- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Managed Pressure Drilling Market Size, Share & Growth Analysis | CAGR 11.2%

Global Managed Pressure Drilling Market Size, Share, Analysis By Equipment Type (Rotating Control Devices, Automated Choke Manifolds, Continuous Circulation Systems, Downhole Monitoring & Control Systems, Pressure Control Pumps & Ancillary Equipment), By Service Type (Managed Pressure Drilling Services, Equipment Rental Services, Training & Consulting Services), By Application (Offshore Deepwater & Ultra-Deepwater, Onshore HPHT & Tight Reservoirs), By End-User (Oilfield Services Companies, International Oil Companies, National Oil Companies, Independent Operators) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

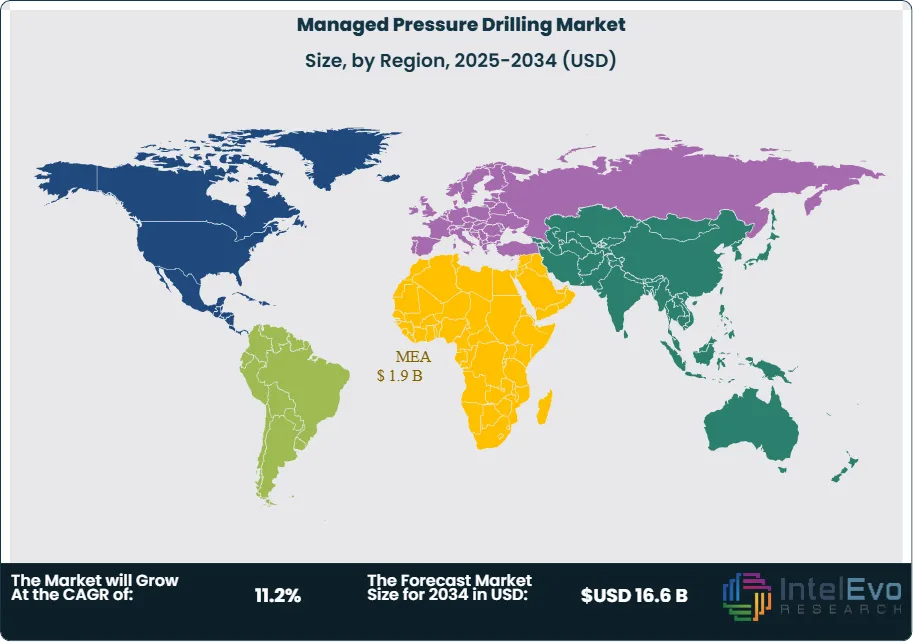

| USD 6.4 Billion, 2025 | USD 16.6 Billion, 2034 | 11.2%, 2026–2034 | MEA, 30.40%, 2025 |

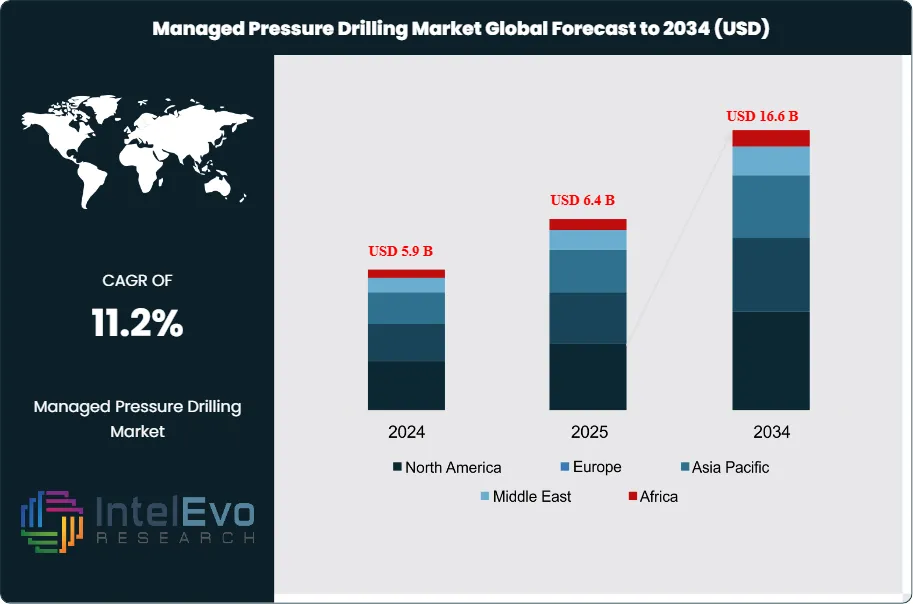

The Managed Pressure Drilling Market was valued at approximately USD 5.9 Billion in 2024 and increased to USD 6.4 Billion in 2025. The market is projected to reach nearly USD 16.6 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 11.2% during the forecast period from 2026 to 2034. The managed pressure drilling market is experiencing broad-based adoption across deepwater, ultra-deepwater, and high-pressure high-temperature well environments as operators seek to drill through narrow drilling windows, reduce nonproductive time, and mitigate wellbore stability risks that conventional overbalanced and underbalanced drilling methods cannot adequately address. Managed pressure drilling technologies, encompassing continuous circulation systems, rotating control devices, automated choke manifolds, and real-time downhole pressure monitoring platforms, enable precise wellbore pressure management that expands the range of technically drillable reservoir targets and significantly reduces drilling cost per well in challenging formations.

Get More Information about this report -

Request Free Sample ReportDemand forces driving the managed pressure drilling market include the global shift toward increasingly complex well architectures in narrow pressure window reservoirs, the rising proportion of deepwater and ultra-deepwater drilling programs where wellbore pressure management is critical to safe and efficient well delivery, and the demonstrated economic benefit of managed pressure drilling in reducing kick and loss circulation events that generate the majority of nonproductive drilling time. Industry data indicates that kick and loss circulation events account for approximately 35–40% of total nonproductive drilling time globally, making managed pressure drilling one of the highest-return-on-investment drilling technology investments available to upstream operators. Supply-side dynamics reflect competitive development among specialized service providers including Halliburton, Weatherford, Baker Hughes, and Schlumberger, alongside specialist MPD technology companies that have built differentiated equipment and service capabilities.

Regulatory frameworks are increasingly incorporating managed pressure drilling requirements into deepwater well control standards. The Bureau of Safety and Environmental Enforcement in the United States updated its deepwater well control regulations following the 2010 Deepwater Horizon incident, with provisions that effectively mandate managed pressure drilling or equivalent pressure management capability for ultra-deepwater wells with narrow drilling windows. Norway's Petroleum Safety Authority has established technical requirements for pressure management systems in high-pressure high-temperature wells on the Norwegian Continental Shelf. Brazil's National Agency of Petroleum has incorporated managed pressure drilling technical standards into its pre-salt deepwater licensing requirements, reflecting the extreme pressure and temperature conditions of Santos Basin reservoirs.

Risk factors in the managed pressure drilling market include the high capital cost of managed pressure drilling equipment packages, the specialized crew training requirements that limit rapid deployment to new operating environments, and the technical complexity of integrating managed pressure drilling systems with existing rig infrastructure. The market is also shaped by oil price sensitivity, as managed pressure drilling adoption rates among independent operators are correlated with capital expenditure cycles. The Middle East and Africa region leads global managed pressure drilling market revenue at 30.4% in 2025 at USD 1.9 Billion, driven by complex carbonate reservoir drilling programs. North America follows at 28.6% at USD 1.8 Billion, anchored by deepwater Gulf of Mexico and high-pressure tight reservoir activity. By 2034, autonomous closed-loop pressure management systems are projected to redefine operational standards across the managed pressure drilling market, fundamentally changing how operators manage wellbore pressure in the most challenging drilling environments globally.

, By Service Type (Managed Pressure Drilling Services, Equipment Rental Services, Training & Consulting Services), By Application (Offshore Deepwater & Ultra-Deepwater, Onshore HPHT & Tight Reservoirs), By End-User (Oilfield Services Companies, International Oil Companies, National Oil Companies, Independent Operators) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global managed pressure drilling market was valued at USD 6.4 Billion in 2025 and is projected to reach USD 16.6 Billion by 2034, registering a CAGR of 11.2% during the forecast period 2026–2034, driven by rising deepwater drilling complexity and expanding high-pressure high-temperature well programs globally.

- Segment Dominance (By Equipment): Rotating control devices are the dominant equipment segment in the managed pressure drilling market with a 34.2% share in 2025 at USD 2.2 Billion, as the fundamental wellbore pressure containment component required for all managed pressure drilling operations across surface and subsea well environments.

- Segment Dominance (By Application): Offshore applications lead the managed pressure drilling market with a 61.4% share in 2025 at USD 3.9 Billion, driven by deepwater and ultra-deepwater drilling programs in the Gulf of Mexico, Brazilian pre-salt basins, and West African deepwater blocks where narrow drilling windows make conventional drilling methods technically inadequate.

- Driver: The accelerating global deepwater and ultra-deepwater drilling program backlog, with active deepwater rig utilization exceeding 86% in 2025 and deepwater well count growing at 12.4% annually, is compelling operators to adopt managed pressure drilling to drill through narrow pressure windows that would otherwise require costly remedial operations or well abandonment.

- Restraint: High equipment mobilization and integration costs, averaging USD 4–8 Million per well for full managed pressure drilling system deployment on deepwater semi-submersibles and drillships, limit adoption among cost-sensitive independent operators and create a barrier to managed pressure drilling market penetration in price-sensitive emerging market drilling programs.

- Opportunity: Onshore high-pressure high-temperature managed pressure drilling in unconventional tight reservoirs represents a USD 3.8 Billion addressable opportunity within the managed pressure drilling market by 2034. Current managed pressure drilling penetration in onshore tight gas and geothermal drilling programs covers less than 14% of technically viable well candidates globally as of 2025.

- Trend: Autonomous closed-loop managed pressure drilling systems, which integrate real-time downhole pressure data with automated surface choke and pump control to maintain continuous wellbore pressure management without human intervention, are growing at 34.2% annually in 2025 and are redefining operational efficiency benchmarks across deepwater and high-pressure high-temperature drilling programs.

- Regional Analysis: The Middle East and Africa region leads the global managed pressure drilling market with a 30.4% share in 2025, equivalent to USD 1.9 Billion, anchored by complex carbonate reservoir drilling programs in Saudi Arabia, Iraq, and Oman where narrow pressure windows and high-pressure high-temperature conditions mandate advanced wellbore pressure management systems.

Competitive Landscape

The Global Managed Pressure Drilling (MPD) Market is moderately consolidated, with the top four companies accounting for an estimated 42.0% of total market revenue in 2025. Competition is highly technology-driven, centered on closed-loop pressure control systems, automated choke systems, real-time downhole pressure monitoring, and integrated drilling optimization platforms rather than commoditized service pricing. Leading oilfield service providers are strengthening integrated drilling service portfolios, combining MPD with digital drilling, well control, and reservoir navigation capabilities. Competitive intensity increased in 2025–2026 as operators prioritized reducing non-productive time (NPT) and improving well safety in deepwater, HPHT, and complex geology environments.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| SLB | US | Leader | Automated MPD systems and integrated digital drilling platforms | North America, Middle East, global offshore | Expanded automated MPD solutions integrated with digital drilling platforms for deepwater operations in 2025. |

| HALLIBURTON | US | Leader | Managed Pressure Drilling services and real-time well control systems | North America, Latin America, Middle East | Expanded MPD service contracts for offshore and HPHT wells with major operators in 2025. |

| WEATHERFORD | US | Leader | Victus intelligent MPD system and closed-loop pressure control solutions | Middle East, North America, Asia-Pacific | Expanded deployment of Victus MPD systems across Middle East drilling campaigns in 2025. |

| BAKER HUGHES | US | Leader | Automated drilling and MPD-integrated well construction services | North America, Europe, Middle East | Strengthened integrated drilling services with MPD-enabled well control solutions in 2025. |

| NOV | US | Challenger | MPD equipment including rotating control devices and choke systems | North America, global offshore | Expanded MPD equipment portfolio with advanced pressure control technologies in 2025. |

| EXPRO | UK | Challenger | Surface and subsea MPD solutions and well control services | North Sea, Middle East, Asia-Pacific | Expanded MPD service offerings for offshore well construction projects in 2025. |

| NATIONAL OILWELL VARCO | US | Challenger | MPD hardware systems and drilling automation technologies | North America, global drilling markets | Enhanced automation-driven MPD solutions integrated with drilling rigs in 2025. |

| ENERMECH | UK | Niche Player | MPD support services and pressure control solutions | Europe, Middle East, Asia-Pacific | Expanded well control and pressure management services for offshore clients in 2025. |

| DRILLING SYSTEMS | UK | Niche Player | Simulation-based MPD training and well control solutions | Europe, Middle East | Expanded digital training platforms for MPD and well control operations in 2025. |

| PELAGIC PRESSURE CONTROL | US | Niche Player | Offshore MPD and subsea pressure control systems | U.S. Gulf, West Africa | Expanded offshore MPD deployment capabilities for deepwater drilling operations in 2025. |

Segmentation Analysis

The managed pressure drilling market segmentation analysis covers four key dimensions: By Equipment Type, By Service Type, By Application, and By End-User. Each dimension reveals distinct technology requirements, adoption patterns, and competitive dynamics that define the global managed pressure drilling market through 2034.

By Equipment Type

Rotating control devices are the dominant equipment type in the managed pressure drilling market, accounting for 34.2% of equipment segment revenue in 2025 at USD 2.2 Billion. Rotating control devices, also known as rotating blowout preventers or rotating control heads, provide the primary pressure containment seal at the wellbore annulus while allowing drill string rotation and axial movement, forming the essential mechanical foundation for all managed pressure drilling operations. Surface rotating control devices are deployed on land rigs and jackup platforms, while subsea rotating control devices are engineered for semi-submersible and drillship applications where pressure management must function within the subsea blowout preventer stack configuration. Major RCD manufacturers including Weatherford, NOV, and Schlumberger have invested in higher-pressure rated models capable of continuous operation at wellbore pressures exceeding 3,000 pounds per square inch, expanding the addressable well population for managed pressure drilling technology.

Automated choke manifolds represent 24.6% of equipment revenue in the managed pressure drilling market at USD 1.6 Billion in 2025. Automated chokes control annular back pressure with millisecond response times, enabling continuous wellbore pressure management during connections, trips, and circulation events. The integration of automated chokes with real-time downhole pressure sensors and surface control software creates closed-loop pressure management systems that maintain target bottomhole pressure within tight tolerances regardless of drilling operation phase. Continuous circulation systems hold 18.4% of equipment revenue at USD 1.2 Billion in 2025, providing uninterrupted mud circulation during drill pipe connections that prevents wellbore pressure fluctuations associated with conventional pump-off and pump-on events. Downhole monitoring and control systems account for 14.8% at USD 948 Million in 2025, while pressure control pumps and related ancillary equipment represent the remaining 8.0% at USD 512 Million.

By Service Type

Managed pressure drilling services constitute the largest revenue category in the managed pressure drilling market by service type, accounting for 58.4% of service segment revenue in 2025 at USD 3.7 Billion. Services encompass the full operational delivery of managed pressure drilling programs, including well-specific system design, equipment mobilization and rig-up, crew provision, real-time pressure management during drilling operations, and post-well reporting and performance analysis. The service delivery model is predominant in the managed pressure drilling market because the technical complexity of wellbore pressure management requires specialized expertise that most operators do not maintain in-house. Halliburton's MPD services division, Weatherford's MPD services business, and Schlumberger's MPD service line compete intensively for offshore deepwater managed pressure drilling service contracts through competitive bidding processes that often include performance guarantee provisions.

Equipment rental services hold 28.2% of the service type segment in 2025 at USD 1.8 Billion, covering the provision of rotating control devices, automated choke manifolds, and continuous circulation systems on a day-rate rental basis without operational crew services. Equipment rental is particularly common among operators and drilling contractors who maintain in-house managed pressure drilling operational capability and require only equipment supply. Training and consulting services represent 13.4% of managed pressure drilling service revenue at USD 858 Million in 2025, encompassing managed pressure drilling crew certification programs, well planning consultation, and post-well analysis services. Demand for managed pressure drilling training services is growing at above-market rates as operators seek to build internal capability rather than relying entirely on third-party service provision for routine managed pressure drilling applications.

By Application

Offshore applications dominate the managed pressure drilling market, representing 61.4% of application segment revenue in 2025 at USD 3.9 Billion. Offshore managed pressure drilling encompasses deepwater and ultra-deepwater well programs where narrow drilling windows, high formation pressures, and significant nonproductive time risk create compelling economic justification for managed pressure drilling system deployment. The Gulf of Mexico deepwater, Brazilian pre-salt Santos Basin, Norwegian Continental Shelf high-pressure high-temperature wells, and West African deepwater blocks collectively represent the primary demand centers for offshore managed pressure drilling services and equipment. Offshore managed pressure drilling programs typically command premium day-rate service charges due to the specialized nature of subsea-rated equipment, the technical difficulty of operating managed pressure drilling systems in deepwater environments, and the high value of nonproductive time reduction that managed pressure drilling delivers in costly deepwater operations.

Onshore applications account for 38.6% of managed pressure drilling market revenue in 2025 at USD 2.5 Billion. Onshore managed pressure drilling is concentrated in high-pressure tight gas formations in the Middle East, high-pressure high-temperature geothermal wells in North America and Asia Pacific, and complex carbonate reservoir drilling programs in the Arabian Peninsula and North Africa. The onshore segment is growing at above-average rates within the managed pressure drilling market as the high-pressure gas reservoirs of Saudi Arabia, Iraq, and Oman increasingly require wellbore pressure management to drill safely through formation pressure regimes that exceed conventional overbalanced drilling capabilities. Unconventional tight reservoir drilling in North America and China is creating additional onshore managed pressure drilling demand as operators encounter abnormal pressure zones and wellbore instability in horizontal well sections that benefit from continuous annular pressure management.

By End-User

Oilfield services companies are the primary end-user category in the managed pressure drilling market by procurement, representing 42.8% of revenue in 2025 at USD 2.7 Billion, as integrated services firms incorporate managed pressure drilling capabilities into their well services portfolios to provide operators with turnkey drilling solutions. However, from a demand origination perspective, international oil companies are the primary procurement drivers, specifying managed pressure drilling requirements in drilling contracts and making the capital investment decisions that drive equipment and service demand. International oil companies represent 34.6% of direct end-user market revenue at USD 2.2 Billion in 2025, with Shell, BP, TotalEnergies, ExxonMobil, and Equinor operating managed pressure drilling programs across their deepwater and high-pressure high-temperature portfolios.

National oil companies account for 16.2% of managed pressure drilling market revenue in 2025 at USD 1.0 Billion, with Saudi Aramco, ADNOC, Petrobras, and Petronas deploying managed pressure drilling across their complex reservoir drilling programs. Saudi Aramco's extensive high-pressure high-temperature drilling programs in the Khuff and Pre-Khuff formations represent one of the largest individual managed pressure drilling demand concentrations globally. Independent oil companies represent the remaining 6.4% at USD 410 Million in 2025, with managed pressure drilling adoption among independents concentrated in technically complex deepwater and high-pressure onshore operations where the economics clearly justify the additional service cost.

Regional Analysis

Middle East & Africa Managed Pressure Drilling Market

The Middle East and Africa region leads the global managed pressure drilling market with a 30.4% share in 2025, equivalent to USD 1.9 Billion. Saudi Arabia is the dominant country market, with Saudi Aramco operating the world's most extensive onshore managed pressure drilling program across its Khuff and Pre-Khuff high-pressure high-temperature gas reservoir drilling campaigns. The Khuff formation, a prolific gas reservoir underlying Aramco's super-giant oil fields at depths of 4,000–6,000 meters, contains reservoir pressures exceeding 10,000 pounds per square inch and temperatures above 300 degrees Fahrenheit that require managed pressure drilling systems to drill safely and efficiently. Saudi Aramco's annual managed pressure drilling equipment and services expenditure is estimated at over USD 600 Million in 2025, making it the single largest individual operator consumer of managed pressure drilling services globally.

Iraq is the second-largest Middle East managed pressure drilling market, with international oil companies operating under technical service agreements including BP, ExxonMobil, Lukoil, and TotalEnergies deploying managed pressure drilling across challenging carbonate reservoir drilling programs in the Rumaila, West Qurna, and Majnoon fields. Oman contributes through Petroleum Development Oman's managed pressure drilling programs in the deep gas reservoirs of the Huqf Supergroup carbonate formations. The United Arab Emirates is a growing market, with ADNOC deploying managed pressure drilling in offshore Abu Dhabi carbonate reservoir wells and evaluating expanded managed pressure drilling application across its Khuff gas development program. The Middle East and Africa region is projected to grow at a CAGR of 12.2% through 2034 as national oil company drilling programs in deep high-pressure formations intensify.

North America Managed Pressure Drilling Market

North America holds a 28.6% share of the global managed pressure drilling market in 2025, equivalent to USD 1.8 Billion. The United States is the dominant country market, with managed pressure drilling demand concentrated in deepwater Gulf of Mexico operations and onshore high-pressure tight gas programs in the Gulf Coast and Midcontinent regions. Gulf of Mexico deepwater operators including Shell, BP, Chevron, and Murphy Oil routinely specify managed pressure drilling for wells penetrating narrow pressure window reservoir sections, with managed pressure drilling utilization rates on deepwater semi-submersibles and drillships in the Gulf of Mexico estimated at approximately 45% of active deepwater well programs in 2025. The BSEE's well control regulations that effectively mandate pressure management capability for certain deepwater well categories provide regulatory support for sustained managed pressure drilling adoption in U.S. waters.

Canada contributes approximately 12% of North American managed pressure drilling market revenue in 2025, with managed pressure drilling deployed in deep tight gas reservoir drilling programs in British Columbia's Montney and Deep Basin plays where abnormal pressure gradients and wellbore instability necessitate continuous annular pressure management. The United States geothermal energy sector is creating a new and growing managed pressure drilling demand segment, with high-pressure high-temperature geothermal wells requiring continuous bottomhole pressure management to prevent formation fluid influx during drilling. Mexico's managed pressure drilling market is growing as Pemex and private operators drill increasingly complex wells in deep gas-prone formations in the Burgos Basin and Gulf of Mexico shallow water. North America is projected to grow at a CAGR of 10.4% through 2034.

Asia Pacific Managed Pressure Drilling Market

Asia Pacific accounts for 20.8% of the global managed pressure drilling market in 2025, generating USD 1.3 Billion in revenue. China is the dominant country market, with PetroChina and SINOPEC deploying managed pressure drilling across deep tight gas reservoir drilling programs in the Sichuan Basin, Tarim Basin, and Ordos Basin where abnormally high formation pressures and narrow drilling windows create conditions requiring continuous wellbore pressure management. China's unconventional gas development strategy, which prioritizes deep Cambrian and Sinian tight gas formations at depths exceeding 7,000 meters, has created substantial managed pressure drilling demand at well pressure and temperature conditions approaching the technical limits of current equipment rated performance envelopes.

Australia is the second-largest Asia Pacific managed pressure drilling market, driven by geothermal energy development in South Australia and Queensland where high-temperature basement formations require managed pressure drilling capability, and by offshore deepwater managed pressure drilling applications in Woodside Energy's Carnarvon Basin operations. India's ONGC deploys managed pressure drilling in high-pressure high-temperature wells in the Krishna-Godavari deepwater Basin and in onshore tight gas formations in Rajasthan. Malaysia's Petronas is increasing managed pressure drilling utilization for complex deepwater well programs in the South China Sea. Indonesia represents a growing managed pressure drilling market as Pertamina and its production-sharing partners develop deep high-pressure gas reservoirs requiring sophisticated wellbore pressure management. Asia Pacific is projected to grow at a CAGR of 12.8% through 2034.

Europe Managed Pressure Drilling Market

Europe holds a 12.6% share of the global managed pressure drilling market in 2025, valued at USD 807 Million. Norway is the dominant European market, with managed pressure drilling widely deployed across high-pressure high-temperature wells on the Norwegian Continental Shelf where the Norwegian Petroleum Safety Authority's stringent well control requirements effectively mandate advanced pressure management capability for wells meeting specific high-pressure high-temperature criteria. Equinor, Aker BP, and Vår Energi are the primary Norwegian managed pressure drilling consumers, with Equinor's extensive exploration and production well programs involving managed pressure drilling for a significant proportion of technically complex wells drilled annually. Norway's position as one of the world's most technologically advanced deepwater drilling environments means that managed pressure drilling equipment qualification standards developed for Norwegian operations are often adopted globally as industry benchmarks.

The United Kingdom contributes through North Sea high-pressure high-temperature well programs operated by Harbour Energy, Repsol Sinopec, and independent operators in the Central North Sea where deep Triassic and Permian reservoirs contain high-pressure gas with narrow drilling windows. The Netherlands hosts Shell's European managed pressure drilling technology development activities, with Shell's research programs contributing to advances in automated pressure management control systems. Germany's geothermal energy sector is creating modest but growing managed pressure drilling demand for deep crystalline basement geothermal wells in Bavaria and Baden-Württemberg. Europe is projected to grow at a CAGR of 9.8% through 2034, with geothermal energy expansion providing incremental growth beyond conventional oil and gas applications.

Latin America Managed Pressure Drilling Market

Latin America accounts for 7.6% of the global managed pressure drilling market in 2025, totaling USD 487 Million. Brazil is the dominant country market, with Petrobras deploying managed pressure drilling across its pre-salt Santos Basin deepwater drilling program where reservoir pressures of 8,000–12,000 pounds per square inch at water depths of 2,000–3,000 meters create extreme well control challenges that require continuous managed pressure drilling capability. Petrobras has developed specialized managed pressure drilling procedures for its pre-salt well architecture, incorporating rotating control devices rated for subsea installation below the riser tensioner system to manage wellbore pressure at extraordinary combined depth and pressure conditions. The Santos Basin pre-salt represents one of the technically most demanding managed pressure drilling environments globally, with well total depths exceeding 7,000 meters below sea surface.

Colombia represents the second-largest Latin American managed pressure drilling market, with Ecopetrol and international operator partners deploying managed pressure drilling in deep tight gas and high-pressure oil reservoir drilling programs in the Llanos Basin and Pacific Coast offshore blocks. Argentina's Vaca Muerta unconventional play is creating managed pressure drilling demand for horizontal well programs encountering abnormal pressure zones in the deeper Vaca Muerta and underlying tight gas formations. Mexico's managed pressure drilling market is growing as Pemex and private operators push into deeper high-pressure gas formations in the Burgos Basin and offshore deepwater blocks. Latin America is projected to grow at a CAGR of 11.6% through 2034, anchored by Petrobras's sustained pre-salt deepwater managed pressure drilling program expansion.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Equipment Type

- Rotating Control Devices

- Automated Choke Manifolds

- Continuous Circulation Systems

- Downhole Monitoring and Control Systems

- Pressure Control Pumps and Ancillary Equipment

By Service Type

- Managed Pressure Drilling Services

- Equipment Rental Services

- Training and Consulting Services

By Application

- Offshore (Deepwater and Ultra-Deepwater)

- Onshore (High-Pressure High-Temperature and Tight Reservoirs)

By End-User

- Oilfield Services Companies

- International Oil Companies

- National Oil Companies

- Independent Oil Companies

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.4 B |

| Forecast Revenue (2034) | USD 16.6 B |

| CAGR (2025-2034) | 11.2% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Equipment Type (Rotating Control Devices, Automated Choke Manifolds, Continuous Circulation Systems, Downhole Monitoring and Control Systems, Pressure Control Pumps and Ancillary Equipment), By Service Type (Managed Pressure Drilling Services, Equipment Rental Services, Training and Consulting Services), By Application (Offshore (Deepwater and Ultra-Deepwater), Onshore (High-Pressure High-Temperature and Tight Reservoirs)), By End-User (Oilfield Services Companies, International Oil Companies, National Oil Companies, Independent Oil Companies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | HALLIBURTON COMPANY, WEATHERFORD INTERNATIONAL PLC, SLB (SCHLUMBERGER LIMITED), BAKER HUGHES COMPANY, NATIONAL OILWELL VARCO INC. (NOV), MANAGED PRESSURE OPERATIONS LTD. (MPO), ENHANCED DRILLING AS, BLADE ENERGY PARTNERS, DEEP CASING TOOLS, SECURE ENERGY SERVICES INC., DELTATEK OIL TOOLS AS, WELL CONTROL SCHOOL, RDT INC. (ROTATING DRILLING TECHNOLOGIES), STRATUM RESERVOIR, EXPRO GROUP HOLDINGS N.V., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Service Type (Managed Pressure Drilling Services, Equipment Rental Services, Training & Consulting Services), By Application (Offshore Deepwater & Ultra-Deepwater, Onshore HPHT & Tight Reservoirs), By End-User (Oilfield Services Companies, International Oil Companies, National Oil Companies, Independent Operators) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Service Type (Managed Pressure Drilling Services, Equipment Rental Services, Training & Consulting Services), By Application (Offshore Deepwater & Ultra-Deepwater, Onshore HPHT & Tight Reservoirs), By End-User (Oilfield Services Companies, International Oil Companies, National Oil Companies, Independent Operators) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Service Type (Managed Pressure Drilling Services, Equipment Rental Services, Training & Consulting Services), By Application (Offshore Deepwater & Ultra-Deepwater, Onshore HPHT & Tight Reservoirs), By End-User (Oilfield Services Companies, International Oil Companies, National Oil Companies, Independent Operators) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Managed Pressure Drilling Market?

The Global Managed Pressure Drilling Market was valued at USD 6.4 Billion in 2025, projected to reach USD 16.6 Billion by 2034 at a CAGR of 11.2% from 2026–2034. Growth is driven by increasing deepwater and HPHT drilling activities, demand for wellbore pressure control, reduced non-productive time, and adoption of real-time monitoring and automation technologies.

Who are the major players in the Managed Pressure Drilling Market?

HALLIBURTON COMPANY, WEATHERFORD INTERNATIONAL PLC, SLB (SCHLUMBERGER LIMITED), BAKER HUGHES COMPANY, NATIONAL OILWELL VARCO INC. (NOV), MANAGED PRESSURE OPERATIONS LTD. (MPO), ENHANCED DRILLING AS, BLADE ENERGY PARTNERS, DEEP CASING TOOLS, SECURE ENERGY SERVICES INC., DELTATEK OIL TOOLS AS, WELL CONTROL SCHOOL, RDT INC. (ROTATING DRILLING TECHNOLOGIES), STRATUM RESERVOIR, EXPRO GROUP HOLDINGS N.V., Others

Which segments covered the Managed Pressure Drilling Market?

By Equipment Type (Rotating Control Devices, Automated Choke Manifolds, Continuous Circulation Systems, Downhole Monitoring and Control Systems, Pressure Control Pumps and Ancillary Equipment), By Service Type (Managed Pressure Drilling Services, Equipment Rental Services, Training and Consulting Services), By Application (Offshore (Deepwater and Ultra-Deepwater), Onshore (High-Pressure High-Temperature and Tight Reservoirs)), By End-User (Oilfield Services Companies, International Oil Companies, National Oil Companies, Independent Oil Companies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Managed Pressure Drilling Market

Published Date : 17 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date