- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Microcarriers Market Size, Share, Growth & Forecast 2034 | 9.8% CAGR

Global Microcarriers Market Size, Share & Analysis By Type (Dextran, Collagen, Synthetic), By Application (Cell Therapy, Vaccine Production), By End-User Industry Regions & Key Players – Bioprocessing Trends & Forecast 2025–2034

Report Overview:

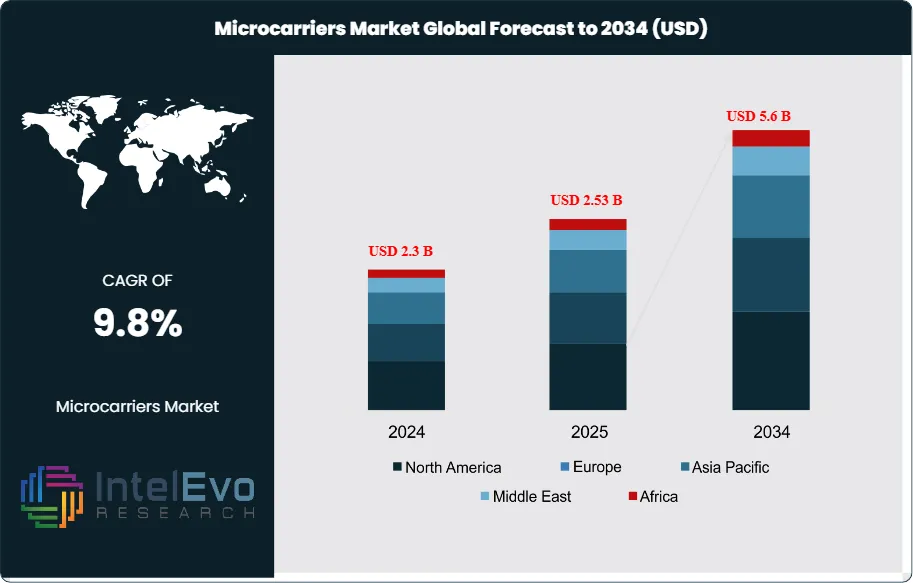

The Global Microcarriers Market size is expected to be worth around USD 5.6 billion by 2034, up from USD 2.3 billion in 2024, growing at a CAGR of 9.8% during the forecast period from 2025 to 2034. The market growth is driven by the increasing demand for cell-based vaccines, regenerative medicines, and biopharmaceutical production, which rely heavily on scalable cell culture systems. The growing adoption of single-use bioreactors, advancements in stem cell therapy, and expanding biomanufacturing infrastructure are further fueling market expansion. With strong investments in biotechnology and cell therapy research, the microcarriers market is set to witness substantial innovation and global growth over the coming decade.

Get More Information about this report -

Request Free Sample ReportMicrocarriers are small, spherical particles—typically ranging from 100 to 300 micrometers in diameter—used as a surface for the attachment and growth of anchorage-dependent cells in suspension cultures. Made from materials such as dextran, collagen, gelatin, or synthetic polymers, microcarriers provide a large surface area within a relatively small volume, allowing high-density cell culture in bioreactors. They are commonly used in biotechnology, vaccine production, and regenerative medicine to scale up cell cultivation processes efficiently.

The expansion of the microcarriers market is largely driven by the rising demand for cell-based vaccines and therapies, alongside the growing prevalence of chronic and autoimmune diseases such as cancer, diabetes, hemophilia, and rheumatoid arthritis. Substantial investments in cutting-edge therapeutic development and ongoing innovations in cell biology are further supporting this growth. For example, in May 2024, Sartorius entered into a collaboration with Sanofi to co-develop a platform aimed at streamlining and optimizing downstream bioprocessing workflows. This partnership is expected to boost efficiency in biopharmaceutical production and could pave the way for advancements in microcarrier-based processing technologies.

North America holds a significant position in the global microcarriers market, driven by its advanced biopharmaceutical industry, strong research infrastructure, and increasing focus on regenerative medicine and cell-based therapies. The region benefits from substantial investments in biotechnology and life sciences, particularly in the United States, where government agencies and private players actively support research and development. The growing demand for cell-based vaccines, especially following the COVID-19 pandemic, has also accelerated the adoption of microcarrier technologies for scalable cell culture processes. Moreover, the presence of leading pharmaceutical and biotech companies, coupled with a high prevalence of chronic diseases such as cancer and autoimmune disorders, is fueling the need for innovative therapeutic solutions. These factors, along with continuous technological advancements and collaborations between academic institutions and industry players, are expected to further strengthen North America's role in the expansion of the microcarriers market.

The COVID-19 pandemic had a notable impact on the microcarriers market, accelerating its growth and highlighting its importance in the field of biopharmaceutical manufacturing. As the demand for vaccines and therapeutic biologics surged globally, microcarrier-based cell culture systems gained prominence due to their ability to support large-scale production of anchorage-dependent cells—crucial for vaccine development and biologic therapies. Many pharmaceutical companies and research institutions adopted microcarrier technologies to enhance the efficiency and scalability of their bioprocessing platforms. Additionally, the urgent need for rapid vaccine deployment pushed investment into advanced manufacturing solutions, including single-use bioreactors and microcarrier-compatible systems. This unprecedented demand not only expanded the use of microcarriers during the pandemic but also set the stage for long-term growth, as companies continue to prioritize scalable, high-yield cell culture systems for future pandemics and biologics production.

, By Application (Cell Therapy, Vaccine Production), By End-User Industry Regions & Key Players – Bioprocessing Trends & Forecast 2025–2034")

Key Takeaways:

- Market Growth: The microcarriers market is expected to reach USD 5.6 billion by 2034, growing at a robust CAGR of 9.8%, indicating strong market expansion.

- Product Segment Dominance: The product segment is dominated by consumables, accounting for over 67% of the market share. The consumables segment is expected to witness strong growth, largely due to the expanding use of microcarriers in cell production workflows. As pharmaceutical companies ramp up bioprocessing activities, there's a growing demand for microcarrier beads that enable efficient cell growth by offering a high surface area within bioreactor systems. This trend is accelerating the need for ready-to-use, scalable consumables that support high-density cell culture across various therapeutic applications.

- Application Segment Insights: Biopharmaceuticals is anticipated to hold the largest market share, owing to the increasing development and use of cell-based vaccines are driving a higher demand for microcarriers, as they provide the necessary support for efficient and scalable cell growth during vaccine production.

- Driver: The growing demand for biopharmaceutical products—such as vaccines, monoclonal antibodies, and cell-based therapies—is a major factor fueling the microcarrier market. These therapies rely on cultivating large numbers of adherent cells, which require an efficient and scalable growth surface. Microcarriers offer an effective solution by providing the necessary structure for cells to attach and proliferate in suspension cultures, making them essential for modern biopharmaceutical manufacturing.

- Restraint: The regulatory landscape governing microcarrier-based culture systems in biopharmaceutical manufacturing is continuously evolving. Manufacturers are required to comply with strict guidelines and demonstrate that their processes meet high standards for safety, effectiveness, and consistency. Navigating these complex regulatory pathways, along with ensuring adherence to current good manufacturing practices (cGMP), adds layers of difficulty and cost to both the development and commercialization of microcarrier technologies.

- Opportunity: The rising biomanufacturing capacity, particularly in emerging economies, is playing a key role in boosting the demand for microcarriers. As global production of biopharmaceuticals scales up to meet increasing healthcare needs, there is a growing reliance on efficient cell culture techniques—such as microcarriers—to support high-yield, cost-effective manufacturing processes.

- Trend: To accelerate drug discovery efforts, the pharmaceutical industry is increasingly adopting automation and high-throughput screening methods. This shift is fueling the demand for microcarriers that can seamlessly integrate with automated cell culture platforms, enabling more efficient and scalable research processes.

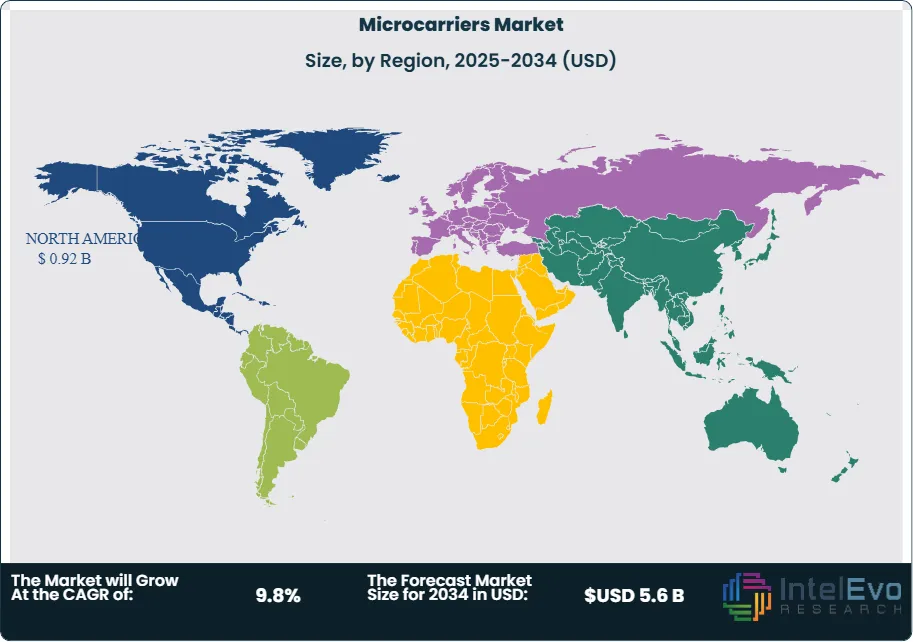

- Regional Analysis: North America holds a leading position in the microcarrier market and is expected to maintain steady growth in the coming years. This dominance is largely driven by the strong presence of major biotechnology and pharmaceutical companies, especially in the United States. These firms extensively use microcarriers in cell culture processes for drug development, vaccine production, and large-scale biomanufacturing, reinforcing the region’s role as a hub for innovation and advanced bioprocessing technologies.

Product Analysis:

Microcarriers market can be categorized by product . These include consumables and equipment. The shift toward single-use systems in bioprocessing has significantly boosted the demand for consumables, as they eliminate the need for time-consuming cleaning and sterilization typically required with reusable equipment. This convenience and efficiency make consumables an attractive option across various applications. Moreover, they offer adaptability in scale-up processes. For example, Sartorius AG provides microcarrier beads available in both animal component-free and animal protein-coated forms, suitable for adherent cell cultures. These beads are widely used in different stages of bioprocessing, contributing to the growing reliance on consumables. This allows bioprocess engineers to efficiently expand operations by simply incorporating additional pre-sterilized microcarriers as needed, streamlining the scale-up process.

Application Analysis:

There are three categories for the application segment: biopharmaceutical production, regenerative medicine, and other applications. Producing biopharmaceuticals such as vaccines and therapeutic treatments often requires cultivating large quantities of cells. Microcarriers help streamline this process by offering an efficient, scalable surface for cell growth, which is crucial for meeting production demands. As more biosimilars gain regulatory approval, there's been a noticeable increase in both manufacturing activity and research aimed at improving production methods. Because microcarriers can easily support the shift from small-scale lab work to large-scale operations, they’ve become an essential tool for companies looking to expand their bioprocessing capabilities.

End-user Analysis:

End-users in the case of the market segmentation of the microcarriers include pharmaceutical & biotechnology companies, CROs & CMOs, academic & research institutes, and cell banks. The growing need for large-scale biopharmaceutical production has made bioprocessing technologies essential, positioning pharmaceutical and biotech companies as key users of microcarriers. As interest in advanced cell-based therapies—such as CAR-T and other immunotherapies—continues to rise, microcarriers are becoming increasingly important for expanding and producing the therapeutic cells required for these cutting-edge treatments. In addition, the ongoing global demand for vaccines, particularly those targeting emerging infectious diseases, is driving further innovation in vaccine production. This, in turn, continues to strengthen the role of microcarriers in modern manufacturing processes.

Region Analysis:

North America Leads With 40% Market Share in the Microcarriers Market: North America plays a leading role in the global microcarriers market, owing to its strong biotechnology and pharmaceutical sectors. North America holds approximately 40% of the market share, owing to the presence of a strong research base in the region. The region is home to major players in cell therapy, vaccine development, and biopharmaceutical manufacturing—all of which rely heavily on efficient cell culture systems. Microcarriers are widely used in these industries to support scalable production, especially for adherent cell lines. Growing investment in regenerative medicine, along with rising approvals of cell-based therapies and biosimilars, has further fueled demand. In addition, the presence of advanced research facilities, supportive regulatory frameworks, and increasing public and private funding make North America a key driver of innovation and growth in the microcarriers market.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Product Type

- Consumables

- Microcarrier Beads

- Media & Reagents

- Equipment

- Bioreactors

- Culture Vessels

- Accessories & Support Equipment

By Material Type

- Polystyrene-Based Microcarriers

- Glass-Based Microcarriers

- Alginate-Based Microcarriers

- Cellulose-Based Microcarriers

- Dextran-Based Microcarriers

- Collagen-Coated & Other Specialty Microcarriers

By Application

- Vaccine Manufacturing

- Cell Therapy & Regenerative Medicine

- Biopharmaceutical Production

- Tissue Engineering

- Research & Development

By End User

- Pharmaceutical & Biotechnology Companies

- Contract Research Organizations (CROs)

- Academic & Research Institutes

- Hospitals & Diagnostic Centers

By Region

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.53 B |

| Forecast Revenue (2034) | USD 5.6 B |

| CAGR (2025-2034) | 9.8% |

| Historical data | 2018-2023 |

| Base Year For Estimation | 2024 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Consumables, (Microcarrier Beads, Media & Reagents), Equipment, (Bioreactors, Culture Vessels, Accessories & Support Equipment)), By Material Type (Polystyrene-Based Microcarriers, Glass-Based Microcarriers, Alginate-Based Microcarriers, Cellulose-Based Microcarriers, Dextran-Based Microcarriers, Collagen-Coated & Other Specialty Microcarriers), By Application (Vaccine Manufacturing, Cell Therapy & Regenerative Medicine, Biopharmaceutical Production, Tissue Engineering, Research & Development), By End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), Academic & Research Institutes, Hospitals & Diagnostic Centers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Corning Incorporated, denovoMATRIX GmbH, Fujiform Holdings Corporation, Merck KGaA, Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., Cytiva (Danaher Corporation), Eppendorf AG, Lonza Group Ltd., Sartorius AG, HiMedia Laboratories Pvt. Ltd., Pall Corporation, Chemglass Life Sciences, MicroVention Inc., Esco Lifesciences Group, Getinge AB, Becton, Dickinson and Company (BD) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Cell Therapy, Vaccine Production), By End-User Industry Regions & Key Players – Bioprocessing Trends & Forecast 2025–2034")

, By Application (Cell Therapy, Vaccine Production), By End-User Industry Regions & Key Players – Bioprocessing Trends & Forecast 2025–2034")

, By Application (Cell Therapy, Vaccine Production), By End-User Industry Regions & Key Players – Bioprocessing Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Microcarriers Market?

Explore insights on the Global Microcarriers Market, projected to reach USD 5.6 billion by 2034 at a 9.8% CAGR. Discover key trends, growth drivers & forecasts.

Who are the major players in the Microcarriers Market?

Corning Incorporated, denovoMATRIX GmbH, Fujiform Holdings Corporation, Merck KGaA, Thermo Fisher Scientific Inc., Bio-Rad Laboratories, Inc., Cytiva (Danaher Corporation), Eppendorf AG, Lonza Group Ltd., Sartorius AG, HiMedia Laboratories Pvt. Ltd., Pall Corporation, Chemglass Life Sciences, MicroVention Inc., Esco Lifesciences Group, Getinge AB, Becton, Dickinson and Company (BD)

Which segments covered the Microcarriers Market?

By Product Type (Consumables, (Microcarrier Beads, Media & Reagents), Equipment, (Bioreactors, Culture Vessels, Accessories & Support Equipment)), By Material Type (Polystyrene-Based Microcarriers, Glass-Based Microcarriers, Alginate-Based Microcarriers, Cellulose-Based Microcarriers, Dextran-Based Microcarriers, Collagen-Coated & Other Specialty Microcarriers), By Application (Vaccine Manufacturing, Cell Therapy & Regenerative Medicine, Biopharmaceutical Production, Tissue Engineering, Research & Development), By End User (Pharmaceutical & Biotechnology Companies, Contract Research Organizations (CROs), Academic & Research Institutes, Hospitals & Diagnostic Centers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date