- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Multiple Unit Pellet Systems Market Size, Share & Forecast | CAGR 3.3%

Global Multiple Unit Pellet Systems Market Size, Share, Analysis By Dosage Form (Capsules, Tablets, Sachets, Others), By Formulation (Extended Release, Delayed Release, Orodispersible Systems), By Drug Class (Proton Pump Inhibitors, Anti-Hypertensive, Antibiotics, Analgesics), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Drug Stores, Online), Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 3.8 Billion | USD 5.1 Billion | 3.3% | North America, 36.9% |

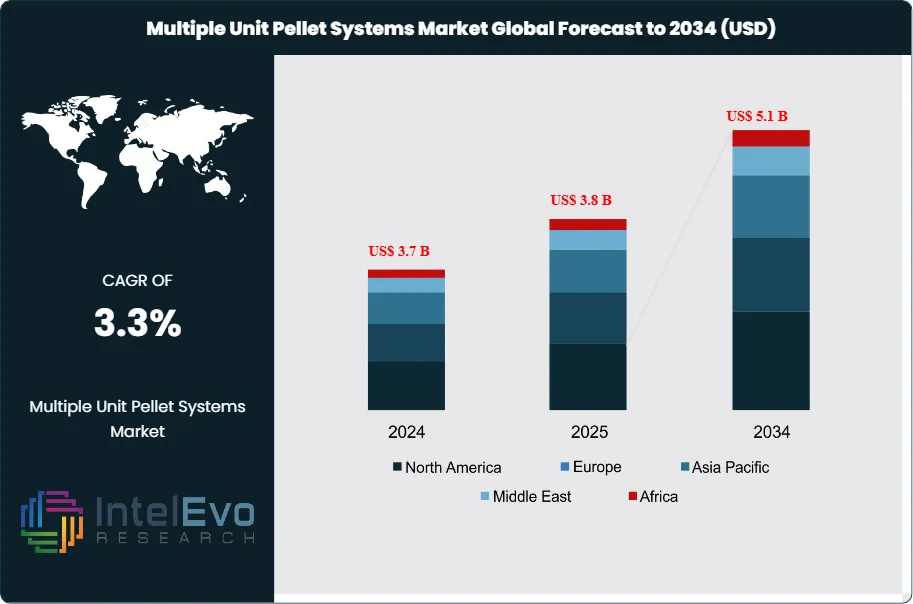

The Multiple Unit Pellet Systems Market is estimated at US$ 3.7 Billion in 2024 and is on track to reach roughly US$ 5.1 Billion by 2034, The market is further estimated to reach approximately US$ 3.8 Billion in 2025, and is expected to expand at a compound annual growth rate (CAGR) of around 3.3% during the forecast period from 2026 to 2034. Growth is driven by increasing demand for controlled-release drug delivery systems, rising adoption of multi-unit pellet technologies in pharmaceutical formulations, and growing focus on patient-centric dosage forms. Additionally, advancements in pellet coating technologies and expansion of generic drug manufacturing are further supporting market growth globally.

Get More Information about this report -

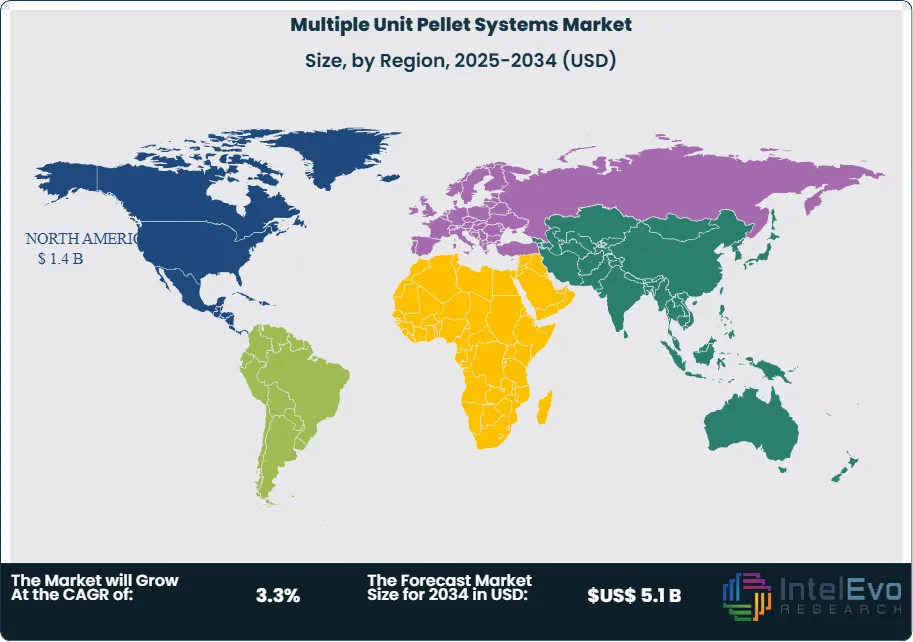

Request Free Sample ReportNorth America leads demand, holding 36.9% share in 2024 and generating about US$ 1.4 Billion in revenue, supported by high prescription volumes for chronic therapies and strong uptake of differentiated generics.

Demand is anchored in patient-centric modified-release oral solids that deliver consistent exposure while reducing variability tied to gastric emptying and transit time. MUPS designs support proton pump inhibitor tablets that disintegrate into pellets for sustained acid control in reflux disease, and they enable once-daily cardiovascular regimens built on extended-release beta-blocker pellets. Enteric-coated NSAID pellets lower gastric irritation while maintaining duration of action, and layered pellet architectures support combination products that separate actives with different release needs. The September 30, 2025 quarter highlighted the commercial pull of such platforms, as Dr. Reddy’s Laboratories reported about US$ 1.06 Billion in global generics revenue within total quarterly revenue near US$ 1.2 Billion, up 10% year over year, reflecting rising contribution from modified-release franchises.

On the supply side, competition centers on scale, coating know-how, and manufacturability at high tableting speeds. Firms invest in extrusion-spheronization capacity, fluid-bed coating lines, and specialty excipients that cushion pellets during compression and protect functional films. Regulatory expectations from FDA and EMA push tighter dissolution specifications, bioequivalence evidence for multiparticulates, and process controls aligned with Quality by Design. This raises barriers for smaller formulators and increases reliance on CDMOs with validated coating and compression toolkits. Key risks include coating rupture during compaction, batch-to-batch variability in pellet size distribution, polymer supply tightness, and patent disputes around reference modified-release products.

Technology is shifting operating models. Automated inspection, in-line spectroscopy, and real-time process analytical technology improve pellet integrity monitoring and shorten deviation investigations. Machine-learning models are being applied to predict coating thickness drift, optimize spray rates, and reduce scrap in high-drug-load pellets. Europe is estimated to hold about 28% share in 2024, while Asia-Pacific is near 24% and is expected to gain share as India and China expand modified-release generics investment and add high-throughput coating capacity. Emerging hotspots include India’s export-focused generics clusters and select Southeast Asian CDMO hubs building multiparticulate suites for orodispersible and fixed-dose combination MUPS programs.

, By Formulation (Extended Release, Delayed Release, Orodispersible Systems), By Drug Class (Proton Pump Inhibitors, Anti-Hypertensive, Antibiotics, Analgesics), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Drug Stores, Online), Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The market generates 3.7 billion USD, 2024 and grows at 3.3%, 2026-2034 to reach 5.1 billion USD, 2034.

- Segment Dominance: Capsules lead the dosage form segment at 48.7%, 2024.

- Segment Dominance: Extended-release formulations lead at 44.6%, 2024, while proton pump inhibitors lead the drug class mix at 41.9%, 2024.

- Driver: Manufacturers scale modified-release adoption to support chronic therapy demand, estimated: 1.9 billion USD, 2024.

- Restraint: Complex pellet coating and compression controls raise development and validation costs, estimated: 0.3 billion USD, 2024.

- Opportunity: Hospital pharmacies anchor distribution at 46.3%, 2024, and firms expand fixed-dose and patient-friendly formats, estimated: 0.7 billion USD, 2024.

- Trend: Developers accelerate platform standardization across programs to improve time-to-market, estimated: 3.0 years, 2024.

- Regional Analysis: North America leads with 36.9%, 2024, supported by strong modified-release uptake, estimated: 1.4 billion USD, 2024.

Competitive Landscape

The Global Multiple Unit Pellet Systems (MUPS) Market is moderately consolidated, with the top five pharmaceutical manufacturers and CDMOs accounting for an estimated 40.0%–47.0% of 2025 market revenue. Competition is formulation-driven and capability-based, where expertise in pelletization, coating technologies, controlled-release systems, and regulatory compliance shapes market share more than pricing. Competitive intensity increased in 2025–2026 as companies expanded modified-release portfolios, invested in advanced oral solid dosage infrastructure, and formed partnerships for complex generics and specialty drugs.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Strategic Move |

| ASTRAZENECA | UK | Leader | MUPS-based drug formulations (e.g., Nexium) | Europe, North America, Global | Continued lifecycle management of MUPS-based therapies and expansion in emerging markets in 2025. |

| PFIZER | US | Leader | Controlled-release and pellet-based oral drug formulations | North America, Global | Expanded oral solid dosage capabilities and CDMO partnerships in 2025. |

| NOVARTIS | Switzerland | Leader | Advanced drug delivery systems including multiparticulates | Europe, North America | Strengthened complex generics and specialty medicines portfolio in 2025. |

| LONZA GROUP | Switzerland | Leader | CDMO services for pelletization and drug delivery systems | Europe, North America, Asia | Expanded oral solid dosage manufacturing capacity in 2025. |

| EVONIK INDUSTRIES | Germany | Leader | Functional excipients and drug delivery technologies for MUPS | Europe, Global | Advanced EUDRAGIT polymer technologies for controlled release in 2025. |

| RECIPHARM | Sweden | Challenger | CDMO specializing in oral solid dosage and pellet systems | Europe, Global | Expanded manufacturing footprint and CDMO services in 2025. |

| CATALENT | US | Challenger | Advanced delivery technologies including multiparticulate systems | North America, Europe | Strengthened oral technologies and CDMO service offerings in 2025. |

| ACG WORLDWIDE | India | Challenger | Capsule systems, pelletization equipment, and manufacturing solutions | Asia-Pacific, Global | Expanded integrated manufacturing and equipment solutions in 2025. |

| ROQUETTE | France | Niche Player | Pharmaceutical excipients for pellet formulations | Europe, North America | Focused on functional excipients and oral dosage innovation in 2025. |

| COLORCON | UK | Niche Player | Coating systems and controlled-release technologies | Global | Expanded polymer coating solutions for modified-release formulations in 2025. |

Summary Insight:

The market is evolving toward advanced controlled-release formulations and CDMO-led manufacturing ecosystems. Companies with strong formulation expertise, regulatory capabilities, and scalable pelletization infrastructure are gaining share, while smaller players compete through niche technologies and regional manufacturing advantages. Strategic partnerships and complex generics development are expected to define competitive positioning through 2034.

By Dosage Form

Capsules remain the dominant dosage form within the Multiple Unit Pellet Systems market and account for 48.7% of total share as of the latest assessment. Their leadership is driven by strong compatibility with pellet filling processes and consistent dose uniformity across multiparticulate formulations. Capsule shells protect coated pellets from compression stress, preserving release integrity and supporting predictable in vivo performance. Patient preference for ease of swallowing continues to reinforce demand, particularly in long-term therapies.

Manufacturers rely on capsules to combine multiple pellet populations within a single unit, enabling complex release patterns such as blended immediate and sustained delivery. This design flexibility supports product differentiation and lifecycle management strategies for branded and generic portfolios. High-speed encapsulation lines allow efficient commercial-scale output, lowering per-unit manufacturing costs while maintaining quality consistency.

Regulatory familiarity with capsule-based modified-release products further strengthens adoption. Approval pathways for pellet-filled capsules are well established across major agencies, reducing development timelines. As chronic disease prescriptions rise across gastrointestinal, cardiovascular, and central nervous system indications, capsule-based MUPS formats are expected to retain structural dominance through 2030 and beyond.

By Application

Extended-release formulations represent the largest application area and account for 44.6% of market share. Demand is closely tied to chronic disease management, where stable plasma concentration and reduced dosing frequency remain primary clinical objectives. Pellet-based extended-release systems provide controlled dissolution profiles that lower peak-to-trough variability and improve safety margins.

Healthcare providers increasingly favor once-daily extended-release regimens to support adherence and minimize treatment interruptions. Pharmaceutical companies continue to convert immediate-release products into extended-release MUPS to extend market relevance and protect revenues post-patent expiry. Blended pellet architectures allow fine adjustment of release kinetics across therapeutic windows.

Clinical acceptance remains high due to consistent symptom control and reduced adverse events. Hospital formularies and outpatient protocols increasingly specify extended-release variants for hypertension, gastroesophageal reflux disease, and neurological disorders. This segment is expected to expand steadily in parallel with global growth in chronic disease prevalence.

By End-Use

Hospital pharmacies represent the leading end-use channel with a 46.3% revenue share. Hospitals act as primary initiation points for modified-release therapies, particularly for patients transitioning between inpatient and outpatient care. Clinical oversight, structured monitoring, and pharmacist-led counseling support early adoption of MUPS-based medicines.

Institutional purchasing frameworks favor formulations that demonstrate safety, adherence benefits, and predictable pharmacokinetics. Hospitals also manage high volumes of polypharmacy patients, where pellet-based combinations simplify dosing schedules and reduce medication burden. Integration with electronic prescribing systems further supports standardized utilization.

As specialty therapies and extended-release regimens expand, hospital pharmacies are expected to maintain a central role in distribution. Their influence extends into protocol development, physician education, and post-market evaluation, reinforcing long-term leadership within the channel mix.

By Region

North America leads the global Multiple Unit Pellet Systems market with a 36.9% share. Strong uptake reflects widespread use of sustained-release therapies for gastrointestinal and cardiovascular conditions, alongside regulatory support for complex generics. Manufacturers actively reformulate established molecules using pellet technologies to achieve differentiated pharmacokinetic profiles and secure competitive positioning.

Demographic aging has increased demand for taste-masked and easy-to-administer multiparticulate formulations in pediatric and geriatric care. Clinical guidelines increasingly incorporate pellet-based combinations to address adherence and polypharmacy risks. Manufacturing investments emphasize quality-by-design frameworks and validated spheronization processes. In 2024, the U.S. Center for Drug Evaluation and Research approved 50 novel medicines, reinforcing a robust regulatory environment.

Asia Pacific is projected to record the fastest growth rate through the forecast horizon. Rising chronic disease incidence, expanding domestic pharmaceutical production, and government-backed manufacturing incentives are key drivers. Regional firms focus on cost-effective sustained-release generics adapted for climatic stability and export compliance. With noncommunicable diseases accounting for more than 81% of deaths in upper-middle-income Asia-Pacific economies, demand for pellet-based modified-release therapies is expected to accelerate significantly.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Dosage Form

- Capsules

- Tablets

- Sachets

- Others

By Formulation

- Extended Release Dosage Form

- Delayed Release Orodispersible Dosage Form

- Delayed Release Dosage Form

- Other

By Drug Class

- Proton Pump Inhibitors

- Anti-Hypertensive

- Antibiotics

- Analgesics

- Others

By Distribution Channel

- Hospital Pharmacies

- Drug Stores

- Retail Pharmacies

- Online Pharmacies

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | US$ 3.8 B |

| Forecast Revenue (2034) | US$ 5.1 B |

| CAGR (2025-2034) | 3.3% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Dosage Form, (Capsules, Tablets, Sachets, Others), By Formulation, (Extended Release Dosage Form, Delayed Release Orodispersible Dosage Form, Delayed Release Dosage Form, Other), By Drug Class, (Proton Pump Inhibitors, Anti-Hypertensive, Antibiotics, Analgesics, Others), By Distribution Channel, (Hospital Pharmacies, Drug Stores, Retail Pharmacies, Online Pharmacies) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Galderma SA, Pfizer Inc., Cipla Ltd., Merck KGaA, Astellas Pharma Inc., Perrigo Company Plc, Novartis AG, Johnson & Johnson Services, Inc., AstraZeneca PLC, GlaxoSmithKline PLC |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Formulation (Extended Release, Delayed Release, Orodispersible Systems), By Drug Class (Proton Pump Inhibitors, Anti-Hypertensive, Antibiotics, Analgesics), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Drug Stores, Online), Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034")

, By Formulation (Extended Release, Delayed Release, Orodispersible Systems), By Drug Class (Proton Pump Inhibitors, Anti-Hypertensive, Antibiotics, Analgesics), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Drug Stores, Online), Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034")

, By Formulation (Extended Release, Delayed Release, Orodispersible Systems), By Drug Class (Proton Pump Inhibitors, Anti-Hypertensive, Antibiotics, Analgesics), By Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Drug Stores, Online), Industry Overview, Market Dynamics, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Multiple Unit Pellet Systems Market?

The Global Multiple Unit Pellet Systems Market was valued at US$ 3.8 Billion in 2025, projected to hit US$ 5.1 Billion by 2034, growing at a CAGR of 3.3% from 2026–2034, driven by demand for controlled-release drug delivery and advanced pharmaceutical formulations.

Who are the major players in the Multiple Unit Pellet Systems Market?

Galderma SA, Pfizer Inc., Cipla Ltd., Merck KGaA, Astellas Pharma Inc., Perrigo Company Plc, Novartis AG, Johnson & Johnson Services, Inc., AstraZeneca PLC, GlaxoSmithKline PLC

Which segments covered the Multiple Unit Pellet Systems Market?

By Dosage Form, (Capsules, Tablets, Sachets, Others), By Formulation, (Extended Release Dosage Form, Delayed Release Orodispersible Dosage Form, Delayed Release Dosage Form, Other), By Drug Class, (Proton Pump Inhibitors, Anti-Hypertensive, Antibiotics, Analgesics, Others), By Distribution Channel, (Hospital Pharmacies, Drug Stores, Retail Pharmacies, Online Pharmacies)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Multiple Unit Pellet Systems Market

Published Date : 26 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date