- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Luxury E-commerce Market Growth & Trends 2034 | 10.9% CAGR

Global Luxury E-commerce Market Size, Share, Analysis Report By Platform (Mobile Apps, Websites - leads); Payment Mode (Cash on Delivery, Credit/Debit Cards - leads, Bank Transfers, Digital Wallets, Others); Product Type( Beauty Products, Apparel - leads, Footwear, Jewellery, Accessories, Others); End-User: (Women - leads, Men, Unise) Industry Region and Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034

Report Overview:

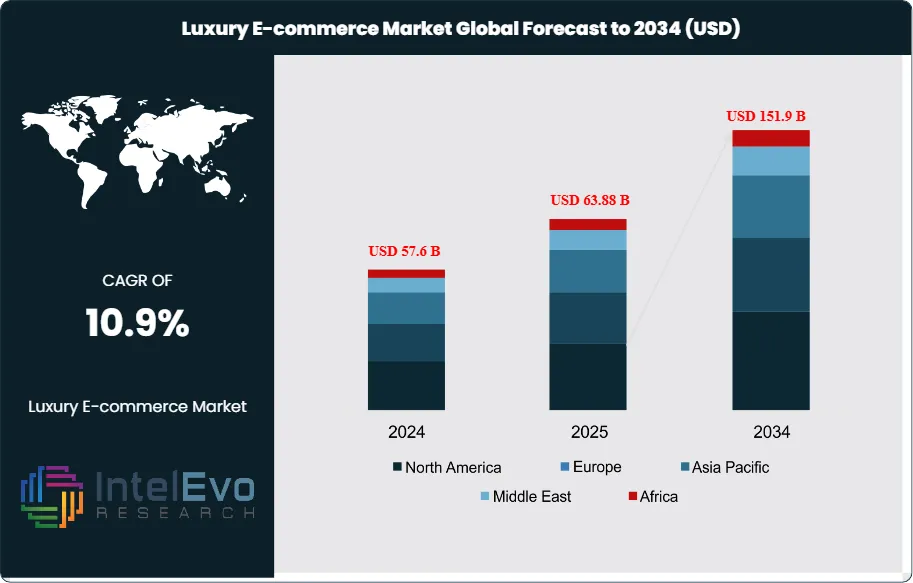

The Luxury E-commerce Market size is projected to reach approximately USD 151.9 Billion by 2034, up from USD 57.6 Billion in 2024, growing at a CAGR of 10.9% during the forecast period from 2025 to 2034. This growth is being driven by the rising digital transformation of luxury brands, the surge in online luxury fashion and accessories, and the expanding high-net-worth customer base in emerging economies. The integration of AR-based virtual try-ons, AI-powered personalization, and exclusive online luxury experiences is redefining premium shopping journeys. As luxury consumption becomes more digital and experiential, brands that combine heritage with high-tech innovation are leading the e-commerce revolution — transforming how affluent consumers engage with prestige products online.

Get More Information about this report -

Request Free Sample ReportThe luxury e-commerce market represents a sophisticated segment of digital commerce characterized by premium brands, high-end products, and affluent consumers seeking exclusive shopping experiences through online platforms. This market encompasses luxury apparel, accessories, jewelry, beauty products, and footwear, distributed through dedicated luxury websites and mobile applications that emphasize personalized service, authenticity, and premium user experiences.

The market's growth trajectory is driven by increasing digital adoption among luxury consumers, rising disposable income in emerging markets, and the growing acceptance of online luxury shopping among millennials and Gen Z consumers. Additionally, the integration of advanced technologies such as virtual reality, artificial intelligence, and augmented reality has enhanced the online luxury shopping experience, while social media influence and celebrity endorsements continue to drive brand awareness and consumer engagement in the digital luxury space.

Several critical factors are shaping the luxury e-commerce landscape, including the increasing importance of brand storytelling and heritage communication through digital channels, the rise of sustainable luxury consumption, and the growing demand for personalized shopping experiences that mirror the exclusivity of traditional luxury retail. The market is also influenced by changing consumer preferences toward experiential luxury, the emergence of luxury rental and resale platforms, and the integration of omnichannel strategies that seamlessly blend online and offline luxury experiences. Furthermore, the expansion of luxury brands into new geographic markets through e-commerce platforms, the adoption of innovative payment solutions, and the increasing focus on cybersecurity and data protection measures are crucial factors driving market evolution and consumer trust in luxury online transactions.

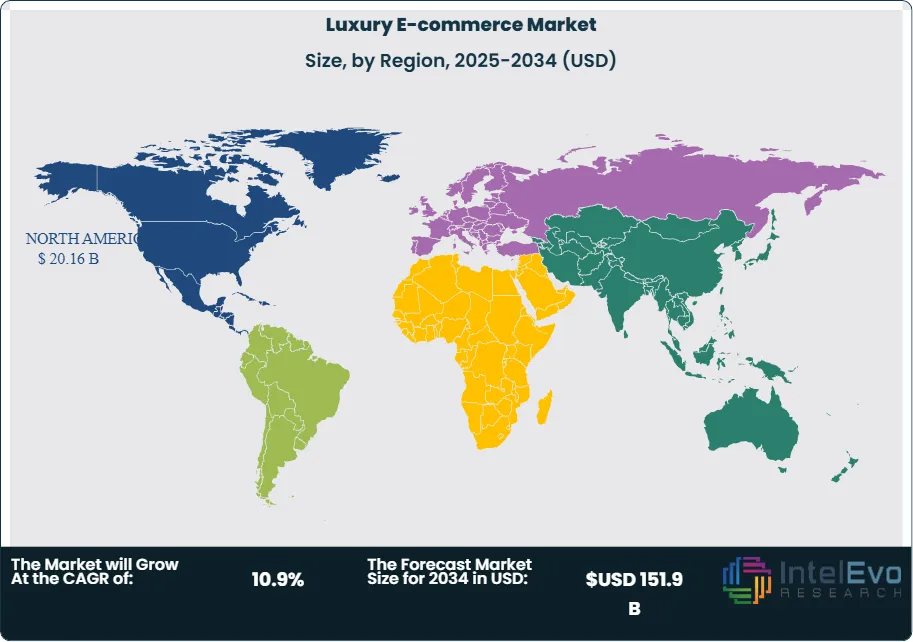

Regional Analysis: North America leads the global luxury e-commerce market, driven by high consumer spending power, widespread digital adoption, and the presence of major luxury retailers and technology companies. The region benefits from sophisticated logistics infrastructure, advanced payment systems, and a culture of online shopping that extends to luxury purchases, supported by strong consumer confidence in digital transactions and brand authenticity.

COVID-19 Impact: The COVID-19 pandemic significantly accelerated luxury e-commerce adoption as store closures and travel restrictions forced luxury consumers to embrace online shopping. This shift resulted in unprecedented growth rates for luxury e-commerce platforms, with many luxury brands rapidly expanding their digital presence and investing heavily in online capabilities to maintain customer relationships and sales during lockdowns. The pandemic also highlighted the importance of digital customer engagement strategies and led to lasting changes in luxury consumer behavior toward online shopping.

; Payment Mode (Cash on Delivery, Credit/Debit Cards - leads, Bank Transfers, Digital Wallets, Others); Product Type( Beauty Products, Apparel - leads, Footwear, Jewellery, Accessories, Others); End-User: (Women - leads, Men, Unise) Industry Region and Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Key Takeaways:

- Market Growth: The Luxury E-commerce Market is expected to reach USD 151.9 Billion by 2034, as consumers increasingly embrace online channels to access high-end products with convenience and personalized experiences.

- Platform Dominance: Websites remain the primary platform for luxury purchases due to superior visual merchandising, intuitive navigation, and integrated brand storytelling that elevate customer engagement.

- Payment Mode Dominance: Credit and debit cards dominate payment modes because they offer security, reward programs, and widespread acceptance across luxury e-retailers.

- Product Type Dominance: Among product types, apparel commands the largest share, driven by seasonal designer collections and consumer enthusiasm for exclusive online fashion drops.

- End-User Dominance: Women are the largest end-user segment, reflecting their higher propensity for purchasing luxury apparel, accessories, and beauty products online.

- Driver: The demand for seamless omnichannel experiences and personalized recommendations is driving investments in AI-powered platforms and virtual shopping assistants.

- Restraint: Counterfeit risks and concerns over product authenticity deter some consumers from embracing luxury e-commerce fully.

- Opportunity: Expanding in emerging markets like China and India offers lucrative growth avenues, supported by increasing digital literacy and aspirational consumption.

- Trend: Integration of augmented reality (AR) and virtual fitting rooms is enhancing customer confidence and reducing return rates.

- Regional Analysis: North America leads due to mature e-commerce ecosystems, strong luxury spending, and early digital adoption, with Europe and Asia-Pacific poised for significant future growth.

Platform Analysis:

The dominance of luxury e-commerce websites stems from their ability to provide comprehensive, immersive brand experiences that mobile applications cannot fully replicate. Luxury websites offer extensive product catalogs with detailed descriptions, high-resolution imagery, and interactive features that allow consumers to explore products thoroughly before making high-value purchases. These platforms serve as digital flagships for luxury brands, incorporating sophisticated design elements, brand storytelling, and exclusive content that reinforce brand heritage and prestige. The desktop experience remains crucial for luxury shopping, as consumers often spend considerable time researching and comparing products before making purchase decisions. Additionally, luxury websites can accommodate complex product configurations, customization options, and personalized services that require more screen space and functionality than mobile apps can provide. The integration of advanced technologies such as virtual reality, 3D product visualization, and live chat with personal stylists further enhances the website experience, making it the preferred platform for luxury e-commerce transactions.

Payment Mode Analysis:

Credit/Debit Cards Leads With over 55% Market Share In Luxury E-commerce Market. Credit and debit cards maintain their dominance in luxury e-commerce payments due to their universal acceptance, robust security features, and alignment with luxury consumers' expectations for premium service and protection. Luxury shoppers typically prefer established, trusted payment methods that offer comprehensive fraud protection, dispute resolution, and purchase insurance, all of which are standard features of major credit card networks. Premium credit cards often provide additional benefits that appeal to luxury consumers, including exclusive rewards programs, concierge services, and access to special events or products. The integration of advanced security technologies such as tokenization, biometric authentication, and real-time fraud monitoring has further enhanced consumer confidence in card-based payments for high-value transactions. Additionally, the ability to finance large purchases through credit facilities and the seamless integration of card payments with luxury retailers' existing systems make credit and debit cards the most practical choice for luxury e-commerce transactions.

Product Type Analysis:

The luxury apparel segment's dominance in luxury e-commerce is driven by the fashion industry's natural alignment with digital marketing and social media engagement. Luxury fashion brands have successfully leveraged online platforms to showcase their collections through high-quality imagery, runway videos, and behind-the-scenes content that builds brand desirability and consumer engagement. The frequent release of seasonal collections, limited editions, and exclusive collaborations creates ongoing demand and urgency that drives online sales. Additionally, the aspirational nature of luxury fashion makes it particularly suitable for digital marketing campaigns, influencer partnerships, and social media promotion. The segment benefits from strong brand loyalty and the ability to command premium prices for unique designs and craftsmanship. The rise of sustainable luxury fashion and the increasing importance of brand values have further enhanced the segment's appeal, particularly among younger consumers who prioritize environmental and social responsibility in their purchasing decisions.

End-User Analysis:

Women's dominance in luxury e-commerce reflects their higher engagement with luxury brands, greater influence over household purchasing decisions, and stronger presence on social media platforms where luxury brands actively market their products. Female consumers demonstrate higher brand loyalty and are more likely to engage with luxury brands through digital channels, including social media, email marketing, and influencer content. The luxury beauty and fashion categories, which are traditionally female-focused, represent significant portions of luxury e-commerce sales, contributing to women's dominance in this market. Additionally, women are more likely to share their luxury purchases on social media, creating valuable word-of-mouth marketing for luxury brands. The segment's purchasing behavior is characterized by extensive research, comparison shopping, and engagement with brand content, making them valuable customers for luxury e-commerce platforms. The increasing economic empowerment of women globally, combined with their growing influence in luxury purchasing decisions, continues to drive their dominance in the luxury e-commerce market.

Region Analysis:

North America Leads With more than 35% Market Share In Luxury E-commerce Market. North America leads the global luxury e-commerce market, driven by several key factors including high consumer spending power, widespread digital adoption, and the presence of major luxury retailers and technology companies. The region's sophisticated logistics infrastructure enables efficient delivery of luxury products, while advanced payment systems and strong consumer protection laws build confidence in high-value online transactions. American consumers have embraced online luxury shopping more readily than consumers in other regions, supported by a culture of convenience and digital innovation. The presence of major luxury e-commerce platforms such as Net-A-Porter, Bergdorf Goodman, and Neiman Marcus has created a competitive environment that drives innovation and service excellence.

Europe represents the second-largest market, benefiting from its rich luxury heritage and the presence of numerous established luxury brands that have successfully transitioned to digital platforms. The region's strong fashion industry and sophisticated consumer base create favorable conditions for luxury e-commerce growth. Asia Pacific shows the fastest growth potential, driven by emerging affluent populations in countries like China, India, and Southeast Asia, where luxury brand awareness is rapidly increasing. The region's high smartphone adoption rates and mobile-first commerce strategies are particularly conducive to luxury e-commerce expansion. Latin America and the Middle East present emerging opportunities, with growing wealthy populations and increasing internet penetration driving luxury e-commerce adoption. The apparel segment is expected to maintain its growth trajectory across all regions, while the beauty and accessories segments show promising potential in emerging markets as luxury brand awareness expands and consumer preferences evolve.

Get More Information about this report -

Request Free Sample ReportKey Market Segment:

By Product Type

- Apparel and Footwear

- Accessories (Watches, Jewelry, Handbags)

- Beauty and Personal Care

- Home Décor and Furnishings

- Luxury Electronics

- Others (Automobiles, Art, Wines & Spirits)

By Platform Type

- Company-Owned Platforms

- Third-Party Marketplaces

- Mobile Apps

- Social Media Commerce

By End User

- Men

- Women

- Unisex

By Payment Mode

- Credit/Debit Card

- Digital Wallets

- Bank Transfers

- Others

By Price Range

- Premium (USD 500–1,000)

- Ultra-Luxury (Above USD 1,000)

By Business Model

- Business-to-Consumer (B2C)

- Business-to-Business (B2B)

- Consumer-to-Consumer (C2C)

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 63.88 B |

| Forecast Revenue (2034) | USD 151.9 B |

| CAGR (2025-2034) | 10.9% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Apparel and Footwear, Accessories (Watches, Jewelry, Handbags), Beauty and Personal Care, Home Décor and Furnishings, Luxury Electronics, Others (Automobiles, Art, Wines & Spirits)), By Platform Type (Company-Owned Platforms, Third-Party Marketplaces, Mobile Apps, Social Media Commerce), By End User (Men, Women, Unisex), By Payment Mode (Credit/Debit Card, Digital Wallets, Bank Transfers, Others), By Price Range (Premium (USD 500–1,000), Ultra-Luxury (Above USD 1,000)), By Business Model(Business-to-Consumer (B2C), Business-to-Business (B2B), Consumer-to-Consumer (C2C)) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Farfetch, Hudson's Bay Company, Net-A-Porter, MatchesFashion, Mytheresa, SSENSE, Amazon, Moda Operandi, 24S, Luxury Garage Sale, LuisaViaRoma, Gilt Groupe, Tessabit, Browns Fashion, Lane Crawford, Barneys New York, Harrods, Neiman Marcus, Bergdorf Goodman, Nordstrom |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

; Payment Mode (Cash on Delivery, Credit/Debit Cards - leads, Bank Transfers, Digital Wallets, Others); Product Type( Beauty Products, Apparel - leads, Footwear, Jewellery, Accessories, Others); End-User: (Women - leads, Men, Unise) Industry Region and Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

; Payment Mode (Cash on Delivery, Credit/Debit Cards - leads, Bank Transfers, Digital Wallets, Others); Product Type( Beauty Products, Apparel - leads, Footwear, Jewellery, Accessories, Others); End-User: (Women - leads, Men, Unise) Industry Region and Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

; Payment Mode (Cash on Delivery, Credit/Debit Cards - leads, Bank Transfers, Digital Wallets, Others); Product Type( Beauty Products, Apparel - leads, Footwear, Jewellery, Accessories, Others); End-User: (Women - leads, Men, Unise) Industry Region and Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends and Forecast 2025-2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date