- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Medical Affairs Technology Market Size, Share | CAGR 11.7%

Global Medical Affairs Technology Market Size, Share, Growth Analysis By Offering (Software Platforms, Services & Consulting, Content Management Tools, Analytics & Reporting), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (MSL Enablement, Scientific Content Management, Real-World Evidence Generation, Regulatory Affairs Support, HCP Engagement & CRM), By End-User, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 5.38 Billion | USD 14.92 Billion | 11.7% | North America, 42.3% |

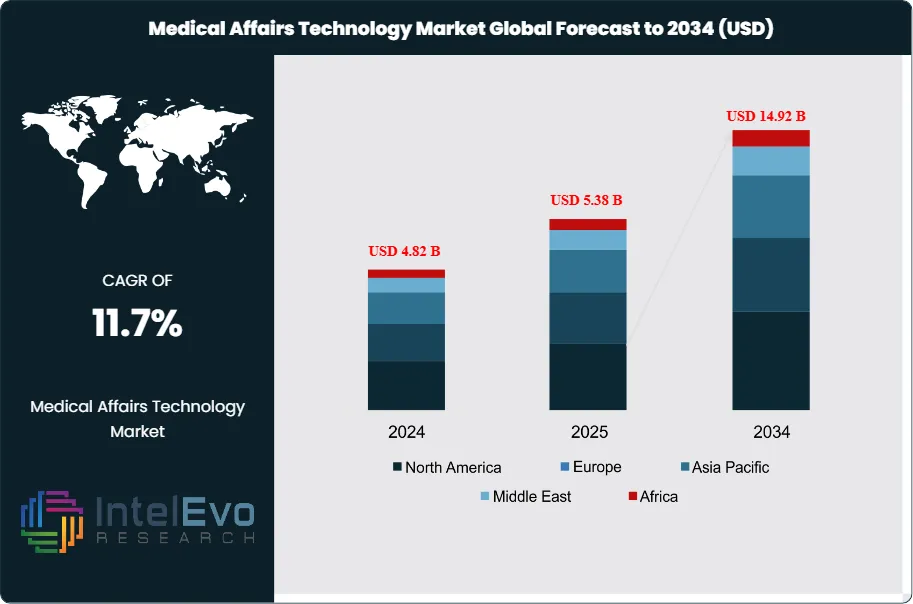

The Medical Affairs Technology Market was valued at approximately USD 4.82 Billion in 2024 and reached USD 5.38 Billion in 2025. The market is projected to grow to USD 14.92 Billion by 2034, expanding at a CAGR of 11.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 9.54 Billion over the analysis period, reflecting accelerating investment in digital platforms that support scientific engagement, regulatory compliance, and evidence generation across the pharmaceutical and biotechnology sectors.

Get More Information about this report -

Request Free Sample ReportMedical affairs technology encompasses a broad suite of software and services designed to enable medical science liaison (MSL) field activities, scientific content management, health care professional (HCP) engagement, real-world evidence (RWE) generation, and regulatory intelligence. The market's sustained growth reflects structural shifts in how biopharma companies communicate scientific value to payers, physicians, and regulatory bodies. As commercial and medical boundaries converge, organizations are investing heavily in integrated platforms that comply with evolving FDA guidance on scientific exchange and adhere to PhRMA Medical Affairs principles.

Demand for medical affairs technology is concentrated among large biopharmaceutical companies navigating complex product launches across oncology, immunology, and rare disease. These organizations face increasing payer scrutiny, requiring robust real-world evidence pipelines and evidence synthesis tools embedded directly into MSL workflows. Cloud-based deployments now account for 61.4% of total revenue in 2025, driven by enterprise-wide digital transformation mandates and the need for scalable platforms that support global MSL teams operating across multiple regulatory jurisdictions.

Artificial intelligence is redefining the medical affairs technology value proposition. Generative AI capabilities are being embedded into MSL coaching engines, scientific query response tools, and key opinion leader (KOL) profiling platforms. Adoption of AI-assisted medical affairs tools reached 34.8% of enterprise deployments in 2025, up from 17.2% in 2022, with analysts projecting over 70% penetration by 2030. Vendors integrating large language models trained on peer-reviewed literature are gaining rapid traction, particularly in oncology and neurology where scientific complexity is highest.

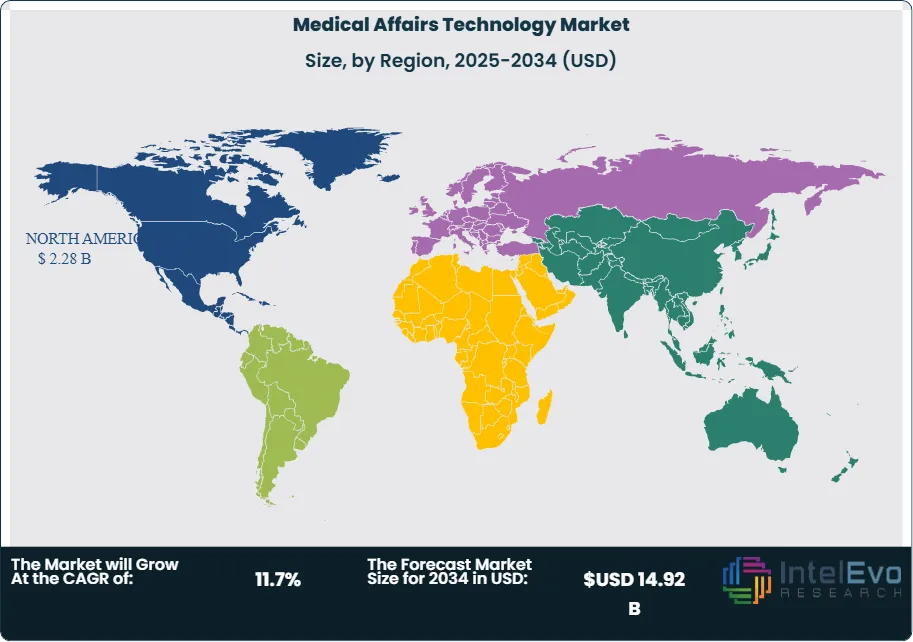

North America accounted for 42.3% of global medical affairs technology revenue in 2025, reflecting the region's dense concentration of biopharma headquarters, FDA regulatory requirements around scientific exchange, and high MSL field-force density. Europe is the second-largest region at 26.1%, with adoption accelerating in Germany, France, and Switzerland following updated EMA guidelines on medical information dissemination. Asia Pacific represents the fastest-growing region, driven by rapid pharmaceutical market expansion in China, Japan, and India, where regulatory modernization and localization of global medical affairs operations are generating new platform deployment demand.

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (MSL Enablement, Scientific Content Management, Real-World Evidence Generation, Regulatory Affairs Support, HCP Engagement & CRM), By End-User, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global medical affairs technology market was valued at USD 5.38 Billion in 2025 and is forecast to reach USD 14.92 Billion by 2034, expanding at a CAGR of 11.7% over the 2026–2034 forecast period.

- Segment Dominance: By Offering, software platforms held the leading position with 58.3% of total market share in 2025, driven by enterprise demand for integrated MSL enablement, content management, and HCP engagement solutions.

- Segment Dominance: By Application, MSL Enablement was the largest application segment at 29.7% of global revenue in 2025, reflecting the critical role of field-based scientific engagement in modern pharmaceutical commercialization strategies.

- Driver: Rising biopharma pipeline complexity, particularly in oncology (51% of late-stage assets in 2025) and rare disease, is compelling organizations to invest in specialized medical affairs technology to manage scientific exchange, real-world evidence, and regulatory communications simultaneously.

- Restraint: Data privacy regulations including GDPR, HIPAA, and emerging national HCP interaction transparency laws impose significant compliance overhead, increasing implementation costs by 18–24% and slowing adoption among mid-market pharmaceutical companies.

- Opportunity: Integration of AI-powered scientific content generation and pharmacovigilance signal detection into unified medical affairs platforms represents an addressable incremental market of USD 2.3 Billion by 2034, as organizations seek to reduce manual scientific review timelines by 40–60%.

- Trend: Convergence of commercial CRM and medical affairs platforms into single orchestrated customer engagement systems is accelerating, with 38.4% of biopharma companies adopting unified commercial-medical data environments in 2025, up from 19.1% in 2022.

- Regional Analysis: North America remained the dominant region with a 42.3% market share, equivalent to USD 2.28 Billion in revenue in 2025, anchored by dense biopharma headquarters, stringent FDA scientific exchange regulations, and high MSL deployment ratios.

Competitive Landscape Overview

The medical affairs technology market exhibits a moderately consolidated structure, with the top four vendors — Veeva Systems, IQVIA Holdings, Salesforce Health Cloud, and Medidata Solutions — collectively accounting for approximately 52.4% of total global revenue in 2025. Competition centers on platform breadth, AI integration depth, and the ability to serve global medical affairs operations with regulatory-compliant scientific content management. The market has experienced a meaningful uptick in M&A activity since 2023, as platform vendors acquire specialized analytics and pharmacovigilance firms to extend their medical affairs footprint. New entrants with AI-native architectures are intensifying pressure on legacy CRM-based vendors, particularly in the MSL coaching and scientific query management segments.

Competitive Matrix

| Company | HQ | Position | Key Product | Geo Strength | Recent Move |

| Veeva Systems | USA | Leader | Veeva Medical CRM | North America | Acquired Crossix for HCP data, Jan 2025 |

| IQVIA Holdings | USA | Leader | Orchestrated Customer Engagement | North America / Europe | Launched AI-driven MSL insights platform, Mar 2025 |

| Medidata Solutions | USA | Challenger | Medidata Rave Medical Affairs | North America / Europe | Partnered with Roche for real-world evidence integration, Jun 2025 |

| Inovalon | USA | Challenger | Inovalon Medical Affairs Suite | North America | Expanded claims analytics to EU markets, Sep 2025 |

| Salesforce Health Cloud | USA | Leader | Health Cloud for Medical Affairs | Global | Integrated GenAI co-pilot for MSL workflows, Nov 2025 |

| Zinc Health | UK | Niche Player | Zinc Medical Affairs Platform | Europe | Raised Series C USD 45M for EU MSL expansion, Feb 2025 |

| Aktana | USA | Niche Player | Aktana Contextual Intelligence | North America / Asia Pacific | Deployed AI recommendation engine for oncology MSLs, Apr 2025 |

| ProNAi Therapeutics (MedComms) | Canada | Niche Player | MedComms Digital Platform | North America | Entered strategic alliance with Pfizer medical affairs, Aug 2025 |

By Offering

The medical affairs technology market by offering is bifurcated into software platforms and services and consulting. Software platforms dominate the market, commanding 58.3% of global revenue, equivalent to USD 3.14 Billion in 2025. This segment encompasses dedicated MSL enablement systems, scientific content repositories, HCP engagement platforms, RWE data management tools, and analytics dashboards. Demand is concentrated among large biopharmaceutical organizations managing multi-country product portfolios with diverse MSL field teams. Cloud-native software is displacing legacy on-premise systems, with SaaS deployments growing at 13.1% annually through 2034. Vendors offering pre-built integrations with third-party clinical data sources and regulatory submission systems command premium pricing, with enterprise contracts averaging USD 1.2–3.8 Million annually.

Services and consulting hold a 41.7% share valued at USD 2.24 Billion in 2025 and are growing at 10.1% CAGR through 2034. This segment includes implementation services, medical affairs strategy consulting, content development outsourcing, MSL training programs, and managed analytics services. Mid-size pharmaceutical companies without in-house medical affairs technology expertise rely heavily on service providers to configure and operate platforms. The managed services sub-segment is particularly robust, growing at 14.6% annually as organizations seek to transfer operational complexity to specialized vendors while maintaining compliance with FDA and EMA scientific exchange guidelines.

By Deployment Mode

Cloud-based deployment is the dominant mode in the medical affairs technology market, representing 61.4% of total revenue in 2025 at USD 3.30 Billion. Pharmaceutical organizations are migrating to cloud platforms to support globally distributed MSL teams, enable real-time data synchronization across regulatory jurisdictions, and reduce IT infrastructure costs. Major platform vendors including Veeva and Salesforce operate entirely on cloud architectures, benefiting from continuous feature updates and enterprise-scale security compliance. Cloud adoption is accelerating particularly in Asia Pacific and Latin America, where biopharma companies are establishing regional medical affairs operations without legacy infrastructure constraints.

On-premise deployments account for 24.8% of the market at USD 1.34 Billion in 2025, primarily serving large pharmaceutical companies in the EU and Japan where data localization regulations and stringent IT governance policies require internal data hosting. The on-premise segment is contracting at a 2.3% annual rate as regulatory clarity on cloud data residency improves. Hybrid deployment architectures represent 13.8% of the market at USD 742 Million in 2025, catering to enterprises requiring cloud agility for field-force tools while maintaining on-premise control over sensitive patient interaction and pharmacovigilance data.

By Application

MSL enablement is the largest application segment in the medical affairs technology market, representing 29.7% of revenue at USD 1.60 Billion in 2025 and growing at 12.4% CAGR. MSL platforms integrate call planning, scientific content delivery, interaction logging, and KOL relationship management into unified mobile-accessible environments. Demand is highest in oncology and rare disease therapy areas, where MSLs must communicate complex mechanism-of-action data and support investigator-initiated trials. AI-powered call briefing and sentiment analysis tools embedded in MSL platforms are delivering measurable productivity gains, with leading adopters reporting a 31% increase in high-value HCP interactions per MSL per quarter.

Scientific content and publication management holds 22.6% of global revenue at USD 1.22 Billion in 2025. This segment supports the creation, review, approval, and distribution of scientific materials including medical information letters, publication plans, slide kits, and congress materials. Regulatory requirements under 21 CFR Part 11 and ICH E6(R2) drive demand for audit-trail-enabled content management systems. Real-world evidence generation and analytics represents 18.9% of the market at USD 1.02 Billion, fueled by growing payer and regulatory reliance on post-approval evidence. HCP engagement and CRM accounts for 17.4% at USD 936 Million, while regulatory affairs support tools represent the remaining 11.4% at USD 614 Million in 2025.

By End-User

Biopharmaceutical companies constitute the dominant end-user segment in the medical affairs technology market, accounting for 64.8% of global revenue at USD 3.49 Billion in 2025. Tier-1 biopharma organizations — those with revenues exceeding USD 5 Billion — are the primary investment drivers, typically deploying enterprise medical affairs platforms across 30–120 MSL field personnel per major therapeutic area. Patent cliff management is a critical buying trigger; companies facing loss of exclusivity on blockbuster assets are investing in medical affairs technology to accelerate generic defense strategies through real-world evidence and expanded label activities.

Medical device manufacturers represent 14.3% of the market at USD 770 Million in 2025, increasingly deploying medical affairs platforms to support physician training, post-market clinical follow-up, and EU MDR compliance documentation. Contract research organizations account for 12.1% at USD 651 Million, leveraging medical affairs platforms to deliver managed MSL programs for small and mid-size pharma clients without in-house field forces. Healthcare systems and academic medical centers represent the remaining 8.8% at USD 473 Million, primarily using RWE and scientific content tools to support value-based care initiatives and physician-investigator programs.

Regional Analysis

North America Medical Affairs Technology Market

North America leads the global medical affairs technology market with a 42.3% share, equivalent to USD 2.28 Billion in 2025. The United States accounts for 88.6% of regional revenue, driven by the world's largest concentration of biopharma headquarters, the highest per-capita MSL deployment rates globally, and FDA requirements governing scientific exchange and off-label communication. The US Inflation Reduction Act's drug pricing provisions are reshaping medical affairs strategy, pushing organizations to invest earlier in real-world evidence and comparative effectiveness data to defend formulary positions. Canada represents 7.2% of North American revenue, with strong adoption of medical affairs platforms among mid-size specialty pharma companies operating in oncology and immunology. Mexico accounts for the remaining 4.2%, with growth driven by multinational biopharma regional hub expansions in Mexico City.

Europe Medical Affairs Technology Market

Europe holds 26.1% of global medical affairs technology revenue at USD 1.40 Billion in 2025, supported by a strong regulatory framework under EMA scientific advice procedures and a high concentration of multinational pharmaceutical headquarters in Switzerland, Germany, and the UK. Germany is the largest European market at 22.4% of regional revenue, driven by institutional adoption among Bayer, Boehringer Ingelheim, and Merck KGaA, along with stringent FSA (Fachgesellschaft-kompatible Scienceinformationssystem) requirements. France contributes 17.8% of European revenue, with the ANSM's requirements for medical information documentation accelerating platform adoption. Switzerland's 15.3% share reflects Roche and Novartis driving best-in-class medical affairs technology globally. The United Kingdom is recovering post-Brexit pharmaceutical repositioning, with NICE-driven evidence requirements fueling RWE platform investment.

Asia Pacific Medical Affairs Technology Market

Asia Pacific represents 19.4% of global revenue at USD 1.04 Billion in 2025 and is the fastest-growing regional market, expanding at a 15.3% CAGR through 2034. China is the largest APAC market at 34.2% of regional revenue, with the NMPA's accelerating drug approval reforms and a rapidly maturing domestic biopharma sector driving platform investment. Japanese pharmaceutical companies represent 28.6% of APAC revenue, with established MSL field forces at organizations such as Takeda, Astellas, and Eisai increasingly upgrading to AI-enabled engagement platforms. India contributes 18.1% of regional revenue, supported by the world's largest pharmaceutical generics industry deploying medical affairs tools for global market expansion. South Korea is an emerging growth market at 10.4% of APAC revenue, with Samsung Biologics and Celltrion expanding medical affairs technology investments to support biosimilar market launches across the US and EU.

Latin America Medical Affairs Technology Market

Latin America holds 7.4% of global medical affairs technology revenue at USD 398 Million in 2025. Brazil dominates the regional market at 47.3% of LATAM revenue, with ANVISA's evolving digital health regulations and the presence of multinational biopharma affiliates driving adoption. Mexico contributes 24.6% of regional revenue, benefiting from its position as a regional operations hub for US-based pharmaceutical companies. Colombia is an emerging market at 9.8% of LATAM revenue, supported by government healthcare infrastructure investment and growing clinical trial activity. Investment in cloud-based MSL platforms is particularly strong across the region, as pharmaceutical companies seek scalable tools that accommodate high field-force turnover rates without significant retraining costs.

Middle East & Africa Medical Affairs Technology Market

The Middle East and Africa region accounts for 4.8% of global medical affairs technology revenue at USD 258 Million in 2025. The UAE leads the regional market with 31.4% of MEA revenue, driven by Dubai's emergence as a regional pharmaceutical hub and MOHAP's digital health strategy encouraging technology adoption across biopharma affiliates. Saudi Arabia represents 27.2% of MEA revenue, with Vision 2030 healthcare transformation initiatives encouraging multinational pharmaceutical companies to invest in local medical affairs infrastructure. South Africa contributes 18.6% of MEA revenue, representing the primary entry point for medical affairs technology penetration across Sub-Saharan Africa. Regional growth is constrained by lower digital infrastructure maturity in parts of Africa and conservative procurement cycles, but Gulf Cooperation Council markets are expected to outperform the regional average through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Offering

- Software Platforms

- Services & Consulting

- Content Management Tools

- Analytics & Reporting

By Deployment Mode

- Cloud-Based

- On-Premise

- Hybrid

By Application

- Medical Science Liaison (MSL) Enablement

- Scientific Content & Publication Management

- Real-World Evidence (RWE) Generation

- Regulatory Affairs Support

- HCP Engagement & CRM

By End-User

- Biopharmaceutical Companies

- Medical Device Manufacturers

- Contract Research Organizations (CROs)

- Healthcare Systems

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.38 B |

| Forecast Revenue (2034) | USD 14.92 B |

| CAGR (2025-2034) | 11.7% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Offering (Software Platforms, Services & Consulting, Content Management Tools, Analytics & Reporting), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (Medical Science Liaison (MSL) Enablement, Scientific Content & Publication Management, Real-World Evidence (RWE) Generation, Regulatory Affairs Support, HCP Engagement & CRM ), By End-User (Biopharmaceutical Companies, Medical Device Manufacturers, Contract Research Organizations (CROs), Healthcare Systems) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | VEEVA SYSTEMS, IQVIA HOLDINGS, SALESFORCE HEALTH CLOUD, MEDIDATA SOLUTIONS (DASSAULT SYSTEMES), INOVALON, AKTANA, ZINC HEALTH, ORACLE HEALTH SCIENCES, IBM WATSON HEALTH (MERATIVE), BIGTINCAN (MEDIA PHARMA), SYMPLUR (RELATIVITY HEALTH), INDEGENE, PROSCAPE TECHNOLOGIES, PITCHER AG, DATAVANT, CEGEDIM HEALTHCARE SOLUTIONS, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (MSL Enablement, Scientific Content Management, Real-World Evidence Generation, Regulatory Affairs Support, HCP Engagement & CRM), By End-User, Industry Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (MSL Enablement, Scientific Content Management, Real-World Evidence Generation, Regulatory Affairs Support, HCP Engagement & CRM), By End-User, Industry Trends & Forecast 2026-2034")

, By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (MSL Enablement, Scientific Content Management, Real-World Evidence Generation, Regulatory Affairs Support, HCP Engagement & CRM), By End-User, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Medical Affairs Technology Market?

The Global Medical Affairs Technology Market was valued at USD 4.82 Billion in 2024 and is projected to reach USD 14.92 Billion by 2034, growing at a CAGR of 11.7% from 2026 to 2034, driven by increasing digital transformation in life sciences, rising adoption of AI-powered medical affairs platforms, and growing demand for real-world evidence and omnichannel engagement solutions.

Who are the major players in the Medical Affairs Technology Market?

VEEVA SYSTEMS, IQVIA HOLDINGS, SALESFORCE HEALTH CLOUD, MEDIDATA SOLUTIONS (DASSAULT SYSTEMES), INOVALON, AKTANA, ZINC HEALTH, ORACLE HEALTH SCIENCES, IBM WATSON HEALTH (MERATIVE), BIGTINCAN (MEDIA PHARMA), SYMPLUR (RELATIVITY HEALTH), INDEGENE, PROSCAPE TECHNOLOGIES, PITCHER AG, DATAVANT, CEGEDIM HEALTHCARE SOLUTIONS, OTHERS

Which segments covered the Medical Affairs Technology Market?

By Offering (Software Platforms, Services & Consulting, Content Management Tools, Analytics & Reporting), By Deployment Mode (Cloud-Based, On-Premise, Hybrid), By Application (Medical Science Liaison (MSL) Enablement, Scientific Content & Publication Management, Real-World Evidence (RWE) Generation, Regulatory Affairs Support, HCP Engagement & CRM ), By End-User (Biopharmaceutical Companies, Medical Device Manufacturers, Contract Research Organizations (CROs), Healthcare Systems)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Medical Affairs Technology Market

Published Date : 11 May 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date