Global Mushroom-Based Meat Alternative Market Size, Share | CAGR of 10.7%

Global Mushroom-Based Meat Alternative Market Size, Share, Analysis By Source (Oyster, Shiitake, Button, Portobello), By Format (Patties, Nuggets, Sausages, Minced/Crumbles, Strips), By Distribution Channel (Supermarkets, Specialty, Online, Foodservice), By Storage, By End User Region, Key Players – Dynamics, Strategies, Plant-Based Food & Mycoprotein Packaging Trends & Forecast 2026-2034

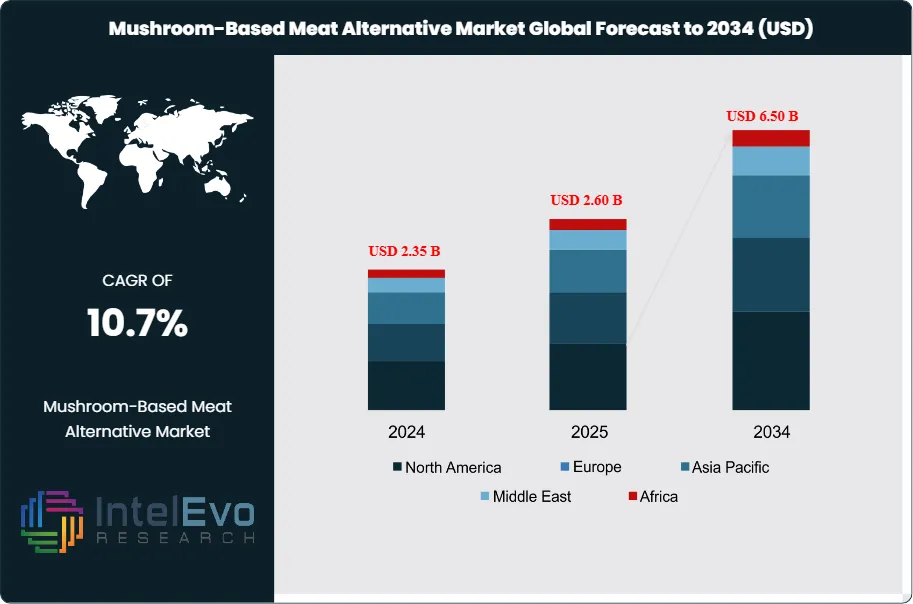

The Mushroom-Based Meat Alternative Market was valued at USD 2.35 Billion in 2024 and is estimated to reach USD 2.60 Billion in 2025. The market is projected to grow to USD 6.50 Billion by 2034, expanding at a CAGR of 10.7% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 3.90 Billion over the analysis period, equal to roughly 2.5 times the 2025 base value. Demand splits across three production routes: mycoprotein from continuous fermentation of Fusarium venenatum (the foundation of Quorn since 1985), whole-cut mycelium platforms that grow filamentous fungi into steak- and chicken-format protein (Meati Foods, MyForest Foods, Nature's Fynd), and whole-mushroom-based products built around portobello, shiitake, oyster, and lion's mane species.

The category is differentiating itself from broader plant-based meat where retail velocities have softened. According to Circana data published by 210 Analytics, U.S. retail dollar sales of meat alternatives fell 10.2% year-over-year to USD 70 Million in September 2025, with average refrigerated assortment dropping from 14 SKUs in 2021 to 9.3 in 2025. Mushroom-based offerings have countered this trend through clean-label positioning (typical SKUs carry five to seven recognizable ingredients), genuinely meat-like fibrous structure delivered without extrusion, and a measurable productivity gap: replacing 20% of beef with fungal protein could cut global deforestation by roughly 50% according to a peer-reviewed Nature publication.

Regulatory frameworks are stable and supportive. Mycoprotein from Fusarium venenatum has been approved in the United Kingdom since 1985, classified as not novel in the European Union under Regulation (EU) 2015/2283 because of pre-1997 consumption history, and Generally Recognized as Safe under the U.S. FDA framework since 2002. The Better Meat Co. holds GRAS clearance from both the FDA and USDA for Rhiza mycoprotein from Neurospora crassa, the only mycoprotein the USDA has formally evaluated as safe and suitable for inclusion in conventional meat. Singapore Food Agency clearance and a positive EFSA opinion on The Protein Brewery's Fermotein extend the global regulatory perimeter.

Innovation is concentrating along three axes. Whole-cut mycelium produced by submerged fermentation (Meati Foods) and solid-state fermentation (MyForest Foods, Nature's Fynd) is unlocking premium retail price points above USD 8 per pound. CRISPR-engineered Fusarium venenatum strains demonstrated 88.4% higher protein yield with 44% less feedstock in research published November 19, 2025 in Trends in Biotechnology by a Jiangnan University team. Continuous-fermentation cost compression is bringing pricing closer to commodity meat parity, with The Better Meat Co. publicly targeting Rhiza mycoprotein prices below U.S. commodity ground beef during 2026.

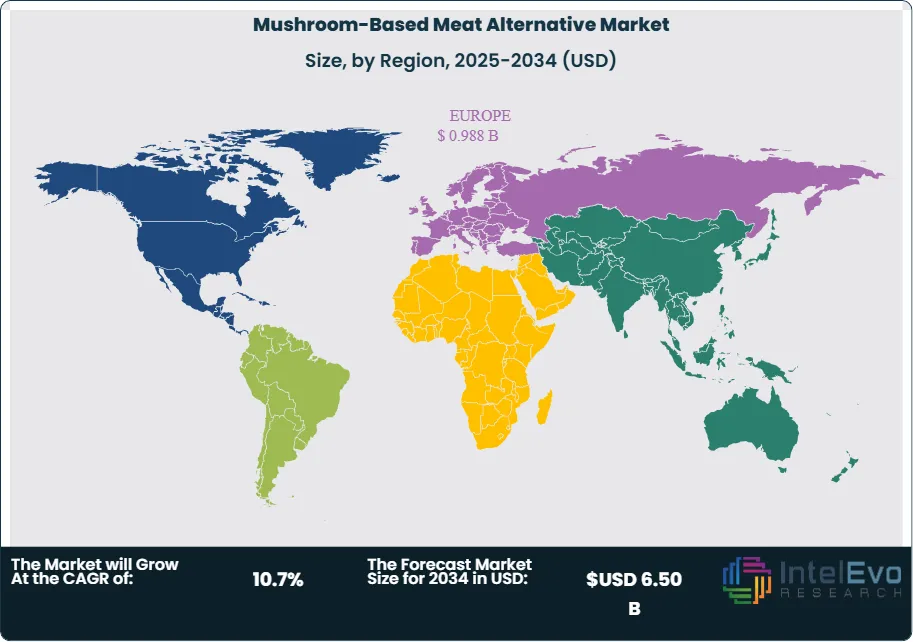

Europe led the market with 38.0% revenue share in 2025, anchored by Quorn's deep retail presence across the United Kingdom, Ireland, Germany, and the Netherlands. North America followed at 36.0%, supported by Meati Foods' national rollout into 7,000-plus retail doors and MyForest Foods' nationwide Whole Foods Market partnership reaching 2,500-plus stores. Asia Pacific captured 16.0% with the fastest forecast growth at 13.5% CAGR, driven by Chinese commercial scale-up of Fushine Bio and Japan's premium mushroom culinary tradition. The forecast assumes continued retail acceptance of fungal protein labeling and no material reversal in flexitarian consumer adoption trends across major markets.

Market Definition & Scope

The mushroom-based meat alternative market covers food products that use mushrooms, mycelium, or fungal mycoprotein as the primary protein source to replicate the texture, flavor, and nutritional profile of conventional meat. The market encompasses three production routes: continuous-fermentation mycoprotein from Fusarium venenatum and similar filamentous fungi; whole-cut mycelium grown through submerged or solid-state fermentation; and processed whole-mushroom products built around culinary varieties such as portobello, oyster, shiitake, and lion's mane.

This analysis includes finished consumer-packaged products (burgers, patties, sausages, nuggets, strips, deli slices, bacon, jerky, ground formats) sold through retail and foodservice. Excluded are dietary supplements, mushroom-based functional beverages, pure mushroom culinary ingredients without meat-mimicking processing, animal feed applications of fungal protein, and B2B mycoprotein ingredient sales except where they pass through to branded finished products. The mushroom-based segment captured approximately 31% of the broader USD 8.4 Billion meat substitutes market in 2025, making it the second-largest source category behind soy-based formulations.

Key Takeaways

Market Growth: The mushroom-based meat alternative market expanded from USD 2.60 Billion in 2025 toward a projected USD 6.50 Billion by 2034, representing a 10.7% CAGR over the nine-year forecast horizon.

Segment Dominance by Source: Mycoprotein from continuous fermentation (Fusarium venenatum and related strains) held 42.0% revenue share in 2025, anchored by Quorn's roughly USD 250 Million in fiscal 2024 sales reported by parent Marlow Foods.

Segment Dominance by Format: Burgers and patties led the format split with 28.0% revenue share in 2025, supported by mainstream foodservice partnerships including Sweetgreen, Birdcall, and Whole Foods Market deli programs.

Driver: Clean-label positioning is the primary competitive advantage versus broader plant-based meat, with leading mushroom-based SKUs carrying five to seven recognizable ingredients compared to 15-plus on extruded soy and pea alternatives.

Restraint: Category-wide alt-meat retail dollar sales fell 10.2% year-over-year to USD 70 Million in September 2025 per Circana data, signaling consumer fatigue with the broader plant-based aisle that mushroom-based brands must overcome through education.

Opportunity: The Better Meat Co. publicly targets pricing below U.S. commodity ground beef during 2026, which would unlock blended-meat (50/50 mycoprotein-and-meat) volume across Tyson Foods, Hormel Foods, Maple Leaf Foods, and Perdue Farms supply chains.

Trend: CRISPR-engineered Fusarium venenatum strains demonstrated an 88.4% increase in protein output with 44% lower feedstock consumption in research published November 19, 2025 in Trends in Biotechnology, signaling cost-compression headroom through 2030.

Regional: Europe generated USD 0.988 Billion in 2025 revenue (38.0% global share), with the United Kingdom alone contributing roughly USD 0.364 Billion through Quorn's 60% share of the British meat-replacement market.

Key Insights Summary

On August 19, 2025, The Better Meat Co. closed an oversubscribed USD 31 Million Series A round co-led by Future Ventures and Resilience Reserve, taking total capital raised to USD 43.1 Million and funding a tenfold scale-up from 9,000 liters to 90,000 liters of fermentation capacity.

Per Marlow Foods' fiscal 2024 disclosure, Quorn generated approximately USD 250 Million in annual sales despite a 9% year-over-year decline, with Monde Nissin (the Philippine parent company) recording a 20.5 Billion peso impairment charge against its meat alternatives portfolio in fiscal 2022.

Research published November 19, 2025 in Trends in Biotechnology reported that CRISPR-edited Fusarium venenatum strain FCPD produced 88.4% more protein while consuming 44% fewer nutrients than the unmodified Quorn parent strain, with texture analysis showing closer resemblance to chicken breast than the original.

Across U.S. retail in September 2025, Circana data analyzed by 210 Analytics showed total meat alternative dollar sales falling 10.2% year-over-year to USD 70 Million while MyForest Foods reported natural-channel velocity of 5.7 units per door each week and foodservice velocity above 10 weekly units per location.

On October 27, 2025, MyForest Foods rolled out MyBacon and MyPulledPork to 520 nationwide Whole Foods Market locations, broadening total retail footprint above 2,500 stores across all 50 U.S. states and growing year-over-year retail revenue 300% in 2024.

The Better Meat Co.'s Rhiza mycoprotein achieved a Protein Digestibility Corrected Amino Acid Score of 0.87 to 0.96 (close to casein and egg) and 45 to 50% crude protein on a dry-weight basis, with FDA GRAS clearance and a unique USDA designation as safe and suitable for inclusion in conventional meat.

Per the EU regulatory record, mycoprotein from Fusarium venenatum A 3/5 strains IMI 145425 and NRRL 26139 was confirmed not novel under Regulation (EU) 2015/2283 in 2024, opening the same B2B ingredient channel that Marlow Ingredients has pursued through partnerships such as Tempty Foods in Denmark.

Competitive Landscape Overview

The mushroom-based meat alternative market is moderately consolidated, with the four largest brands (Quorn Foods, Meati Foods, MyForest Foods, and Nature's Fynd) collectively accounting for an estimated 52 to 56% of 2025 revenue. Quorn maintains incumbent leadership through 40 years of consumer brand recognition and four large-scale fermenters in the United Kingdom, while the three U.S.-based whole-cut specialists have built rapid retail presence on the strength of clean-label positioning and venture funding totaling above USD 800 Million across the category.

Strategic activity is shifting toward B2B ingredient supply and incumbent-meat-company partnerships rather than direct-to-consumer brand building. Marlow Ingredients (the Quorn B2B division spun out in 2023) supplies mycoprotein to Tempty Foods and the U.K. National Health Service hospital network. The Better Meat Co. supplies Rhiza to Hormel Foods through 199 Ventures, Maple Leaf Foods, K-12 caterer SFE, and Perdue Farms (which has used the ingredient in Chicken Plus since 2019). Mycorena's 2024 bankruptcy, the consolidation of MycoTechnology, and the launch of Smaqo by Mycorena's former founder all signal an industry maturing past the early venture-flush phase into operational discipline.

Competitive Landscape Matrix

Company

HQ

Position

Key Product

Geographic Strength

Recent Strategic Move

Quorn Foods (Marlow Foods)

United Kingdom

Leader

Quorn mince, pieces, sausages, nuggets, escalopes

United Kingdom, Europe, USA

Brought Garlic & Mushroom Escalopes to UK retail in September 2025 alongside Marlow Ingredients B2B push

Meati Foods

USA (Boulder, CO)

Leader

Eat Meati cutlets, steaks, jerky from MushroomRoot mycelium

United States

Pushed national distribution past 7,000 retail doors via Sprouts, Whole Foods, Giant, Meijer, and Target

MyForest Foods (Ecovative)

USA (New York)

Leader

MyBacon, MyPulledPork from oyster mushroom mycelium

United States

On October 27, 2025, scaled MyBacon and MyPulledPork into 520 nationwide Whole Foods locations and 2,500-plus total stores

Brought Fy Bites to commercial debut at Natural Products Expo West in March 2025

The Better Meat Co.

USA (Sacramento, CA)

Challenger

Rhiza mycoprotein from Neurospora crassa (B2B)

United States, Asia, South America

Banked USD 31 Million Series A on August 19, 2025, scaling fermentation tenfold to 90,000 liters

ENOUGH

Scotland

Challenger

ABUNDA mycoprotein (B2B ingredient)

Europe

Joined forces with Unilever in May 2024 to develop new mycoprotein-based products in the UK

The Protein Brewery

Netherlands

Challenger

Fermotein mycoprotein from Rhizomucor pusillus

Europe

Earned a positive EFSA scientific opinion on Fermotein, the first fungal biomass through that EU pathway

Prime Roots

USA

Niche

Koji-mycelium deli meats (turkey, ham, salami)

United States

Posted retail velocity 5 to 10 times higher than other plant-based alternatives at partner stores

MycoTechnology

USA

Niche

ClearIQ flavor modulators, FermentIQ proteins

United States

Continued investment in shiitake-derived ingredient platforms for B2B food formulators

Mush Foods / Smaqo / Millow

Israel / Sweden

Niche

50Cut blended mycelium, hybrid mince products

Israel, Nordics

Smaqo emerged from former Mycorena founder Ram Nair's blended mycoprotein-and-meat play through 2025

Segmentation Analysis

The mushroom-based meat alternative market segments along five primary axes: source, format, distribution channel, storage temperature, and end user. Cross-referencing source against format shows that mycoprotein-based mince and pieces sold through retail represents the single largest revenue cell, accounting for roughly 18% of 2025 global revenue.

By Source

Mycoprotein led the source split with 42.0% revenue share in 2025, equal to roughly USD 1.09 Billion. Quorn anchors this segment through Fusarium venenatum strain PTA-2684, fermented continuously in a 40-cubic-meter air-lift reactor that produces 7 hydrated metric tonnes of biomass per 24-hour cycle. Adjacent mycoprotein platforms include The Better Meat Co.'s Neurospora crassa (Rhiza), The Protein Brewery's Rhizomucor pusillus (Fermotein), ENOUGH's Fusarium venenatum (ABUNDA), and Nature's Fynd's Fusarium yellowstonensis (Fy).

Whole-cut mycelium captured 25.0% revenue share at approximately USD 0.65 Billion, anchored by Meati Foods' submerged-fermentation MushroomRoot, MyForest Foods' solid-state oyster-mushroom mycelium, and Bosque Foods' similar platform. The whole-cut mycelium segment is the fastest-growing sub-source at a 14.8% forecast CAGR through 2034, reflecting clean-label premium pricing of USD 8 to USD 12 per pound. Whole-mushroom-based products built on portobello, shiitake, oyster, and lion's mane held 28.0% share, with restaurants and foodservice operators driving the bulk of demand. The remaining 5.0% covered hybrid blends and novel-strain experimental SKUs.

By Format

Burgers and patties led the format split with 28.0% revenue share in 2025, equivalent to roughly USD 0.73 Billion. Strips, nuggets, and fillets followed at 22.0%, anchored by Quorn's frozen breaded chicken-style products and Meati's Crispy Cutlets. Sausages and hot dogs took 18.0% share, ground or mince formats 16.0%, bacon and jerky specialty products 11.0%, and meatballs plus other formats the remaining 5.0%.

Bacon and jerky has been the fastest-growing format sub-segment at a 16.4% forecast CAGR through 2034, anchored by MyBacon's leadership in the U.S. natural-channel plant-based bacon category per SPINS data and Meati's mycelium-based jerky line. Format share is migrating from heavily processed extruded shapes toward whole-cut formats that highlight the inherent fibrous texture of mushroom-derived ingredients without secondary processing.

By Distribution Channel

Retail (B2C) accounted for 65.0% revenue share in 2025, equal to roughly USD 1.69 Billion, dominated by refrigerated and frozen sets at conventional grocers, natural-foods chains, and warehouse clubs. Whole Foods Market is the single largest U.S. retail channel for mushroom-based brands, anchoring the national footprint of MyForest Foods (520 stores), Nature's Fynd (full national distribution), and Meati Foods (full chain). Foodservice (B2B and B2B2C) captured 35.0%, with Sweetgreen's plant-based protein menu, Birdcall, university dining, and U.K. National Health Service hospital meals all featuring mushroom-based offerings. The Better Meat Co.'s ingredient-supply model and Marlow Ingredients' B2B push are accelerating B2B share through 2034.

By Storage Temperature

Refrigerated formats held 52.0% revenue share in 2025, frozen formats 38.0%, and shelf-stable formats 10.0%. Refrigerated dominance reflects consumer perception of fresher, cleaner-label products and the natural fit of whole-cut mycelium SKUs that mimic raw meat case presentation. Frozen growth is anchored by Quorn's traditional freezer-case footprint across Europe and growing U.S. distribution. Shelf-stable formats including jerky and ambient-temperature mycoprotein ingredients (Rhiza ships at ambient with an 18-month shelf life) are projected to grow at a 13.2% CAGR through 2034 because of distribution and storage cost advantages.

By End User

Flexitarian consumers led end-user demand with 55.0% revenue share in 2025, validating the strategic shift among mycoprotein incumbents toward blended-meat and mainstream-flexitarian positioning rather than vegan-dedicated SKUs. Vegan and vegetarian consumers held 38.0% share, anchored by long-standing Quorn brand loyalty in the United Kingdom and category penetration of Meati and MyForest in the U.S. natural channel. Other end-user segments including foodservice operators, K-12 catering, and institutional kitchens captured the remaining 7.0%, with ingredient suppliers such as The Better Meat Co. directly serving these channels through Hormel Foods, Maple Leaf Foods, and SFE.

Regional Analysis

The global mushroom-based meat alternative market splits across five regions, with revenue concentration tracking incumbent brand penetration and regulatory permissiveness. Europe led with 38.0% share, North America followed at 36.0%, Asia Pacific captured 16.0%, Latin America 5.0%, and Middle East and Africa 5.0%, summing to 100% of 2025 revenue.

Europe

Europe generated USD 0.988 Billion in 2025 revenue, holding 38.0% global share. The United Kingdom anchors regional value through Quorn's 60% share of the British meat-replacement market and four large-scale fermenters operated by parent Marlow Foods. Germany follows with rising adoption of Quorn, ENOUGH ABUNDA, and domestic mycelium players. The Netherlands hosts The Protein Brewery, which secured a positive EFSA opinion on Fermotein. Mycoprotein retains non-novel status across all 27 EU member states under Regulation (EU) 2015/2283 because of pre-1997 consumption history, providing regulatory tailwind that adjacent novel-protein platforms must navigate around.

North America

North America contributed USD 0.936 Billion in 2025, equal to 36.0% global share. The United States anchors the region through Meati Foods' 7,000-plus retail door footprint, MyForest Foods' 2,500-plus store network, and Nature's Fynd's full national Whole Foods Market distribution. The FDA's GRAS pathway has cleared multiple mycoprotein platforms including Quorn (since 2002), Rhiza from The Better Meat Co. (with USDA dual clearance), and Fy from Nature's Fynd. Canada's market is supplied largely through U.S. distribution of Quorn and MyForest products, while Mexico remains an early-stage market with limited retail penetration.

Asia Pacific

Asia Pacific posted USD 0.416 Billion in 2025 with 16.0% share and is the fastest-growing region at a forecast 13.5% CAGR through 2034. China hosts Fushine Bio in commercial mycoprotein development and is the source of a Jiangnan University CRISPR-edited Fusarium venenatum study published November 19, 2025 in Trends in Biotechnology. Singapore approved Rhiza mycoprotein through the Singapore Food Agency, opening Southeast Asian distribution. Japan and South Korea are mature whole-mushroom culinary markets with rising flexitarian demand for fungal-protein-based meat alternatives, while Australia hosts Fable Food Co.'s shiitake-based platform with growing retail and foodservice penetration.

Latin America

Latin America accounted for USD 0.130 Billion in 2025 (5.0% share). Brazil leads regional demand through major meat producers exploring blended-meat formats; The Better Meat Co. signed a letter of intent with one of South America's largest meat producers covering 30 tonnes of Rhiza monthly (90 tonnes meat-equivalent on a dry-weight basis). Argentina and Mexico follow with smaller adoption pockets. Limited domestic mycoprotein production capacity and consumer price sensitivity remain near-term constraints, though regional foodservice chains have begun trial deployments of mushroom-based menu items.

Middle East & Africa

Middle East and Africa generated USD 0.130 Billion in 2025, holding 5.0% share. Israel anchors the region through Mush Foods' blended-meat platform and adjacent fungi-based food technology specialists; Tel Aviv has emerged as a regional hub for alternative-protein innovation aligned with the country's broad food-tech ecosystem. The United Arab Emirates and Saudi Arabia are rolling out mushroom-based menu items across major hotel and foodservice operations linked to food-security policy under Vision 2030 frameworks. South Africa and Egypt represent emerging consumer markets with growing flexitarian pockets in major urban centers.

Country Analysis

United States

The U.S. mushroom-based meat alternative market reached USD 0.806 Billion in 2025 and is forecast to grow at a 9.8% CAGR through 2034. Federal regulatory clearance is the primary anchor, with the FDA having recognized mycoprotein from Fusarium venenatum as Generally Recognized as Safe since 2002 and the USDA designating Rhiza mycoprotein from The Better Meat Co. as safe and suitable for inclusion in conventional meat. The Department of Defense's Distributed Bioindustrial Manufacturing Program awarded a USD 1.5 Million biomanufacturing grant to The Better Meat Co. in August 2024. State-level activity is concentrated in California (Sacramento-based BMC, plus venture-funded Bay Area startups), Colorado (Boulder-based Meati), and New York (Green Island-based MyForest Foods).

United Kingdom

The U.K. market reached USD 0.364 Billion in 2025, growing at an 8.5% CAGR through 2034 in a relatively mature competitive environment. Quorn dominates with approximately 60% of the U.K. meat-replacement category and roughly USD 250 Million in fiscal 2024 sales reported by Marlow Foods. The Quorn brand has been on British shelves since 1985 following Ministry of Agriculture, Fisheries and Food approval and a ten-year evaluation. Marlow Ingredients spun out as a B2B division in 2023 and supplies mycoprotein into the National Health Service hospital meal program and to start-ups including Tempty Foods. Quorn's parent Monde Nissin has been pushing operational improvements after recording a 20.5 Billion Philippine peso impairment in fiscal 2022.

Germany

Germany's market reached USD 0.182 Billion in 2025, growing at an 11.0% CAGR through 2034. Quorn maintains the leading retail footprint following its 2012 relaunch through quorn.de, complemented by ENOUGH's ABUNDA ingredient distribution and Mushlabs' Berlin-based mycelium platform. Federal sustainability programs and the Bioeconomy 2030 strategy support fungal-protein research at Fraunhofer institutes. German consumers have demonstrated relatively higher acceptance of fungi-based labeling than in markets where mycoprotein is positioned as exotic, supporting per-capita consumption above the European average for plant-based and mushroom-based meat substitutes combined.

China

China's mushroom-based meat alternative market reached USD 0.156 Billion in 2025 at a 13.5% CAGR through 2034, the fastest among major country markets. Domestic production is anchored by Fushine Bio's commercial mycoprotein operations, complemented by joint ventures linking Chinese meat majors with Western fermentation specialists. Jiangnan University's research team published a CRISPR-engineered Fusarium venenatum strain (FCPD) in Trends in Biotechnology on November 19, 2025, demonstrating 88.4% higher protein output and 44% lower nutrient input. China's broader meat alternatives market reached approximately USD 3 Billion in 2025 according to industry trackers, of which mushroom-based products are estimated to contribute the noted 5.2% share. Government dietary-pivot programs and rising flexitarian adoption among urban consumers under 35 are the primary near-term growth drivers.

By Source, (Oyster Mushroom, Shiitake Mushroom, Button Mushroom, Portobello Mushroom, Others), By Format, (Patties, Nuggets, Sausages, Minced/Crumbles, Strips & Slices, Others), By Distribution Channel, (Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Foodservice Channels, Others), By Storage Temperature, (Frozen, Refrigerated, Shelf-Stable), By End User, (Retail Consumers, Restaurants & Foodservice, Food Manufacturers, Others),

Research Methodology

Primary Research- 100 Interviews of Stakeholders

Secondary Research

Desk Research

Regional scope

North America (United States, Canada, Mexico)

Latin America (Brazil, Argentina, Columbia)

East Asia And Pacific (China, Japan, South Korea, Australia, Cambodia, Fiji, Indonesia)

Sea And South Asia (India, Singapore, Thailand, Taiwan, Malaysia)

Eastern Europe (Poland, Russia, Czech Republic, Romania)

Western Europe (Germany, U.K., France, Spain, Itlay)

Middle East & Africa (GCC Countries, Egypt, Nigeria, South Africa, Israel)

Competitive Landscape

QUORN FOODS (MARLOW FOODS), MEATI FOODS, MYFOREST FOODS, NATURE'S FYND, THE BETTER MEAT CO., ENOUGH, THE PROTEIN BREWERY, PRIME ROOTS, MYCOTECHNOLOGY, MUSH FOODS, FABLE FOOD CO., BOSQUE FOODS, MUSHLABS, THE MUSHROOM MEAT CO., PAN'S MUSHROOM JERKY, FORTE PROTEIN, AQUA CULTURED FOODS, SMAQO, MILLOW, FUSHINE BIO, NAPLASOL, Others

Customization Scope

Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements.

Pricing and Purchase Options

Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF).

TABLE OF CONTENTS

1. EXECUTIVE SUMMARY

1.1. MARKET SNAPSHOT

1.2. KEY FINDINGS & INSIGHTS

1.3. ANALYST RECOMMENDATIONS

1.4. FUTURE OUTLOOK

2. RESEARCH METHODOLOGY

2.1. MARKET DEFINITION & SCOPE

2.2. RESEARCH OBJECTIVES: PRIMARY & SECONDARY DATA SOURCES

2.3. DATA COLLECTION SOURCES

2.3.1. COVERAGE OF 100+ PRIMARY RESEARCH/CONSULTATION CALLS WITH INDUSTRY STAKEHOLDERS

FIGURE 17 NORTH AMERICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 18 NORTH AMERICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 19 MARKET SHARE BY COUNTRY

FIGURE 20 LATIN AMERICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 21 LATIN AMERICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 22 MARKET SHARE BY COUNTRY

FIGURE 23 EASTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 24 EASTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 25 MARKET SHARE BY COUNTRY

FIGURE 26 WESTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 27 WESTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 28 MARKET SHARE BY COUNTRY

FIGURE 29 EAST ASIA AND PACIFIC MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 30 EAST ASIA AND PACIFIC MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 31 MARKET SHARE BY COUNTRY

FIGURE 32 SEA AND SOUTH ASIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 33 SEA AND SOUTH ASIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 34 MARKET SHARE BY COUNTRY

FIGURE 35 MIDDLE EAST AND AFRICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 36 MIDDLE EAST AND AFRICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 37 NORTH AMERICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 38 U.S. MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 39 U.S. MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 40 CANADA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 41 CANADA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 42 LATIN AMERICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 43 MEXICO MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 44 MEXICO MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 45 BRAZIL MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 46 BRAZIL MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 47 ARGENTINA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 48 ARGENTINA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 49 COLUMBIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 50 COLUMBIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 51 REST OF LATIN AMERICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 52 REST OF LATIN AMERICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 53 EASTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 54 POLAND MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 55 POLAND MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 56 RUSSIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 57 RUSSIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 58 CZECH REPUBLIC MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 59 CZECH REPUBLIC MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 60 ROMANIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 61 ROMANIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 62 REST OF EASTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 63 REST OF EASTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 64 WESTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 65 GERMANY MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 66 GERMANY MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 67 FRANCE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 68 FRANCE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 69 UK MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 70 UK MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 71 SPAIN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 72 SPAIN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 73 ITALY MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 74 ITALY MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 75 REST OF WESTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 76 REST OF WESTERN EUROPE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 77 EAST ASIA AND PACIFIC MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 78 CHINA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 79 CHINA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 80 JAPAN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 81 JAPAN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 82 AUSTRALIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 83 AUSTRALIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 84 CAMBODIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 85 CAMBODIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 86 FIJI MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 87 FIJI MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 88 INDONESIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 89 INDONESIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 90 SOUTH KOREA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 91 SOUTH KOREA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 92 REST OF EAST ASIA AND PACIFIC MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 93 REST OF EAST ASIA AND PACIFIC MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 94 SEA AND SOUTH ASIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 95 BANGLADESH MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 96 BANGLADESH MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 97 NEW ZEALAND MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 98 NEW ZEALAND MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 99 INDIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 100 INDIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 101 SINGAPORE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 102 SINGAPORE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 103 THAILAND MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 104 THAILAND MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 105 TAIWAN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 106 TAIWAN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 107 MALAYSIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 108 MALAYSIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 109 REST OF SEA AND SOUTH ASIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 110 REST OF SEA AND SOUTH ASIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 111 MIDDLE EAST AND AFRICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE MARKET VOLUME SHARE REGIONAL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 112 GCC COUNTRIES MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 113 GCC COUNTRIES MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 114 SAUDI ARABIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 115 SAUDI ARABIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 116 UAE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 117 UAE MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 118 BAHRAIN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 119 BAHRAIN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 120 KUWAIT MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 121 KUWAIT MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 122 OMAN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 123 OMAN MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 124 QATAR MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 125 QATAR MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 126 EGYPT MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 127 EGYPT MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 128 NIGERIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 129 NIGERIA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 130 SOUTH AFRICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 131 SOUTH AFRICA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 132 ISRAEL MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 133 ISRAEL MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 134 REST OF MEA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE TYPE ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 135 REST OF MEA MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE END USER ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 136 U. S. MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 137 U. S. MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 138 CANADA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 139 CANADA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 140 MEXICO MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 141 MEXICO MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 142 CHINA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 143 CHINA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 144 JAPAN MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 145 JAPAN MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 146 INDIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 147 INDIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 148 SOUTH KOREA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 149 SOUTH KOREA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 150 SAUDI ARABIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 151 SAUDI ARABIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 152 UAE MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 153 UAE MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 154 EGYPT MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 155 EGYPT MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 156 NIGERIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 157 NIGERIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 158 SOUTH AFRICA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 159 SOUTH AFRICA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 160 GERMANY MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 161 GERMANY MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 162 FRANCE MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 163 FRANCE MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 164 UK MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 165 UK MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 166 SPAIN MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 167 SPAIN MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 168 ITALY MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 169 ITALY MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 170 BRAZIL MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 171 BRAZIL MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 172 ARGENTINA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 173 ARGENTINA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 174 COLUMBIA MARKET SHARE ANALYSIS BY TYPE (2025)

FIGURE 175 COLUMBIA MARKET SHARE ANALYSIS BY END USER (2025)

FIGURE 176 MUSHROOM-BASED MEAT ALTERNATIVE MARKET CURRENT AND FUTURE MARKET KEY COUNTRY LEVEL ANALYSIS, 2025–2034, (USD MILLION)

FIGURE 177 FINANCIAL OVERVIEW:

Key Player Analysis

Quorn Foods (Marlow Foods)

Quorn Foods, operated by Marlow Foods Limited and owned by Philippine consumer-goods major Monde Nissin Corporation (PSE: MONDE), is the leading mushroom-based meat alternative brand globally. Marlow Foods reported approximately USD 250 Million in Quorn brand sales for fiscal 2024, a 9% year-over-year decline reflecting broader category headwinds. Production runs through four large-scale 40-cubic-meter air-lift fermenters in the United Kingdom, each operating in continuous mode and producing 7 hydrated metric tonnes of Fusarium venenatum biomass per 24-hour cycle.

On the strategic side, Marlow Ingredients spun out as a B2B division in 2023 and supplies mycoprotein into NHS hospital meal programs in the United Kingdom and to international start-ups including Denmark's Tempty Foods. In September 2025, Quorn brought Garlic & Mushroom Escalopes to U.K. retail under its core branded line, complementing a broader Nothing to Hide marketing campaign emphasizing five-to-seven-ingredient labeling on frozen products. Differentiation rests on 40 years of consumer brand recognition, regulatory clearance across 20 country markets, and the only commercial-scale continuous-fermentation infrastructure with multi-decade operating history. Monde Nissin recorded a 20.5 Billion peso impairment on the meat alternatives portfolio in fiscal 2022, signaling investment discipline ahead of any near-term reacceleration.

Meati Foods

Meati Foods, headquartered in Boulder, Colorado, is a leading whole-cut mycelium specialist with cumulative funding above USD 278 Million across multiple rounds including a USD 150 Million Series C led by Revolution Growth and Rockefeller Capital. The company operates the Mega Ranch, a 125,000-square-foot production facility commissioned in phases through 2023 and 2024, with submerged-fermentation tanks growing Neurospora crassa-derived MushroomRoot biomass that is then formed into steaks, cutlets, and jerky.

Strategic priorities through 2025 included scaling national distribution to 7,000-plus retail doors across Sprouts Farmers Market, Whole Foods Market, Giant, Meijer, and Target, plus foodservice partnerships with Sweetgreen and Birdcall. In November 2025, Meati introduced four new SKUs including Italian-Seasoned Cutlet, Garlic & Black Pepper Steak, Crispy Bites, and Spicy Crispy Cutlet, expanding the company's product line beyond its Core Four cutlets and steaks. The company faced a legal challenge in 2025 over its mushroom root marketing terminology and has implemented workforce restructuring during the broader category slowdown. Differentiation rests on submerged-fermentation speed (which produces aligned fibers in days rather than the weeks required by solid-state) and a Mega Ranch capacity capable of supporting hundreds of millions of pounds of annual mycelium output as utilization ramps.

MyForest Foods

MyForest Foods, the food subsidiary of Ecovative LLC and headquartered in Green Island, New York, is a leading whole-cut mycelium platform specializing in MyBacon and MyPulledPork products grown from organic oyster mushroom mycelium through 12-day solid-state fermentation in vertical farms. Parent Ecovative closed a USD 30 Million-plus Series E in July 2023 led by Viking Global Investors that split funding between MyForest and the MycoComposite packaging line. MyForest added an additional USD 11 Million in 2025 including a USD 1.68 Million grant from the Advance Albany County Alliance.

On October 27, 2025, the company rolled out MyBacon and MyPulledPork into 520 nationwide Whole Foods Market locations, broadening total retail footprint above 2,500 stores across all 50 U.S. states. Recent additions to the retailer mix include Hannaford, Schnucks, Price Chopper, Giant, and Natural Grocers. Per founder Eben Bayer, the company became direct-margin-positive in late 2024 and projects double-digit-million-dollar revenue with EBITDA-positive operations by the first half of 2027. SPINS data places MyBacon as the top-selling plant-based bacon in the U.S. natural grocery channel. Differentiation rests on a five-ingredient label (organic mycelium, salt, sugar, coconut oil, natural flavors), a vertical-farming production model uniquely suited to solid-state fermentation, and demonstrated retail velocity around 5.7 weekly units per natural-grocery door.

Nature's Fynd

Nature's Fynd, headquartered in Chicago, Illinois, is a leading fungi-based food platform built around Fy protein, fermented from Fusarium yellowstonensis (a microbe originally identified by NASA-funded research in Yellowstone National Park hot springs by co-founder Mark Kozubal). The company has secured cumulative funding above USD 500 Million in equity and debt, backed by Bill Gates, Jeff Bezos, and Generation Investment Management. The 35,000-square-foot Chicago production facility grows fresh Fy biomass on a three-to-four-day fermentation cycle, with output crafted into Meatless Fy Patties, Fy Bites, and Dairy-Free Fy Yogurt across three flavor variants.

Strategic milestones through 2024 and 2025 included the January 2024 Whole Foods Market national launch of Dairy-Free Fy Yogurt (the world's first fungi-based yogurt), the March 2025 Natural Products Expo West introduction of Fy Bites, and the April 2025 launch of Spicy Indian Fy Bites. The company appointed three-Michelin-starred Chef Eric Ripert as Culinary Advisor and won the 2025 NEXTY Award for Best New Dairy Alternative for Strawberry Dairy-Free Fy Yogurt. Differentiation rests on a unique Yellowstone-origin extremophile microbe, breakthrough fermentation IP licensed from NASA-funded research, and a sheet-form Fy biomass that uniquely supports both meat analogs and dairy analogs from the same fermentation platform without separate downstream lines.

Market Key Players

QUORN FOODS (MARLOW FOODS)

MEATI FOODS

MYFOREST FOODS

NATURE'S FYND

THE BETTER MEAT CO.

ENOUGH

THE PROTEIN BREWERY

PRIME ROOTS

MYCOTECHNOLOGY

MUSH FOODS

FABLE FOOD CO.

BOSQUE FOODS

MUSHLABS

THE MUSHROOM MEAT CO.

PAN'S MUSHROOM JERKY

FORTE PROTEIN

AQUA CULTURED FOODS

SMAQO

MILLOW

FUSHINE BIO

NAPLASOL

Others

Drivers

Rising Consumer Demand for Plant-Based Meat Alternatives

The increasing shift toward plant-based diets and sustainable food consumption is a major driver of the global mushroom-based meat alternative market. Consumers are becoming more conscious about health, environmental impact, and animal welfare, leading to greater demand for meat substitutes made from natural and nutritious ingredients. Mushrooms are gaining popularity due to their high fiber content, low fat profile, umami flavor, and ability to provide a meat-like texture.

Food manufacturers are increasingly incorporating mushroom-based ingredients into burgers, nuggets, sausages, and other alternative meat products to meet changing dietary preferences. The expansion of vegan, vegetarian, and flexitarian consumer groups worldwide is further accelerating market growth and encouraging innovation in mushroom-based food formulations.

Growing Focus on Sustainable Food Production

The rising emphasis on sustainable food systems is significantly supporting the adoption of mushroom-based meat alternatives. Mushroom cultivation requires fewer resources compared with traditional livestock production, including less land, water, and energy, making it an environmentally friendly protein solution. This aligns with global efforts to reduce greenhouse gas emissions and improve food sustainability.

Governments, food companies, and investors are increasingly supporting alternative protein development to address climate challenges and future food security concerns. These initiatives are encouraging companies to expand production capacity and introduce innovative mushroom-based products across global markets.

Restraints

Higher Production Costs and Limited Supply Chain Infrastructure

The production of mushroom-based meat alternatives involves specialized cultivation, processing, and formulation technologies, which can result in higher manufacturing costs compared with conventional meat products. Maintaining consistent mushroom quality, scaling production, and ensuring efficient supply chains remain challenging for many producers.

Limited availability of advanced processing facilities and fluctuations in raw material supply can impact product pricing and profitability. These challenges may restrict market penetration, particularly in price-sensitive regions where consumers are less willing to pay premium prices for alternative protein products.

Consumer Acceptance and Taste Challenges

Although mushroom-based meat alternatives are gaining popularity, some consumers remain hesitant due to differences in taste, texture, appearance, and familiarity compared with traditional meat products. Achieving a realistic meat-like experience continues to be a key challenge for manufacturers developing plant-based alternatives.

Additionally, limited consumer awareness regarding the nutritional benefits and versatility of mushroom-based proteins can slow adoption. Companies need effective marketing strategies, product education, and continuous innovation to improve consumer acceptance and expand market reach.

Trends

Innovation in Mushroom-Based Food Formulations

Continuous innovation in food technology is a major trend shaping the mushroom-based meat alternative market. Manufacturers are developing advanced formulations using mushroom mycelium and other fungal-based ingredients to improve texture, flavor, nutritional value, and cooking performance. These innovations are enabling the creation of products that closely replicate the sensory characteristics of conventional meat.

The development of clean-label, minimally processed, and allergen-friendly mushroom-based products is also gaining momentum. Companies are focusing on creating diverse product offerings, including plant-based burgers, seafood alternatives, ready-to-eat meals, and protein snacks to attract a broader consumer base.

Expansion of Retail and Foodservice Adoption

The increasing availability of mushroom-based meat alternatives through supermarkets, online platforms, restaurants, and foodservice providers is a key market trend. Retailers are expanding plant-based product sections as consumer interest in sustainable food options continues to grow.

Restaurants and food chains are also introducing mushroom-based menu items to meet demand from health-conscious and environmentally aware customers. This expansion across multiple sales channels is improving product accessibility and supporting wider market adoption globally.

Opportunities

Growing Demand for Alternative Protein Solutions

The rapid growth of the alternative protein industry presents significant opportunities for mushroom-based meat alternative manufacturers. As consumers search for healthier and more sustainable protein sources, mushroom-derived products are emerging as an attractive option due to their natural origin, nutritional benefits, and versatility.

Investments in biotechnology, fermentation techniques, and advanced food processing are expected to enhance production efficiency and reduce costs. These advancements can create new opportunities for companies to expand their product portfolios and compete more effectively within the growing plant-based food sector.

Expansion Across Emerging Markets

Emerging economies offer significant growth opportunities due to rising disposable incomes, urbanization, and increasing awareness of sustainable nutrition. Growing demand for convenient and healthy food options is encouraging consumers in developing regions to explore alternative protein products, including mushroom-based meat substitutes.

Strategic partnerships between food manufacturers, retailers, and agricultural producers can help improve distribution networks and increase market penetration. As awareness of plant-based nutrition continues to expand, mushroom-based meat alternatives are expected to gain stronger acceptance across Asia-Pacific, Latin America, and other developing markets.

Investment & M&A Activity

The mushroom-based meat alternative market recorded approximately USD 65 Million in disclosed venture and partnership activity over the trailing 12 months ending Q1 2026, reflecting a measured capital environment after broader alternative-protein funding contracted 27% in 2024 and a further 49% in the first half of 2025. Capital flow has concentrated on commercial-scale fermentation infrastructure and B2B ingredient supply rather than direct-to-consumer brand building, marking a clear strategic pivot in the category.

On August 19, 2025, The Better Meat Co. closed a USD 31 Million oversubscribed Series A round co-led by Future Ventures and Resilience Reserve, with Hickman's Family Farms CEO Glenn Hickman, Epic Ventures, and Sigma Ventures participating. Total capital raised by the Sacramento-based mycoprotein specialist reached USD 43.1 Million; the proceeds will fund a tenfold capacity scale-up from 9,000-liter fermentation to 90,000 liters and underpin the company's stated target of selling Rhiza mycoprotein below U.S. commodity ground beef pricing during 2026. Future Ventures co-founder Steve Jurvetson joined the company's board of directors as part of the round.

MyForest Foods added approximately USD 11 Million to its capital base during 2025, including a USD 1.68 Million grant from the Advance Albany County Alliance to support MyBacon production scale-up at the Green Island, New York vertical-farming facility. Earlier in the trailing window, parent Ecovative completed Series E activity led by Viking Global Investors. On the other side of the sector, Sweden's Mycorena entered bankruptcy proceedings during 2024 amid B2B go-to-market timing pressure; founder Ram Nair then launched Smaqo with a blended mycoprotein-and-meat strategy targeting the same flexitarian segment Mycorena had pursued.

Acquisition appetite from large incumbent meat companies has shifted toward minority equity and ingredient-supply agreements rather than full acquisitions. Hormel Foods supplies Rhiza through its 199 Ventures arm, Perdue Farms uses the ingredient in Chicken Plus nuggets, and Maple Leaf Foods has deployed it across blended-meat product trials. Comparable transaction multiples in the mushroom-based meat category landed near 3 to 4 times trailing revenue for established branded assets and 6 to 8 times forward revenue for fermentation specialists with regulatory clearance, reflecting a maturity step away from the 12-times-plus multiples seen at the 2021-2022 peak.

Recent Developments

December 2025 – Jiangnan University Research Team: On November 19, 2025, a Jiangnan University team led by Xiao Liu published research in the journal Trends in Biotechnology demonstrating that CRISPR-edited Fusarium venenatum strain FCPD produced 88.4% more protein while consuming 44% less feedstock than the unmodified parent strain used in Quorn since 1985.

Strategic Impact: Demonstrated yield improvements at this scale point to a multi-year cost-compression runway for incumbent mycoprotein platforms, narrowing the gap to commodity meat pricing without requiring novel-strain regulatory approvals.

November 2025 – Meati Foods: During November 2025, Meati introduced four new SKUs (Italian-Seasoned Cutlet, Garlic & Black Pepper Steak, Crispy Bites, and Spicy Crispy Cutlet), expanding the company's whole-cut mycelium portfolio beyond the original four-product Core Four lineup of cutlets and steaks.

Strategic Impact: SKU breadth expansion against fixed national-retail distribution unlocks per-store revenue density and supports continued utilization ramp at the Mega Ranch production facility.

October 2025 – MyForest Foods (Ecovative): On October 27, 2025, the company scaled MyBacon and MyPulledPork into 520 nationwide Whole Foods Market locations, with total U.S. retail footprint surpassing 2,500 stores across all 50 states; SPINS data confirmed MyBacon as the top-selling plant-based bacon in the natural grocery channel.

Strategic Impact: National Whole Foods rollout combined with category-leading SPINS velocity validates clean-label five-ingredient positioning as the differentiator at a moment when broader plant-based meat sales fell 10.2% year-over-year.

October 2025 – The Better Meat Co.: On October 9, 2025, TIME magazine named Rhiza mycoprotein from The Better Meat Co. to its Best Inventions of 2025 list, highlighting the Sacramento-based company's allergen-free Neurospora crassa fermentation process and the only USDA-evaluated safe-and-suitable mycoprotein for blended meat applications.

Strategic Impact: Editorial recognition tied to USDA inclusion clearance reinforces Rhiza's positioning with major meat companies including Hormel Foods, Maple Leaf Foods, and Perdue Farms during the company's commercial-scale ramp.

September 2025 – Quorn Foods: During September 2025, Quorn brought Garlic & Mushroom Escalopes to U.K. retail under its core branded frozen line, made with Fusarium venenatum mycoprotein and complementing the company's broader Nothing to Hide marketing campaign emphasizing simple ingredient labeling.

Strategic Impact: Premium-format SKU launches by the incumbent address consumer fatigue with heavily processed plant-based meat by leaning into the clean-label five-to-seven-ingredient positioning that whole-cut newcomers have used to disrupt the category.

May 2024 – Unilever and ENOUGH: In May 2024, Unilever PLC entered into a development partnership with Scotland-based ENOUGH to bring new mycoprotein-based meat alternatives to market in the United Kingdom using ABUNDA, a zero-waste fermentation product made from wheat and corn that yields a complete amino acid profile.

Strategic Impact: A consumer-goods major committing to mycoprotein-based product development through a B2B ingredient partnership signals durable category demand from mainstream brand owners and accelerates ENOUGH's path to commercial scale.

Frequently Asked Questions

How big is the Mushroom-Based Meat Alternative Market?

Global Mushroom-Based Meat Alternative Market was valued at USD 2.60 Billion in 2025 and is projected to reach USD 6.50 Billion by 2034, growing at a CAGR of 10.7% during 2026–2034. Explore market trends, drivers, opportunities, segmentation, and industry insights.

Who are the major players in the Mushroom-Based Meat Alternative Market?

QUORN FOODS (MARLOW FOODS), MEATI FOODS, MYFOREST FOODS, NATURE'S FYND, THE BETTER MEAT CO., ENOUGH, THE PROTEIN BREWERY, PRIME ROOTS, MYCOTECHNOLOGY, MUSH FOODS, FABLE FOOD CO., BOSQUE FOODS, MUSHLABS, THE MUSHROOM MEAT CO., PAN'S MUSHROOM JERKY, FORTE PROTEIN, AQUA CULTURED FOODS, SMAQO, MILLOW, FUSHINE BIO, NAPLASOL, Others

Which segments covered the Mushroom-Based Meat Alternative Market?

By Source, (Oyster Mushroom, Shiitake Mushroom, Button Mushroom, Portobello Mushroom, Others), By Format, (Patties, Nuggets, Sausages, Minced/Crumbles, Strips & Slices, Others), By Distribution Channel, (Supermarkets & Hypermarkets, Specialty Stores, Online Retail, Foodservice Channels, Others), By Storage Temperature, (Frozen, Refrigerated, Shelf-Stable), By End User, (Retail Consumers, Restaurants & Foodservice, Food Manufacturers, Others),

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

, By Format (Patties, Nuggets, Sausages, Minced/Crumbles, Strips), By Distribution Channel (Supermarkets, Specialty, Online, Foodservice), By Storage, By End User Region, Key Players – Dynamics, Strategies, Plant-Based Food & Mycoprotein Packaging Trends & Forecast 2026-2034")

, By Format (Patties, Nuggets, Sausages, Minced/Crumbles, Strips), By Distribution Channel (Supermarkets, Specialty, Online, Foodservice), By Storage, By End User Region, Key Players – Dynamics, Strategies, Plant-Based Food & Mycoprotein Packaging Trends & Forecast 2026-2034")

, By Format (Patties, Nuggets, Sausages, Minced/Crumbles, Strips), By Distribution Channel (Supermarkets, Specialty, Online, Foodservice), By Storage, By End User Region, Key Players – Dynamics, Strategies, Plant-Based Food & Mycoprotein Packaging Trends & Forecast 2026-2034")

, By Format (Patties, Nuggets, Sausages, Minced/Crumbles, Strips), By Distribution Channel (Supermarkets, Specialty, Online, Foodservice), By Storage, By End User Region, Key Players – Dynamics, Strategies, Plant-Based Food & Mycoprotein Packaging Trends & Forecast 2026-2034")