- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

mRNA Vaccine and Therapeutics Market Size, Share & Growth | CAGR 13.3%

Global mRNA Vaccine and Therapeutics Market Size, Share, Analysis By Product Type (mRNA Vaccines, mRNA Therapeutics), By Application (Infectious Diseases, Oncology, Rare Disease & Metabolic Disorders), By Technology Type (Conventional Non-Replicating mRNA Platforms, Self-Amplifying mRNA, Personalized and Specialty Therapeutic mRNA Platforms), By End-User (Hospitals & Health Systems, Retail Pharmacies & Vaccination Clinics, Specialty Oncology Centers, Academic & Research Centers) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 6.9 Billion, 2025 | USD 21.2 Billion, 2034 | 13.3%, 2026–2034 | North America, 47.0%, 2025 |

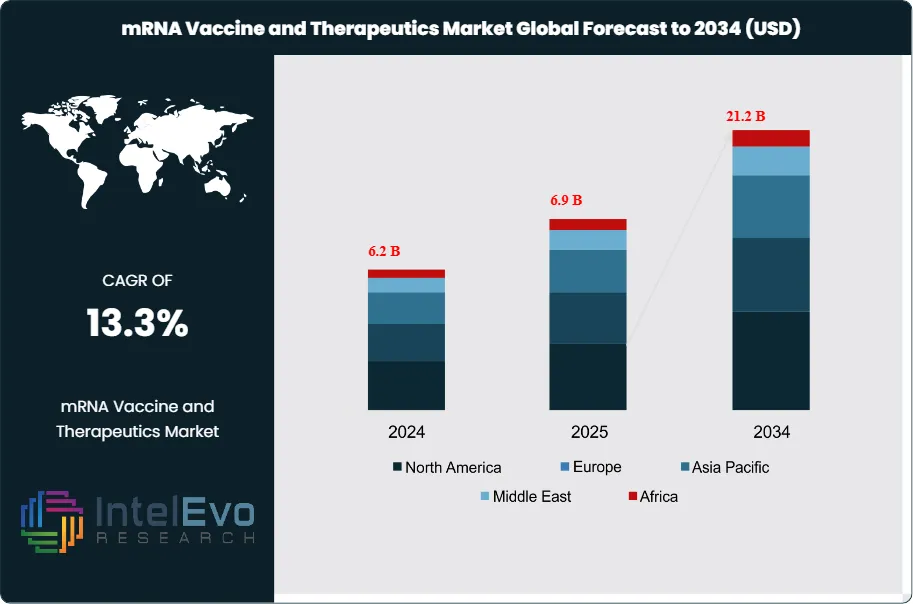

The mRNA Vaccine and Therapeutics Market was valued at approximately USD 6.2 Billion in 2024 and increased to USD 6.9 Billion in 2025. The market is projected to reach nearly USD 21.2 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 13.3% during the forecast period from 2026 to 2034. Market growth is primarily driven by the continued commercialization of mRNA-based vaccines alongside rapid expansion into oncology, rare disease, and personalized medicine applications. Additionally, increasing regulatory approvals, advancements in delivery technologies such as lipid nanoparticles, and strong pipeline development across therapeutic areas are expected to further accelerate adoption and long-term market expansion.

Get More Information about this report -

Request Free Sample ReportThe mRNA Vaccine and Therapeutics Market in 2025 remained commercially led by vaccines, but its strategic center of gravity began shifting toward therapeutics. Pfizer reported USD 4.37 Billion in full-year 2025 Comirnaty revenue. Moderna reported USD 1.94 Billion in 2025 total revenue, supported by Spikevax, mRESVIA, and MNEXSPIKE. Moderna also stated that it ended 2025 with three products on the market. These figures show that the current market is still powered by prophylactic vaccination revenue, while the therapeutic side remains earlier-stage and is expressed mainly through pipeline investment, licensing, and collaboration economics rather than broad product sales.

The mRNA Vaccine and Therapeutics Market changed materially in 2025 because the commercial vaccine base broadened beyond legacy COVID-19 boosters. The FDA approved Moderna’s MNEXSPIKE in 2025, creating a second approved U.S. COVID-19 mRNA product within Moderna’s updated respiratory franchise. Outside the United States, CSL and Arcturus expanded the self-amplifying mRNA category. Japan approved KOSTAIVE in 2024, and the European Commission approved it in February 2025, making it the first approved self-amplifying mRNA COVID-19 vaccine in Europe. These approvals matter because they show that the market is no longer defined by one vaccine platform architecture. It now includes conventional mRNA and sa-mRNA formats, with broader room for competitive differentiation in dose, persistence, and manufacturing efficiency.

On the therapeutics side, no broad commercial mRNA therapeutic franchise had yet matched vaccine scale in 2025, but capital and pipeline momentum accelerated. BioNTech announced in June 2025 that it would acquire CureVac to strengthen mRNA design, delivery formulations, manufacturing, and cancer immunotherapy development. Moderna and Merck continued advancing intismeran autogene, with Merck stating in 2025 that the Phase 3 adjuvant melanoma trial was fully enrolled and NSCLC Phase 3 programs were enrolling. Moderna also announced a global commercialization collaboration with Recordati in January 2026 for mRNA-3927 in propionic acidemia. These moves indicate that the mRNA Vaccine and Therapeutics Market is entering a second phase where oncology and rare-disease programs increasingly influence valuation, partnering, and manufacturing strategy.

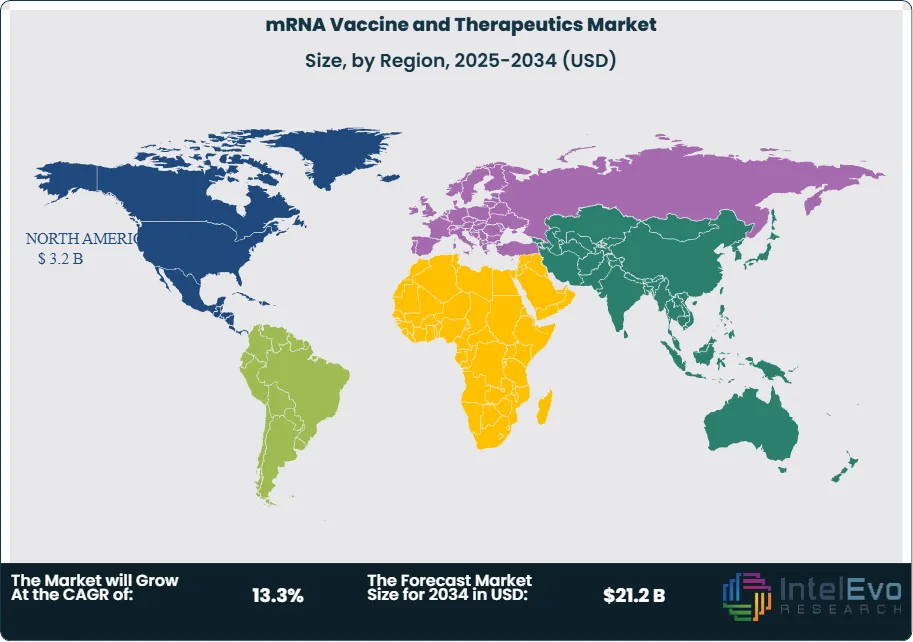

Supply and regulation remain the main risk factors. The market still depends on lipid nanoparticle supply, cold-chain management, fill-finish readiness, and seasonal demand forecasting. Pfizer’s 2025 results showed Comirnaty sales were pressured by lower vaccination rates and narrower U.S. vaccination recommendations. Moderna’s 2025 results also reflected a still-evolving respiratory vaccine market. Regionally, North America held 47.0% of the mRNA Vaccine and Therapeutics Market in 2025, equal to USD 3.2 Billion, followed by Europe at 28.0% and Asia Pacific at 18.0%. North America led because it combines the largest approved-product base, deeper reimbursement, and the most advanced clinical ecosystem for mRNA oncology and rare-disease programs. Europe remained the main platform and IP center, while Asia Pacific emerged as the most active partnership and self-amplifying mRNA growth zone.

, By Application (Infectious Diseases, Oncology, Rare Disease & Metabolic Disorders), By Technology Type (Conventional Non-Replicating mRNA Platforms, Self-Amplifying mRNA, Personalized and Specialty Therapeutic mRNA Platforms), By End-User (Hospitals & Health Systems, Retail Pharmacies & Vaccination Clinics, Specialty Oncology Centers, Academic & Research Centers) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The mRNA Vaccine and Therapeutics Market stood at USD 6.9 Billion in 2025 and is projected to reach USD 21.2 Billion by 2034 at a 13.3% CAGR. The 2025 revenue base was still dominated by approved mRNA vaccines, especially Comirnaty and Moderna’s respiratory franchise.

- Segment Dominance: By product type, mRNA vaccines led with 89.0% share in 2025, or USD 6.1 Billion. This segment stayed dominant because Pfizer reported USD 4.37 Billion in 2025 Comirnaty sales and Moderna reported USD 1.82 Billion in 2025 net product sales across marketed mRNA products.

- Segment Dominance: By application, infectious diseases held the largest share at 86.0% in 2025, equal to USD 5.9 Billion. COVID-19, RSV, and other respiratory vaccine programs remained the main commercial engine, while oncology therapeutics were still pipeline-led.

- Driver: The main driver is approved-product expansion and platform renewal. Moderna added MNEXSPIKE in 2025, and Pfizer still generated USD 4.37 Billion from Comirnaty in 2025 despite a narrower recommendation environment.

- Restraint: The main restraint is seasonal demand volatility and policy sensitivity. Pfizer said lower vaccination rates and a narrower U.S. recommendation reduced Comirnaty sales in 2025, and Moderna described the respiratory vaccine market as still evolving.

- Opportunity: The largest opportunity sits in oncology and rare-disease therapeutics. BioNTech’s CureVac acquisition, Moderna’s Recordati deal, and Merck-Moderna Phase 3 expansion indicate more than USD 5.0 Billion of incremental therapeutic market potential could be created between 2025 and 2034.

- Trend: Self-amplifying mRNA is the clearest technology trend. KOSTAIVE became the first approved sa-mRNA COVID-19 vaccine in Japan and then in Europe, creating a second commercial architecture beyond conventional mRNA LNP vaccines.

- Regional Analysis: North America led the mRNA Vaccine and Therapeutics Market with 47.0% share and USD 3.2 Billion revenue in 2025. The region leads because it has the strongest approved-product revenue base and the deepest clinical and commercial ecosystem for mRNA medicines.

Competitive Landscape

The mRNA Vaccine and Therapeutics Market is moderately consolidated. The top four companies controlled an estimated 82.0% of 2025 market revenue. Competition is technology-driven and platform-based, centered on delivery systems, manufacturing control, seasonal commercial execution, and therapeutic pipeline credibility. Pfizer remained the largest single revenue contributor through USD 4.37 Billion of 2025 Comirnaty sales, while Moderna generated USD 1.94 Billion of total 2025 revenue and expanded to three marketed products. Competitive intensity rose in 2025 as BioNTech moved to acquire CureVac and sa-mRNA products gained commercial approval in Japan and Europe.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| PFIZER | US | Leader | Comirnaty | North America, Europe | Reported USD 4.37 Billion in 2025 Comirnaty revenue and continued seasonal COVID-19 franchise management in Feb 2026 results. |

| MODERNA | US | Leader | Spikevax / MNEXSPIKE / mRESVIA platform | North America | Reported USD 1.94 Billion in 2025 revenue and launched MNEXSPIKE after 2025 FDA approval. |

| BIONTECH | Germany | Leader | Comirnaty profit-share and mRNA oncology platform | Europe, North America | Announced acquisition of CureVac in June 2025 to strengthen mRNA cancer immunotherapy capabilities. |

| CSL SEQIRUS / ARCTURUS | Australia / US | Leader | KOSTAIVE self-amplifying mRNA vaccine | Asia Pacific, Europe | Won European Commission approval for KOSTAIVE in Feb 2025 after Japan approval in 2024. |

| GSK | UK | Challenger | Licensed mRNA respiratory vaccine portfolio from CureVac | Europe | Restructured collaboration with CureVac into a licensing agreement in Jul 2024 and later participated in the Aug 2025 U.S. litigation settlement. |

| CUREVAC | Germany | Challenger | mRNA design and delivery platform | Europe | Recognized 2025 revenue from GSK amendments and BioNTech/Pfizer royalties before being acquired by BioNTech. |

| SANOFI | France | Challenger | mRNA vaccine platform and Center of Excellence | Europe, North America | Continued scaling its mRNA vaccine platform and broader vaccine M&A strategy through 2025. |

| MERCK & CO. | US | Challenger | Intismeran autogene (mRNA-4157/V940) with Moderna | North America | Reported in 2025 that the Phase 3 adjuvant melanoma trial was fully enrolled and NSCLC studies were enrolling. |

| CSL | Australia | Niche Player | Commercialization of KOSTAIVE | Asia Pacific, Europe | Expanded sa-mRNA vaccine commercialization through EU approval in Feb 2025. |

| RECORDATI | Italy | Niche Player | mRNA-3927 commercialization partner | Europe | Entered global collaboration with Moderna for propionic acidemia candidate mRNA-3927 in Jan 2026. |

By Product Type

By product type, mRNA vaccines accounted for 89.0% of the mRNA Vaccine and Therapeutics Market in 2025, or USD 6.1 Billion. This segment dominated because almost all commercialized mRNA revenue still came from preventive vaccines rather than therapeutic products. Pfizer’s USD 4.37 Billion of 2025 Comirnaty revenue and Moderna’s USD 1.82 Billion of 2025 net product sales largely explain the segment’s lead. Commercial vaccines also benefit from mature regulatory paths, defined seasonal purchasing cycles, and much broader patient populations than personalized or specialty therapeutics. Within vaccines, COVID-19 remained the overwhelming revenue driver, while RSV added diversification through mRESVIA and self-amplifying mRNA gained commercial legitimacy through KOSTAIVE. Competition in this segment is shaped by immunogenicity, durability, manufacturing scale, and ability to respond quickly to strain updates. The segment should remain dominant through 2034, but its share will gradually decline as therapeutic programs begin to convert pipeline value into product revenue.

mRNA therapeutics represented 11.0% of the market in 2025, or USD 0.8 Billion. This segment was still early commercially and was driven mainly by collaboration economics, milestone structures, licensing value, and clinical investment rather than broad marketed-product sales. The clearest examples were BioNTech’s acquisition of CureVac to strengthen mRNA oncology development and Moderna’s global commercialization collaboration with Recordati for mRNA-3927. Merck and Moderna also continued expanding intismeran autogene into Phase 3 melanoma and NSCLC settings, which reinforced therapeutic market credibility even without 2025 product sales at scale. The segment is smaller today, but it should be the faster-growing portion of the mRNA Vaccine and Therapeutics Market through 2034 because oncology, rare disease, and personalized medicine create much larger untapped value pools than seasonal vaccine updates alone.

By Application

By application, infectious diseases held 86.0% share in 2025, equal to USD 5.9 Billion. This segment remained dominant because approved mRNA products are still concentrated in COVID-19 and RSV prevention. Comirnaty remained the single largest product, while Moderna’s marketed portfolio included Spikevax, MNEXSPIKE, and mRESVIA. Infectious disease applications benefit from large target populations, clearer regulatory precedent, and government or payer familiarity with vaccination campaigns. The segment also includes self-amplifying mRNA vaccines, which started to matter commercially after KOSTAIVE approvals in Japan and Europe. Despite ongoing market normalization after the pandemic peak, infectious disease remained the structural revenue anchor for the mRNA Vaccine and Therapeutics Market in 2025.

Oncology represented 10.0%, or USD 0.7 Billion, and rare disease and metabolic disorders accounted for 4.0%, or USD 0.3 Billion. These segments were still mainly pipeline-led in 2025, but they are strategically more important than their current revenue share suggests. Oncology is led by personalized cancer vaccines and other mRNA immunotherapy programs, especially Moderna and Merck’s intismeran autogene and BioNTech’s broader cancer strategy after the CureVac transaction. Rare disease remained smaller, but Moderna’s Recordati collaboration around propionic acidemia shows that high-value, low-population therapeutic use cases are becoming more commercial. These applications carry higher development risk than vaccines, yet they also carry stronger pricing power and more durable differentiation if approved. That combination makes them the most important future expansion area in the mRNA Vaccine and Therapeutics Market.

By Technology Type

By technology type, conventional non-replicating mRNA platforms held 83.0% of the mRNA Vaccine and Therapeutics Market in 2025, or USD 5.7 Billion. This segment led because every large commercial product in the U.S. market in 2025 used the established non-replicating mRNA plus lipid nanoparticle format. Comirnaty, Spikevax, MNEXSPIKE, and mRESVIA all sit within this segment. Conventional mRNA benefited from manufacturing experience, clinical familiarity, and a larger commercial evidence base. It remains the benchmark platform for both vaccines and near-term therapeutic development.

Self-amplifying mRNA accounted for 7.0%, equal to USD 0.5 Billion, while personalized and specialty therapeutic mRNA platforms represented 10.0%, or USD 0.7 Billion. Self-amplifying mRNA is still commercially small, but it became strategically important after KOSTAIVE became the first approved sa-mRNA COVID-19 vaccine in Japan and then Europe. Personalized and specialty therapeutic mRNA includes oncology and rare-disease programs such as mRNA-4157 and mRNA-3927. This category is still pre-scale in 2025, but it attracts disproportionate strategic interest because it could expand the market beyond seasonal vaccination and into individualized medicine. Over time, technology mix will matter more because the mRNA Vaccine and Therapeutics Market is no longer only about product labels. It is also about which platform architecture can deliver better persistence, tolerability, and manufacturing economics.

By End User

By end user, hospitals and health systems accounted for 36.0% of the mRNA Vaccine and Therapeutics Market in 2025, or USD 2.5 Billion. They led because a large share of adult COVID-19 and RSV vaccination, as well as future therapeutic administration, flows through organized healthcare systems rather than retail-only channels. Retail pharmacies and vaccination clinics held 34.0%, equal to USD 2.3 Billion, reflecting the established commercial model for seasonal mRNA vaccination in the U.S. and selected European markets. Specialty oncology centers represented 18.0%, or USD 1.2 Billion, even though therapeutic revenue remained early. This share is strategically important because it reflects where future mRNA oncology products will be adopted first.

Academic and research centers held 12.0%, or USD 0.8 Billion, supported by clinical trial activity and translational medicine programs. End-user mix matters because the market is gradually moving from population-wide vaccination channels toward more specialized therapeutic delivery networks. That transition will reshape commercial models between 2026 and 2034.

Regional Analysis

North America mRNA Vaccine and Therapeutics Market

North America held 47.0% of the mRNA Vaccine and Therapeutics Market in 2025, equal to USD 3.2 Billion. The United States led overwhelmingly, followed by Canada and Mexico. The region remained the largest because it combined the biggest commercial product base with the deepest clinical-development ecosystem. Pfizer reported USD 4.37 Billion in 2025 Comirnaty revenue, and Moderna reported USD 1.94 Billion in 2025 total revenue with three marketed products. The FDA also approved MNEXSPIKE in 2025, which helped preserve U.S. market breadth even as COVID vaccination recommendations narrowed. North America also led therapeutic development because Moderna, Merck, Pfizer, and many emerging mRNA oncology programs are concentrated in U.S.-centered clinical networks.

The region’s main advantage is commercial infrastructure. Retail pharmacies, hospital systems, specialty oncology centers, and advanced reimbursement pathways allow mRNA products to scale faster here than in any other region. Its main risk is policy sensitivity. Pfizer explicitly linked lower Comirnaty sales to lower vaccination rates and narrower U.S. recommendations in 2025. That means North America remains the most commercially important region, but it is also the region where guideline changes can move revenue most sharply. Mexico adds an additional strategic layer because Moderna announced a long-term agreement with the Mexican government for respiratory vaccines. That gives North America both current revenue scale and future franchise diversification.

Europe mRNA Vaccine and Therapeutics Market

Europe accounted for 28.0% of the mRNA Vaccine and Therapeutics Market in 2025, or USD 1.9 Billion. Germany, France, the UK, and Switzerland were the most strategically relevant countries. Europe remained the main platform and IP hub of the market. BioNTech is based in Germany, CureVac was also Germany-based before its BioNTech acquisition, and many major partnerships and patent disputes were centered in Europe. The region also led in cross-border strategic activity. BioNTech announced the CureVac transaction in June 2025, and GSK had already restructured its CureVac collaboration into a licensing agreement in 2024. These moves show that Europe is not only a sales market. It is also the main control center for mRNA platform ownership and technology reshaping.

Europe also strengthened its commercial diversity in 2025 through self-amplifying mRNA. The European Commission approved CSL and Arcturus’ KOSTAIVE in February 2025, giving the region the first sa-mRNA COVID vaccine approval. Reimbursement and procurement remain more fragmented than in North America, which slows rapid scaling, but the region compensates with strong manufacturing capability and scientific depth. Germany and France remain central for R&D and platform ownership. The UK matters through large pharmaceutical capital and vaccine strategy. Switzerland is strategically relevant because Novartis and several advanced platform companies anchor broader European biotech influence, even outside pure mRNA. Europe should retain a strong share of the mRNA Vaccine and Therapeutics Market through 2034 because it remains the region where platform control, licensing, and translational science intersect most directly.

Asia Pacific mRNA Vaccine and Therapeutics Market

Asia Pacific held 18.0% of the mRNA Vaccine and Therapeutics Market in 2025, equal to USD 1.2 Billion. China, Japan, India, and Australia were the most relevant countries. Japan stood out because it approved KOSTAIVE in 2024, making it the first approved self-amplifying mRNA COVID-19 vaccine globally. Australia matters because CSL commercialized KOSTAIVE with Arcturus and because the region is increasingly important in vaccine manufacturing and launch sequencing. China is strategically important for future growth and clinical scaling, while India remains earlier-stage commercially but highly relevant for long-term vaccine deployment and cost-sensitive market expansion.

Asia Pacific’s main strength is its ability to support both commercial rollout and future platform diversification. The region is also less tied to one single commercial structure than North America. Japan supports premium regulated launches, while broader Asia creates room for differentiated manufacturing and partnership models. The region’s main limitation is uneven reimbursement and infrastructure for future therapeutics. Vaccines can scale more easily than oncology or rare-disease mRNA medicines in most Asia Pacific markets today. Even so, the region should post one of the fastest growth rates through 2034 because self-amplifying mRNA, respiratory vaccine expansion, and future personalized oncology programs can all find important footholds here.

Latin America mRNA Vaccine and Therapeutics Market

Latin America represented 4.0% of the mRNA Vaccine and Therapeutics Market in 2025, or USD 0.3 Billion. Brazil led the region, followed by Mexico and Argentina. Commercial scale remained limited compared with North America and Europe because access is shaped by public procurement, payer constraints, and uneven adult vaccination penetration. The region’s importance is strategic rather than purely financial. Mexico became more visible after Moderna announced a long-term respiratory vaccine agreement with the Mexican government. Brazil remains the largest healthcare market and likely long-term anchor, but 2025 revenue still reflected a relatively small installed mRNA base compared with mature Western markets.

The region’s main opportunity lies in respiratory vaccination and eventual public-health procurement rather than near-term therapeutic rollout. mRNA oncology and rare-disease therapeutics require specialist infrastructure and reimbursement discipline that remain concentrated in a limited number of centers. Over time, Latin America should benefit from lower-dose formats, broader government partnerships, and simpler seasonal vaccine distribution models. Its 2025 share remained modest, but it represents a clear secondary expansion market for established mRNA franchises.

Middle East & Africa mRNA Vaccine and Therapeutics Market

Middle East & Africa held 3.0% of the mRNA Vaccine and Therapeutics Market in 2025, equal to USD 0.2 Billion. The UAE, Saudi Arabia, and South Africa were the most relevant countries. The region remained the smallest because premium mRNA access is still limited by budget capacity, procurement timing, and specialized therapeutic infrastructure. The Gulf states led because they have stronger tertiary care and faster uptake of premium imported vaccines. South Africa remained the most relevant sub-Saharan market because of its stronger clinical infrastructure and public health capabilities.

The market is still early, but there is clear strategic interest in advanced biologics platforms. Commercial growth will be led first by vaccines and later by selected specialty therapeutics. The main barrier is not scientific acceptance. It is sustained reimbursement and delivery capacity. Through 2034, Middle East & Africa will remain the smallest major regional market, but targeted investment in high-income Gulf healthcare systems should raise absolute revenue from a low base.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- mRNA Vaccines

- mRNA Therapeutics

By Application

- Infectious Diseases

- Oncology

- Rare Disease and Metabolic Disorders

By Technology Type

- Conventional Non-Replicating mRNA Platforms

- Self-Amplifying mRNA

- Personalized and Specialty Therapeutic mRNA Platforms

By End User

- Hospitals and Health Systems

- Retail Pharmacies and Vaccination Clinics

- Specialty Oncology Centers

- Academic and Research Centers

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | 6.9 B |

| Forecast Revenue (2034) | 21.2 B |

| CAGR (2025-2034) | 13.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (mRNA Vaccines, mRNA Therapeutics), By Application (Infectious Diseases, Oncology, Rare Disease and Metabolic Disorders), By Technology Type (Conventional Non-Replicating mRNA Platforms, Self-Amplifying mRNA, Personalized and Specialty Therapeutic mRNA Platforms), By End User (Hospitals and Health Systems, Retail Pharmacies and Vaccination Clinics, Specialty Oncology Centers, Academic and Research Centers) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | PFIZER, MODERNA, BIONTECH, CSL SEQIRUS / ARCTURUS, GSK, CUREVAC, SANOFI, MERCK & CO., RECORDATI, CSL, ARCTURUS THERAPEUTICS, CRISPR THERAPEUTICS, NOVARTIS, REGENERON, MEIJI SEIKA PHARMA, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Infectious Diseases, Oncology, Rare Disease & Metabolic Disorders), By Technology Type (Conventional Non-Replicating mRNA Platforms, Self-Amplifying mRNA, Personalized and Specialty Therapeutic mRNA Platforms), By End-User (Hospitals & Health Systems, Retail Pharmacies & Vaccination Clinics, Specialty Oncology Centers, Academic & Research Centers) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2026–2034")

, By Application (Infectious Diseases, Oncology, Rare Disease & Metabolic Disorders), By Technology Type (Conventional Non-Replicating mRNA Platforms, Self-Amplifying mRNA, Personalized and Specialty Therapeutic mRNA Platforms), By End-User (Hospitals & Health Systems, Retail Pharmacies & Vaccination Clinics, Specialty Oncology Centers, Academic & Research Centers) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2026–2034")

, By Application (Infectious Diseases, Oncology, Rare Disease & Metabolic Disorders), By Technology Type (Conventional Non-Replicating mRNA Platforms, Self-Amplifying mRNA, Personalized and Specialty Therapeutic mRNA Platforms), By End-User (Hospitals & Health Systems, Retail Pharmacies & Vaccination Clinics, Specialty Oncology Centers, Academic & Research Centers) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Innovation Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the mRNA Vaccine and Therapeutics Market?

The Global mRNA Vaccine and Therapeutics Market was valued at USD 6.9 Billion in 2025, projected to reach USD 21.2 Billion by 2034 at a CAGR of 13.3% from 2026–2034. Growth is driven by expanding mRNA applications in oncology, rare diseases, and personalized medicine, along with advancements in delivery technologies and increasing regulatory approvals.

Who are the major players in the mRNA Vaccine and Therapeutics Market?

PFIZER, MODERNA, BIONTECH, CSL SEQIRUS / ARCTURUS, GSK, CUREVAC, SANOFI, MERCK & CO., RECORDATI, CSL, ARCTURUS THERAPEUTICS, CRISPR THERAPEUTICS, NOVARTIS, REGENERON, MEIJI SEIKA PHARMA, Others

Which segments covered the mRNA Vaccine and Therapeutics Market?

By Product Type (mRNA Vaccines, mRNA Therapeutics), By Application (Infectious Diseases, Oncology, Rare Disease and Metabolic Disorders), By Technology Type (Conventional Non-Replicating mRNA Platforms, Self-Amplifying mRNA, Personalized and Specialty Therapeutic mRNA Platforms), By End User (Hospitals and Health Systems, Retail Pharmacies and Vaccination Clinics, Specialty Oncology Centers, Academic and Research Centers)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

mRNA Vaccine and Therapeutics Market

Published Date : 17 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date