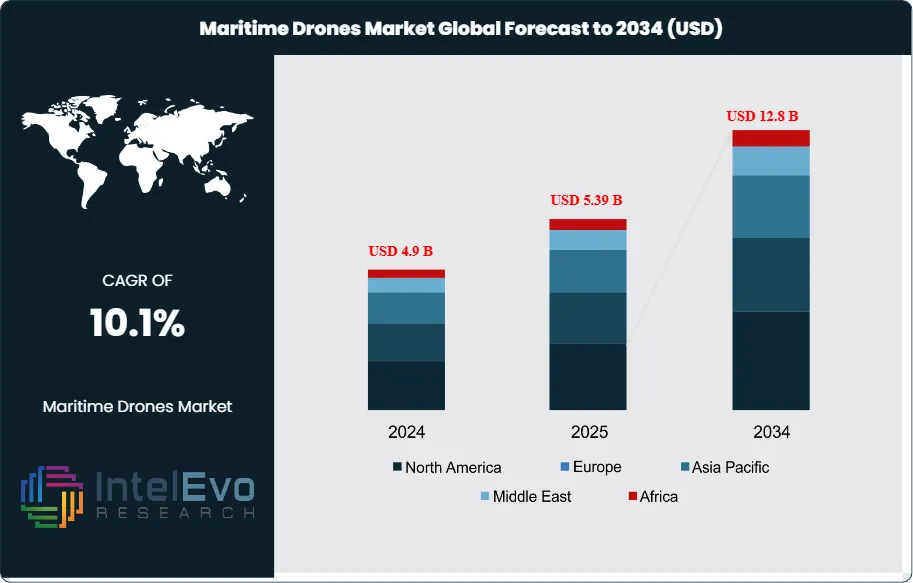

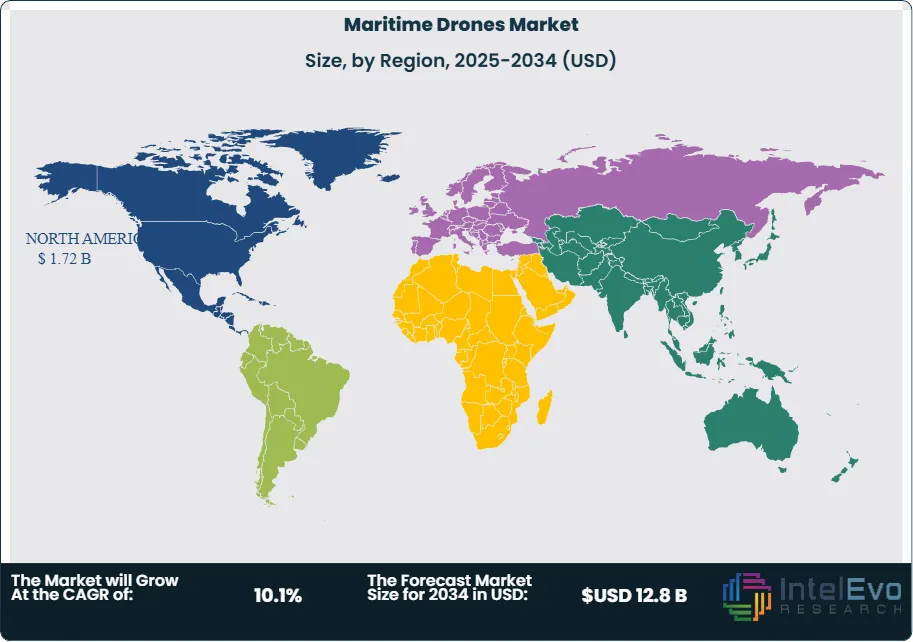

The Maritime Drones Market is projected to reach approximately USD 12.8 billion by 2034, rising from USD 4.9 billion in 2024, and expanding at a CAGR of 10.1% during the forecast period from 2024 to 2034. This growth is driven by increasing adoption of unmanned surface and underwater vehicles for maritime surveillance, offshore inspection, and environmental monitoring. Rising investments in naval modernization, offshore energy exploration, and port security—combined with advances in AI, autonomous navigation, and sensor technologies—are further accelerating the deployment of maritime drones across commercial and defense applications worldwide.

The maritime drones market encompasses a broad ecosystem of unmanned surface vehicles (USVs), unmanned underwater vehicles (UUVs), and associated systems and services supporting naval defense, commercial shipping, offshore energy, environmental monitoring, and search & rescue operations. This market includes drone platforms, payloads (sensors, cameras, sonar), communication systems, control software, and supporting infrastructure. Maritime drones serve a diverse set of end-users, including naval forces, coast guards, shipping companies, offshore oil & gas operators, marine researchers, and environmental agencies, each with unique operational requirements and performance standards.

Market growth is being driven by rising maritime security concerns, increased adoption of autonomous technologies, and the need for cost-effective, risk-reducing solutions for ocean monitoring and operations. Technological advancements in AI-driven navigation, real-time data analytics, and long-endurance battery systems are enhancing the capabilities and reliability of maritime drones. The market is also benefiting from regulatory support for unmanned systems integration, growing investments in smart port infrastructure, and the expansion of offshore renewable energy projects.

North America leads the global maritime drones market, underpinned by significant defense budgets, robust R&D activity, and early adoption of unmanned maritime systems by the U.S. Navy and Coast Guard. The Asia-Pacific region is the fastest-growing market, fueled by territorial disputes, increased naval modernization, and expanding commercial shipping activity. Europe maintains a strong presence due to established maritime industries, advanced technology providers, and collaborative defense initiatives.

The COVID-19 pandemic initially disrupted supply chains and delayed project deployments, but ultimately accelerated digital transformation and remote monitoring trends, increasing demand for unmanned maritime solutions. The crisis highlighted the value of autonomous systems for maintaining operations and surveillance with minimal human intervention. Rising geopolitical tensions, piracy, and illegal fishing have further intensified demand for maritime drones in defense and law enforcement. Export controls and technology transfer restrictions are creating opportunities for domestic manufacturers, while also challenging global supply chains. The growing need for environmental monitoring and disaster response is expanding the market’s civilian and commercial applications.

Key Takeaways

Market Growth: The Maritime Drones Market is expected to reach USD 12.8 Billion by 2034, driven by maritime security needs, technological innovation, and the expansion of offshore industries.

ProductTypeDominance: Unmanned Surface Vehicles (USVs) lead the segment, favored for their versatility in surveillance, inspection, and logistics.

ApplicationDominance: Naval Defense holds the largest share, supported by rising defense budgets and modernization programs.

Driver: Key growth drivers include increasing maritime security threats, cost pressures in offshore operations, and regulatory support for unmanned systems.

Restraint: High acquisition and integration costs, as well as regulatory and operational complexities, hinder broader adoption.

Opportunity: The market is poised for growth through AI integration, smart port initiatives, and expansion into commercial and environmental monitoring.

Trend: Emerging trends include swarm drone operations, hybrid propulsion systems, and integration with satellite and IoT networks.

RegionalAnalysis: North America leads due to defense investment and innovation; Asia-Pacific is the fastest-growing region; Europe remains strong in technology and collaboration.

Product Type Analysis

Unmanned Surface Vehicles (USVs) dominate the maritime drones market, owing to their adaptability for a wide range of missions, including surveillance, mine countermeasures, and cargo delivery. USVs are favored for their ease of deployment, modular payload options, and ability to operate in both open ocean and littoral environments. Their cost-effectiveness and operational flexibility make them the preferred choice for both military and commercial users. Unmanned Underwater Vehicles (UUVs), including autonomous underwater vehicles (AUVs) and remotely operated vehicles (ROVs), are critical for subsea inspection, mine detection, and scientific research. Their ability to operate at great depths and in hazardous environments is driving adoption in offshore energy and marine research.

Application Analysis

Naval Defense is the leading application, accounting for over 50% of the market share. Maritime drones are increasingly integral to naval operations, providing persistent surveillance, anti-submarine warfare, and mine countermeasure capabilities. Defense sector demand is sustained by ongoing modernization, procurement programs, and the strategic imperative to maintain maritime domain awareness. Commercial Shipping is a rapidly growing segment, leveraging drones for hull inspection, cargo monitoring, and port security. The adoption of drones in logistics and smart port operations is improving efficiency and reducing operational risks. Environmental Monitoring and Search & Rescue are expanding applications, utilizing drones for pollution tracking, wildlife monitoring, and rapid response in disaster scenarios.

Region Analysis

North America leads with more than 35% market share, driven by U.S. Navy investments, advanced R&D, and a strong ecosystem of technology providers. The region benefits from early adoption, robust regulatory frameworks, and a focus on maritime security. Asia-Pacific is the fastest-growing region, propelled by rising defense spending, territorial disputes in the South China Sea, and the expansion of commercial shipping and offshore energy sectors. Countries like China, Japan, South Korea, and India are investing heavily in maritime drone capabilities. Europe maintains a significant market presence, supported by established maritime industries, collaborative defense projects (such as the European Defence Fund), and a focus on environmental monitoring in the North Sea and Mediterranean. Latin America and Middle East & Africa are emerging markets, with growth driven by port security, anti-piracy operations, and offshore resource development.

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

Teledyne Technologies Inc., Kongsberg Gruppen, L3Harris Technologies, Elbit Systems Ltd., Saab AB, ECA Group, Atlas Elektronik, Ocean Aero, ASV Global, Hydroid Inc.

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA MARITIME DRONES CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA MARITIME DRONES CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE MARITIME DRONES CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE MARITIME DRONES CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC MARITIME DRONES CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA MARITIME DRONES CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA MARITIME DRONES CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA MARITIME DRONES CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA MARITIME DRONES CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2024)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2024)

FIGURE 176 GLOBAL MARITIME DRONES CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2024–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Players Analysis

Teledyne Technologies Inc.: is known for its advanced underwater drones, both autonomous (AUVs) and remotely operated (ROVs). Their products are widely used in defense (like naval surveillance), energy (such as offshore oil and gas inspection), and scientific research (like oceanography).

L3Harris Technologies: specializes in unmanned surface vehicles (USVs) and offers integrated maritime surveillance solutions. Their technology is used by both military and commercial customers for tasks like patrolling, monitoring, and data collection.

Kongsberg Maritime: is famous for its autonomous underwater and surface vehicles. Their systems are used by navies for mine detection, by researchers for mapping the ocean floor, and by commercial operators for subsea inspection.

Elbit Systems: provides a variety of unmanned maritime systems, mainly for naval defense and homeland security. Their solutions help navies with surveillance, reconnaissance, and protection of coastal areas.

Ocean Aero: is an innovator in hybrid drones that can operate both on the ocean surface and underwater. These drones are designed for long-term ocean monitoring, collecting data for environmental research, defense, and commercial applications.

ECA Group: focuses on mine countermeasure drones and integrated unmanned systems for naval use. Their technology helps navies detect and neutralize underwater mines, making sea routes safer.

Saab AB: offers advanced unmanned underwater vehicles (UUVs) and unmanned surface vehicles (USVs) for defense, surveillance, and research. Their products are used for tasks like underwater reconnaissance, mine detection, and scientific exploration.

Key Market Players

Teledyne Technologies Inc.

Kongsberg Gruppen

L3Harris Technologies

Elbit Systems Ltd.

Saab AB

ECA Group

Atlas Elektronik

Ocean Aero

ASV Global

Hydroid Inc.

Drivers:

Rising Maritime Security Threats:

The growing incidents of piracy, smuggling, illegal fishing, and territorial disputes are making maritime security a top priority for many nations. Maritime drones are increasingly used because they provide real-time situational awareness and can be rapidly deployed for surveillance and response. This makes them essential tools for modern naval and coast guard operations, helping authorities monitor vast ocean areas efficiently and respond quickly to threats.

Offshore Industry Expansion:

As offshore oil & gas, wind energy, and undersea cable projects expand, there is a greater need for drones that can perform inspection, maintenance, and environmental monitoring. These drones help reduce operational risks and costs by accessing hazardous or hard-to-reach areas, ensuring the safety and efficiency of offshore operations while minimizing the need for human intervention in dangerous environments.

Restraints:

High Acquisition and Integration Costs:

Acquiring advanced maritime drone platforms, along with their specialized payloads (such as sensors and communication systems), requires a significant financial investment. Additionally, integrating these drones with existing maritime systems and infrastructure can be complex and costly. These high upfront and ongoing costs can be a major barrier, especially for smaller operators and organizations in developing regions, limiting their ability to adopt and benefit from maritime drone technology.

Regulatory and Operational Complexity:

Operating maritime drones involves navigating a complex web of international and national maritime regulations, which can vary widely between regions. Ensuring that drones can safely operate alongside manned vessels, while also addressing cybersecurity risks, adds further layers of operational complexity. These regulatory and technical challenges can slow down the adoption of maritime drones, as organizations must invest time and resources to ensure compliance and safe integration into existing maritime operations.

Opportunities:

AI and Autonomous Navigation:

The integration of artificial intelligence (AI), machine learning, and advanced sensor fusion is revolutionizing maritime drones by enabling them to operate fully autonomously. This means drones can navigate complex environments, avoid obstacles, and make real-time decisions without human intervention. These capabilities also support predictive maintenance—drones can monitor their own systems and predict when repairs are needed, reducing downtime and costs. Overall, AI-driven autonomy enhances mission effectiveness, allowing drones to perform tasks like surveillance, inspection, and data collection more efficiently and reliably.

Smart Port and Logistics Integration:

As global trade volumes increase, ports and logistics hubs are turning to drones for enhanced security, faster cargo inspection, and automated logistics operations. Drones can patrol port perimeters, monitor cargo movement, and even assist in inventory management, making port operations safer and more efficient. The adoption of drones in these environments creates new commercial opportunities, as they help reduce labor costs, speed up processes, and improve overall operational visibility.

Environmental and Disaster Response:

With growing awareness of ocean health and the impacts of climate change, there is rising demand for drones in environmental monitoring and disaster response. Maritime drones can be deployed to track pollution, monitor marine life, and collect data on water quality. In disaster scenarios—such as oil spills, hurricanes, or shipwrecks—drones provide rapid situational awareness, support search and rescue missions, and help coordinate emergency responses. Their ability to access remote or hazardous areas quickly makes them invaluable tools for protecting the environment and saving lives. In summary, these opportunities highlight how maritime drones are becoming smarter, more integrated into critical infrastructure, and essential for both commercial and environmental missions.

Trends

Swarm Drone Operations:

This trend involves deploying multiple drones that work together in a coordinated manner, much like a swarm of bees. These swarms can cover larger areas for surveillance, conduct search and rescue missions more efficiently, and perform complex tasks like mine detection and countermeasures. By working as a team, swarm drones increase operational effectiveness, provide redundancy, and ensure better coverage than single-drone operations.

Hybrid Propulsion and Endurance:

Recent advances in hybrid-electric and solar-powered propulsion systems are allowing drones to fly for much longer periods without needing to refuel or recharge. This extended endurance means drones can undertake longer missions, monitor vast ocean areas, and reduce the frequency and cost of maintenance or battery changes. As a result, operational costs go down and mission capabilities expand.

Digital Integration:

The integration of cloud-based data analytics, Internet of Things (IoT) connectivity, and satellite communications is transforming how maritime drones are managed and how their data is used. These technologies enable real-time mission management, remote control from anywhere in the world, and instant sharing of data with all relevant stakeholders. This digital connectivity ensures that decision-makers have up-to-date information and can coordinate responses quickly and effectively.

Recent Developments

In June 2025: Teledyne Technologies introduced the Gavia Pro, a next-generation Autonomous Underwater Vehicle (AUV). This new model features AI-driven navigation, which allows it to make smarter decisions underwater, avoid obstacles, and optimize its route in real time. Its extended endurance means it can operate for longer periods and reach greater depths, making it ideal for deep-sea exploration and defense missions such as surveillance or mine detection.

In March 2025: L3Harris Technologies secured a major contract with the U.S. Navy to supply and integrate autonomous Unmanned Surface Vehicles (USVs) for mine countermeasure operations. This means L3Harris will provide advanced surface drones that can detect and neutralize underwater mines, improving naval safety and operational efficiency. The size of the contract highlights the growing trust in autonomous systems for critical defense tasks.

November 2024: Kongsberg Maritime partnered with Shell to deploy autonomous drones for inspecting and maintaining offshore wind farms. These drones can perform regular checks, spot maintenance needs, and even carry out minor repairs, all without human intervention. This partnership enhances safety (by reducing the need for human workers in hazardous environments) and boosts efficiency in the rapidly growing renewable energy sector.

September 2024: Elbit Systems launched an upgraded version of its Seagull Unmanned Surface Vehicle (USV), now equipped with advanced anti-submarine warfare and electronic warfare payloads. This makes the Seagull more versatile and effective for naval defense, especially in detecting and countering submarines and electronic threats. The company is targeting export markets in Asia-Pacific and Europe, reflecting strong international demand for such advanced maritime security solutions.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, Unmanned Underwater Vehicles (UUVs), Hybrid Maritime Drones) Application Type (Naval Defense, Commercial Shipping, Offshore Energy, Environmental Monitoring, Search & Rescue) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, Unmanned Underwater Vehicles (UUVs), Hybrid Maritime Drones) Application Type (Naval Defense, Commercial Shipping, Offshore Energy, Environmental Monitoring, Search & Rescue) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, Unmanned Underwater Vehicles (UUVs), Hybrid Maritime Drones) Application Type (Naval Defense, Commercial Shipping, Offshore Energy, Environmental Monitoring, Search & Rescue) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")

, Unmanned Underwater Vehicles (UUVs), Hybrid Maritime Drones) Application Type (Naval Defense, Commercial Shipping, Offshore Energy, Environmental Monitoring, Search & Rescue) Industry Region & Key Players-Industry Segment Overview, Market Dynamics, Competitive Strategies, Trends & Forecast 2025-2034")