- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Methane Detection Market Size & Forecast 2034 | CAGR 9.9%

Global Methane Detection and Monitoring Market Size, Share, Growth & Industry Analysis By Technology (Optical Gas Imaging Systems, Laser-Based Detection Systems, Electrochemical & Semiconductor Sensors, Satellite & Aerial Monitoring, Other Technologies), By End-User (Oil & Gas, Waste Management & Landfills, Coal Mining, Agriculture & Livestock, Industrial Manufacturing), By Deployment (Fixed, Portable, Mobile, Aerial), By Component (Hardware, Software, Services) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

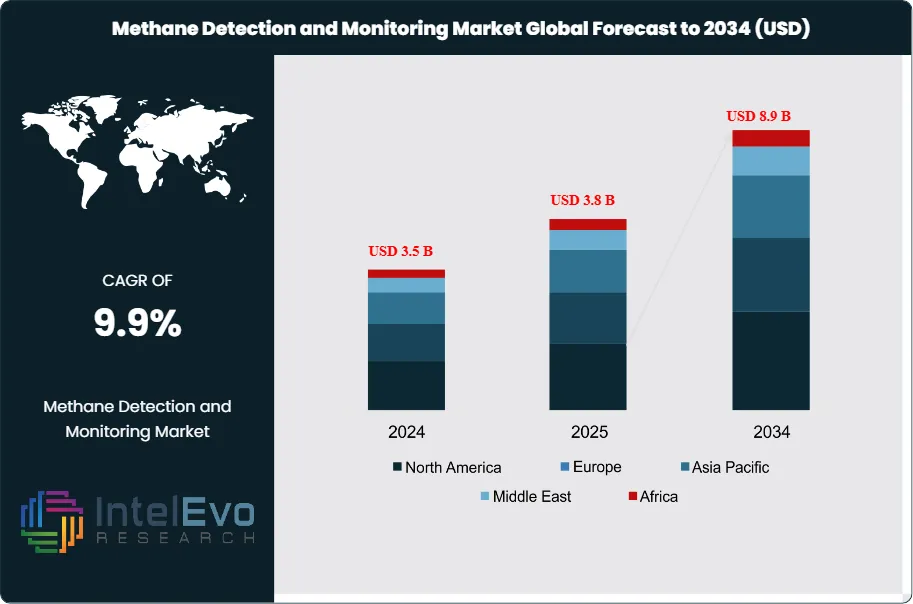

| USD 3.8 Billion | USD 8.9 Billion | 9.9% | North America, 38.4% |

The Methane Detection and Monitoring Market was valued at approximately USD 3.5 Billion in 2024 and reached USD 3.8 Billion in 2025. The market is projected to grow to USD 8.9 Billion by 2034, expanding at a CAGR of 9.9% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 5.1 Billion over the analysis period. Methane detection and monitoring systems encompass sensors, analyzers, cameras, and software platforms that identify, quantify, and track methane emissions across oil and gas operations, landfills, agriculture, and industrial facilities.

Get More Information about this report -

Request Free Sample ReportMarket expansion is driven by tightening emissions regulations, corporate net-zero commitments, and growing investor pressure on ESG compliance. The US EPA Methane Rules finalized in 2024 require oil and gas operators to conduct quarterly monitoring and achieve 98% capture efficiency. The EU Methane Regulation mandates leak detection and repair programs with penalty rates reaching EUR 100 per tonne of methane released. The International Energy Agency estimates that eliminating oil and gas methane emissions could deliver 15% of the emissions reductions needed to limit global warming to 1.5 degrees Celsius.

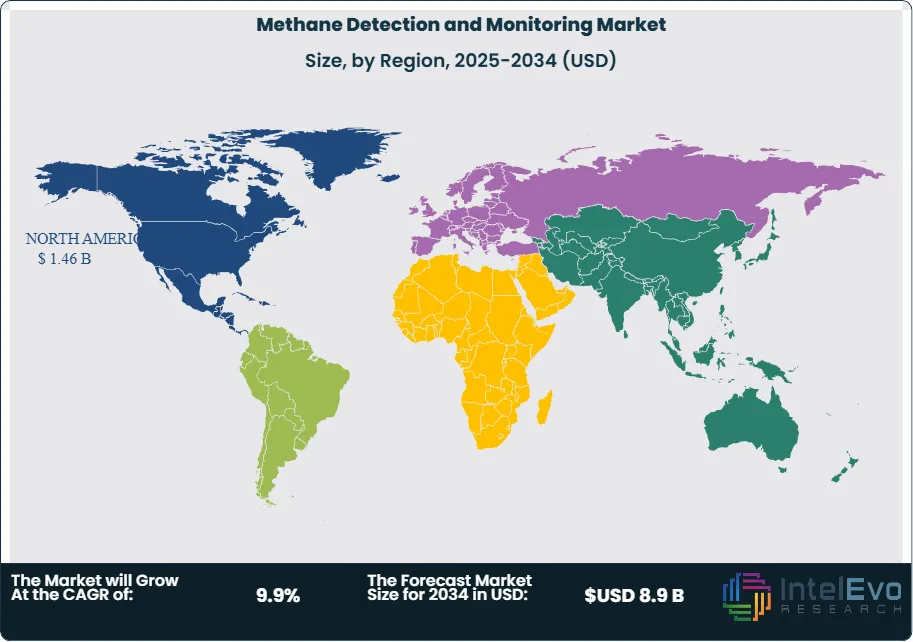

North America leads the methane detection and monitoring market with 38.4% revenue share in 2025, valued at USD 1.46 Billion. The Permian Basin, Marcellus Shale, and Bakken Formation represent primary deployment zones. Europe follows with 24.2% share as OGMP 2.0 reporting requirements drive adoption among operators. Asia Pacific captures 18.9% driven by coal mine safety regulations in China and expanding LNG infrastructure across the region.

Technology advancement is accelerating across the industry. Satellite-based detection from operators like GHGSat, Kayrros, and MethaneSAT now provides basin-level and facility-level emission quantification. Optical gas imaging cameras enable rapid leak surveys at production sites. Continuous monitoring systems integrate with SCADA platforms for real-time alerting. AI-enabled analytics are improving source attribution and emission quantification accuracy by 35-50% compared to manual methods. The convergence of ground-based sensors, aerial surveys, and satellite data creates comprehensive monitoring networks that satisfy regulatory reporting requirements while supporting operational efficiency improvements.

, By End-User (Oil & Gas, Waste Management & Landfills, Coal Mining, Agriculture & Livestock, Industrial Manufacturing), By Deployment (Fixed, Portable, Mobile, Aerial), By Component (Hardware, Software, Services) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The methane detection and monitoring market is projected to expand from USD 3.8 Billion in 2025 to USD 8.9 Billion by 2034, registering a CAGR of 9.9% during 2025-2034.

- Segment Dominance (By Technology): Optical gas imaging systems command 34.2% market share in 2025, valued at USD 1.30 Billion, due to regulatory acceptance and rapid leak detection capabilities.

- Segment Dominance (By End-User): Oil and gas operations represent 58.4% of market demand in 2025 at USD 2.22 Billion, driven by EPA and EU regulatory compliance requirements.

- Driver: Regulatory mandates are accelerating adoption. Over 50 countries have implemented or announced methane reduction targets, with penalty rates reaching USD 1,500 per tonne under US EPA Super-Emitter provisions.

- Restraint: High equipment costs and technical complexity limit adoption among smaller operators. Average continuous monitoring system costs range from USD 50,000 to USD 250,000 per installation.

- Opportunity: Satellite-based monitoring services present a USD 1.2 Billion addressable market by 2034, enabling cost-effective wide-area surveillance for operators and regulators.

- Trend: Continuous monitoring systems are being adopted by 42% of large operators in 2025, replacing periodic survey approaches with real-time emission tracking.

- Regional Analysis: North America leads the global market with 38.4% share and USD 1.46 Billion revenue in 2025, supported by EPA methane regulations and state-level requirements.

Competitive Landscape Overview

The methane detection and monitoring market exhibits moderate fragmentation, with the top four players capturing approximately 48% combined market share in 2025. ABB Ltd leads through its integrated monitoring platform, followed by Honeywell International, Emerson Electric, and Siemens AG. Competition centers on technology differentiation, with suppliers emphasizing detection sensitivity, quantification accuracy, and software integration. Recent strategic activity has intensified, including four acquisitions exceeding USD 100 million and multiple partnerships between hardware providers and satellite operators.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| ABB LTD | Switzerland | Leader | ABB Ability Methane Platform | Global | Launched satellite integration module (Feb 2025) |

| HONEYWELL INTERNATIONAL | US | Leader | Gas Cloud Imaging System | North America | Acquired sensing tech firm USD 420M (Dec 2024) |

| EMERSON ELECTRIC | US | Leader | Rosemount CT5400 | North America | Expanded cloud analytics suite (Mar 2025) |

| SIEMENS AG | Germany | Challenger | Sitrans SL Laser Analyzer | Europe | Partnership with GHGSat (Jan 2025) |

| TELEDYNE FLIR | US | Challenger | FLIR GF Series Cameras | North America | New compact OGI camera launch (Jun 2025) |

| SENSIRION AG | Switzerland | Niche Player | SCD4x Sensors | Europe | IoT platform integration (Sep 2025) |

| AEROQUAL LTD | New Zealand | Niche Player | AQM 65 Monitor | Asia Pacific | Expanded distributor network (Nov 2025) |

| QUBE TECHNOLOGIES | Canada | Niche Player | Qube Methane Monitor | North America | Series C funding USD 45M (Jan 2026) |

By Technology

The methane detection and monitoring market segmentation by technology reveals optical gas imaging systems as the dominant category with 34.2% share valued at USD 1.30 Billion in 2025. These systems utilize infrared cameras to visualize methane plumes, enabling rapid leak identification during field surveys. FLIR, Opgal, and Infrared Cameras Inc. lead this segment. Laser-based detection systems hold 28.6% market share at USD 1.09 Billion, utilizing tunable diode laser absorption spectroscopy for precise concentration measurement. These systems serve both portable survey applications and fixed continuous monitoring installations. Electrochemical and semiconductor sensors account for 18.4% share at USD 699 million, providing cost-effective solutions for point detection applications in industrial facilities and underground mines. Satellite and aerial monitoring services comprise 12.3% at USD 467 million, delivering wide-area surveillance capabilities through platforms like GHGSat, MethaneSAT, and airborne lidar systems. Other technologies including acoustic sensors and flame ionization detectors represent the remaining 6.5% at USD 247 million.

By End-User

End-user segmentation of the methane detection and monitoring market positions oil and gas operations as the largest segment with 58.4% share worth USD 2.22 Billion in 2025. Upstream production facilities, midstream pipeline networks, and downstream refineries all require monitoring to meet regulatory compliance. EPA and EU regulations drive mandatory quarterly surveys at US facilities and annual reporting under OGMP 2.0 in Europe. Waste management and landfill operations represent 18.2% share at USD 692 million, addressing methane capture requirements and emissions reporting under Clean Air Act provisions. Coal mining operations account for 12.8% at USD 486 million, with continuous monitoring systems addressing underground safety requirements and ventilation air methane abatement. Agriculture and livestock operations comprise 6.4% at USD 243 million, targeting enteric fermentation and manure management emissions as sustainability reporting expands. Industrial manufacturing facilities represent the remaining 4.2% at USD 160 million, addressing process emissions from chemical plants and steel production.

By Deployment

Deployment-based analysis shows fixed continuous monitoring systems commanding 42.1% of the methane detection and monitoring market in 2025, valued at USD 1.60 Billion. These installations provide real-time emission data through networked sensor arrays integrated with facility control systems. Regulatory trends favor continuous monitoring over periodic surveys, driving adoption growth at 12.5% CAGR through 2034. Portable and handheld detection equipment accounts for 31.8% share at USD 1.21 Billion, serving field survey applications and leak investigation activities. These tools remain essential for pinpointing emission sources identified by area monitors. Mobile and vehicle-mounted systems represent 14.6% at USD 555 million, enabling rapid surveys of pipeline rights-of-way and large production areas. Aerial and satellite-based services comprise 11.5% at USD 437 million, providing basin-level surveillance and third-party verification of operator-reported emissions.

By Component

Component-based segmentation of the methane detection and monitoring market reveals hardware comprising 56.2% of market revenue at USD 2.14 Billion in 2025. This includes sensors, analyzers, cameras, and communication equipment required for detection systems. Software and analytics platforms account for 26.4% at USD 1.00 Billion, providing data management, visualization, and reporting capabilities. Cloud-based platforms are gaining share as operators consolidate monitoring data across multiple facilities. Services including installation, calibration, maintenance, and third-party monitoring comprise 17.4% at USD 661 million. Managed monitoring services are emerging as smaller operators seek to outsource compliance activities.

Regional Analysis

North America

North America commands 38.4% of the global methane detection and monitoring market with USD 1.46 Billion revenue in 2025. The United States dominates regional consumption at 86% share, driven by EPA Methane Rules requiring quarterly monitoring at oil and gas facilities and Super-Emitter Response Program provisions imposing penalties up to USD 1,500 per tonne for large releases. The Permian Basin alone operates over 250,000 active wells requiring monitoring coverage. Texas, New Mexico, and Colorado have implemented state-level requirements exceeding federal standards. Canada contributes 11% of regional demand, with Alberta Energy Regulator directives targeting 45% methane reduction from 2012 levels by 2025. British Columbia and Saskatchewan maintain similar programs. Mexico accounts for 3% as Pemex implements monitoring at onshore and offshore facilities. Technology adoption in North America exceeds other regions, with 52% of large operators deploying continuous monitoring systems in 2025.

Europe

Europe represents 24.2% of the methane detection and monitoring market with USD 920 million in 2025. The EU Methane Regulation adopted in 2024 establishes mandatory monitoring and reporting requirements for all oil and gas operations, creating sustained demand through 2034. The United Kingdom leads regional adoption at 28% share, driven by North Sea Transition Authority requirements and Climate Change Committee recommendations. Germany follows at 22%, with upstream operators and downstream distribution networks implementing monitoring programs. Norway contributes 18% through Equinor and other North Sea operators maintaining industry-leading monitoring practices. The Netherlands accounts for 14% via NAM and other operators addressing Groningen field emissions. OGMP 2.0 voluntary reporting framework has secured participation from operators representing 60% of European production, establishing measurement-based reporting standards. The European Chemicals Agency REACH regulations support sensor technology development and certification.

Asia Pacific

Asia Pacific captures 18.9% of the methane detection and monitoring market with USD 718 million in 2025 and represents the fastest-growing region at 12.4% CAGR through 2034. China leads at 44% regional share, driven by coal mine safety regulations requiring continuous monitoring of underground methane concentrations and State Administration of Work Safety requirements. PetroChina, Sinopec, and CNOOC are implementing monitoring across upstream operations. India follows at 18%, with ONGC and Oil India Limited addressing Ministry of Petroleum directives on emission reduction. Australia contributes 16% through coal seam gas operations in Queensland and conventional production in Western Australia, with National Greenhouse and Energy Reporting Scheme requirements. Japan accounts for 12% via LNG import terminal monitoring and INPEX domestic production. Southeast Asian operators in Indonesia, Malaysia, and Thailand collectively represent 10% as offshore production expands.

Middle East and Africa

The Middle East and Africa region holds 12.1% of the methane detection and monitoring market with USD 460 million in 2025. Saudi Arabia leads at 35% regional share, with Saudi Aramco deploying comprehensive monitoring networks across Ghawar, Shaybah, and offshore fields to support net-zero 2050 commitments. The UAE follows at 28%, with ADNOC implementing monitoring programs aligned with Abu Dhabi Economic Vision 2030 sustainability targets. Qatar contributes 18% through QatarEnergy programs at North Field LNG expansion and domestic gas networks. Nigeria accounts for 12% as Shell, TotalEnergies, and NNPC address flaring and fugitive emissions in the Niger Delta. The region benefits from national oil company investment capacity and pressure from international oil company partners to meet global sustainability standards.

Latin America

Latin America accounts for 6.4% of the methane detection and monitoring market with USD 243 million in 2025. Brazil dominates at 52% regional share, with Petrobras pre-salt operations incorporating monitoring systems in field design. The company has committed to 55% methane intensity reduction by 2030. Mexico represents 26% as Pemex rehabilitation programs address legacy infrastructure emissions. Argentina contributes 14% through Vaca Muerta shale development, where YPF and international operators deploy monitoring equipment at new production facilities. Colombia accounts for 8% via Ecopetrol programs at Llanos Basin operations. Regional growth is supported by World Bank Global Gas Flaring Reduction Partnership commitments and pressure from international financing institutions requiring emissions monitoring as condition of project funding.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technology

- Optical Gas Imaging Systems

- Laser-Based Detection Systems

- Electrochemical and Semiconductor Sensors

- Satellite and Aerial Monitoring

- Other Technologies

By End-User

- Oil and Gas Operations

- Waste Management and Landfills

- Coal Mining Operations

- Agriculture and Livestock

- Industrial Manufacturing

By Deployment

- Fixed Continuous Monitoring

- Portable and Handheld

- Mobile and Vehicle-Mounted

- Aerial and Satellite-Based

By Component

- Hardware

- Software and Analytics

- Services

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 3.8 B |

| Forecast Revenue (2034) | USD 8.9 B |

| CAGR (2025-2034) | 9.9% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (Optical Gas Imaging Systems, Laser-Based Detection Systems, Electrochemical and Semiconductor Sensors, Satellite and Aerial Monitoring, Other Technologies), By End-User, (Oil and Gas Operations, Waste Management and Landfills, Coal Mining Operations, Agriculture and Livestock, Industrial Manufacturing), By Deployment, (Fixed Continuous Monitoring, Portable and Handheld, Mobile and Vehicle-Mounted, Aerial and Satellite-Based), By Component, (Hardware, Software and Analytics, Services) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | ABB LTD, HONEYWELL INTERNATIONAL INC., EMERSON ELECTRIC CO., SIEMENS AG, TELEDYNE FLIR LLC, SENSIRION AG, AEROQUAL LTD, QUBE TECHNOLOGIES INC., GHGSAT INC., KAYRROS SAS, OPGAL OPTRONIC INDUSTRIES LTD, BRIDGER PHOTONICS INC., PICARRO INC., LOS GATOS RESEARCH (ABB), HEATH CONSULTANTS INC., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By End-User (Oil & Gas, Waste Management & Landfills, Coal Mining, Agriculture & Livestock, Industrial Manufacturing), By Deployment (Fixed, Portable, Mobile, Aerial), By Component (Hardware, Software, Services) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By End-User (Oil & Gas, Waste Management & Landfills, Coal Mining, Agriculture & Livestock, Industrial Manufacturing), By Deployment (Fixed, Portable, Mobile, Aerial), By Component (Hardware, Software, Services) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By End-User (Oil & Gas, Waste Management & Landfills, Coal Mining, Agriculture & Livestock, Industrial Manufacturing), By Deployment (Fixed, Portable, Mobile, Aerial), By Component (Hardware, Software, Services) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Methane Detection and Monitoring Market?

Global methane detection and monitoring market valued at USD 3.5B in 2024, reaching USD 8.9B by 2034, growing at a CAGR of 9.9% from 2026–2034.

Who are the major players in the Methane Detection and Monitoring Market?

ABB LTD, HONEYWELL INTERNATIONAL INC., EMERSON ELECTRIC CO., SIEMENS AG, TELEDYNE FLIR LLC, SENSIRION AG, AEROQUAL LTD, QUBE TECHNOLOGIES INC., GHGSAT INC., KAYRROS SAS, OPGAL OPTRONIC INDUSTRIES LTD, BRIDGER PHOTONICS INC., PICARRO INC., LOS GATOS RESEARCH (ABB), HEATH CONSULTANTS INC., Others

Which segments covered the Methane Detection and Monitoring Market?

By Technology, (Optical Gas Imaging Systems, Laser-Based Detection Systems, Electrochemical and Semiconductor Sensors, Satellite and Aerial Monitoring, Other Technologies), By End-User, (Oil and Gas Operations, Waste Management and Landfills, Coal Mining Operations, Agriculture and Livestock, Industrial Manufacturing), By Deployment, (Fixed Continuous Monitoring, Portable and Handheld, Mobile and Vehicle-Mounted, Aerial and Satellite-Based), By Component, (Hardware, Software and Analytics, Services)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Methane Detection and Monitoring Market

Published Date : 27 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date