- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Muscle Pain Treatment Market Size & Forecast 2034 | CAGR 8.12%

Global Muscle Pain Treatment Market Size, Share, Analysis By Type of Treatment (Pharmacological – Analgesics, Muscle Relaxants, Topical NSAIDs; Non-Pharmacological – Physical Therapy, Acupuncture, Massage, Heat & Cold Therapy), By Cause (Overuse, Injury, Inflammatory & Neurological Conditions), By Pain Type (Acute, Chronic), By Distribution Channel (Hospital, Retail & Online Pharmacies) – Industry Trends & Forecast 2025–2034

Report Overview

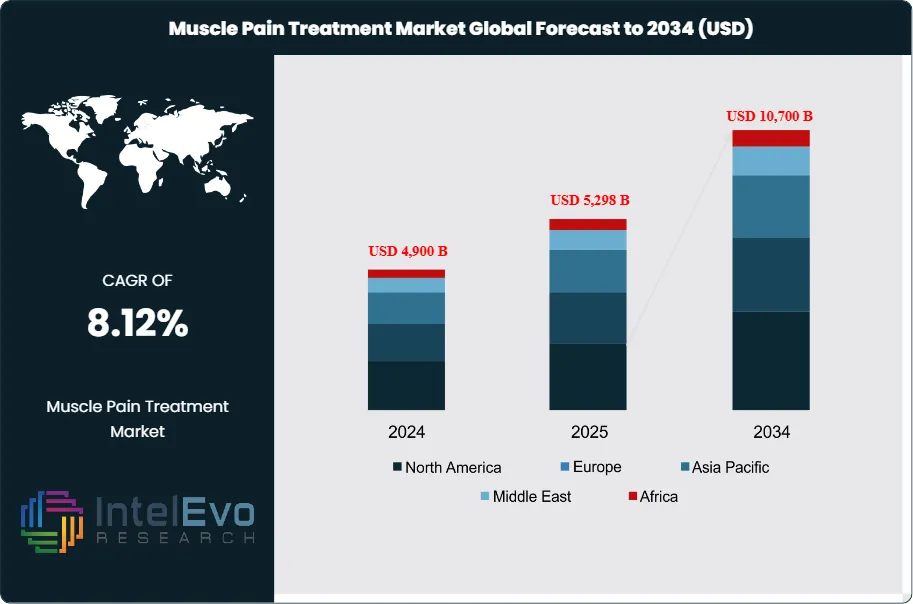

The Muscle Pain Treatment Market was valued at approximately USD 4,900 million in 2024 and is projected to reach nearly USD 10,700 million by 2034, reflecting sustained expansion driven by rising musculoskeletal disorders and growing demand for non-opioid pain management therapies. Based on the projected growth trajectory, the market size for 2025 is estimated at around USD 5,298 million. Beginning in 2026, the market is expected to grow at a compound annual growth rate (CAGR) of about 8.12% from 2026 to 2034, ultimately reaching an estimated valuation of approximately USD 10,700 million by 2034.

Get More Information about this report -

Request Free Sample ReportMuscle pain affects nearly the entire population at some point in life, and rising diagnosis rates, longer life expectancy, and higher physical activity participation drive steady demand for both prescription and over-the-counter therapies. Recurrent pain linked to aging populations, sedentary work styles, and sports injuries sustains a large chronic user base and supports stable revenue streams for pharmaceutical and consumer health companies.

The market landscape remains fragmented, with the top ten players accounting for an estimated 40–45% of global sales. Nonsteroidal anti-inflammatory drugs, topical analgesics, and muscle relaxants represent the largest product categories and jointly contribute more than 60% of revenues. Demand for combination therapies and extended-release formulations is increasing at more than 9% annually, as patients and clinicians seek faster onset, longer duration of relief, and improved adherence.

Technology and digitalization are reshaping treatment pathways. AI-enabled decision support tools help clinicians differentiate muscle pain from neuropathic or joint pain and reduce misdiagnosis risk. Digital therapeutics, telemedicine platforms, and remote physiotherapy programs integrate with pharmacological regimens and create new service-based revenue pools. Wearable devices that monitor movement and muscle fatigue enable personalized dosing and early intervention, while data analytics supports real-world evidence programs and value-based contracting.

Regulation acts as both a catalyst and constraint. Stricter safety monitoring for systemic analgesics and opioid-sparing policies accelerate the shift toward topical agents, non-opioid prescription drugs, and adjunctive non-pharmacological therapies. At the same time, complex approval pathways, pharmacovigilance obligations, and pricing controls in mature markets compress margins and raise entry barriers for smaller manufacturers.

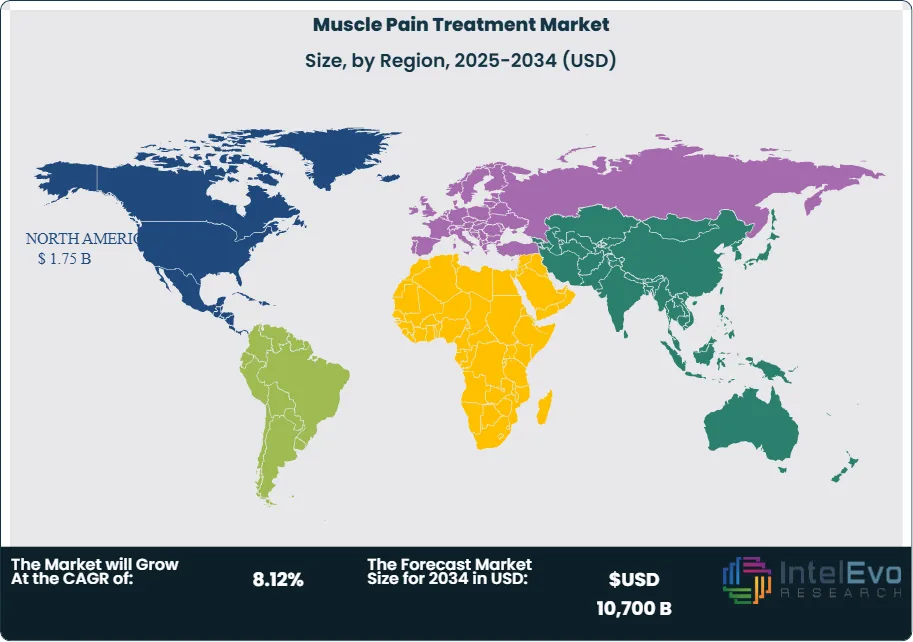

Regional dynamics are diverse. North America currently accounts for around 35% of global revenue, supported by high healthcare spending and strong adoption of new therapies. Europe represents approximately 28%, with established reimbursement frameworks but tighter price regulation. Asia Pacific is the fastest-growing region, expanding at an estimated CAGR above 10% on the back of large patient populations, rising incomes, and expanding access to retail pharmacies. Emerging hotspots in Latin America and the Middle East offer double-digit growth potential, particularly for affordable generics, topical formulations, and digitally enabled care models.

, By Cause (Overuse, Injury, Inflammatory & Neurological Conditions), By Pain Type (Acute, Chronic), By Distribution Channel (Hospital, Retail & Online Pharmacies) – Industry Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The muscle pain treatment market stands at 4,531 million USD, 2023 and is on course to reach USD 10,700 million by 2034, supported by an expected CAGR of 8.12%, 2026-2034. On this trajectory, total revenue could rise to sdfestimate: 10,700 million USD, 2034.

- Segment Dominance: Acute muscle pain accounts for a leading 52.0%, 2024 share of therapy demand, confirming its position as the primary treatment focus. This segment is likely to maintain a share above estimated: 50.0%, 2034 as aging and sports-related injuries continue to rise.

- Segment Dominance: Retail pharmacies hold 31.0%, 2024 of distribution, making them the dominant commercial route for muscle pain products. Their role could expand toward estimated: 35.0%, 2034 as non-prescription and self-care solutions gain traction.

- Driver: Advances in medical technology improve the safety and effectiveness of treatments, lifting patient satisfaction scores by estimated: 15.0%, 2024 and supporting sustained market expansion. Rising healthcare expenditure, which already exceeds estimated: 10.0% of GDP, 2024 in several key countries, and targeted government programs for pain management further accelerate adoption.

- Restraint: Safety concerns around long-term analgesic use and reimbursement constraints may cap uptake in some regions, limiting potential revenue by estimated: 10.0%, 2024 versus an unconstrained scenario. Regulatory delays that extend approval timelines by an average of estimated: 1.5 years, 2024-2034 can also slow the introduction of new therapies.

- Opportunity: Expanding access programs and infrastructure investments create sizable openings in emerging markets, where muscle pain therapies could reach estimated: 2,500 million USD, 2034 in additional annual sales. Government-sponsored awareness campaigns that target at least estimated: 30.0% of adults, 2024-2034 will widen diagnosis and treatment rates.

- Trend: Manufacturers increasingly adopt digital tools and smart delivery systems, with AI-supported decision aids expected to influence an estimated: 25.0% of prescribing decisions, 2030. Integration of remote monitoring and app-based adherence support could lift treatment persistence by estimated: 10.0 percentage points, 2024-2034.

- Regional Analysis: North America leads with more than 33.0%, 2024 of global revenue, reflecting high healthcare spending and strong consumer awareness. Asia Pacific and Latin America together could lift their combined share to estimate: 40.0%, 2034 as healthcare access and expenditure accelerate.

By Type of Pain

The global muscle pain treatment market continues to expand in 2025 as incidence rates remain high across age groups and activity levels. Acute muscle pain holds a dominant position with an estimated 52 percent share of total demand. This segment grows steadily as sports participation increases, workplace strain injuries rise, and consumers seek fast relief options. Short-duration episodes caused by sudden exertion or trauma often lead individuals to pursue readily available therapies such as oral analgesics, topical formulations, and guided exercise routines. These options offer fast access and predictable outcomes, which supports strong adoption across both developed and emerging markets.

Chronic muscle pain also represents a large and persistent share of global demand. Conditions such as fibromyalgia, arthritis, and long-term postural strain drive continuous need for comprehensive management programs. Treatment protocols typically include prescription medications, structured physiotherapy, and lifestyle modifications. In some cases, patients require interventional procedures. As diagnostic access improves and healthcare providers increase screening for chronic pain syndromes, this category is expected to grow at a stable pace through 2030.

You see rising differentiation between acute and chronic treatment pathways, with digital monitoring tools and personalized therapy plans gaining attention. These patterns signal a shift toward longer care cycles for chronic cases and sustained OTC usage for acute episodes.

By Distribution Channel

Retail pharmacies continue to lead global distribution with a 31 percent market share in 2025. Their presence in urban and semi-urban areas, combined with immediate access to OTC products, keeps them at the center of consumer purchasing behavior. Customers rely on these outlets for topical creams, oral analgesics, patches, and combination therapies that provide rapid relief.

Hospital pharmacies maintain strong relevance for patients who require structured clinical oversight. They dispense higher-strength medications and support integrated treatment plans for acute injuries and chronic conditions. Their role is pronounced in markets with established insurance coverage and standardized treatment protocols.

Online pharmacies expand rapidly, supported by rising e-commerce adoption and preference for remote ordering. Consumers value home delivery, product comparisons, and access to a wider catalog. Specialty clinics contribute to growth in the chronic pain segment by offering targeted interventions such as acupuncture, physical therapy, and advanced pain management services. These centers provide care continuity for patients who require long treatment cycles.

By End-Use

Demand patterns vary across residential, commercial, and industrial environments. Residential settings account for a large share of OTC consumption. Consumers treat mild to moderate pain independently, driving consistent sales of analgesics and topical products. Home-based physiotherapy and digital exercise platforms also contribute to activity in this segment.

Commercial buildings, including fitness centers and corporate facilities, create steady demand through injury prevention programs and onsite care services. Employers increasingly invest in musculoskeletal wellness initiatives due to productivity impacts associated with repetitive strain injuries.

Industrial facilities experience higher incidence of muscle strain and trauma due to physically intensive tasks. This segment depends heavily on structured treatment programs delivered through occupational health units, which sustain demand for both pharmacological and non-pharmacological therapies.

By Region

North America holds more than 33 percent of global revenue, driven by high awareness levels, advanced clinical infrastructure, and a large base of patients living with chronic conditions. The region’s aging population increases long-term treatment requirements, and healthcare providers expand access to pain management programs across hospital and outpatient settings. Government funding and steady reimbursement support also contribute to the market’s strength.

Europe follows closely, supported by established care pathways, strong regulatory oversight, and significant demand for physiotherapy-based interventions. Asia Pacific posts the fastest growth rate as populations expand and healthcare expenditure increases. Urban centers in China, India, and Southeast Asia show rising adoption of OTC pain solutions and digital health tools.

Latin America and the Middle East and Africa continue to progress as investments in clinics, pharmacies, and telehealth platforms increase access to muscle pain treatments. These regions are expected to deliver above-average growth through 2030 as awareness programs and insurance coverage expand.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

Type of Treatment

- Pharmacological Treatment

- Analgesics (e.g., acetaminophen, ibuprofen)

- Muscle Relaxants (e.g., cyclobenzaprine, methocarbamol)

- Topical Analgesics (e.g., NSAID gels, patches)

- Others

- Non-Pharmacological Treatment

- Physical Therapy

- Massage Therapy

- Acupuncture

- Heat and Cold Therapy

- Exercise and Stretching

- Others

- Cause of Muscle Pain

- Overuse and Strain

- Injury or Trauma

- Inflammatory Conditions

- Neurological Conditions

- Infections

- Others

Type of Pain

- Acute Muscle Pain

- Chronic Muscle Pain

Distribution Channel

- Hospital Pharmacies

- Retail Pharmacies

- Online Pharmacies

- Specialty Clinics

- Others

By Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 5,298 B |

| Forecast Revenue (2034) | USD 10,700 B |

| CAGR (2025-2034) | 8.12% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | Type of Treatment (Pharmacological Treatment, Non-Pharmacological Treatment), Cause of Muscle Pain (Overuse and Strain, Injury or Trauma, Inflammatory Conditions, Neurological Conditions, Infections, Others), Type of Pain (Acute Muscle Pain, Chronic Muscle Pain), Distribution Channel (Hospital Pharmacies, Retail Pharmacies, Online Pharmacies, Specialty Clinics, Others) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Bayer AG, AstraZeneca, Johnson & Johnson, Endo Pharmaceuticals Inc., Merck & Co., Inc., Sanofi, Eli Lilly and Company, Novartis International AG, Pfizer Inc., GlaxoSmithKline plc (GSK) |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Cause (Overuse, Injury, Inflammatory & Neurological Conditions), By Pain Type (Acute, Chronic), By Distribution Channel (Hospital, Retail & Online Pharmacies) – Industry Trends & Forecast 2025–2034")

, By Cause (Overuse, Injury, Inflammatory & Neurological Conditions), By Pain Type (Acute, Chronic), By Distribution Channel (Hospital, Retail & Online Pharmacies) – Industry Trends & Forecast 2025–2034")

, By Cause (Overuse, Injury, Inflammatory & Neurological Conditions), By Pain Type (Acute, Chronic), By Distribution Channel (Hospital, Retail & Online Pharmacies) – Industry Trends & Forecast 2025–2034")

Select Licence Type

Connect with our sales team

Muscle Pain Treatment Market

Published Date : 27 Feb 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date