- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Multilateral Well Technology Market Size, Share & Growth Analysis | CAGR 6.6%

Global Multilateral Well Technology Market Size, Share, Analysis By TAML Level (TAML Level 4–6 Sealed Junction Systems, TAML Level 2–3 Intermediate Junction Systems, TAML Level 1 Open Hole Laterals), By Application (Oil & Gas Exploration and Production, Geothermal Energy Exploration, Mining & Water Well Applications), By Deployment Environment (Onshore, Offshore), By Component (Completion Hardware, Engineering & Installation Services, Digital Monitoring Solutions) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 6.3 Billion, 2025 | USD 11.2 Billion, 2034 | 6.6%, 2026–2034 | North America, 47.0%, 2025 |

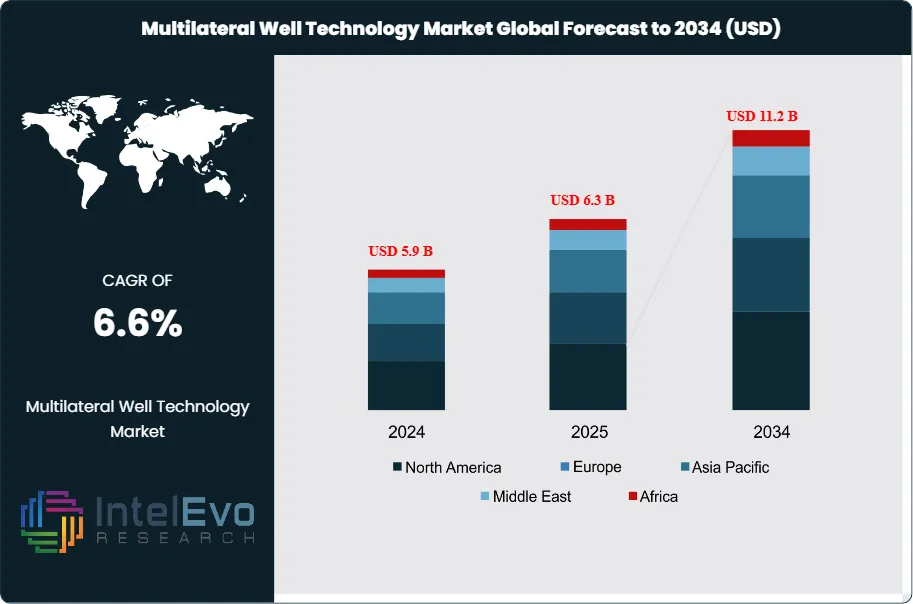

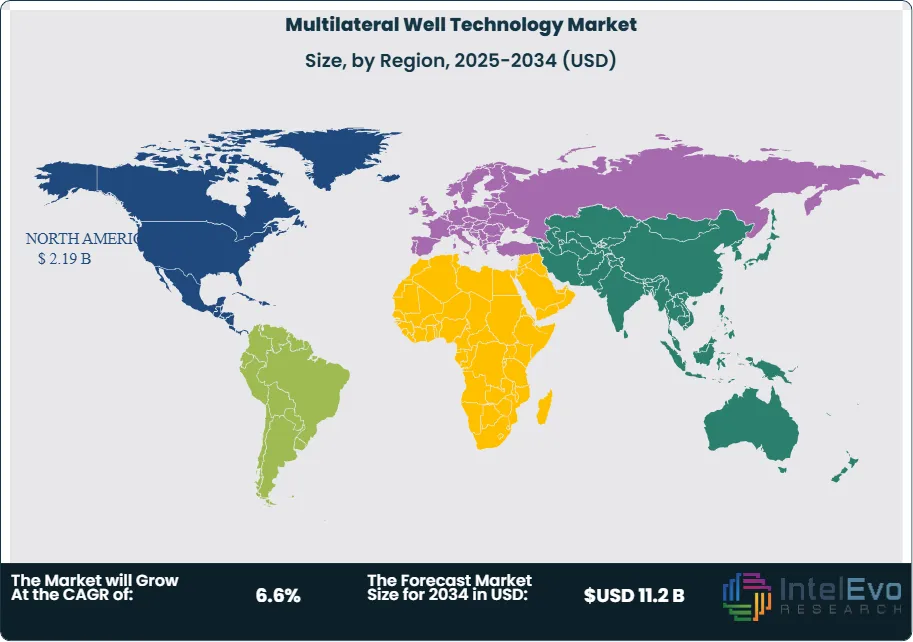

The Multilateral Well Technology Market was valued at approximately USD 5.9 Billion in 2024 and increased to USD 6.3 Billion in 2025. The market is projected to reach nearly USD 11.2 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 6.6% during the forecast period from 2026 to 2034. The multilateral well technology market encompasses the full spectrum of hardware, completion systems, engineering services, and digital management tools required to design, construct, and operate wellbores with multiple lateral branches extending from a single main wellbore. This architecture enables operators to access multiple reservoir zones, increase reservoir contact, and reduce the total number of wells required to achieve target production rates, making it one of the most capital-efficient completion strategies available in the modern oil and gas industry.

Get More Information about this report -

Request Free Sample ReportThe multilateral well technology market is shaped by the intersection of maturing conventional reservoir economics and rising exploration ambitions in unconventional and deepwater settings. As the majority of the world's largest producing fields enter production plateau or decline phases, operators face the imperative of extracting maximum value from existing well locations. Multilateral well completions address this challenge directly; industry data indicates that a single TAML Level 4 or higher multilateral completion can replace two to four individual vertical or horizontal wells, reducing total well costs by 30–45% per unit of production achieved. With global upstream capital expenditure estimated at USD 520 Billion in 2025, and an increasing proportion of that budget directed toward brownfield optimization and enhanced oil recovery programs, the multilateral well technology market is positioned to capture a growing share of the well construction and completion budget cycle.

Technology is actively redefining the multilateral well technology market structure. The integration of intelligent completion systems, encompassing fiber-optic distributed sensing, permanent downhole gauges, and autonomous inflow control valves, into multilateral wellbore architectures is creating a new category of sensor-embedded, data-rich well completions. These smart multilateral systems allow operators to monitor production from individual lateral branches in real time, enabling flow allocation decisions that were previously impossible without well intervention. Automation in lateral junction construction, guided by advanced steerable drilling assemblies and AI-assisted trajectory planning tools, is reducing installation times by an estimated 20–28% compared to conventional multilateral operations conducted just five years ago.

Regulatory forces present a dual influence on the multilateral well technology market. National energy security policies across Saudi Arabia, the UAE, Iraq, and China are actively mandating accelerated development of proven reserves, generating sustained demand for advanced completion architectures. In North America, permitting efficiency improvements and revised federal drilling regulations on public lands have contributed to a more predictable investment environment for multi-well pad programs incorporating multilateral designs. Environmental considerations are also emerging as indirect demand enablers; the ability to reduce surface footprint and aggregate well count through multilateral designs aligns with increasingly stringent land-use and emissions disclosure requirements in regulated markets.

The Asia Pacific region represents the most significant growth hotspot within the multilateral well technology market forecast period, driven by China's state-directed increase in domestic hydrocarbon output and India's accelerated appraisal of deep sedimentary basins. The Middle East retains the highest absolute expenditure concentration, with national oil companies committing to multi-year multilateral drilling programs across prolific carbonate reservoirs. As the multilateral well technology market expands from USD 6.3 Billion in 2025 toward USD 11.2 Billion by 2034, the competitive dynamics will increasingly reward vendors that combine hardware excellence with digital reservoir management capabilities.

, By Application (Oil & Gas Exploration and Production, Geothermal Energy Exploration, Mining & Water Well Applications), By Deployment Environment (Onshore, Offshore), By Component (Completion Hardware, Engineering & Installation Services, Digital Monitoring Solutions) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The Global Multilateral Well Technology Market was valued at USD 6.3 Billion in 2025 and is projected to reach USD 11.2 Billion by 2034, registering a CAGR of 6.6% across the forecast period 2026–2034.

- Segment Dominance (By TAML Level): TAML Level 4–6 systems held the dominant share at approximately 54.3% of the multilateral well technology market revenue in 2025, driven by growing operator preference for fully sealed, re-accessible lateral junctions in complex reservoir environments.

- Segment Dominance (By Application): The oil and gas exploration and production application segment accounted for the largest share at approximately 82.6% of the multilateral well technology market in 2025, reflecting the technology's near-exclusive adoption within upstream hydrocarbon recovery programs.

- Driver: Rising global demand for enhanced oil recovery and brownfield optimization, supported by upstream E&P capital expenditure of USD 520 Billion in 2025, is the primary growth driver, directly funding multilateral completion programs that replace multiple single-bore wells at 30–45% lower per-barrel development cost.

- Restraint: High upfront capital requirements for advanced TAML Level 4–6 systems, averaging USD 3.5–7.0 Million per multilateral completion versus USD 1.5–2.5 Million for a conventional horizontal well, restrict adoption among independent operators with constrained balance sheets.

- Opportunity: The deployment of intelligent multilateral completions integrating real-time downhole sensing and autonomous inflow control in deepwater and HPHT environments represents an addressable technology upgrade market estimated at USD 2.1 Billion by 2034, growing from approximately USD 870 Million in 2025.

- Trend: Smart and intelligent multilateral completion systems, embedding fiber-optic sensing and autonomous flow control, accounted for approximately 28% of all new multilateral well installations in 2025 and are projected to reach 52% of installations by 2034.

- Regional Analysis: North America led the multilateral well technology market with a 34.8% share and USD 2.19 Billion in revenue in 2025, driven by high-density shale pad drilling programs and brownfield recompletion activity in the Permian Basin, Eagle Ford, and Gulf of Mexico deepwater blocks.

Competitive Summary

The multilateral well technology market is moderately consolidated. The top four players, SLB, Baker Hughes, Halliburton, and Weatherford International, collectively held approximately 62% of total market revenue in 2025. Competition is primarily technology-driven, with differentiation based on TAML-level capability, junction re-entry reliability, and integrated digital production management. Competitive intensity rose materially during 2024–2026, with SLB and Baker Hughes both announcing next-generation intelligent junction platforms and expanding their Middle East service footprints through strategic operator partnerships.

Competitive Landscape Matrix

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| SLB (Schlumberger) | USA | Leader | SURE SELECT Intelligent System | North America, Middle East | Expanded contract with Saudi Aramco for 120 wells (Mar 2025) |

| Baker Hughes | USA | Leader | MultiNode Intelligent Platform | North America, Global | Launched digital-twin-enabled management system (Feb 2025) |

| Halliburton | USA | Challenger | AccessFlex Completion System | North America, Middle East | Awarded USD 280M contract with ADNOC (May 2025) |

| Weatherford International | Ireland | Challenger | MaxTRACK Junction System | Europe, North America | Introduced AI-assisted junction placement monitoring (Jan 2026) |

| National Oilwell Varco | USA | Challenger | Cerberus Multilateral System | North America | Expanded rental fleet by 35% for Permian Basin (Apr 2025) |

| GWDC | China | Niche Player | ML-II Junction Assembly | Asia Pacific | Secured contract across Sichuan Basin deep gas program (Jun 2025) |

| SPT Energy Group | China | Niche Player | SPT-ML Completion String | Asia Pacific | Expanded services into Central Asia via Uzbekneftegaz (Sep 2025) |

| Tendeka | UK | Niche Player | PulseEight Autonomous ICV | Europe, MEA | Partnered with Equinor for North Sea multilateral wells (Dec 2024) |

| Packers Plus Energy | Canada | Niche Player | StackFRAC HD System | North America | Released upgraded StackFRAC HD-X platform (Mar 2026) |

By TAML Level

The Technology Advancement of Multilaterals (TAML) classification system defines the technical complexity and mechanical integrity of lateral junctions, and it serves as the primary segmentation architecture for the multilateral well technology market. TAML Level 4–6 systems dominated market revenue with a combined share of 54.3%, equivalent to USD 3.42 Billion in 2025. These advanced-level systems provide hydraulically sealed junctions with full pressure integrity, enabling operators to access, re-enter, and selectively produce individual lateral branches under wellbore pressure conditions. Level 4 systems, which offer mechanical sealing between the main bore and lateral branches, are the most widely adopted within this tier, particularly in Middle Eastern carbonate reservoirs and North Sea brownfield applications where well integrity requirements are stringent. Level 5 and 6 systems, providing pressure-tight junctions with full zonal control capability, are increasingly specified for HPHT offshore wells and deep onshore gas reservoirs. Key technology providers including SLB and Baker Hughes compete primarily at this tier, where proprietary junction design and installation tooling create high switching costs for operator clients.

TAML Level 2–3 systems captured approximately 30.4% of the multilateral well technology market at USD 1.92 Billion in 2025. These intermediate-complexity systems provide openhole or cased-hole lateral junctions without full pressure isolation between the main bore and the lateral, making them appropriate for applications where zonal isolation is less critical, such as coal bed methane production, tight sandstone appraisal, and shallow onshore gas wells. Demand concentrates in Asia Pacific, Latin America, and parts of Africa where cost sensitivity and reservoir characteristics favor simpler junction architectures. Halliburton and National Oilwell Varco hold strong positions in this segment, offering competitive pricing on rental equipment and field service packages. TAML Level 1 systems, representing the most basic openhole lateral configuration without a formal junction, accounted for the remaining 13.8% of market revenue at USD 871 Million in 2025, primarily serving frontier exploration programs and cost-constrained onshore operators.

By Application

The oil and gas exploration and production application segment commanded 82.6% of the multilateral well technology market at USD 5.20 Billion in 2025. Within this dominant segment, brownfield optimization and enhanced oil recovery programs account for the largest share of multilateral completion activity, as operators seek to extend the productive life of existing reservoirs without the capital requirements of new-field development. Onshore carbonate reservoir programs in Saudi Arabia, the UAE, and Iraq generate the highest concentration of TAML Level 4–6 deployments globally. Offshore deepwater programs, particularly in Brazil's pre-salt basins and the Gulf of Mexico, drive premium multilateral system demand given the high per-well development cost environment where maximizing reservoir contact per wellbore delivers the greatest economic return. Unconventional resource programs in North America, covering shale oil and gas plays in the Permian and Marcellus basins, represent the fastest-growing sub-segment within oil and gas applications, with multilateral horizontal designs increasingly replacing stacked single-lateral wells on multi-pad drilling programs.

Geothermal energy exploration represented approximately 9.8% of the multilateral well technology market at USD 617 Million in 2025. Geothermal developers are adopting multilateral well architectures to maximize heat extraction contact within permeable geothermal reservoirs, reducing the number of production wells required per megawatt of installed capacity. This application is particularly active in the United States, Iceland, Indonesia, and Kenya, where government incentives for renewable energy development are accelerating geothermal project pipelines. Mining and water well applications collectively accounted for the remaining 7.6% of the multilateral well technology market at USD 479 Million in 2025, covering underground mine ventilation, in-situ leach mining, and horizontal directional drilling for aquifer management programs.

By Deployment Environment

Onshore deployment dominated the multilateral well technology market with a 61.4% share at USD 3.87 Billion in 2025. Onshore multilateral programs benefit from lower mobilization costs, established service infrastructure, and the technical maturity of land drilling rigs equipped for complex multilateral operations. The Middle East, North America, and Russia represent the three largest onshore multilateral markets, where carbonate and tight sandstone reservoirs are well-suited to multilateral architectures. National oil companies in Saudi Arabia and the UAE have standardized TAML Level 4 multilateral designs into their carbonate field development plans, creating predictable long-term procurement demand for junction hardware and installation services.

Offshore deployment captured 38.6% of the multilateral well technology market at USD 2.43 Billion in 2025. The offshore segment carries a structural premium over onshore applications due to the higher per-unit cost of deepwater completion equipment, the technical challenges of installing multilateral junctions in subsea wellheads, and the critical importance of junction integrity under high hydrostatic pressures. Deepwater markets in Brazil, the Gulf of Mexico, the North Sea, and West Africa drive offshore multilateral demand. SLB and Baker Hughes collectively account for approximately 74% of the offshore multilateral completion services market, reflecting the capital-intensive nature of subsea intervention capability and the barriers to entry created by proprietary deepwater junction tooling systems.

By Component

Completion hardware, encompassing lateral junction assemblies, deflection tools, liner hangers, and packers, represented the largest component segment at 46.2% of the multilateral well technology market, equating to USD 2.91 Billion in 2025. Hardware quality directly determines junction integrity and the ability to re-enter lateral branches throughout the producing life of the well, making it the primary capital expenditure item in any multilateral program. Engineering and installation services captured 35.8% of the market at USD 2.25 Billion in 2025, reflecting the specialist crew time, directional drilling expertise, and wellsite supervision required for complex multilateral construction. Digital management and monitoring solutions, including real-time downhole data platforms, production allocation software, and AI-assisted reservoir management systems, represented the fastest-growing component at 18.0% of the market and USD 1.13 Billion in 2025, with adoption accelerating as operators seek data-driven production management across multi-lateral well portfolios.

Regional Analysis

North America Multilateral Well Technology Market

North America held the largest regional share of the global multilateral well technology market at 34.8%, representing USD 2.19 Billion in 2025. The United States accounts for approximately 87% of North American market revenue, driven by the scale and technical maturity of unconventional resource development in the Permian Basin, Eagle Ford, Marcellus, and Haynesville shale plays. Major operators including ExxonMobil, Chevron, and ConocoPhillips have integrated multilateral horizontal designs into their multi-pad drilling programs, achieving 20–30% reductions in surface land requirements and measurable improvements in per-foot hydrocarbon recovery rates. Deepwater Gulf of Mexico programs add incremental offshore multilateral demand, particularly for TAML Level 5 and 6 systems deployed in subsea completions at water depths exceeding 1,500 meters. Canada contributes approximately 10% of North American multilateral revenue, primarily from oil sands thermal wells in Alberta where multilateral steam-assisted gravity drainage (SAGD) configurations improve steam injection efficiency in heterogeneous reservoir intervals. Mexico's Pemex is increasing multilateral deployment in the Sureste Basin as part of its mature field revitalization program, adding incremental demand for mid-complexity TAML Level 3–4 systems. The North American competitive environment is the most technically advanced globally, with all four market leaders maintaining full multilateral technology suites, training centers, and rental tool fleets in the region.

Europe Multilateral Well Technology Market

Europe represented 17.6% of the multilateral well technology market at USD 1.11 Billion in 2025. The United Kingdom is the dominant European market, where North Sea operators are applying multilateral technology to extend the productive life of mature fields and reduce the cost of reservoir access in an environment of rising decommissioning timelines and complex subsea infrastructure. Norway's Equinor is one of the most technically advanced multilateral completion operators globally, having deployed autonomous inflow control systems in multilateral wellbores across Statfjord, Gullfaks, and Oseberg field extensions. Germany contributes through geothermal multilateral exploration programs and subsurface research institutions that advance junction technology for high-temperature formations. The Netherlands hosts major service company engineering centers that support European offshore multilateral operations. EU carbon storage policy is creating an emerging application for multilateral well technology in carbon capture and storage site characterization, where multiple lateral branches allow simultaneous monitoring of different stratigraphic intervals within a single injection or monitoring well. European demand for multilateral well technology is expected to grow steadily through 2034, supported by brownfield maximization imperatives and emerging geothermal and CCS application pathways.

Asia Pacific Multilateral Well Technology Market

Asia Pacific accounted for 24.3% of the multilateral well technology market at USD 1.53 Billion in 2025, positioning it as the fastest-growing region across the forecast period. China is the dominant country market within the region, with CNOOC, CNPC, and Sinopec operating multilateral drilling programs in the Tarim Basin, Sichuan Basin, and South China Sea that collectively represent one of the largest state-directed multilateral deployment programs globally. GWDC and SPT Energy Group serve as the primary domestic multilateral well technology providers in China, supplying junction hardware and installation services to national oil companies at competitive price points that international majors struggle to match on high-volume standard programs. India represents the fastest-growing single country market within Asia Pacific; ONGC and Oil India are incorporating multilateral designs into their deep-basin exploration programs as part of the Directorate General of Hydrocarbons' mandate to increase domestic hydrocarbon production. Australia's offshore oil and gas sector, centered on the North West Shelf and Browse Basin, drives demand for deepwater multilateral completions, with Woodside Energy and Santos deploying advanced subsea completion systems. Government energy security programs across Southeast Asia, particularly in Indonesia and Vietnam, are accelerating multilateral well adoption in mature offshore fields as national companies seek production maintenance strategies without full field redevelopment capital.

Latin America Multilateral Well Technology Market

Latin America captured 13.2% of the global multilateral well technology market at USD 832 Million in 2025. Brazil is the region's primary multilateral market, with Petrobras deploying advanced TAML Level 5 and 6 multilateral completion systems in the ultra-deepwater pre-salt Santos and Campos Basin blocks where reservoir complexity and development cost economics strongly favor multi-branch wellbore architectures over single-bore alternatives. Each pre-salt multilateral well in Brazil can cost USD 80–120 Million to complete but replaces three to five separate wells that would collectively cost substantially more, making the economic case for multilateral technology compelling despite the high absolute capital requirement. Argentina's Vaca Muerta shale formation represents a significant growth opportunity for land-based multilateral technology, as YPF and its international partners explore multi-lateral horizontal designs for tight formation development. Colombia and Ecuador contribute smaller volumes of multilateral activity, primarily in mature onshore fields where secondary recovery programs include multilateral re-entry and sidetracking operations. The region's overall growth trajectory in the multilateral well technology market is anchored to Brazil's offshore investment program and the gradual scaling of Argentine unconventional development.

Middle East and Africa Multilateral Well Technology Market

The Middle East and Africa region represented 10.1% of the multilateral well technology market at USD 636 Million in 2025, with the highest absolute concentration of TAML Level 4–6 deployments globally relative to total well count. Saudi Aramco is the single largest individual operator client for multilateral well technology globally, deploying hundreds of multilateral completions per year across its giant Ghawar, Safaniya, and Marjan fields as part of a systematic strategy to maximize ultimate recovery from prolific carbonate reservoirs without disproportionate surface facility expansion. ADNOC in the UAE is similarly committed to multilateral technology across its onshore and offshore carbonate fields, having awarded a multi-year multilateral services contract to Halliburton valued at USD 280 Million in 2025 for operations across Abu Dhabi's onshore concessions. Iraq's national oil company and the Kuwait Oil Company are expanding multilateral programs in their southern field development programs. In Africa, Angola and Nigeria drive offshore multilateral demand through deepwater block development in the Lower Congo and Niger Delta basins, with international oil companies including Shell, TotalEnergies, and bp deploying advanced subsea multilateral completions in water depths exceeding 1,200 meters. The region's strategic importance to the multilateral well technology market will increase through 2034 as national oil companies formalize long-term field development plans that systematically embed multilateral designs into carbonate reservoir recovery strategies.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By TAML Level

- TAML Level 4–6 (Sealed Junction Systems)

- TAML Level 2–3 (Intermediate Junction Systems)

- TAML Level 1 (Open Hole Lateral)

By Application

- Oil and Gas Exploration and Production

- Geothermal Energy Exploration

- Mining and Water Well Applications

By Deployment Environment

- Onshore

- Offshore

By Component

- Completion Hardware (Junction Assemblies, Deflection Tools, Liner Hangers, Packers)

- Engineering and Installation Services

- Digital Management and Monitoring Solutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 6.3 B |

| Forecast Revenue (2034) | USD 11.2 B |

| CAGR (2025-2034) | 6.6% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By TAML Level (TAML Level 4–6 (Sealed Junction Systems), TAML Level 2–3 (Intermediate Junction Systems), TAML Level 1 (Open Hole Lateral)), By Application (Oil and Gas Exploration and Production, Geothermal Energy Exploration, Mining and Water Well Applications), By Deployment Environment (Onshore, Offshore), By Component (Completion Hardware (Junction Assemblies, Deflection Tools, Liner Hangers, Packers), Engineering and Installation Services, Digital Management and Monitoring Solutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | SLB (SCHLUMBERGER), BAKER HUGHES, HALLIBURTON, WEATHERFORD INTERNATIONAL, NATIONAL OILWELL VARCO (NOV), GWDC (GREAT WALL DRILLING COMPANY), SPT ENERGY GROUP, TENDEKA, PACKERS PLUS ENERGY SERVICES, PETROFAC LIMITED, CALFRAC WELL SERVICES, ARCHROCK INC., SAIPEM S.P.A., EXALO DRILLING S.A., ZAMAM OFFSHORE SERVICES LIMITED, C&J ENERGY SERVICES, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Oil & Gas Exploration and Production, Geothermal Energy Exploration, Mining & Water Well Applications), By Deployment Environment (Onshore, Offshore), By Component (Completion Hardware, Engineering & Installation Services, Digital Monitoring Solutions) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034")

, By Application (Oil & Gas Exploration and Production, Geothermal Energy Exploration, Mining & Water Well Applications), By Deployment Environment (Onshore, Offshore), By Component (Completion Hardware, Engineering & Installation Services, Digital Monitoring Solutions) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034")

, By Application (Oil & Gas Exploration and Production, Geothermal Energy Exploration, Mining & Water Well Applications), By Deployment Environment (Onshore, Offshore), By Component (Completion Hardware, Engineering & Installation Services, Digital Monitoring Solutions) Industry Region & Key Players – Market Dynamics, Competitive Strategies, Technology Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Multilateral Well Technology Market?

The Global Multilateral Well Technology Market was valued at USD 6.3 Billion in 2025, projected to reach USD 11.2 Billion by 2034 at a CAGR of 6.6% from 2026–2034. Growth is driven by rising demand for enhanced reservoir recovery, cost-efficient drilling, and increasing adoption of advanced multilateral well technologies in offshore and unconventional fields.

Who are the major players in the Multilateral Well Technology Market?

SLB (SCHLUMBERGER), BAKER HUGHES, HALLIBURTON, WEATHERFORD INTERNATIONAL, NATIONAL OILWELL VARCO (NOV), GWDC (GREAT WALL DRILLING COMPANY), SPT ENERGY GROUP, TENDEKA, PACKERS PLUS ENERGY SERVICES, PETROFAC LIMITED, CALFRAC WELL SERVICES, ARCHROCK INC., SAIPEM S.P.A., EXALO DRILLING S.A., ZAMAM OFFSHORE SERVICES LIMITED, C&J ENERGY SERVICES, Others

Which segments covered the Multilateral Well Technology Market?

By TAML Level (TAML Level 4–6 (Sealed Junction Systems), TAML Level 2–3 (Intermediate Junction Systems), TAML Level 1 (Open Hole Lateral)), By Application (Oil and Gas Exploration and Production, Geothermal Energy Exploration, Mining and Water Well Applications), By Deployment Environment (Onshore, Offshore), By Component (Completion Hardware (Junction Assemblies, Deflection Tools, Liner Hangers, Packers), Engineering and Installation Services, Digital Management and Monitoring Solutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Multilateral Well Technology Market

Published Date : 17 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date