanoparticles, and perovskite nanocrystals — are gaining rapid traction due to their superior photostability, size-tunable optical properties, and high quantum yields compared to conventional fluorescent dyes. Industry analysis indicates that quantum dots held the largest product type share in 2025, accounting for approximately 44.1% of total luminescent nanoparticle revenue, driven by their entrenched role in consumer display panels and expanding use in next-wave in-vitro diagnostic (IVD) platforms. The convergence of nanotechnology with precision oncology has further accelerated demand, as luminescent nanoparticles are integral to sentinel lymph node mapping, tumor margin delineation, and multiplexed biomarker detection assays.

On the supply side, manufacturing cost reduction through continuous-flow synthesis reactors and improved ligand-exchange processes has lowered the per-gram production cost of high-purity quantum dots by an estimated 28% between 2021 and 2025, opening the luminescent nanoparticle market to mid-tier diagnostics manufacturers previously priced out of the segment. Regulatory evolution also shapes market access: the U.S. FDA's 2024 draft guidance on nanotechnology-based in-vitro diagnostics has provided clearer review pathways, while the EU's updated REACH framework has accelerated adoption of cadmium-free and heavy-metal-free luminescent nanoparticle formulations, particularly in Germany, France, and the Netherlands.

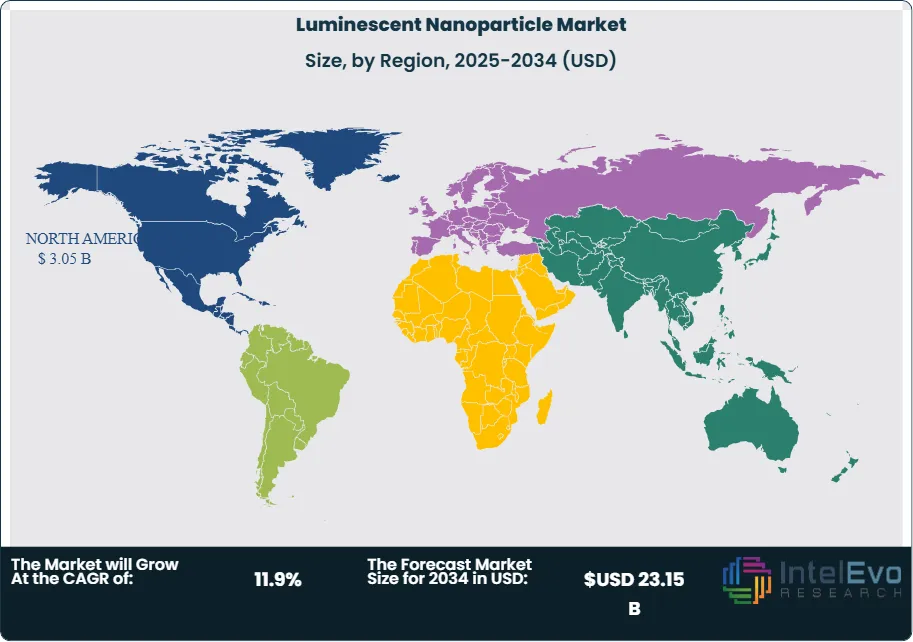

Regional investment patterns show North America leading with a 36.2% market share in 2025, supported by concentrated NIH funding in nanomedicine and robust VC deployment in biotech startups utilizing luminescent nanoparticles for liquid biopsy applications. Asia Pacific ranks second at 29.4%, with China's national semiconductor and display technology programs driving volume demand for display-grade quantum dots, and South Korea's panel manufacturers reinforcing supply chain depth. Europe holds 22.1%, where REACH compliance is steering innovation toward safer nanoparticle chemistries. Latin America and Middle East and Africa collectively account for 12.3%, with both regions showing accelerating demand through government-backed healthcare modernization programs. The luminescent nanoparticle market outlook through 2034 reflects a structurally favorable convergence of healthcare investment, display industry growth, and materials science advancement.

, By Application (Biomedical Imaging, Diagnostics, Display & Lighting, Solar Energy, Security & Anti-Counterfeiting, Drug Delivery, Environmental Monitoring), By End-Use Industry, Competitive Landscape, Technology Trends, Regional Outlook & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global luminescent nanoparticle market is projected to grow from USD 8.42 Billion in 2025 to USD 23.15 Billion by 2034, at a CAGR of 11.9% during the forecast period 2026–2034.

- Segment Dominance: By product type, quantum dots led the luminescent nanoparticle market in 2025 with a 44.1% revenue share, driven by high demand from display manufacturers and clinical diagnostics developers.

- Segment Dominance: By application, the biomedical imaging and diagnostics segment captured 38.7% of the luminescent nanoparticle market in 2025, reflecting accelerating adoption in cancer detection, immunoassays, and pathogen identification platforms.

- Driver: Escalating global investment in precision diagnostics and nanomedicine drove luminescent nanoparticle adoption; the global in-vitro diagnostics market surpassed USD 105 Billion in 2025, with nanoparticle-based assays representing a rapidly expanding sub-category.

- Restraint: Regulatory complexity surrounding nanoparticle toxicology assessment and inconsistent international classification standards constrained commercialization timelines, adding 12–18 months to average product approval cycles across major markets.

- Opportunity: The emerging application of luminescent nanoparticles in solar energy conversion, particularly as luminescent solar concentrators (LSCs), represents an addressable opportunity exceeding USD 2.8 Billion by 2034 as photovoltaic installations scale globally.

- Trend: Cadmium-free and heavy-metal-free luminescent nanoparticle formulations accounted for 31.6% of new product launches in 2025, a figure projected to exceed 60% by 2030 as REACH and RoHS compliance requirements tighten across the EU and increasingly in North America.

- Regional Analysis: North America dominated the luminescent nanoparticle market in 2025 with a 36.2% share, equating to USD 3.05 Billion in revenue, supported by concentrated federal research funding and a mature biotech commercialization pipeline.

Competitive Landscape Overview

The luminescent nanoparticle market is moderately consolidated, with the top four players — Thermo Fisher Scientific, Merck KGaA (MilliporeSigma), Nanoco Group, and Ocean NanoTech — collectively holding an estimated 48.3% combined revenue share in 2025. Competition is primarily technology-driven, with differentiation occurring along axes of quantum yield performance, particle size uniformity (measured in nm), surface functionalization breadth, and regulatory compliance credentials (cadmium-free, RoHS, REACH). M&A activity intensified in 2024 to 2025, as large life sciences and materials companies acquired specialty nanoparticle producers to gain proprietary synthesis IP and expand application-specific product portfolios.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Platform | Geographic Strength | Recent Strategic Move |

| Thermo Fisher Scientific | USA | Leader | Qdot Nanocrystals | North America | Jan 2025: expanded quantum dot production capacity by 30% at Eugene, OR facility. |

| Merck KGaA (MilliporeSigma) | Germany | Leader | Lumidot Quantum Dots | Europe | Mar 2025: launched 12 new perovskite nanoparticle grades for biomedical imaging. |

| Nanoco Group | UK | Challenger | CFQD Cadmium-Free QDs | Europe | Feb 2025: signed multi-year supply agreement with Samsung Display for display-grade QDs. |

| Ocean NanoTech | USA | Challenger | Fluorescent Silica NPs | North America | Apr 2025: partnered with NIH-funded consortium to supply nanoparticles for cancer diagnostics. |

| Evident Scientific (Olympus) | Japan | Niche Player | FluoSpheres Bioassay Particles | Asia Pacific | Jun 2025: integrated AI-guided fluorescence calibration into its nanoparticle imaging kits. |

| Sigma-Aldrich (Merck Group) | USA | Leader | Aldrich Quantum Dots | North America | May 2025: introduced 8 heavy-metal-free luminescent NP grades targeting EU REACH compliance. |

| PlasmaChem GmbH | Germany | Niche Player | PL-EGO Carbon QDs | Europe | Nov 2024: secured EUR-equivalent USD 18M Series B for scale-up of carbon quantum dot production. |

| Cytodiagnostix | USA | Niche Player | FluoroNP Bioconjugates | North America | Aug 2025: received FDA 510(k) clearance for luminescent NP-based lateral flow assay platform. |

By Product Type

Quantum dots remain the largest product type segment in the luminescent nanoparticle market, accounting for 44.1% of global revenue in 2025, equivalent to approximately USD 3.71 Billion. Their commercial dominance stems from exceptional molar extinction coefficients (typically 10 to 100 times greater than organic dyes), narrow emission linewidths (20–30 nm FWHM), and broad excitation spectra. In display applications, QD-enhanced LCD panels and direct-emissive QLED televisions drove volume demand, with major panel manufacturers in South Korea, China, and Japan consuming an estimated 85 metric tonnes of quantum dot material in 2025. In biomedical applications, QDs with surface bioconjugation (streptavidin, antibody, or oligonucleotide functionalization) are used in flow cytometry, FRET-based sensors, and multiplexed immunofluorescence assays. Cadmium-based QDs (CdSe/ZnS) still held 62% of QD revenue in 2025 but face progressive displacement by indium phosphide (InP) and silicon-based variants as regulatory pressure mounts in the EU and California.

Upconversion nanoparticles (UCNPs) represented 18.6% of the luminescent nanoparticle market in 2025, valued at USD 1.57 Billion. UCNPs — typically lanthanide-doped NaYF4 or NaGdF4 matrices — convert near-infrared excitation into visible or UV emission, enabling background-free detection in complex biological matrices. Their adoption in lateral flow assay (LFA) platforms for point-of-care diagnostics accelerated sharply post-2022, as manufacturers sought alternatives to colloidal gold with superior sensitivity at low analyte concentrations. Government programs in China under the 14th Five-Year Plan specifically funded UCNP synthesis scale-up for domestic diagnostics manufacturers, supporting a regional CAGR exceeding the global average in this sub-segment.

Fluorescent silica nanoparticles accounted for 16.2% of revenue in 2025 (USD 1.36 Billion), benefiting from their well-established biocompatibility, straightforward surface chemistry (via silane coupling agents), and compatibility with standard fluorescence microscopy platforms. They are widely used in cell tracking, drug delivery visualization, and environmental sensor arrays. Carbon quantum dots, the fastest-growing sub-segment, held 12.4% market share in 2025 but are projected to reach 19.1% by 2034, driven by their low toxicity, photostability, and scalable synthesis from bio-derived precursors such as citric acid and urea. Perovskite nanocrystals and other emerging luminescent NP types collectively comprised the remaining 8.7%, with perovskites attracting significant R&D interest for ultra-narrow emission display applications despite ongoing stability and lead content challenges.

By Application

Biomedical imaging and diagnostics represented the dominant application in the luminescent nanoparticle market, capturing 38.7% of global revenue in 2025 (USD 3.26 Billion). This segment encompasses in-vitro diagnostic assays, in-vivo fluorescence imaging, pathogen detection, and companion diagnostic platforms for oncology therapeutics. The U.S. National Cancer Institute's sustained funding — exceeding USD 800 Million annually directed toward nanotechnology-enabled cancer diagnostics — has been a primary catalyst for clinical adoption. Lateral flow assays incorporating luminescent nanoparticles demonstrated sensitivity improvements of 10 to 100-fold over gold nanoparticle-based formats in peer-reviewed validation studies, accelerating their integration into point-of-care platforms for infectious disease and cardiac biomarker testing.

Display and lighting applications represented 28.3% of the luminescent nanoparticle market in 2025 (USD 2.38 Billion). Quantum dot films, tubes, and direct-emissive structures are now standard in premium consumer electronics, with global shipments of QD-enhanced displays exceeding 42 million units in 2025. The transition from QD enhancement films to electroluminescent QLED and QD-OLED hybrid architectures is driving demand for narrower-emission, higher-purity nanoparticle grades from display integrators. Solar energy applications — including luminescent solar concentrators, photovoltaic downconverters, and spectral-converting coatings — held 14.2% of the market in 2025, with growing government mandates for building-integrated photovoltaics (BIPV) supporting a projected CAGR of 14.6% through 2034 in this vertical.

Security and anti-counterfeiting applications accounted for 9.4% of luminescent nanoparticle market revenue in 2025 (USD 0.79 Billion), as central banks, pharmaceutical packagers, and premium brand owners adopted covert luminescent tagging for authentication. Drug delivery and theranostics comprised 6.8% of the market, with nanoparticle-photosensitizer conjugates used in photodynamic therapy for superficial cancers. Environmental monitoring and agricultural sensing applications collectively made up the remaining 2.6%, representing early-stage adoption but with a compound growth rate approximately 1.8 times the overall market average due to growing regulatory requirements for water quality monitoring and pesticide residue detection.

By End-Use Industry

The healthcare and life sciences industry accounted for the largest end-use share in the luminescent nanoparticle market in 2025, contributing 45.8% of global revenue. This figure encompasses hospitals, clinical laboratories, pharmaceutical manufacturers, and academic medical centers purchasing luminescent nanoparticle-based reagents, kits, and imaging agents. The consumer electronics industry represented 26.4% of market revenue in 2025, primarily through display panel manufacturers and LED lighting integrators sourcing quantum dot materials. Energy sector end-users — including solar panel manufacturers, energy storage researchers, and utility companies deploying smart metering solutions — contributed 11.2%. Defense and security end-users accounted for 8.3%, with governments procuring luminescent nanoparticle-based authentication materials for currency, identity documents, and secure communications hardware. The remaining 8.3% was distributed across agriculture, environmental services, and industrial process monitoring end-users, segments characterized by nascent but accelerating adoption as performance-cost thresholds are crossed.

Regional Analysis

North America Luminescent Nanoparticle Market

North America led the global luminescent nanoparticle market in 2025 with a 36.2% share and USD 3.05 Billion in revenue. The United States accounted for approximately 91% of regional revenue, supported by a concentrated biotech cluster in Massachusetts, California, and the Research Triangle, where luminescent nanoparticles are embedded in liquid biopsy, single-molecule detection, and high-content screening workflows. Federal funding through the NIH National Cancer Institute, the NSF, and DARPA's biological technologies office directed over USD 1.1 Billion toward nanotechnology research in fiscal year 2025, of which an estimated 22% specifically touched luminescent nanomaterial applications. The FDA's 2024 draft guidance on nanotechnology-based in-vitro diagnostics provided clearer regulatory pathways, reducing developer uncertainty and accelerating pre-submission engagement from diagnostic companies. Canada contributed 7% of regional revenue, with the University of Toronto and National Research Council of Canada sustaining active quantum dot and UCNP research programs that feed into commercialization pipelines. Mexico holds early-stage manufacturing capacity for lower-complexity fluorescent silica nanoparticle formats, primarily serving domestic agricultural and food safety testing applications. North America luminescent nanoparticle demand is projected to maintain above-average growth through 2034, with biomedical diagnostics and solar energy conversion applications as the primary incremental revenue drivers.

Europe Luminescent Nanoparticle Market

Europe held a 22.1% share of the global luminescent nanoparticle market in 2025, equivalent to USD 1.86 Billion. Germany is the largest single country market in the region, driven by its strength in precision instrumentation, automotive display technology, and a highly active pharmaceutical sector requiring nanoparticle-based assay reagents. German institutions and Mittelstand manufacturers invested an estimated EUR 420 Million (approximately USD 460 Million) in nanotechnology R&D in 2025, with luminescent nanoparticles representing a meaningful sub-category. The UK sustained leadership in UCNP research through university spinouts, particularly from Oxford and Cambridge, with several companies transitioning from lab-scale to pilot production by 2025. France concentrated investment in perovskite nanocrystal research for photovoltaic applications through the CEA's INES solar energy institute. REACH regulation's restriction on cadmium compounds (Annex XVII) has been a defining supply-side force across Europe, compelling manufacturers to accelerate development of cadmium-free InP and carbon QD alternatives. European luminescent nanoparticle market growth is projected at approximately 10.8% CAGR through 2034, slightly below the global average, as regulatory compliance costs constrain product development timelines for smaller manufacturers.

Asia Pacific Luminescent Nanoparticle Market

Asia Pacific held 29.4% of the global luminescent nanoparticle market in 2025 with USD 2.48 Billion in revenue, and is the fastest-growing region with a projected CAGR of 14.2% through 2034. China dominates regional demand, accounting for approximately 52% of Asia Pacific revenue in 2025, driven by massive state-backed investment in semiconductor display technology, domestic diagnostics manufacturing under the 14th and upcoming 15th Five-Year Plans, and an aggressive push to achieve self-sufficiency in quantum dot material supply chains. South Korea's display panel manufacturers — particularly Samsung Display and LG Display — drive substantial quantum dot consumption, with both companies accelerating development of QD-OLED architectures that require tighter particle size distributions and higher quantum yield specifications. Japan contributed approximately 12% of regional revenue in 2025 through its strength in high-purity fluorescent nanoparticle reagents for analytical chemistry and its mature LED lighting retrofit market. India represented approximately 8% of regional revenue but is gaining momentum through government-funded nanotechnology centers under the National Nanotechnology Initiative (NNI-India) and increasing pharmaceutical sector interest in nanoparticle-based diagnostic kits manufactured domestically to reduce import dependence.

Latin America Luminescent Nanoparticle Market

Latin America accounted for 7.1% of the global luminescent nanoparticle market in 2025, representing USD 0.60 Billion in revenue. Brazil dominated the regional market with approximately 58% of Latin American revenue, supported by federal investment through FINEP (Financiadora de Estudos e Projetos) in nanotechnology research at institutions including the University of Campinas (UNICAMP) and the Brazilian Center for Physics Research (CBPF). The Brazilian healthcare system's expansion of diagnostic laboratory infrastructure under the Unified Health System (SUS) created incremental demand for luminescent nanoparticle-based diagnostic kits, particularly for dengue and Chagas disease detection using lateral flow assay formats. Mexico represented approximately 24% of regional revenue in 2025, with luminescent nanoparticle demand driven by maquiladora-linked electronics manufacturing and growing pharmaceutical sector investment in near-border manufacturing facilities. Argentina contributed approximately 11% of regional revenue, anchored by its biotech research base and nascent UCNP adoption in academic research programs. Latin America luminescent nanoparticle market growth is projected at 12.4% CAGR through 2034, with diagnostics and agricultural sensor applications serving as primary growth pillars.

Middle East and Africa Luminescent Nanoparticle Market

The Middle East and Africa region contributed 5.2% of global luminescent nanoparticle market revenue in 2025 (USD 0.44 Billion), representing the smallest regional share but with a projected CAGR of 13.1% through 2034. The UAE is the most advanced market in the region, with government investments under Abu Dhabi's National Strategy for Advanced Technologies directing capital toward nanotechnology research at Khalifa University and through the Advanced Technology Research Council (ATRC). Saudi Arabia's Vision 2030 healthcare modernization initiative has increased hospital laboratory procurement budgets significantly, with diagnostic laboratories upgrading to luminescent nanoparticle-based immunoassay analyzers to improve throughput and sensitivity. South Africa anchors the Sub-Saharan Africa segment, where luminescent nanoparticles are applied in HIV/TB rapid diagnostic applications and water quality monitoring programs supported by international development organizations. Israel, though geographically categorized within this region for trade purposes, operates a highly sophisticated nanotechnology research and commercialization environment, with companies like Applied Nanostructures advancing functionalized fluorescent nanoparticle platforms for security and biodefense applications. Infrastructure investment and growing public health modernization programs across the region will sustain above-average growth for the luminescent nanoparticle market through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Quantum Dots (Cadmium-Based)

- Quantum Dots (Cadmium-Free / InP / Silicon)

- Upconversion Nanoparticles (UCNPs)

- Fluorescent Silica Nanoparticles

- Carbon Quantum Dots

- Perovskite Nanocrystals

- Other Luminescent Nanoparticles

By Application

- Biomedical Imaging and Diagnostics

- Display and Lighting

- Solar Energy (LSC, Photovoltaics)

- Security and Anti-Counterfeiting

- Drug Delivery and Theranostics

- Environmental Monitoring

By End-Use Industry

- Healthcare and Life Sciences

- Consumer Electronics

- Energy

- Defense and Security

- Agriculture and Environmental Services

By Form

- Colloidal Dispersion

- Powder

- Thin Film / Coating

- Embedded in Matrix (Polymer, Glass)

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 8.42 B |

| Forecast Revenue (2034) | USD 23.15 B |

| CAGR (2025-2034) | 11.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type, (Quantum Dots (Cadmium-Based), Quantum Dots (Cadmium-Free / InP / Silicon), Upconversion Nanoparticles (UCNPs), Fluorescent Silica Nanoparticles, Carbon Quantum Dots, Perovskite Nanocrystals, Other Luminescent Nanoparticles), By Application, (Biomedical Imaging and Diagnostics, Display and Lighting, Solar Energy (LSC, Photovoltaics), Security and Anti-Counterfeiting, Drug Delivery and Theranostics, Environmental Monitoring), By End-Use Industry, (Healthcare and Life Sciences, Consumer Electronics, Energy, Defense and Security, Agriculture and Environmental Services), By Form, (Colloidal Dispersion, Powder, Thin Film / Coating, Embedded in Matrix (Polymer, Glass)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | THERMO FISHER SCIENTIFIC, LONZA GROUP, MILTENYI BIOTEC, SARTORIUS AG, CYTIVA (DANAHER CORPORATION), BECTON DICKINSON AND COMPANY (BD), CATALENT CELL & GENE, WAISMAN BIOMANUFACTURING, NIKON CELL INNOVATION CO., LTD., OXFORD BIOMEDICA (OXGENE), PLURILOCK SECURITY / PLURI INC., CELLULAR DYNAMICS INTERNATIONAL (CDI), FUJIFILM CELLULAR DYNAMICS, BIO-TECHNE CORPORATION, NCARDIA, HITACHI SOLUTIONS, CORNING INCORPORATED, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Biomedical Imaging, Diagnostics, Display & Lighting, Solar Energy, Security & Anti-Counterfeiting, Drug Delivery, Environmental Monitoring), By End-Use Industry, Competitive Landscape, Technology Trends, Regional Outlook & Forecast 2026-2034")

, By Application (Biomedical Imaging, Diagnostics, Display & Lighting, Solar Energy, Security & Anti-Counterfeiting, Drug Delivery, Environmental Monitoring), By End-Use Industry, Competitive Landscape, Technology Trends, Regional Outlook & Forecast 2026-2034")

, By Application (Biomedical Imaging, Diagnostics, Display & Lighting, Solar Energy, Security & Anti-Counterfeiting, Drug Delivery, Environmental Monitoring), By End-Use Industry, Competitive Landscape, Technology Trends, Regional Outlook & Forecast 2026-2034")

Frequently Asked Questions

How big is the Luminescent Nanoparticle Market?

The Global Luminescent Nanoparticle Market was valued at USD 7.52 Billion in 2024 and is projected to reach USD 23.15 Billion by 2034, growing at a CAGR of 11.9% from 2026 to 2034, driven by rising demand in bioimaging, diagnostics, optoelectronics, and advanced nanotechnology applications.

Who are the major players in the Luminescent Nanoparticle Market?

THERMO FISHER SCIENTIFIC, LONZA GROUP, MILTENYI BIOTEC, SARTORIUS AG, CYTIVA (DANAHER CORPORATION), BECTON DICKINSON AND COMPANY (BD), CATALENT CELL & GENE, WAISMAN BIOMANUFACTURING, NIKON CELL INNOVATION CO., LTD., OXFORD BIOMEDICA (OXGENE), PLURILOCK SECURITY / PLURI INC., CELLULAR DYNAMICS INTERNATIONAL (CDI), FUJIFILM CELLULAR DYNAMICS, BIO-TECHNE CORPORATION, NCARDIA, HITACHI SOLUTIONS, CORNING INCORPORATED, Others

Which segments covered the Luminescent Nanoparticle Market?

By Product Type, (Quantum Dots (Cadmium-Based), Quantum Dots (Cadmium-Free / InP / Silicon), Upconversion Nanoparticles (UCNPs), Fluorescent Silica Nanoparticles, Carbon Quantum Dots, Perovskite Nanocrystals, Other Luminescent Nanoparticles), By Application, (Biomedical Imaging and Diagnostics, Display and Lighting, Solar Energy (LSC, Photovoltaics), Security and Anti-Counterfeiting, Drug Delivery and Theranostics, Environmental Monitoring), By End-Use Industry, (Healthcare and Life Sciences, Consumer Electronics, Energy, Defense and Security, Agriculture and Environmental Services), By Form, (Colloidal Dispersion, Powder, Thin Film / Coating, Embedded in Matrix (Polymer, Glass))

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Luminescent Nanoparticle Market

Published Date : 07 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date