- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Military Wearable Technology Market Size, Share | CAGR 10.1%

Global Military Wearable Technology Market Size, Share, Analysis By Wearable Type (Smart Helmets, Vests & Body Armor, Wearable Sensors), By Application (Operations, Health Monitoring, Communication & Navigation), By End User (Army, Navy, Air Force), By Core Tech (AI, IoT, Augmented Reality - AR) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Defense Technology Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

|---|---|---|---|

| USD 5.20 Billion | USD 12.40 Billion | 10.1% | North America, 42.5% |

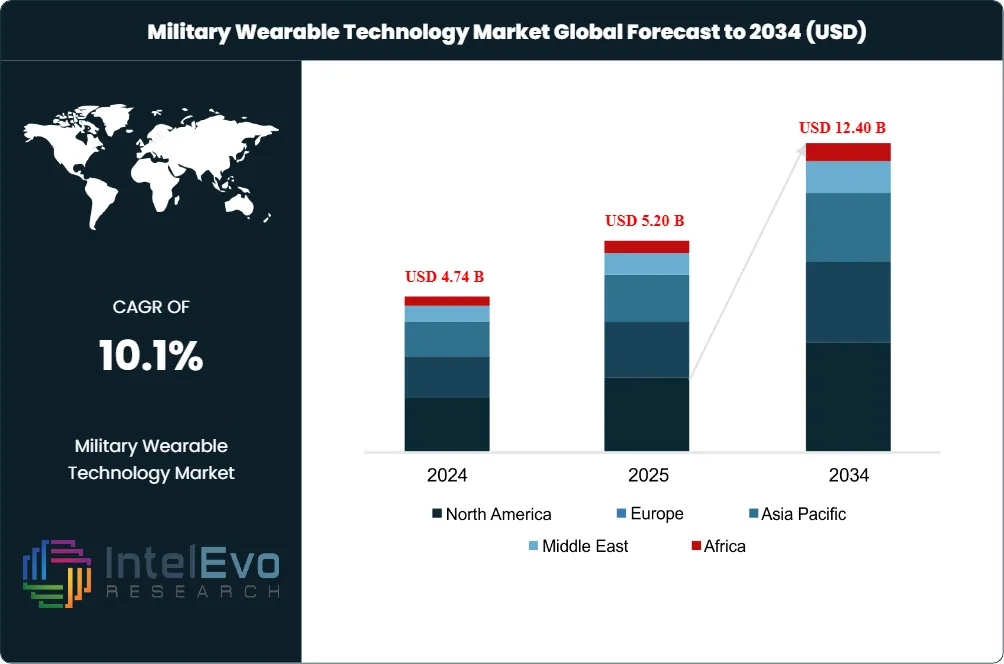

The Military Wearable Technology Market was valued at USD 4.74 Billion in 2024 and USD 5.20 Billion in 2025. The market is projected to reach USD 12.40 Billion by 2034, expanding at a CAGR of 10.1% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 7.20 Billion over the analysis period. Estimates across publicly disclosed defense budgets, contract awards, and primary research diverge by more than 30% at the headline level because vendors define the market with different boundaries; this analysis adopts a mid-range estimate inclusive of head-borne mixed-reality systems, body-worn sensors, smart textiles, hearables, exoskeletons, and the embedded power and communication subsystems that physically attach to the dismounted warfighter.

Get More Information about this report -

Request Free Sample ReportThe Military Wearable Technology Market is being shaped by three converging demand drivers. First, dismounted soldier load remains an operational liability, with infantry packs frequently exceeding 100 pounds, and powered exoskeleton platforms from Lockheed Martin, Sarcos Technology and Robotics, and HeroWear are now in limited fielding to reduce metabolic cost during ruck marches. Second, the U.S. Army's Soldier-Borne Mission Command (SBMC) recompete, formalized after Microsoft's HoloLens-derived IVAS faltered, has redirected procurement attention to Anduril Industries and start-up Rivet, which were each awarded prototyping contracts (USD 159 million and USD 195 million respectively) in September 2025. Third, biometric monitoring has shifted from research to fielded capability through programs such as the Wearable All-hazard Remote-monitoring Program (WARP) using LifeLens patches, with initial deliveries to special operations units in late 2025.

Regulatory and standards gravity rests on MIL-STD-810H environmental qualification, MIL-STD-461G electromagnetic compatibility, the U.S. NETT Warrior interface specification, the European GOSSRA architecture, and Department of War cybersecurity controls under DoD Instruction 8500.01. NATO's interoperability mandates and the EU Permanent Structured Cooperation (PESCO) framework continue to drive requirement convergence between Thales, Rheinmetall, BAE Systems, and Leonardo on dismounted soldier kits.

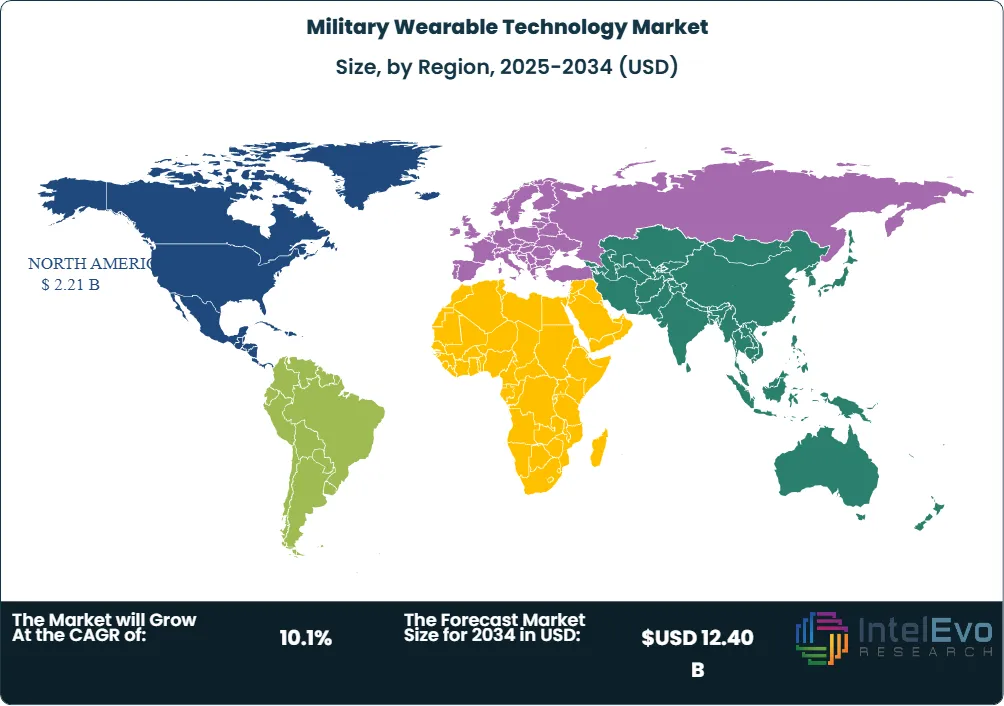

North America commanded approximately 42.5% of 2025 revenue, anchored by U.S. Army, USSOCOM, and U.S. Marine Corps procurement, while Asia Pacific is forecast to record the steepest expansion at roughly 12.5% CAGR through 2034 on the back of indigenous programs in China (PLA digital soldier), India (F-INSAS), South Korea (Warrior Platform), and Japan's accelerated soldier modernization. Defense venture capital reached a record USD 49.1 Billion in 2025, channeling private capital into wearable adjacencies including AI-enabled situational awareness, ear-canal biometric sensors from Aware Defense, and modular exoskeleton subsystems. Forward through 2034, the strongest growth pockets are mixed-reality heads-up displays, wearable robotics for logistics, and CBRN-capable smart patches integrated into the connected-soldier data fabric.

Market Definition & Scope

The Military Wearable Technology Market is defined as the global commercial activity around electronic, optical, robotic, and textile-integrated equipment that is physically attached to or embedded into the uniform, body, or personal load-bearing kit of military personnel for the purpose of enhancing combat effectiveness, situational awareness, physiological monitoring, protection, or load augmentation. The market encompasses head-borne devices (smart helmets, mixed-reality heads-up displays, night vision binoculars, hearables), bodywear (smart vests, biometric patches, smart textiles), wristwear and rings, powered and passive exoskeletons, plus the embedded power, communications, and processing modules that ride directly on the soldier.

This analysis includes military-grade systems procured by armed forces, paramilitary, and special operations entities; dual-use ruggedized commercial wearables (such as smartwatches and rings) deployed under programs like Optimizing the Human Weapon System are within scope when fielded under defense contract. Excluded from scope are vehicle-mounted systems, fixed soldier-system command nodes, training simulators that are not body-worn, consumer fitness wearables sold through retail channels, and law enforcement first-responder kits unless cross-procured under defense vehicles. The Military Wearable Technology Market sits inside the broader Soldier System Market, which industry analysis indicates was approximately USD 14 to 15 Billion in 2025; wearable technology represents roughly one-third of that parent market.

, By Application (Operations, Health Monitoring, Communication & Navigation), By End User (Army, Navy, Air Force), By Core Tech (AI, IoT, Augmented Reality - AR) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Defense Technology Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: the global Military Wearable Technology Market expanded from USD 5.20 Billion in 2025 toward a projected USD 12.40 Billion by 2034 at a 10.1% CAGR.

- Segment Dominance (Type): Bodywear (including smart vests, biometric patches, and smart textiles) accounted for roughly 38.5% of 2025 revenue, the largest share by wearable type.

- Segment Dominance (End User): Land Forces represented approximately 61.5% of 2025 demand by end user, reflecting infantry-led procurement priorities at the U.S. Army, Indian Army, and PLA Ground Force.

- Driver: Connected-soldier modernization programs are pushing wearable spend up by an estimated 15% year-over-year, with the U.S. Department of War allocating more than USD 1 Billion annually to soldier modernization line items.

- Restraint: Unit cost for full mixed-reality kits remains in the USD 30,000 to USD 80,000 per soldier range, slowing procurement pace beyond Tier-1 units.

- Opportunity: Wearable robotics and powered exoskeletons present the steepest opportunity, with industry analysis indicating an 8.85% CAGR through 2030 and an absolute uplift exceeding USD 350 Million by 2034.

- Trend: AI-enabled situational awareness layered onto head-borne displays, exemplified by Anduril's Lattice integration with IVAS-derived hardware, was on the strategy slide of every Tier-1 prime by Q1 2026.

- Regional: North America retained leadership at 42.5% share (USD 2.21 Billion) in 2025, with the United States contributing roughly 88% of regional revenue.

Key Insights Summary

The Military Wearable Technology Market is anchored by a small set of verifiable technical statistics that frame procurement and capability planning across the forecast period.

- The Department of War received an additional USD 7.5 Million in the FY2026 defense appropriations bill to scale up next-generation hearing protection with embedded biometric sensing, work being executed with Aware Defense on custom-molded in-ear systems.

- L3Harris Technologies has shipped more than 18,000 Enhanced Night Vision Goggle-Binocular (ENVG-B) units to U.S. Army users, with Elbit Systems of America logging over 25,000 night vision binocular deliveries cumulatively, providing the installed-base spine for the Binocular Night Observation Device transition.

- The IVAS 1.2 mixed-reality head-borne system carries a measured weight of 3.4 pounds, with the U.S. Army setting an engineering target of 2.9 pounds; the FY2025 budget request included USD 255 Million to procure 3,162 IVAS 1.2 head-up displays.

- Field testing with the U.S. Army's 10th Mountain Division and 101st Airborne Division indicates that powered exoskeleton platforms reduce metabolic cost during sustained ruck marches by approximately 30%, with the SABER passive exosuit evaluated by more than 100 soldiers across Fort Campbell, Fort Sill, and Fort Knox.

- LifeLens patches deployed under the WARP program harvest more than 60 physiological metrics per soldier and are scheduled to become a program of record in fiscal year 2027 following initial fielding to special operations elements in late 2025.

- Defense venture capital posted a record USD 49.1 Billion in calendar 2025, roughly twice the prior-year figure, with wearable-adjacent autonomy and AI infrastructure deals capturing the largest individual rounds.

Competitive Landscape Overview

The Military Wearable Technology Market is moderately consolidated. Industry analysis indicates that the top four publicly traded primes — Lockheed Martin Corporation, L3Harris Technologies, Inc., Elbit Systems Ltd., and BAE Systems plc — together captured an estimated 34% of 2025 revenue, with the next ten players accounting for an additional 28%. Competition is technology-led rather than price-led: contracts are won on sensor fusion, AI-enabled situational awareness, weight reduction, and battery endurance, not on unit price alone.

Competitive evolution accelerated through 2025 and into early 2026 as Anduril Industries displaced Microsoft as production lead on the U.S. Army IVAS program, dragging the soldier mixed-reality category into a defense-tech-native cost structure. Software-defined data architectures from Rivet and Anduril have also reshaped how new entrants compete, with 18-month rapid prototyping sprints replacing decade-long acquisition cycles. M&A and recapitalization activity is concentrated in head-borne autonomy and power management, with Rheinmetall AG closing its Naval Vessels Lürssen takeover on March 1, 2026 to broaden adjacent dismounted-system reach.

Competitive Landscape Matrix

| Company | HQ | Position | Key Product / Solution | Geographic Strength | Recent Strategic Move (Trailing 18 Months) |

|---|---|---|---|---|---|

| Lockheed Martin Corporation | United States | Leader | ONYX Tactical Exoskeleton | North America, NATO | In May 2025, the next-generation ONYX system was placed into the hands of USSOCOM operators under the ROME mobility program. |

| L3Harris Technologies, Inc. | United States | Leader | ENVG-B and BiNOD night vision | North America, Five Eyes | In late February 2026, the company picked up a USD 466 Million Binocular Night Observation Device award from the Department of War. |

| Elbit Systems Ltd. | Israel | Leader | DOMINATOR soldier system, night vision | Israel, U.S., Europe | On August 13, 2025, the company inked a USD 1.635 Billion European country deal spanning C4ISR, electro-optics, and night vision. |

| BAE Systems plc | United Kingdom | Leader | Q-Warrior, Hawkeye image sensors | UK, NATO, Australia | Through 2025 the group widened its smart helmet R&D footprint and rolled the Hawkeye HWK1411 ultra-low-light sensor into NATO night vision kit. |

| Anduril Industries | United States | Challenger | EagleEye / IVAS Next mixed reality | North America | In September 2025 the company secured a USD 159 Million SBMC prototyping contract and assumed IVAS production oversight by April 2025. |

| Thales Group | France | Challenger | Sotas soldier comms, smart helmets | Europe, India, Singapore | During 2025 the group channelled R&D capital into trusted generative AI for soldier-cloud gateways under European NATO frameworks. |

| Honeywell International Inc. | United States | Niche Player | Wearable sensors, smart fabrics | North America, EMEA | Through 2025 the company broadened its physiological monitoring portfolio for harsh-environment military duty cycles. |

| Rheinmetall AG | Germany | Challenger | Gladius soldier system | Germany, Eastern Europe | On March 1, 2026 the group closed its takeover of Naval Vessels Lürssen, widening its German systems-house footprint adjacent to soldier kit. |

Segmentation Analysis

The global Military Wearable Technology Market segments most usefully along four axes — by wearable type, by application, by end user, and by core technology. Each axis reveals different procurement signals and is examined below.

By Wearable Type

The Military Wearable Technology Market is dominated by Bodywear, which industry analysis indicates held approximately 38.5% revenue share (USD 2.00 Billion) in 2025 by virtue of its breadth — the category covers smart vests, plate-carrier-integrated computing, biometric patches such as the LifeLens device fielded under WARP, and conductive smart textiles. Bodywear benefits from a large procurement base because every dismounted soldier wears the category by default, while head-borne devices are issued more selectively. Fortune analysis points to a 38.5% bodywear share against a 21.0% headwear share in the same year, putting the bodywear-headwear delta at 17.5 percentage points. Comparative compliance against ASTM F2992 cut resistance and STANAG 2920 ballistic standards remains a structural barrier to new bodywear entrants.

Headwear (smart helmets, mixed-reality heads-up displays, communication headsets) accounted for around 21.0% (USD 1.09 Billion) in 2025, with a forecast 11.5% CAGR through 2034 — the steepest of any wearable type — driven by the U.S. Army Soldier-Borne Mission Command competition between Anduril Industries and Rivet, plus parallel European programs at Thales and BAE Systems. Hearables, including the Aware Defense in-ear biometric protection device, captured roughly 8.5% (USD 442 Million) and are expected to expand quickly given the FY2026 USD 7.5 Million Department of War increase for biometric-integrated hearing protection. Wristwear and rings took 15.5% (USD 806 Million) in 2025, anchored by ruggedized commercial devices fielded under the Optimizing the Human Weapon System initiative. Exoskeletons remained the smallest category at 5.5% (USD 286 Million) but offer the most aggressive growth profile, with Lockheed Martin's ONYX and Sarcos Technology and Robotics Corporation's Guardian XO Military Variant pulling 8.85% CAGR through 2030 according to industry analysis.

By Application

Communication and Computing led the Military Wearable Technology Market with around 34.2% revenue share (USD 1.78 Billion) in 2025, reflecting the central role of secure tactical voice, data-link encryption, and squad-level mesh networking. The application is anchored to the U.S. NETT Warrior end-user device, the European GOSSRA architecture, and 5G tactical deployments now in pilot at Fort Bragg and RAF Lossiemouth. Vision and Surveillance held the second position at approximately 22.5% (USD 1.17 Billion), buoyed by L3Harris ENVG-B deliveries (over 18,000 cumulative units) and the March 2026 USD 1.27 Billion Binocular Night Observation Device tri-vendor award.

Power and Energy Management is the fastest-rising application and is forecast to expand at roughly 12.0% CAGR through 2034 because every additional sensor on the soldier's body draws additional watts. Conformal batteries, energy-harvesting boots, and modular hot-swap power hubs from Honeywell and Galvion are addressing this constraint. Situational Awareness applications absorbed approximately 18.5% (USD 962 Million) in 2025 and are the principal beneficiary of AI-enabled mixed reality, with Anduril's Lattice software stack now embedded into IVAS-derived head-borne hardware. Training and Simulation, anchored by VirTra recoil kits and squad immersive virtual trainers, contributed a smaller but resilient share.

By End User

Land Forces dominated the Military Wearable Technology Market at 61.5% revenue share (USD 3.20 Billion) in 2025, reflecting infantry-centric procurement at the U.S. Army, Indian Army (F-INSAS), German Bundeswehr (Infanterist der Zukunft), and PLA Ground Force. Within Land Forces, Special Operations Forces drove disproportionate share at an estimated USD 940 Million because USSOCOM functions as the early-adopter unit for ONYX exoskeletons, LifeLens biometric patches, and Anduril mixed-reality prototypes. Airborne Forces held roughly 21.5% (USD 1.12 Billion) and registered the highest end-user growth rate at approximately 12.0% CAGR through 2034 as fighter pilot smart vests (such as the Dutch-developed Flight Sense System) and rotorcraft crew helmets enter wider service.

Naval Forces represented approximately 13.0% (USD 676 Million) in 2025, with the U.S. Marine Corps logistics-focused Sarcos Guardian XO Military Variant and U.K. Royal Navy boarding-party kits as anchor programs. The remainder, including paramilitary and homeland security wearable spend, accounted for roughly 4.0% (USD 208 Million) but is structurally important because it provides the bridge between defense and civilian dual-use procurement. Compared to Land Forces' 61.5% share, Airborne Forces' 21.5% delta of 40.0 percentage points illustrates how concentrated infantry remains as the buying centre for wearable technology.

By Core Technology

Smart Textiles led the Military Wearable Technology Market at approximately 31.1% revenue share (USD 1.62 Billion) in 2025, integrated into combat shirts and base layers from Massif, Crye Precision, and 3M, with conductive yarn fabrics increasingly carrying low-rate data alongside heat. Wearable Robotics and Actuators captured the steepest growth profile at an industry-analysis-indicated 8.85% CAGR through 2030, driven by lower-limb exoskeletons under DEVCOM and SUITX trials at Fort Sill. Augmented and Mixed Reality stood at roughly 18.5% (USD 962 Million) in 2025 and is forecast to outpace the overall market on the back of SBMC, EagleEye, and European equivalents. Network and Connectivity, including 5G tactical, satellite-interoperable radios, and software-defined waveforms, rounds out the core technology stack at approximately 14.0% (USD 728 Million) and is the principal area where Tier-1 buyers benchmark cybersecurity compliance against NIST SP 800-171 and DoD CMMC Level 2 controls.

Regional Analysis

The Military Wearable Technology Market exhibits sharply asymmetric regional shares across the five primary geographies, with North America anchoring revenue and Asia Pacific anchoring growth velocity.

North America accounted for approximately 42.5% revenue share (USD 2.21 Billion) of the Military Wearable Technology Market in 2025. The United States contributed an estimated 88% of regional revenue (USD 1.94 Billion), Canada around 9% (USD 199 Million), and Mexico the balance. The U.S. Department of War's soldier modernization budget exceeded USD 1 Billion annually across FY2025, with the FY2025 IVAS 1.2 procurement line at USD 255 Million for 3,162 head-up displays and the FY2026 DoD biometric hearing protection top-up at USD 7.5 Million. The September 2025 SBMC awards to Anduril (USD 159 Million) and Rivet (USD 195 Million) anchored the regional pipeline through 2027.

Europe represented approximately 24.5% (USD 1.27 Billion) of the Military Wearable Technology Market in 2025, with Germany, the United Kingdom, and France together contributing roughly 65% of European revenue. NATO interoperability mandates and EU PESCO programs continue to drive convergent requirements between Thales, Rheinmetall, BAE Systems, and Leonardo, while Eastern European spending — Poland, Romania, and the Baltic states — accelerated through 2025 on the back of border-security pressure. Rheinmetall's March 1, 2026 closure of the Naval Vessels Lürssen takeover broadened its German dismounted-system adjacencies.

Asia Pacific captured approximately 22.0% (USD 1.14 Billion) of the Military Wearable Technology Market in 2025 and is forecast at 12.5% CAGR through 2034, the steepest of any region. China is targeting indigenous PLA digital-soldier programs, including flexible battery breakthroughs that have triggered NATO counter-investment. India's Future Infantry Soldier as a System (F-INSAS) is rolling indigenous wearables into Indian Army units through 2026, while South Korea's Warrior Platform and Japan's accelerated soldier modernization absorb the remainder. The Asia Pacific market for Japan alone is projected to reach USD 18.8 Million by 2026, China USD 187.3 Million by 2026, and India USD 88.1 Million by 2026 in the narrower military wearable sensors slice.

Latin America accounted for approximately 6.0% (USD 312 Million) of the Military Wearable Technology Market in 2025, with Brazil leading regional procurement through SISFRON border-system extensions and Embraer Defense partnerships. Colombia and Mexico fund counter-insurgency-driven biometric and night vision wearable procurement, with imports primarily from L3Harris and Elbit Systems of America. Regional CAGR through 2034 is forecast at approximately 8.0%, slower than Asia Pacific but ahead of mature Western Europe.

Middle East and Africa held the remaining roughly 5.0% (USD 260 Million) of the Military Wearable Technology Market in 2025, anchored by Saudi Arabia, the UAE, and Israel. Israeli demand sources from indigenous suppliers Elbit Systems and Aselsan partners, while Gulf Cooperation Council buyers source heavily from U.S. and Israeli primes through Foreign Military Sales pathways. Through Q1 2026 the region recorded a step-up in night vision binocular procurement following Israeli operational lessons learned.

Country Analysis

Country-level analysis of the Military Wearable Technology Market sharpens four national pictures that procurement leads cannot extract from regional aggregates alone.

The United States Military Wearable Technology Market reached approximately USD 1.94 Billion in 2025 and is forecast at 9.5% CAGR through 2034, anchored by U.S. Army, USSOCOM, and U.S. Marine Corps procurement. The Soldier-Borne Mission Command program, the Wearable All-hazard Remote-monitoring Program, and the Optimizing the Human Weapon System initiative form the three principal buying vehicles. State-level supplements, including New York and California National Guard pilot fundings for biometric monitoring at the Best Ranger Squad Competition, supplement federal procurement. The Department of War's FY2026 appropriation directed USD 7.5 Million specifically toward biometric-integrated hearing protection development with Aware Defense, and the March 2026 BiNOD tri-vendor award totalling USD 1.27 Billion (L3Harris USD 466 Million, Elbit Systems of America USD 450.6 Million, Photonis Defense USD 352.6 Million) cemented the U.S. as the largest single-country buyer.

China's Military Wearable Technology Market is estimated at approximately USD 540 Million in 2025 with a forecast 13.5% CAGR through 2034, the steepest among the four spotlighted countries. PLA modernization concentrates on flexible-battery breakthroughs, soldier-borne AR optics, and indigenous biometric wristwear from suppliers including DJI's defense spin-outs and state-owned NORINCO subsidiaries. The Pentagon added Unitree to its Chinese Military Companies list in February 2026, signaling the U.S. response to wearable-adjacent robotics. China's procurement path is closed-loop and indigenous, which insulates it from Western export controls but caps interoperability with NATO buyers.

India's Military Wearable Technology Market reached approximately USD 280 Million in 2025 and is forecast at 11.0% CAGR through 2034. The Future Infantry Soldier as a System (F-INSAS) program is the principal vehicle, with Bharat Electronics, Tata Advanced Systems, and BEML supplying subsystems. The Defence Acquisition Council cleared an additional Indian Rupee 2,200 Crore (approximately USD 264 Million) tranche for soldier modernization equipment in late 2025. India's Atmanirbhar Bharat indigenization mandate gives a structural advantage to domestic suppliers over Western primes for body-worn computing, though night vision optics still flow predominantly from imports.

The United Kingdom Military Wearable Technology Market stood at approximately USD 165 Million in 2025 with a forecast 7.5% CAGR through 2034. The Future Soldier program and the Land Industrial Strategy frame procurement, with QinetiQ, BAE Systems, and Leonardo UK as anchor primes. Through 2025 the UK Ministry of Defence channeled funds into ECG-equipped fighter pilot vests under joint Anglo-Dutch development with Elitac Wearables and TNO. The UK's NATO interoperability obligations, combined with AUKUS technology-sharing pathways, position the country as a primary export integration node for U.S. wearable systems entering European service.

Get More Information about this report -

Request Free Sample ReportKey Market Segments

By Wearable Type

- Smart Helmets

- Smart Vests & Body Armor

- Wearable Sensors

- Others

By Application

- Battlefield Operations

- Health & Performance Monitoring

- Communication & Navigation

- Others

By End User

- Army

- Navy

- Air Force

- Others

By Core Technology

- Artificial Intelligence (AI)

- Internet of Things (IoT)

- Augmented Reality (AR)

- Others

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5.20 B |

| Forecast Revenue (2034) | USD 12.40 B |

| CAGR (2025-2034) | 10.1% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Wearable Type, (Smart Helmets, Smart Vests & Body Armor, Wearable Sensors, Others), By Application, (Battlefield Operations, Health & Performance Monitoring, Communication & Navigation, Others), By End User, (Army, Navy, Air Force, Others), By Core Technology, (Artificial Intelligence (AI), Internet of Things (IoT), Augmented Reality (AR), Others), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LOCKHEED MARTIN CORPORATION, L3HARRIS TECHNOLOGIES, INC., ELBIT SYSTEMS LTD., BAE SYSTEMS PLC, ANDURIL INDUSTRIES, INC., THALES GROUP, RHEINMETALL AG, HONEYWELL INTERNATIONAL INC., GENERAL DYNAMICS CORPORATION, NORTHROP GRUMMAN CORPORATION, RTX CORPORATION (COLLINS AEROSPACE), SAAB AB, LEONARDO S.P.A., SAFRAN ELECTRONICS & DEFENSE, ASELSAN A.S., 3M COMPANY, AVON PROTECTION PLC, GALVION LTD., AWARE DEFENSE, OTHERS |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Operations, Health Monitoring, Communication & Navigation), By End User (Army, Navy, Air Force), By Core Tech (AI, IoT, Augmented Reality - AR) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Defense Technology Trends & Forecast 2026-2034")

, By Application (Operations, Health Monitoring, Communication & Navigation), By End User (Army, Navy, Air Force), By Core Tech (AI, IoT, Augmented Reality - AR) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Defense Technology Trends & Forecast 2026-2034")

, By Application (Operations, Health Monitoring, Communication & Navigation), By End User (Army, Navy, Air Force), By Core Tech (AI, IoT, Augmented Reality - AR) Industry Region & Key Players – Industry Segment Overview, Market Dynamics, Competitive Strategies, Defense Technology Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Military Wearable Technology Market?

The Global Military Wearable Technology Market was valued at USD 4.74 Billion in 2024 and USD 5.20 Billion in 2025, and is projected to reach USD 12.40 Billion by 2034, growing at a CAGR of 10.1% from 2026 to 2034. Market growth is driven by soldier modernization programs, AI-powered defense wearables, and advanced battlefield technologies.

Who are the major players in the Military Wearable Technology Market?

LOCKHEED MARTIN CORPORATION, L3HARRIS TECHNOLOGIES, INC., ELBIT SYSTEMS LTD., BAE SYSTEMS PLC, ANDURIL INDUSTRIES, INC., THALES GROUP, RHEINMETALL AG, HONEYWELL INTERNATIONAL INC., GENERAL DYNAMICS CORPORATION, NORTHROP GRUMMAN CORPORATION, RTX CORPORATION (COLLINS AEROSPACE), SAAB AB, LEONARDO S.P.A., SAFRAN ELECTRONICS & DEFENSE, ASELSAN A.S., 3M COMPANY, AVON PROTECTION PLC, GALVION LTD., AWARE DEFENSE, OTHERS

Which segments covered the Military Wearable Technology Market?

By Wearable Type, (Smart Helmets, Smart Vests & Body Armor, Wearable Sensors, Others), By Application, (Battlefield Operations, Health & Performance Monitoring, Communication & Navigation, Others), By End User, (Army, Navy, Air Force, Others), By Core Technology, (Artificial Intelligence (AI), Internet of Things (IoT), Augmented Reality (AR), Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Military Wearable Technology Market

Published Date : 06 Jul 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date