- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Micro Investing App Market Size, Growth Forecast | 23.5% CAGR

Global Micro Investing App Market Size, Share & Analysis By Type (Android, iOS), By Deployment (Cloud-based, On-premises), By End-User (Business, Individual), By User Demographics, FinTech Adoption Trends, Monetization Models, Competitive Landscape & Forecast 2025–2034

Report Overview

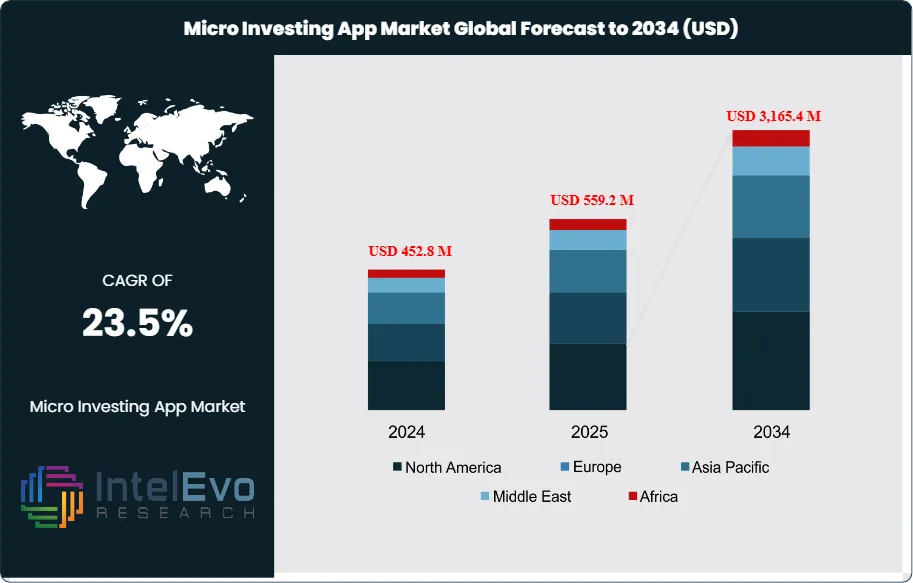

The Micro Investing App Market size is expected to be worth around USD USD 3,165.4 million by 2034, from 452.8 million in 2024, growing at a CAGR of 23.5% during the forecast period from 2025 to 2034. Market has grown quickly due to increased digital financial access, automated wealth-building tools, and the rise of fractional investing among new investors. The upcoming decade will be influenced by greater smartphone use, the onboarding of Gen-Z, partnerships in embedded finance, and updated regulations that improve access to digital investment products globally.

Get More Information about this report -

Request Free Sample ReportMicro investing platforms provide various product options that make wealth creation more accessible by allowing users to invest small amounts, sometimes starting from just USD 1. The product lineup includes fractional share investing, round-up investment tools, robo-advisory micro-portfolios, thematic baskets, index-linked micro funds, automated recurring investment plans, and micro-savings with investment-linked rewards. Many apps are also adding crypto micro investing, ESG-focused micro portfolios, and personalized asset allocation driven by AI. These features appeal particularly to new investors, younger users, and those looking for low-risk, automated ways to build long-term wealth.

The market's growth mainly results from a shift towards digital wealth-building habits among millennials and Gen-Z, who prefer automation, gamified investing, and low-commitment financial tools. Financial education programs, simple user interfaces, and AI-powered risk scoring are helping to boost adoption. However, challenges remain, such as fragmented regulations, differing KYC/AML requirements, and worries about data privacy and cybersecurity risks. Monetization challenges, like low revenue per user and high costs for attracting customers, also impact platform profitability. Despite these hurdles, the market has many opportunities, especially in emerging economies where fintech adoption is speeding up. Partnerships between neobanks, payment apps, and micro-investing platforms are broadening access. Trends like AI-guided investing, social investing communities, and micro-alternatives such as real estate, commodities, and bonds are changing how companies compete.

The COVID-19 pandemic significantly sped up the adoption of micro-investing. It drove more retail participation, raised financial awareness, and spurred interest in digital savings and investment combinations. Lockdowns and economic uncertainty led millions to consider long-term wealth planning, benefiting low-entry digital platforms. On the other hand, the post-pandemic period brought challenges, including reduced disposable income in some areas and increased caution among investors. Moreover, global geopolitical tensions and trade issues, especially involving major tech economies, have affected data storage regulations, cross-border fintech partnerships, and API-based brokerage integrations. These factors have pushed platforms to enhance compliance, diversify their brokerage back-ends, and adopt data-localization strategies to ensure consistent service.

In summary, the Micro Investing App Market is moving from an early-adoption phase toward a scalable financial ecosystem powered by automation, AI, and embedded finance. With growing consumer confidence, faster fintech digitization, and clearer regulations, the market is set for strong growth through 2034.

, By Deployment (Cloud-based, On-premises), By End-User (Business, Individual), By User Demographics, FinTech Adoption Trends, Monetization Models, Competitive Landscape & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Micro Investing App market is projected to scale from USD 452.8 million in 2024 to USD 3,165.4 million by 2034, at a 23.5% CAGR (2025–2034), propelled by fractional investing, round-ups, zero-commission trading, and rising financial-wellness adoption among first-time investors.

- Platform (OS): Android led with ~62% share in 2024, outperforming iOS due to its larger installed base in price-sensitive, emerging markets and lower acquisition costs per user; iOS retained a premium ARPU niche (~38%).

- End User: Individual investors accounted for >70% of revenues in 2024, reflecting strong uptake of automated “spare-change” and paycheck auto-invest features; institutional/SMB use remains nascent but is expanding via white-label and embedded-finance partnerships.

- Driver: Cloud-native deployment underpins scalability and speed-to-market, with >75% of platforms delivered via the cloud in 2024; open-banking rails and instant payments compress onboarding from days to minutes, while mobile-first behavior (millennials are ~43% more likely to invest via smartphone) accelerates conversion.

- Restraint: Profitability is pressured by customer-acquisition cost inflation (~15–20% YoY in mature markets) and elevated early-life churn, alongside tightening rules on gamification, disclosures, and data privacy (KYC/AML, cross-border data) that raise compliance overhead.

- Opportunity: Asia–Pacific is the standout expansion vector, expected to deliver ~40% of absolute growth (≈USD 850–900 million) through 2034 on the back of smartphone penetration and underbanked segments; localized products (multi-currency wallets, small-lot treasuries/ETFs) in India, Indonesia, and the Philippines are poised for outsized uptake (>25% CAGR).

- Trend: Convergence of AI-driven robo-advice and behavioral nudging is lifting engagement and retention; global digital-advice AUM is on track to exceed USD ~5.1 trillion by 2027, reinforcing the funnel for micro-ticket portfolios and goal-based, automated investing.

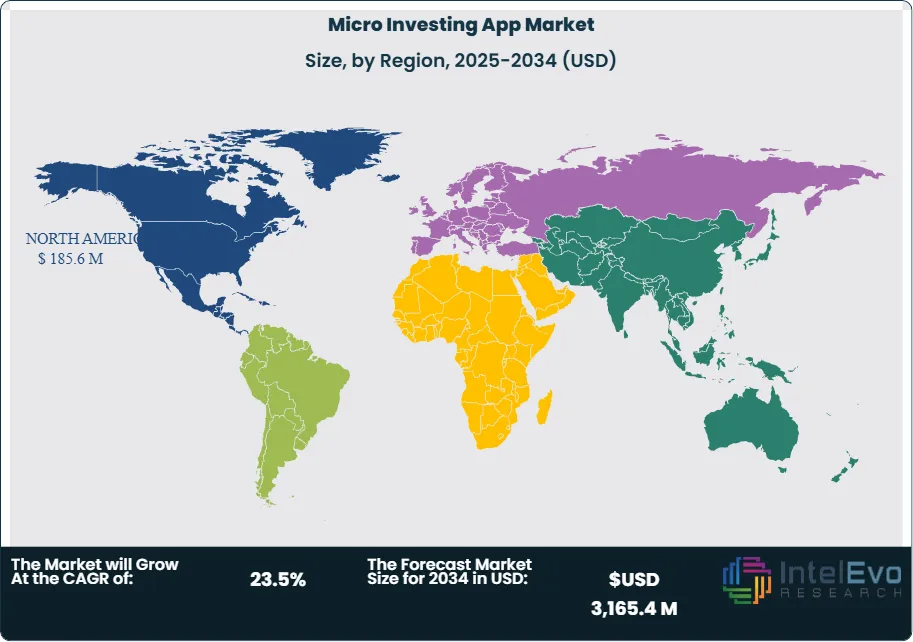

- Regional Analysis: North America remained the largest market in 2024 with >40% share, supported by mature brokerage infrastructure and high fintech adoption; Western Europe follows (≈25–27%) aided by PSD2/open-banking integration, while Asia–Pacific posts the fastest growth (>25% CAGR). Latin America and Middle East & Africa are earlier-stage (<10% share each) but are benefiting from real-time payments and telco-fintech ecosystems.

Type Analysis

Android remains the scale platform for micro-investing in 2025, accounting for an estimated 61–63% of active users and ~58–60% of segment revenue. Its open ecosystem, broad OEM footprint, and affordability underpin penetration in price-sensitive markets, while native integrations with local rails (e.g., UPI in India, Pix in Brazil, DuitNow in Malaysia) and multi-language UI support lower onboarding friction and unit costs. iOS, by contrast, captures a smaller user base (~37–39%) but materially higher monetization—ARPU is typically 1.3–1.6× Android—driven by greater paid-tier uptake, higher average balances, and seamless funding via Apple Pay. Compliance and security features (biometrics, on-device encryption) also translate into superior funding conversion and retention. Looking to 2030, Android users are projected to grow at ~19–21% CAGR on emerging-market expansion, while iOS revenue is set to compound faster (~22–24% CAGR) as premium advisory bundles, tax tools, and high-yield cash features scale.

Deployment Analysis

Cloud-based deployment is the industry default in 2025, representing ~77–79% of revenue and >85% of new builds. Vendors prioritize elastic compute for intraday rebalancing, real-time risk, and AML analytics, while managed services compress release cycles from weeks to days. Enterprise-grade controls (SOC 2/ISO 27001), zero-trust access, HSM-backed key management, and continuous patching have narrowed historic security objections. On-premises persists mainly with Tier-1 financial institutions in markets with strict data-residency mandates, sovereign-cloud preferences, or latency-sensitive brokerage stacks; this cohort is expected to decline to ~15% share by 2030 as confidential computing, bring-your-own-key (BYOK), and regionalized data zones in public clouds meet regulatory thresholds. Hybrid patterns—cloud analytics plus on-prem transaction ledgers—are gaining adoption in Europe and parts of APAC.

End-User Analysis

Individual consumers remain the core demand engine, contributing ~72–74% of 2025 revenue and >80% of net-new accounts. Adoption is propelled by round-ups, paycheck auto-invest, and fractionalization that enable <$10 entry points; platforms report first-90-day funding conversion in the 35–45% range where instant payments are supported. Younger cohorts (Gen Z/young millennials) exhibit the highest growth, but multi-generational uptake is rising as apps bundle goal-based portfolios, micro-treasuries/ETFs, and education modules. The Business segment (26–28% revenue) is expanding faster (~24–26% CAGR through 2030) via embedded finance: employers offering opt-in micro-investing alongside earned-wage access, neobanks and telcos white-labeling robo-advice, and payroll providers enabling default contribution nudges. These channels deliver structurally lower CAC and higher persistence than direct-to-consumer models.

Regional Analysis

North America remains the largest market in 2025 with ~39–41% revenue share, underpinned by zero-commission trading, deep brokerage liquidity, and strong fintech adoption; leading players (e.g., Acorns, Stash, Robinhood) are layering high-yield cash, tax-loss harvesting, and retirement micro-plans to expand wallet share. Europe holds ~24–26%, supported by PSD2/open-banking connectivity, maturing robo-advisors, and rising interest in low-denomination government bond products; regulatory scrutiny of gamification is shaping UX design but also elevating trust.

Asia Pacific is the fastest-growing corridor (CAGR >25%), with share projected to approach 30–32% by 2030. India, Indonesia, and the Philippines are investment hotspots where smartphone penetration, instant-payment networks, and underbanked populations drive step-change adoption; local champions (e.g., Groww-style models, Raiz in ANZ/SEA) tailor micro-lots and vernacular support to accelerate conversion.

Latin America (~6–8%) benefits from real-time rails (Pix in Brazil, CoDi in Mexico) and rising retail participation, while the Middle East & Africa (~5–6%) see momentum in GCC sandboxes (UAE, Saudi Arabia) and mobile-money ecosystems (Kenya, Nigeria). Across emerging regions, partnerships with banks, telcos, and payroll providers are the fastest route to scale, compressing CAC and improving lifetime value.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- Android

- iOS

By Deployment

- Cloud-based

- On-premises

By End-User

- Business

- Individual

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2024) | USD 452.8 M |

| Forecast Revenue (2034) | USD 3,165.4 M |

| CAGR (2024-2034) | 23.5% |

| Historical data | 2020-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type (Android, iOS), By Deployment (Cloud-based, On-premises), By End-User (Business, Individual) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Stash, Acorns, Betterment, Greenlight, Moneyfarm, Wealthify, SoFi, Bamboo, M1, Robinhood, Wealthsimple, Nutmeg, Moneybox, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Deployment (Cloud-based, On-premises), By End-User (Business, Individual), By User Demographics, FinTech Adoption Trends, Monetization Models, Competitive Landscape & Forecast 2025–2034")

, By Deployment (Cloud-based, On-premises), By End-User (Business, Individual), By User Demographics, FinTech Adoption Trends, Monetization Models, Competitive Landscape & Forecast 2025–2034")

, By Deployment (Cloud-based, On-premises), By End-User (Business, Individual), By User Demographics, FinTech Adoption Trends, Monetization Models, Competitive Landscape & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date