- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

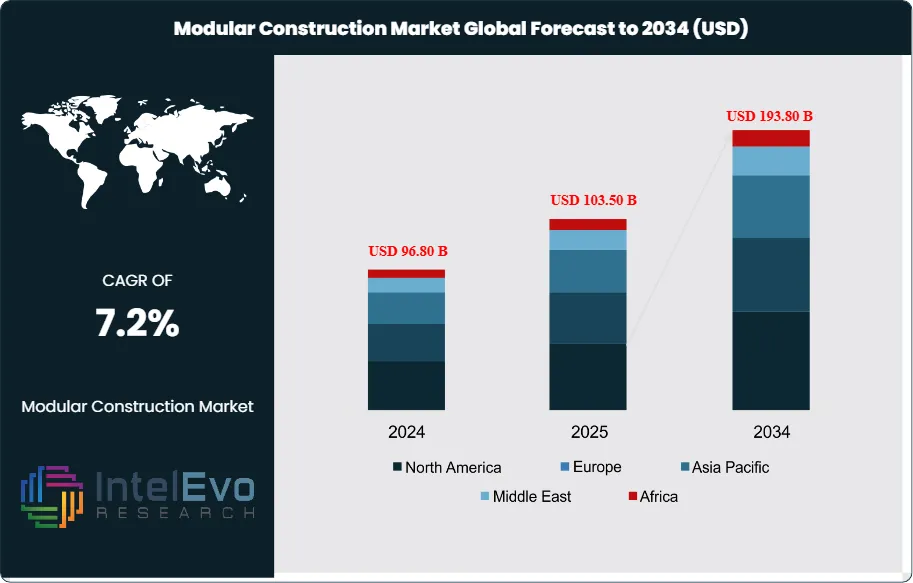

Global Modular Construction Market Size & Forecast | CAGR of 7.2%

Global Modular Construction Market Size, Share, Growth By Type (Permanent - PMC, Relocatable - RMC), By Material (Steel, Wood, Concrete), By End Use (Residential, Commercial, Industrial, Healthcare, Hospitality), By Module Type (Four-Sided, Open-Sided, Mixed, Panels) Region, Key Players – Dynamics, Off-Site Prefabrication & Sustainable Building Tech Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026-2034) | Largest Region (2025) |

| USD 103.50 Billion | USD 193.80 Billion | 7.2% | Asia Pacific, 45.0% |

The Modular Construction Market was valued at USD 96.80 Billion in 2024 and is estimated to reach USD 103.50 Billion in 2025. The market is projected to reach USD 193.80 Billion by 2034, expanding at a CAGR of 7.2% during the forecast period (2026–2034). This represents an absolute dollar opportunity of USD 90.30 billion over the analysis period, driven by accelerating urbanization, structural labor shortages in traditional construction, tightening green building mandates, and growing institutional recognition that offsite factory fabrication delivers 30 to 50% faster project completion than conventional methods.

Get More Information about this report -

Request Free Sample ReportThe structural case for modular construction is grounded in verifiable construction economics. The US Green Building Council reports that buildings in the United States account for approximately 39% of CO2 emissions, 40% of energy use, and 13% of water consumption — a profile that makes factory-controlled construction, with its lower on-site waste and tighter thermal performance standards, a natural compliance vehicle for net-zero building codes. Simultaneously, the Modular Building Institute identified 255 modular manufacturing companies operating in North America alone in its 2024 report, confirming that supply-side infrastructure is reaching a scale that addresses project developers' concern about production capacity and delivery reliability.

Labor market dynamics are accelerating the structural shift toward offsite production. In the United States, a documented 7 million-home supply gap and chronic skilled-trades shortages make factory-based manufacturing — which decouples labor intensity from site location — commercially superior to site-built alternatives at the project level. The US Department of Housing and Urban Development's (HUD) 2024 overhaul of the Manufactured Home Construction and Safety Standards provided regulatory clarity that is unlocking institutional investment in modular housing production. In the United Kingdom, the government's GBP 300 million affordable housing top-up announced in February 2025, channeled through modular supply chains, delivered a commitment to 2,800 additional homes and cemented modular as a primary government housing delivery vehicle.

Technology and digitalization are compressing the cost gap between conventional and modular construction. Building Information Modeling (BIM), digital twins, and generative design tools allow engineers to model entire modular structures virtually — including mechanical, electrical, and plumbing (MEP) coordination — before a single component is fabricated, reducing costly change orders and site rework. Laing O'Rourke's automated UK factory, which in 2025 boosted module production output by 60%, and the integration of robotics into reinforcement cage fabrication that cut manufacturing time by 20% at the company's Bristol facility illustrate how capital investment in production technology is translating into measurable productivity gains.

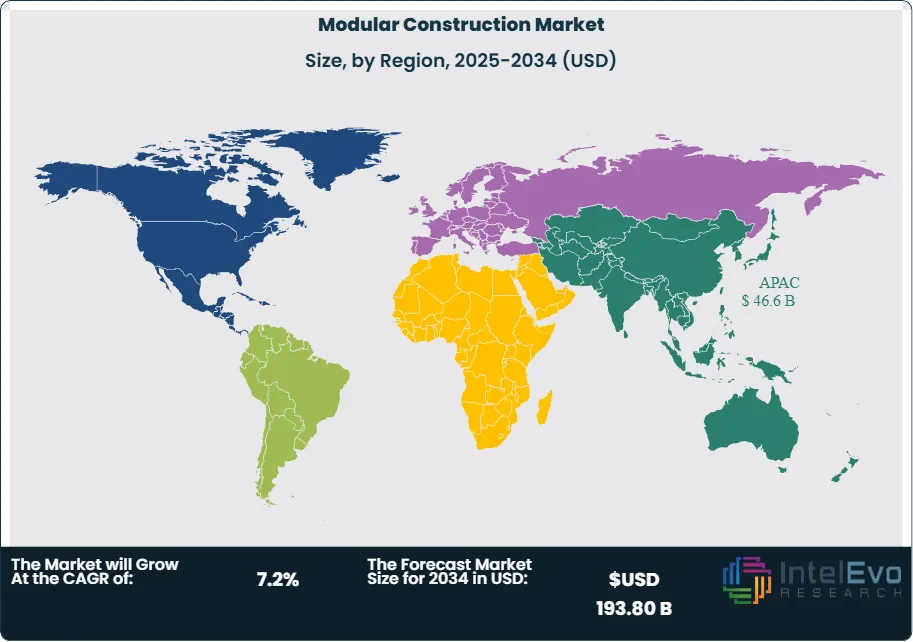

Asia Pacific held 45.0% of global market revenue in 2025 at approximately USD 46.6 billion, with China, Japan, Singapore, and Australia serving as the dominant demand and production centers. Japan's Sekisui House reported net sales exceeding JPY 4 trillion in FY2024, while Singapore's Building and Construction Authority (BCA) Prefabricated Prefinished Volumetric Construction (PPVC) mandate — now covering a minimum 65% of total super-structural floor area for selected government land sales projects — has created the world's most policy-complete modular construction ecosystem. North America represented approximately 25.0% of 2025 revenues, with the United States at USD 24.48 billion and Canada pursuing dedicated prefabricated housing channels under its National Housing Strategy. Europe contributed approximately 22.0%, anchored by Sweden, where 45% of new homes are factory-built, and by the UK's 25% modular penetration target for 2030.

Market Definition and Scope

The modular construction market is defined as the global commercial ecosystem of design, manufacture, transport, and on-site assembly of factory-built three-dimensional modules or volumetric units that are combined at a project site to form permanent or relocatable structures. The market encompasses both permanent modular construction (PMC), where factory-built units are designed for long-term use as fixed structures equivalent in performance and durability to site-built buildings, and relocatable modular construction (RMC), where modules are designed to be disassembled, transported, and redeployed across multiple sites during their operational lifecycle. Materials covered include steel structural frames, concrete panels and volumetric units, engineered wood and cross-laminated timber, and composite or hybrid systems. End applications span residential housing, commercial and office buildings, healthcare facilities, education campuses, hospitality and hotel properties, industrial and energy-sector workforce accommodation, and government infrastructure.

Explicitly excluded from this market scope are manufactured housing and mobile home construction governed by HUD's Title VI provisions, which lack site-assembled volumetric characteristics; conventional precast concrete panel construction where panels are assembled flat rather than as three-dimensional units; and purely modular interior fitout systems not constituting structural building elements. The modular construction sector represents approximately 6 to 8% of global construction spending, with the broader global construction market estimated at more than USD 15 trillion annually per World Bank infrastructure investment data, indicating that modular methods retain substantial headroom for penetration expansion through the forecast period.

, By Material (Steel, Wood, Concrete), By End Use (Residential, Commercial, Industrial, Healthcare, Hospitality), By Module Type (Four-Sided, Open-Sided, Mixed, Panels) Region, Key Players – Dynamics, Off-Site Prefabrication & Sustainable Building Tech Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global modular construction market reached USD 103.50 billion in 2025 and is forecast to reach USD 193.80 billion by 2034, advancing at a CAGR of 7.2% over the 2025-2034 forecast period.

- Segment Dominance (By Type): Permanent modular construction commanded 64.6% of 2025 market revenue, underpinned by growing acceptance that factory-built structures meet or exceed site-built standards for structural integrity, fire resistance, and architectural flexibility in residential, commercial, and institutional applications.

- Segment Dominance (By Material): Steel framing held 84.0% of 2025 material-level market share, valued for its high strength-to-weight ratio, dimensional stability for precision module fabrication, fire resistance, and established global supply chains that support just-in-time factory production schedules.

- Driver: Accelerating urbanization, with the United Nations projecting 6 billion global urban dwellers by 2045, combined with acute skilled construction labor shortages across North America, Europe, and Australia, is compelling developers and governments to adopt offsite factory fabrication that reduces on-site labor dependency by up to 60% versus conventional construction.

- Restraint: Inconsistent building codes across jurisdictions impose project-specific regulatory approval costs, with decentralized permitting in India at the state level and varying International Building Code adoption rates across US counties extending approval timelines by weeks to months and limiting modular operators' ability to replicate standardized designs across geographies.

- Opportunity: Data center modular construction represents an emerging high-value segment, as hyperscale cloud operators including Microsoft, Amazon Web Services, and Google commission pre-fabricated data center modules to compress deployment timelines from 18 to 24 months to under 12 months, while maintaining the precision MEP integration that colocation and edge computing density demands.

- Trend: Building Information Modeling (BIM) integrated with automated design-for-manufacture scripts is becoming the core digital platform for modular project delivery, enabling concurrent site preparation and factory production — the primary mechanism for the 30 to 50% schedule compression that modular advocates cite in client proposals.

- Regional: Asia Pacific led the modular construction market at 45.0% global share, valued at approximately USD 46.6 billion in 2025, sustained by China's vast manufacturing base, Japan's precision housing production platforms, and Singapore's government-mandated PPVC adoption for public housing and government land sales projects.

Key Insights Summary

- Singapore's Building and Construction Authority mandates that Prefabricated Prefinished Volumetric Construction (PPVC) cover a minimum 65% of total super-structural floor area for selected non-landed residential and hotel sites sold under the Government Land Sales (GLS) programme — a regulatory commitment that has turned Singapore's 728 km2 city-state into the world's highest-intensity modular construction market per unit of land area, with the market projected to reach USD 4.79 billion by 2030 at an 8.6% CAGR from 2025.

- Laing O'Rourke's 70:60:30 operating model — 70% of construction value executed offsite, resulting in 60% productivity improvement and 30% delivery time reduction — is the industry's most documented quantification of modular ROI at scale, supported by a record GBP 11.9 billion order book reported in the company's 2025 financial period and net cash generation of GBP 278.5 million in FY2024.

- Sekisui House reported net sales exceeding JPY 4 trillion (approximately USD 27 billion) in FY2024, confirming that residential modular manufacturing at industrial scale can sustain multibillion-dollar revenues; the company's Thailand modular factory achieved an annual production capacity of 1,000 houses, and the company reaffirmed its target to supply 10,000 homes annually in overseas markets by 2025.

- Sweden builds approximately 45% of new homes using factory-based methods — the highest residential modular penetration rate of any non-city-state national market globally — providing a replicable template for the UK, which has set a 25% modular penetration target by 2030 backed by Innovate UK's USD 150 million modular R&D grant program and the February 2025 GBP 300 million affordable housing commitment.

- The Modular Building Institute's 2024 survey documented 255 modular manufacturing companies operating in North America, with total US modular sector investment exceeding USD 2.23 billion over the preceding decade and startup equity funding reaching USD 35.4 million through October 2025 year-to-date — confirming supply-side capacity is scaling alongside demand growth.

- In June 2025, CIMC Modular Building Systems Holdings Co., Ltd. secured a landmark contract to supply 11,000 m2 of offsite-fabricated modular hotel space in Riyadh, Saudi Arabia, targeting 50% construction time reduction versus conventional methods and scheduled for 2026 completion — illustrating how Gulf Cooperation Council megaproject demand is pulling modular capacity into a previously underserved high-value hospitality application.

Competitive Landscape Overview

The modular construction market is moderately fragmented, with Laing O'Rourke, Sekisui House, ATCO Ltd., and Skanska AB collectively commanding an estimated 30 to 35% of global market revenues based on disclosed financial data and project volume estimates, while regional specialists, hospitality-focused operators, and US-centric manufacturers divide the remaining market among more than 255 documented North American manufacturers and numerous Asian and European operators. No single company holds more than a low double-digit percentage of global revenues, reflecting the localized nature of building codes, land costs, and module transport economics that naturally regionalize competition.

Vertical integration distinguishes the highest-margin competitors. Laing O'Rourke, Skanska, and Bouygues Construction deploy models that span development origination, design, factory production, and on-site assembly — capturing value at every stage rather than functioning purely as contract manufacturers for developer clients. This integration compresses design-to-delivery timelines by eliminating interface risk between separate design consultants, manufacturers, and contractors. Japan's Sekisui House carries this further, operating a consumer-direct housing brand with proprietary factory production lines capable of outputting customized homes in days — a model that has produced sustained revenue above JPY 4 trillion and international expansion into Australia and the United States.

The Katerra bankruptcy — which consumed more than USD 2 billion in venture funding before dissolution — established the sector's most instructive failure mode: high fixed-plant cost combined with insufficient throughput to achieve unit economics at scale. The lesson has reoriented capital deployment away from greenfield factory construction toward factory retrofits, factory acquisitions, and hybrid offsite-onsite delivery models that maintain lower fixed-cost bases while growing volume. Sunbelt Modular's acquisition of BRITCO Structures USA in January 2025 as its 11th acquisition, and ATCO's September 2024 acquisition of NRB Modular Solutions, exemplify a roll-up strategy that achieves scale through geographic network expansion rather than single-site megafactory investment.

Competitive Landscape Matrix:

| Company Name | HQ | Market Position | Core Modular Offering | Geographic Strength | Recent Strategic Move |

| Laing O'Rourke | UK | Leader | Design for Manufacture & Assembly (DfMA); 70% offsite delivery model | UK, Australia, Middle East | Record order book of GBP 11.9B in 2025 reporting period; automated Bristol factory boosted module output by 60% in 2025 |

| Sekisui House, Ltd. | Japan | Leader | Factory-precision modular homes; seismic-resistant steel housing systems | Japan, Australia, USA | Expanded modular housing programs in Japan and Australia with high-efficiency units in June 2025 (20% energy reduction, 30% shorter build time) |

| ATCO Ltd. | Canada | Leader | Relocatable and permanent modular structures; remote workforce accommodation | North America, Australia, Middle East | Acquired NRB Modular Solutions in September 2024, expanding Canadian relocatable and permanent portfolio |

| Skanska AB | Sweden | Challenger | Green modular residential and commercial; Nordic off-site ecosystems | Nordic, UK, USA | Sold modular factory BoKlok Byggsystem AB (Gullringen, Sweden) for approx. USD 10.1M to Surewood Housing AB in February 2025 to sharpen focus |

| Bouygues Construction | France | Challenger | Sustainable prefab hospitals, offices; integrated digital twin design | Europe, Middle East | Leveraging modular for healthcare and education infrastructure across Europe and GCC markets (2025) |

| Red Sea International | Saudi Arabia | Challenger | Workforce housing; rapid-deploy camp units; prefab infrastructure for megaprojects | Middle East, Africa | Actively supplying Saudi Vision 2030 megaprojects including NEOM-related workforce accommodation |

| CIMC Modular Building Systems (CIMC-MBS) | China | Niche Player | Steel volumetric modules; hospitality and residential modules | Asia Pacific, Middle East | Secured contract to supply 11,000 m2 modular boutique hotel in Riyadh (June 2025), targeting 50% construction time savings |

| Volumetric Building Companies (VBC / Polcom Group) | USA | Niche Player | Steel and timber hybrid volumetric modules; multifamily and hospitality | North America, Europe | Rebranded as Polcom Group in October 2025, combining wood and steel modular systems for global hospitality and multifamily markets |

By Type

Permanent modular construction (PMC) held 64.6% of 2025 market revenue, generating approximately USD 66.9 billion. Permanent modules are built to meet the same building codes — including the International Building Code (IBC) in the United States and Part A of the UK Building Regulations — as site-built structures, with fire resistance, structural loading, and energy performance requirements identical to conventional construction. The primary commercial driver for PMC adoption is schedule compression: parallel site preparation and factory production reduces overall project timelines by 30 to 50%, enabling developers to achieve earlier occupancy, faster revenue realization, and reduced construction finance carrying costs. Institutional sectors — healthcare, student housing, hotels — where revenue flow begins on day of occupancy rather than years after investment commitment, exhibit the highest PMC adoption rates. VBC's Tracy, California factory, producing 25,000 square feet of modular housing per week, and Berwick, Pennsylvania facility adding 10,000 square feet per week, exemplify the throughput capacity now achievable at factory level.

Relocatable modular construction (RMC) held 35.4% of 2025 market value, approximately USD 36.6 billion, and is expanding at an estimated CAGR of 7.7% — broadly in line with the overall market — because recurring demand from oil and gas workforce accommodation, construction site offices, emergency disaster housing, military deployments, and temporary classrooms creates an annuity-like revenue pattern for fleet-owning operators. ATCO Ltd., WillScot Holdings Corporation, Modulaire Group (Algeco), and Satellite Shelters dominate this segment through large-scale inventories of standardized units available for lease, sale, or lease-to-own. The US government's Federal Emergency Management Agency (FEMA) is an anchor RMC purchaser, with post-disaster rapid housing programs generating purchase orders that sustain factory production through demand cycles. Leasing economics — where the initial module fabrication cost is amortized across multiple deployments — creates structurally higher returns than single-project PMC at equivalent occupancy rates.

By Material

Steel structural systems held 84.0% of 2025 material-level market share, equivalent to approximately USD 86.9 billion, reflecting steel's unmatched combination of structural performance per unit weight, dimensional stability for precision manufacturing, seismic and wind resistance, and mature global supply chains. Steel's capacity to span larger open bays without intermediate columns — a structural requirement for commercial and healthcare applications — gives it functional advantages over concrete and wood in volumetric modules where interior flexibility commands premium valuation. Laing O'Rourke's Bristol factory produces precision steel reinforcement cages that reduce manufacturing time by 20% compared to manual bending, illustrating how factory automation specifically extends steel's cost advantage over on-site fabrication. The US tariff environment of 2025, which raised steel and aluminum import duties to 25% and pushed some steel prices 7.9% above pre-tariff levels by September 2025, introduces cost pressure that is partially offsetting steel's efficiency gains for US-market operators reliant on imported structural steel.

Concrete-based modular construction, including precast volumetric and tilt-up systems, held approximately 10.5% of 2025 material share and is the fastest-growing material segment with an estimated 8.4% CAGR through 2034, driven by its dimensional stability, acoustic performance, thermal mass, and proven suitability for high-rise construction. Singapore's PPVC mandate, which specifies concrete volumetric modules for HDB public housing towers reaching as high as 56 storeys (as demonstrated at Avenue South Residence — the world's tallest PPVC residential building), has created a proven engineering template for high-rise concrete modular construction that China, Hong Kong, and Malaysia are now adopting. Engineered wood and mass timber (CLT, glulam) accounted for approximately 5.5% of 2025 material revenues, with Nordic operators and some Australian and Canadian builders adopting timber modular systems that offer embodied carbon reductions of up to 60% versus structural steel for low-rise residential and education buildings.

By End Use

Residential applications led the modular construction market at 53.5% of 2025 revenues, generating approximately USD 55.4 billion, because housing shortages represent the largest single unmet infrastructure need across all major economies. The US 7 million-home supply gap, the UK's annual new-build requirement of approximately 300,000 homes against a shortfall accumulated over decades, and India's urbanization-driven need for tens of millions of affordable units between 2025 and 2034 create demand at a scale that only factory-production methods can realistically address within government housing timelines. Sekisui House dominates the residential segment globally through its vertically integrated design-build-deliver model, while Clayton Homes (a Berkshire Hathaway subsidiary) controls approximately 50% of the US HUD-code manufactured housing market, distributing factory homes through a network of 350-plus retail locations. Student housing — a residential sub-segment growing at an estimated 8.5% CAGR — is a consistent modular early-adopter because universities can commission factory-built dormitories that avoid disruption to academic calendars with off-site fabrication and commit-date-certain assembly.

Commercial construction held 25.8% of 2025 market revenues, approximately USD 26.7 billion, covering office buildings, retail, hospitality, and data center applications. The hospitality segment has emerged as a particularly active modular adopter — CIMC-MBS's Riyadh hotel contract and Guerdon LLC's North American hotel delivery pipeline illustrate how branded hotel operators can replicate room configurations with factory precision that reduces defect rates and punchlist costs at commissioning. Healthcare at 11.2% of 2025 market revenue is a high-value segment where modular's controlled-environment fabrication ensures MEP service coordination precision — critical for intensive care units, operating theaters, and radiology suites — while schedule certainty allows hospital administrators to plan staff and service migrations with confidence. Industrial and energy sector workforce accommodation (primarily remote oil, gas, and mining camps) constituted the remaining 9.5%, a stable segment anchored by operators including ATCO Ltd. and Red Sea International.

By Module Type

The four-sided fully enclosed (box) module segment held 37.3% of 2025 market share, representing the archetype of volumetric modular construction where a room or room cluster is fabricated as a complete structural unit with floors, walls, ceiling, and MEP services pre-installed. This format optimizes factory productivity through repeatable assembly sequences and minimizes on-site labor. Open-sided modules — which exclude one or more walls to allow wider bays, adaptable floor plans, or large-span commercial spaces — held 29.4% of market share and are growing at the highest module-type CAGR of 9.3% as architects demand formats that eliminate the perception of grid-constrained modular layouts. Partially enclosed and bathroom/kitchen pod modules, which are prefabricated room elements integrated into conventional construction frames rather than full modular buildings, collectively held 33.3% and represent a lower-commitment entry point for developers testing offsite production without committing to full volumetric modular delivery.

Regional Analysis

Asia Pacific held 45.0% of 2025 global modular construction market revenues at approximately USD 46.6 billion, the largest regional share by a substantial margin. China's dominant position as the world's largest construction market, producing modular residential buildings, hotels, and industrial structures through companies including CIMC-MBS and BROAD Group, underpins regional volume. Japan's industry — led by Sekisui House, Misawa Homes, and Daiwa House Industry — operates the world's highest-automation residential modular production lines, with Sekisui's Thai factory producing 1,000 houses per year and its broader global delivery targeting 10,000 overseas homes annually. India represents the highest-growth national market within the region: government programs channeling infrastructure investment through public-private partnerships are accelerating modular school, clinic, and affordable housing production, with steel modular providers Tata Steel Nest-In and BLC India active in the government-sponsored segment. Australia's import of USD 330 million in prefab components over five years confirms cross-border modular trade as a commercially established logistics pattern rather than a theoretical possibility.

North America contributed approximately 25.0% of 2025 global revenues, approximately USD 25.9 billion, with the United States generating USD 24.48 billion and Canada approximately USD 1.4 billion. The US Modular Building Institute's 2024 survey of 255 North American manufacturers documents a supply ecosystem large enough to address the country's 7 million-home supply gap in aggregate — though factory utilization, geographic distribution, and module transport logistics constrain individual project economics significantly. HUD's 2024 standards revision and California's SB 9 accessory dwelling unit streamlining have created tangible regulatory momentum, while state and municipal governments in Massachusetts, Connecticut, and Colorado are pioneering modular procurement frameworks that allow multi-unit housing to bypass conventional site-plan review. Canada's Regional Homebuilding Innovation Initiative, which committed USD 50 million over two years starting 2024, is directing capital toward prefabricated housing supply chains specifically identified in the National Housing Strategy.

Europe represented approximately 22.0% of 2025 market revenues, around USD 22.8 billion. The UK, Germany, Sweden, and Finland lead European market activity, with Sweden's 45% factory-built housing share establishing the regional benchmark for what is achievable when planning policy, land system reform, and industrial standardization align. The UK's Modern Methods of Construction (MMC) framework — supported by Homes England and Innovate UK's USD 150 million modular R&D program — is the primary policy vehicle for achieving the government's 25% modular penetration target by 2030. Germany's Kleusberg GmbH & Co. KG and Riko Group (Slovenia) serve Central European commercial and industrial modular segments, while Modulaire Group (formerly Algeco Scotsman), headquartered in the UK, operates the largest pan-European relocatable modular fleet.

Middle East and Africa held approximately 4.5% of 2025 revenues, approximately USD 4.7 billion, with Saudi Arabia, UAE, and Qatar as the primary demand centers. Saudi Vision 2030's USD 1 trillion in committed infrastructure and megaproject spending — including NEOM, Qiddiya, and the Red Sea Project — has generated workforce housing demand that only rapid-deploy modular solutions can meet at the required scale and timeline. Red Sea International Company, headquartered in Jeddah, supplies the majority of Gulf workforce accommodation through its prefabricated camp and housing portfolio, while CIMC-MBS and international contractors including Laing O'Rourke and Bechtel Corporation supply modular infrastructure for technical project facilities. Latin America contributed approximately 3.5%, approximately USD 3.6 billion, with Brazil, Chile, and Colombia as the primary growth markets, driven by social housing programs and private-sector logistics and energy project workforce accommodation.

Country Analysis

The United States modular construction market generated approximately USD 24.48 billion in 2025, growing at a country CAGR of approximately 6.5% through 2034. The US construction sector faces a documented shortage of 500,000 skilled construction workers per year per Associated Builders and Contractors (ABC) data, creating an economic imperative for factory-based production that reduces on-site skilled labor dependency. HUD's 2024 revision of the Manufactured Home Construction and Safety Standards (24 CFR Parts 3280 and 3282) modernized performance benchmarks that had remained largely static since 1976, signaling federal regulatory alignment with contemporary modular construction methods. The Modular Building Institute documents that modular projects in the US achieve 30 to 50% schedule compression versus comparable site-built projects, directly translating to 5 to 15% lower overall project costs when financing carrying costs are included in the comparative analysis. Sunbelt Modular's January 2025 acquisition of BRITCO Structures USA as its 11th acquisition exemplifies the consolidation trajectory in the US relocatable segment, where scale enables national geographic coverage and fleet optimization across government, healthcare, and education client bases.

Japan's modular construction market was valued at approximately USD 5.89 billion in 2026 (project data) and is one of the most technologically mature residential modular markets globally. Sekisui House — with FY2024 net sales exceeding JPY 4 trillion — operates production lines where custom-configured homes are assembled with automotive-industry precision, achieving factory cycle times that allow complex residential configurations to be produced in days rather than months. Japan's chronic seismic risk has driven technical investment in seismic-resistant steel and hybrid structural systems specifically designed for modular assembly, with government standards from the Ministry of Land, Infrastructure, Transport and Tourism (MLIT) certifying performance requirements that Sekisui House and Daiwa House Industry meet and exceed. The Japan Smart City Initiative supports prefab solutions in urban redevelopment zones, integrating modular construction with energy management systems, EV infrastructure, and building automation in compact high-density residential districts.

The United Kingdom modular construction market generated approximately USD 3.62 billion in 2026 (project data), with the UK government's Modern Methods of Construction (MMC) framework explicitly targeting 25% modular penetration in new residential delivery by 2030. The UK faces an annual housing delivery shortfall estimated at more than 100,000 homes against its 300,000-per-year target, creating political urgency that has translated into Homes England grants, Innovate UK R&D funding of USD 150 million, and the February 2025 GBP 300 million affordable housing top-up directed through modular supply chains. Laing O'Rourke, the UK market's dominant modular constructor, operates a proprietary Design for Manufacture and Assembly (DfMA) platform where 70% of project value is realized in factory — a model that has achieved project delivery 30% faster than site-built alternatives across its UK healthcare, education, and residential portfolio. Make UK Modular, backed by Goldman Sachs, Legal & General, and Sekisui House alongside Laing O'Rourke, has committed GBP 500 million in factory and technology investment and operates capacity sufficient to produce a new home every two hours.

Saudi Arabia's modular construction market is expanding at the fastest pace within the Middle East and Africa region, estimated to grow at a country CAGR exceeding 9.0% through 2034, driven entirely by Saudi Vision 2030's megaproject portfolio. The Kingdom's 50-plus designated gigaproject investments — requiring simultaneous construction of workforce accommodation, logistics bases, and temporary administrative facilities for hundreds of thousands of workers — have made rapid-deploy modular construction the de facto standard for project infrastructure. Red Sea International Company commands the largest share of Saudi workforce housing supply, while international engineering contractors including Bechtel, Fluor, and Laing O'Rourke incorporate modular components into their project delivery frameworks. CIMC-MBS's June 2025 contract for an 11,000 m2 modular boutique hotel in Riyadh signals the transition of Saudi modular demand from purely functional workforce housing toward higher-specification permanent commercial applications aligned with the Kingdom's tourism and hospitality development agenda.

Get More Information about this report -

Request Free Sample ReportKey Market Segment

By Type

- Permanent Modular Construction (PMC)

- Relocatable Modular Construction (RMC)

By Material

- Steel

- Wood

- Concrete

- Others

By End Use

- Residential

- Commercial

- Industrial

- Healthcare

- Education

- Hospitality

- Others

By Module Type

- Four-Sided Modules

- Open-Sided Modules

- Partially Open-Sided Modules

- Mixed Modules

- Modular Panels

By Regional Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 103.50 B |

| Forecast Revenue (2034) | USD 193.80 B |

| CAGR (2025-2034) | 7.2% |

| Historical data | 2021-2025 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, (Permanent Modular Construction (PMC), Relocatable Modular Construction (RMC)), By Material, (Steel, Wood, Concrete, Others), By End Use, (Residential, Commercial, Industrial, Healthcare, Education, Hospitality, Others), By Module Type, (Four-Sided Modules, Open-Sided Modules, Partially Open-Sided Modules, Mixed Modules, Modular Panels), |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | LAING O'ROURKE, SEKISUI HOUSE, LTD., ATCO LTD., SKANSKA AB, BOUYGUES CONSTRUCTION, RED SEA INTERNATIONAL COMPANY, CIMC MODULAR BUILDING SYSTEMS HOLDINGS CO., LTD., MODULAIRE GROUP (ALGECO), LENDLEASE CORPORATION, KLEUSBERG GMBH & CO. KG, BECHTEL CORPORATION, FLUOR CORPORATION, VINCI CONSTRUCTION, GUERDON, LLC, CAVCO INDUSTRIES, INC., CLAYTON HOMES, INC., WILLSCOT HOLDINGS CORPORATION, SUNBELT MODULAR, INC., HICKORY GROUP PTY. LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Material (Steel, Wood, Concrete), By End Use (Residential, Commercial, Industrial, Healthcare, Hospitality), By Module Type (Four-Sided, Open-Sided, Mixed, Panels) Region, Key Players – Dynamics, Off-Site Prefabrication & Sustainable Building Tech Trends & Forecast 2026-2034")

, By Material (Steel, Wood, Concrete), By End Use (Residential, Commercial, Industrial, Healthcare, Hospitality), By Module Type (Four-Sided, Open-Sided, Mixed, Panels) Region, Key Players – Dynamics, Off-Site Prefabrication & Sustainable Building Tech Trends & Forecast 2026-2034")

, By Material (Steel, Wood, Concrete), By End Use (Residential, Commercial, Industrial, Healthcare, Hospitality), By Module Type (Four-Sided, Open-Sided, Mixed, Panels) Region, Key Players – Dynamics, Off-Site Prefabrication & Sustainable Building Tech Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Modular Construction Market?

Global Modular Construction Market was valued at USD 96.80 billion in 2024 and is projected to reach USD 193.80 billion by 2034, at a CAGR of 7.2% (2026–2034).

Who are the major players in the Modular Construction Market?

LAING O'ROURKE, SEKISUI HOUSE, LTD., ATCO LTD., SKANSKA AB, BOUYGUES CONSTRUCTION, RED SEA INTERNATIONAL COMPANY, CIMC MODULAR BUILDING SYSTEMS HOLDINGS CO., LTD., MODULAIRE GROUP (ALGECO), LENDLEASE CORPORATION, KLEUSBERG GMBH & CO. KG, BECHTEL CORPORATION, FLUOR CORPORATION, VINCI CONSTRUCTION, GUERDON, LLC, CAVCO INDUSTRIES, INC., CLAYTON HOMES, INC., WILLSCOT HOLDINGS CORPORATION, SUNBELT MODULAR, INC., HICKORY GROUP PTY. LTD., Others

Which segments covered the Modular Construction Market?

By Type, (Permanent Modular Construction (PMC), Relocatable Modular Construction (RMC)), By Material, (Steel, Wood, Concrete, Others), By End Use, (Residential, Commercial, Industrial, Healthcare, Education, Hospitality, Others), By Module Type, (Four-Sided Modules, Open-Sided Modules, Partially Open-Sided Modules, Mixed Modules, Modular Panels),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date