- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Medical Device Outsourcing Market Size 2025–2034 | CAGR 13.1%

Global Medical Device Outsourcing Market Size, Share, Growth & Analysis By Service (Contract Manufacturing, Component & Device Manufacturing, Design & Development, Quality Assurance, Regulatory Affairs, Clinical Trials Support), By Application (Cardiology, Diagnostic Imaging, Drug Delivery, IVD, Surgical Devices), By Class (Class I, Class II, Class III), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034

Report Overview

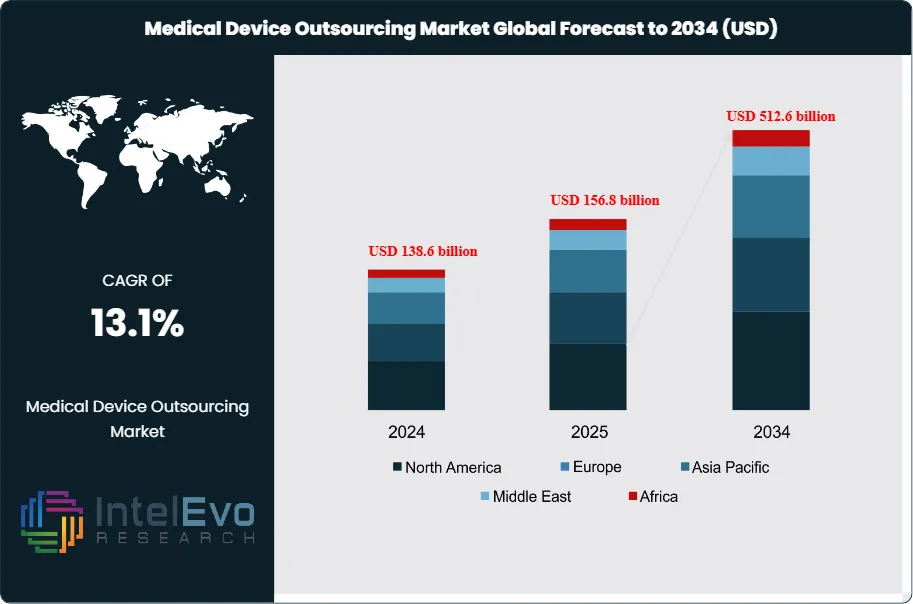

The Medical Device Outsourcing Market is estimated to reach approximately US$ 156.8 billion in 2025 and is projected to expand to around US$ 512.6 billion by 2034, registering a strong compound annual growth rate (CAGR) of about 13.1% during the forecast period from 2026 to 2034. Market growth is driven by rising demand for cost-efficient manufacturing, increasing regulatory complexity, and accelerating innovation in high-value medical devices such as implantables, diagnostics, and minimally invasive systems. OEMs are increasingly outsourcing design, prototyping, testing, and regulatory services to reduce time-to-market and improve scalability. Additionally, growing adoption of contract manufacturing and development services across emerging economies continues to reshape global supply chains, reinforcing long-term market momentum and platform visibility.

Get More Information about this report -

Request Free Sample ReportGrowing regulatory complexity, higher compliance costs, and pressure on margins are pushing medical device manufacturers to rely more on external partners for design, production, and regulatory support. Outsourcing allows original equipment manufacturers to release capital tied up in facilities, redirect spending toward innovation, and shorten time-to-market for advanced devices.

Regulation remains a central force in shaping demand. Tighter approval standards from agencies such as the U.S. Food and Drug Administration and European authorities raise the cost and risk of in-house development. Specialist contract manufacturers spread this burden across multiple clients, maintain dedicated regulatory teams, and operate standardized quality systems. This shift strengthens large, full-service providers but increases dependence on a narrower supplier base and heightens exposure to disruption.

Technology trends accelerate outsourcing further. AI-enabled design tools, automated inspection, and digital production platforms reduce defect rates and support miniaturized components for wearables, home-based diagnostics, and minimally invasive devices. Many manufacturers do not hold these capabilities at scale, so they engage partners with advanced robotics and data-rich manufacturing environments. Partnerships such as the supply and services agreement between Avantor and Catalent show how integrated material supply, laboratory support, and manufacturing services create end-to-end ecosystems around leading contract providers.

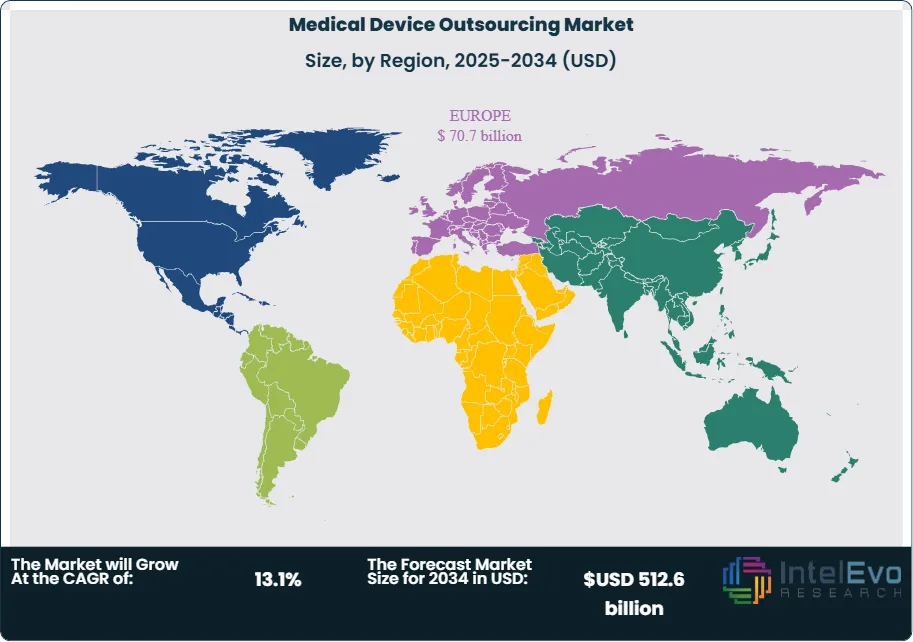

Regional dynamics guide capital allocation. North America accounted for about 42.4% of global revenue in 2024, or roughly US$ 60.4 Billion, supported by a large base of OEMs, regulatory consulting capacity, and high adoption of complex implants and diagnostic systems. Asia Pacific is emerging as the fastest-growing hub, with estimated low-teens annual growth driven by expanding manufacturing clusters in China and India and rising demand for specialized care. Europe maintains a substantial share, backed by a medtech innovation base but tempered by reimbursement pressure and cost-containment policies.

Strategic partnerships and outsourcing agreements, including the collaboration between NAMSA and InspireMD to accelerate device development and commercialization, show how external partners shape the product life cycle. Providers that combine regulatory insight, digital manufacturing, and global supply coverage are positioned to capture value as manufacturers consolidate their vendor base and move toward long-term, integrated outsourcing models.

, By Application (Cardiology, Diagnostic Imaging, Drug Delivery, IVD, Surgical Devices), By Class (Class I, Class II, Class III), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market generated revenue of US$ 156.8 billion in 2025 and is projected to reach US$ 512.6 billion by 2034, delivering a CAGR of 13.1%, 2026-2034.

- Segment Dominance: Contract manufacturing leads the service segment with a 51.7% share, 2023, as OEMs consolidate production with large-scale partners. This leadership likely translates into estimated: 75.0 billion USD, 2024 in outsourced manufacturing value as volumes shift from in-house lines.

- Segment Dominance: In applications, cardiology devices capture the largest share at 42.3%, 2023, reflecting high demand for interventional, monitoring, and implantable solutions. Class II devices also command the highest regulatory class share at 49.4%, 2023, concentrating outsourced activity in mid-risk categories.

- Driver: Rising complexity and cost of in-house production motivate OEMs to outsource, with estimated: 15.0% operating cost reduction per program, 2024 when they shift to specialized partners. Stricter regulatory expectations further push manufacturers toward partners with scaled quality systems and compliance expertise, 2024.

- Restraint: Dependence on a concentrated vendor base raises supply continuity risk, with estimated: 20.0% of OEMs, 2024 reporting moderate-to-high exposure to single-source contract manufacturers. Regulatory lapses or quality issues at an outsourced facility can trigger recalls and revenue loss above estimated: 1.0 billion USD, 2024 across the industry.

- Opportunity: Growing adoption of complex minimally invasive and home-care devices opens new outsourcing demand pools, supporting estimated: 14.0% CAGR in high-value device outsourcing, 2024-2034. Vendors that add design, testing, and regulatory services to manufacturing can raise wallet share per client by estimated: 25.0%, 2024.

- Trend: AI-enabled design, automated inspection, and digital manufacturing dashboards increasingly shape outsourcing contracts, with estimated: 35.0% of new agreements, 2024 including explicit digital or analytics components. Vendors that invest in data-driven process control can cut defect rates by estimated: 30.0%, 2024, strengthening their competitive position.

- Regional Analysis: North America leads the market with a 42.4% share, 2023, anchored by a large OEM base, strong regulatory expertise, and high adoption of complex devices. Asia Pacific emerges as the fastest-growing hub at estimated: 15.0% CAGR, 2024-2034, while Europe maintains an estimated: 25.0% share, 2023 under cost-containment pressure.

Type Analysis

High-performance concrete and self-consolidating concrete account for a growing share of material use in structural and architectural applications. Demand continues to rise in 2025 as builders pursue consistent strength, improved placement efficiency, and reduced maintenance costs. Global construction projects in transport, utilities, and high-density housing are increasing the need for materials that provide predictable performance under load. High-performance formulations have gained particular traction in large infrastructure programs across North America, Europe, and Asia, where long service life and controlled curing conditions are key procurement requirements.

Self-consolidating concrete shows steady expansion as contractors place emphasis on productivity and uniform finishes. The ability to reduce labor hours and achieve better formwork results is driving interest from commercial and industrial developers. Other specialty concrete types retain relevance in smaller or mixed-use projects where customized mixes are necessary. Suppliers that provide consistent batching, digital monitoring, and material traceability are gaining preference among large contractors who must meet strict quality norms.

Growth through 2030 is supported by rising urban development budgets across major economies and stronger adoption of mechanized placement equipment. Global spending on concrete materials is projected to increase at an annual rate near 6 to 7 percent, supported by expansion in transport corridors, renewable energy installations, and mid-rise residential buildings.

Application Analysis

Pavers represent a major share of consumption across municipal and private development projects. Rising investment in walkways, transit terminals, and urban landscaping is lifting demand through 2025. Cities are prioritizing low-maintenance pavements to reduce lifecycle costs, which positions engineered concrete pavers as a strategic material choice. Retaining walls hold a solid portion of overall volume as land development, hillside construction, and flood-management systems rely on reinforced structures for stability.

Other applications include utility corridors, industrial yards, and logistics hubs. These segments benefit from materials that deliver predictable strength and controlled shrinkage. Increased spending on warehousing and distribution networks in North America and Asia contributes to higher demand for heavy-load concrete applications. As supply chains expand and regional manufacturing footprints increase, concrete usage in load-bearing pavements and site-development structures continues to rise.

Manufacturers and contractors are adopting digital mix-design tools and automated monitoring to improve consistency and compliance with regional building codes. This shift helps reduce rework rates and enhances overall project reliability.

End-Use Analysis

Residential buildings account for a meaningful share of global concrete consumption, supported by steady homebuilding activity and public housing programs. Rising urban populations in Asia and Africa continue to widen the need for multi-unit dwellings. Commercial buildings follow closely, driven by steady investment in offices, healthcare facilities, and education infrastructure. Many of these projects require controlled-performance mixes for foundations, slabs, and façade elements.

Industrial buildings are expanding as global manufacturing shifts to more automated production lines and larger distribution centers. These facilities require durable structures capable of supporting heavy machinery and vehicle movement. Demand for high-strength and self-consolidating mixes is increasing due to tighter construction schedules and the need for reliable finishes. By 2030, industrial construction spending is expected to grow at an annual rate above 5 percent, supported by increased investment in energy, automotive, and electronics sectors.

The broader market benefits from modernization of building codes, higher safety expectations, and consistent investment from public and private sectors. Builders are adopting standardized mixes to reduce delays and improve quality verification.

Regional Analysis

North America maintains a strong position in the concrete materials market, supported by stable construction spending and federal investment in transport and utilities. The United States is expected to remain a core consumption base through 2030 due to ongoing projects in bridges, highways, and renewable energy infrastructure. Canada’s urban development programs also contribute to sustained regional demand. Material suppliers with broad distribution networks and certified batching facilities hold a competitive edge in procurement cycles.

Europe shows steady activity, driven by renovation programs and low-carbon building requirements. The region continues to emphasize materials with lower embodied emissions, which encourages use of advanced concrete mixes. Germany, France, and the United Kingdom remain central markets as public infrastructure budgets expand and commercial developers prioritize energy-efficient structures.

Asia Pacific is the fastest-growing region, supported by rapid urbanization, industrial expansion, and strong public infrastructure pipelines in China, India, Indonesia, and Vietnam. Large-scale rail, airport, and housing projects are increasing the need for high-volume concrete supply. Latin America and the Middle East & Africa show gradual improvement, backed by selective investment in transport corridors, industrial parks, and urban development programs. Growth rates in these regions remain tied to economic conditions and public-sector funding stability.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Service

- Contract Manufacturing

- Accessories Manufacturing

- Assembly Manufacturing

- Component Manufacturing

- Device Manufacturing

- Quality Assurance

- Design and Development Services

- Machining

- Molding

- Designing & Engineering

- Packaging

- Maintenance Services

- Regulatory Affairs Services

- Clinical Trials Applications And Product Registrations

- Regulatory Writing And Publishing

- Legal Representation

- Others

By Application

- Cardiology

- General and Plastic Surgery

- Diagnostic Imaging

- Drug Delivery

- IVD

- Others

By Class

- Class I

- Class II

- Class III

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 156.8 billion |

| Forecast Revenue (2034) | USD 512.6 billion |

| CAGR (2025-2034) | 13.1% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Service (Contract Manufacturing, Accessories Manufacturing, Assembly Manufacturing, Component Manufacturing, Device Manufacturing, Quality Assurance, Design and Development Services, Machining, Molding, Designing & Engineering, Packaging, Maintenance Services, Regulatory Affairs Services, Clinical Trials Applications And Product Registrations, Regulatory Writing And Publishing, Legal Representation, Others), By Application (Cardiology, General and Plastic Surgery, Diagnostic Imaging, Drug Delivery, IVD, Others), By Class (Class I, Class II, Class III) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Mandala International, SGS SA, North American Science Associates, LLC, Euro fins Scientific, Pace Analytical Services, Inc, Freyr, Laboratory Corporation of America Holdings, Intertek Group plc, PAREXEL International Corporation, Global Regulatory Partners, WuXiAppTec, Medical Device Testing Services, Charles River Laboratories |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Cardiology, Diagnostic Imaging, Drug Delivery, IVD, Surgical Devices), By Class (Class I, Class II, Class III), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By Application (Cardiology, Diagnostic Imaging, Drug Delivery, IVD, Surgical Devices), By Class (Class I, Class II, Class III), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By Application (Cardiology, Diagnostic Imaging, Drug Delivery, IVD, Surgical Devices), By Class (Class I, Class II, Class III), By Region & Key Players – Industry Overview, Market Dynamics, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Medical Device Outsourcing Market?

The Medical Device Outsourcing Market is projected to grow from US$ 156.8 billion in 2025 to US$ 512.6 billion by 2034, expanding at a CAGR of 13.1% during 2026–2034, driven by rising demand for contract manufacturing, regulatory expertise, and faster medical device innovation.

Who are the major players in the Medical Device Outsourcing Market?

Mandala International, SGS SA, North American Science Associates, LLC, Euro fins Scientific, Pace Analytical Services, Inc, Freyr, Laboratory Corporation of America Holdings, Intertek Group plc, PAREXEL International Corporation, Global Regulatory Partners, WuXiAppTec, Medical Device Testing Services, Charles River Laboratories

Which segments covered the Medical Device Outsourcing Market?

By Service (Contract Manufacturing, Accessories Manufacturing, Assembly Manufacturing, Component Manufacturing, Device Manufacturing, Quality Assurance, Design and Development Services, Machining, Molding, Designing & Engineering, Packaging, Maintenance Services, Regulatory Affairs Services, Clinical Trials Applications And Product Registrations, Regulatory Writing And Publishing, Legal Representation, Others), By Application (Cardiology, General and Plastic Surgery, Diagnostic Imaging, Drug Delivery, IVD, Others), By Class (Class I, Class II, Class III)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Medical Device Outsourcing Market

Published Date : 31 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date