- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Nano Diamond Market Size, Share & Growth Analysis | CAGR 12.4%

Global Nano Diamond Market Size, Share, Analysis By Production Method (Detonation Synthesis, High-Pressure High-Temperature HPHT Synthesis, Chemical Vapor Deposition CVD), By Application (Polishing & Abrasives, Lubricant Additives, Polymer & Composite Reinforcement, Biomedical Drug Delivery & Imaging, Quantum Technology NV-Center Sensing), By End-User Industry (Electronics & Semiconductor, Automotive, Healthcare & Life Sciences, Defense & Aerospace, Industrial), By Particle Size (2–5 nm, 5–10 nm, Above 10 nm) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034

Report Overview

| Market Size | Forecast Value | CAGR | Leading Region |

|---|---|---|---|

| USD 1.9 Billion, 2025 | USD 5.4 Billion, 2034 | 12.4%, 2026–2034 | APAC, 42.6%, 2025 |

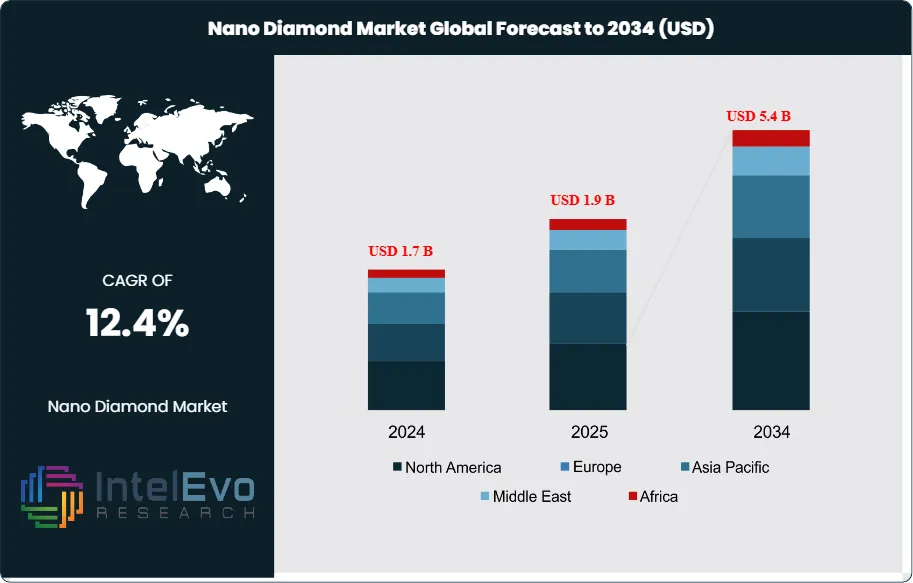

The Nano Diamond Market was valued at approximately USD 1.7 Billion in 2024 and increased to USD 1.9 Billion in 2025. The market is projected to reach nearly USD 5.4 Billion by 2034, expanding at a compound annual growth rate (CAGR) of 12.4% during the forecast period from 2026 to 2034. The nano diamond market is gaining significant commercial momentum as detonation synthesis and high-pressure high-temperature production methods mature, enabling consistent quality production of nanodiamond particles at commercial scales for applications spanning precision polishing, lubricant additives, polymer composites, biomedical drug delivery, and quantum sensing. Nanodiamonds, typically ranging from 2 to 10 nanometers in diameter, possess a unique combination of extreme hardness, high thermal conductivity, large surface area, and tunable surface chemistry that makes them functionally superior to conventional abrasive and additive materials across multiple industrial applications.

Get More Information about this report -

Request Free Sample ReportDemand forces driving the nano diamond market include the semiconductor industry's transition to sub-5-nanometer node fabrication where ultra-precision chemical mechanical planarization requires nanodiamond polishing slurries capable of removing material at atomic-scale precision without surface damage, rising adoption of nanodiamond lubricant additives in automotive and industrial machinery applications that reduce friction coefficients by 15–40% compared to conventional lubricant packages, and growing investment in nanodiamond-based drug delivery systems and fluorescent biomarkers for cancer diagnostics and targeted therapy. Supply-side dynamics reflect increasing production capacity from Russian and Chinese detonation synthesis operators, growing HPHT synthesis capability in Europe and the United States, and the emergence of chemical vapor deposition techniques for producing optically pure nanodiamonds for quantum technology applications.

Regulatory influences on the nano diamond market are primarily channeled through nanomaterial safety assessment frameworks. The European Chemicals Agency's nanomaterial registration requirements under REACH regulations are compelling manufacturers to generate toxicological and ecotoxicological datasets for nanodiamond products, adding compliance costs but also creating quality differentiation opportunities for producers with comprehensive safety documentation. The U.S. Environmental Protection Agency's nanomaterial reporting rule under the Toxic Substances Control Act requires pre-manufacture notifications for new nanodiamond formulations. In the biomedical application segment, nanodiamond-based drug delivery systems are subject to U.S. Food and Drug Administration Investigational New Drug pathway requirements that impose rigorous clinical validation obligations before commercial therapeutic deployment.

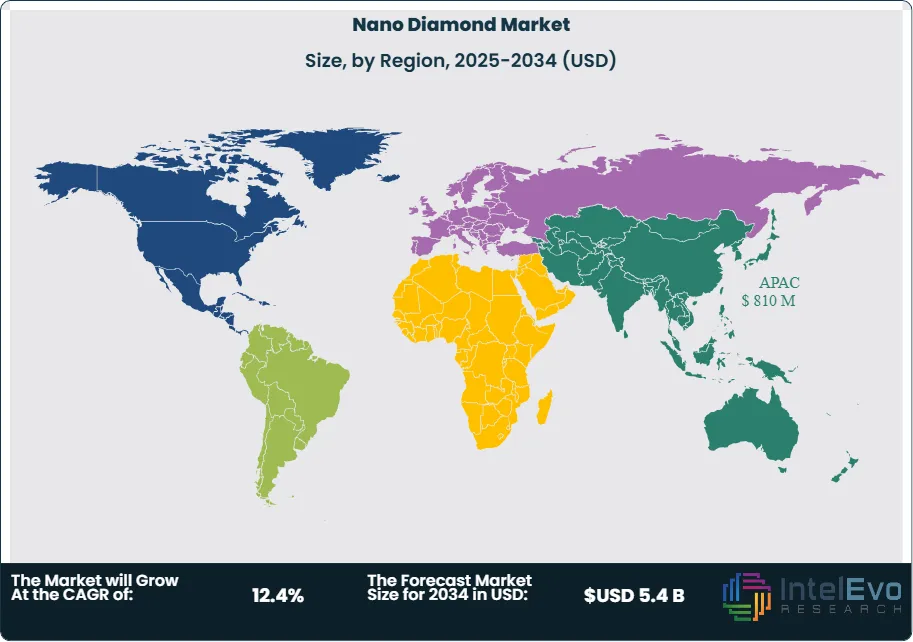

Risk factors in the nano diamond market include the high production costs of pharmaceutical-grade and quantum-grade nanodiamonds relative to conventional substitutes, the regulatory uncertainty surrounding nanomaterial classification in key jurisdictions, and the long qualification cycles for nanodiamond adoption in semiconductor fabrication applications where supply qualification requires 12–24 months of customer testing before commercial program approval. Asia Pacific leads the nano diamond market with a 42.6% share in 2025 at USD 810 Million, driven by Chinese semiconductor manufacturing and precision engineering demand. North America follows at 26.4% at USD 502 Million, anchored by defense, biomedical, and semiconductor applications. By 2034, quantum sensing and biomedical applications are projected to represent the fastest-growing nano diamond market segments, reshaping the competitive landscape toward high-purity specialty producers from the current abrasive and lubricant-dominated demand structure.

, By Application (Polishing & Abrasives, Lubricant Additives, Polymer & Composite Reinforcement, Biomedical Drug Delivery & Imaging, Quantum Technology NV-Center Sensing), By End-User Industry (Electronics & Semiconductor, Automotive, Healthcare & Life Sciences, Defense & Aerospace, Industrial), By Particle Size (2–5 nm, 5–10 nm, Above 10 nm) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global nano diamond market was valued at USD 1.9 Billion in 2025 and is projected to reach USD 5.4 Billion by 2034, registering a CAGR of 12.4% during the forecast period 2025–2034, driven by rising semiconductor polishing demand, lubricant additive adoption, and expanding biomedical and quantum technology applications.

- Segment Dominance (By Type): Detonation nanodiamonds are the dominant product type in the nano diamond market with a 58.6% share in 2025 at USD 1.1 Billion, underpinned by their cost-effective production from explosive detonation processes and wide commercial applicability across polishing, lubrication, and polymer composite applications.

- Segment Dominance (By Application): Polishing and abrasive applications lead the nano diamond market with a 38.4% share in 2025 at USD 730 Million, driven by semiconductor wafer planarization, precision optics finishing, and hard disk substrate polishing programs that require nanodiamond slurries and compounds for sub-nanometer surface quality.

- Driver: The semiconductor industry's transition to sub-5-nanometer node fabrication is compelling chip manufacturers to adopt nanodiamond polishing slurries that deliver atomic-scale material removal precision, with global semiconductor chemical mechanical planarization consumable spending growing at 18.6% annually in 2025 and nanodiamond-based slurries capturing an expanding share of this high-value market.

- Restraint: High production costs for pharmaceutical-grade and quantum-grade nanodiamonds, averaging USD 8,000–25,000 per kilogram for purified fluorescent nanodiamond particles compared to USD 50–200 per kilogram for industrial detonation nanodiamond powders, limit the addressable market for premium nano diamond products and constrain adoption in cost-sensitive applications.

- Opportunity: Nanodiamond-based drug delivery and biomedical imaging applications represent a USD 820 Million addressable opportunity within the nano diamond market by 2034. Clinical-stage nanodiamond drug delivery programs in oncology and neurodegenerative disease treatment covered less than 4% of technically validated therapeutic targets globally as of 2025, signaling substantial untapped commercial potential.

- Trend: Nitrogen-vacancy center nanodiamonds for quantum sensing and quantum computing applications are growing at 41.8% annually in 2025, attracting USD 340 Million in combined government and private sector R&D investment globally, as quantum technology programs in the United States, Europe, China, and Japan target nanodiamond-based qubit platforms for room-temperature quantum sensing.

- Regional Analysis: Asia Pacific leads the global nano diamond market with a 42.6% share in 2025, equivalent to USD 810 Million, anchored by Chinese semiconductor manufacturing polishing demand, Japanese precision engineering applications, and South Korean advanced materials adoption programs across electronics and automotive sectors.

Competitive Landscape

The global nano diamond market is moderately fragmented in 2025, with the top four producers collectively holding an estimated 48–52% of global market revenue. Competition is primarily technology-driven, with differentiation based on nanodiamond purity, particle size distribution consistency, surface functionalization capability, and application-specific technical service depth. The market is experiencing increasing competitive intensity from Chinese detonation synthesis producers who are expanding capacity and competing aggressively on price in industrial-grade segments, while European and North American specialty producers are concentrating on higher-margin pharmaceutical, quantum, and semiconductor-grade nanodiamond products that require stringent quality certifications. Strategic M&A activity accelerated between 2024 and 2026 as established players sought to acquire application-specific nanodiamond technology capabilities and geographic distribution reach.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

|---|---|---|---|---|---|

| Carbodeon Ltd. | Finland | Leader | UDD Nanodiamonds | Europe / Asia Pacific | Expanded polymer composite product line, Jan 2025 |

| Adamas Nanotechnologies | USA | Leader | ND Fluorescent Particles | North America | Launched biomedical ND platform, Mar 2025 |

| NanoCarbon Research Institute | Russia | Leader | Detonation ND Powders | Europe / MEA | Capacity expansion in Siberia, Feb 2025 |

| PlasmaChem GmbH | Germany | Leader | Nano Diamond Suspensions | Europe | Partnership with BASF for lubricant ND, Nov 2024 |

| Ray Techniques Ltd. | Israel | Challenger | Synthetic ND Abrasives | Middle East / Europe | New HPHT synthesis line commissioned, Apr 2025 |

| Microdiamant AG | Switzerland | Challenger | ND Polishing Compounds | Europe / North America | Acquired US distributor, Jun 2025 |

| Van Moppes | Switzerland | Challenger | Diamond Abrasive Powders | Europe | Expanded Asia Pacific distribution, Sep 2025 |

| Beijing Grish Hitech Co. | China | Niche Player | ND Polishing Slurry | Asia Pacific | New production facility, Hebei, Jan 2026 |

| Henan Yuxing Abrasives | China | Niche Player | ND Superabrasive Grains | Asia Pacific | Expanded capacity for semiconductor sector, Mar 2025 |

| International Technology Center | USA | Niche Player | ND Lubricant Additives | North America | Phase II DoD research contract, Oct 2025 |

Segmentation Analysis

The nano diamond market segmentation analysis covers four key dimensions: By Production Method, By Application, By End-User Industry, and By Particle Size. Each dimension reveals distinct technology requirements, pricing structures, and competitive dynamics that define the global nano diamond market through 2034.

By Production Method

Detonation synthesis is the dominant production method in the nano diamond market, accounting for 58.6% of production method segment revenue in 2025 at USD 1.1 Billion. Detonation nanodiamonds are produced by detonating oxygen-deficient explosives in a closed chamber, generating extreme pressure and temperature conditions that convert carbon within the explosive to nanodiamond particles in the 4–6 nanometer primary particle size range. The detonation method produces nanodiamonds at relatively low cost, with large-scale Russian producers including the NanoCarbon Research Institute achieving production costs below USD 100 per kilogram for crude detonation nanodiamond soot. Russia accounts for approximately 65% of global detonation nanodiamond production capacity, with Chinese producers representing a growing secondary production base. The detonation segment supplies the majority of industrial polishing, lubricant additive, and polymer composite applications where cost competitiveness is a primary purchasing criterion.

High-pressure high-temperature synthesis accounts for 24.8% of production method revenue in 2025 at USD 471 Million. HPHT nanodiamonds are produced by converting graphite or other carbon precursors under pressures exceeding 5 gigapascals and temperatures above 1,300 degrees Celsius, generating larger nanodiamond particles with higher crystalline perfection than detonation products. HPHT nanodiamonds are preferred for precision polishing applications requiring consistent particle size distributions and for optical applications where crystal quality is critical. Chemical vapor deposition nanodiamonds represent 16.6% of the production method segment at USD 315 Million in 2025, used primarily in quantum technology applications where nitrogen-vacancy center density and optical purity requirements exceed the capabilities of detonation or HPHT methods. CVD-produced nanodiamonds command premium pricing of USD 5,000–25,000 per kilogram, reflecting the high production cost and specialized application markets they serve.

By Application

Polishing and abrasive applications dominate the nano diamond market with a 38.4% share in 2025 at USD 730 Million. Nanodiamond polishing compounds and slurries are used in semiconductor wafer chemical mechanical planarization, precision optical component finishing, hard disk substrate polishing, and gemstone processing. The semiconductor application is the primary growth engine within polishing, driven by the transition to advanced node logic and memory devices where sub-nanometer surface roughness requirements can only be achieved with nanodiamond-based polishing media. Leading semiconductor manufacturers including TSMC, Samsung, and Intel specify nanodiamond polishing compounds in their advanced node wafer preparation processes, creating concentrated demand from the global semiconductor supply chain. Nanodiamond polishing compounds offer superior material removal rate consistency and lower defect generation compared to conventional cerium oxide and silica polishing slurries in advanced node applications.

Lubricant additives represent 24.6% of nano diamond market application revenue in 2025 at USD 467 Million. Nanodiamond particles added to engine oils, gear lubricants, and industrial greases at concentrations of 0.05–0.5 weight percent create protective films on metal contact surfaces through tribochemical reactions that reduce friction coefficients by 15–40% and extend component wear life by 2–5 times compared to conventional lubricant additives. The automotive sector is the largest lubricant additive end market, with nanodiamond engine oil formulations gaining commercial traction in premium automotive and high-performance marine applications. Polymer and composite reinforcement applications account for 16.8% of application revenue at USD 319 Million in 2025, with nanodiamond-reinforced polymers demonstrating 30–60% improvement in tensile strength and thermal conductivity compared to unfilled polymer matrices. Biomedical applications hold 12.4% at USD 236 Million in 2025, and quantum technology applications represent 7.8% at USD 148 Million, with both segments growing significantly faster than the overall nano diamond market.

By End-User Industry

The electronics and semiconductor industry is the largest end-user of nano diamond market products, accounting for 34.6% of end-user segment revenue in 2025 at USD 657 Million. Semiconductor fabrication consumes nanodiamonds primarily as polishing media in chemical mechanical planarization steps for advanced logic and memory wafer processing, with demand growing in direct proportion to semiconductor capital expenditure programs and the transition to smaller process nodes. The electronics segment also includes hard disk drive substrate polishing and advanced packaging substrate finishing, which require nanodiamond compounds with tightly controlled particle size distributions to achieve required surface smoothness specifications. Asia Pacific dominates electronics sector nanodiamond consumption, reflecting the geographic concentration of semiconductor manufacturing in Taiwan, South Korea, Japan, and China.

The automotive industry represents 22.4% of nano diamond end-user market revenue in 2025 at USD 426 Million, consuming nanodiamonds primarily as engine oil and transmission fluid additives that improve fuel efficiency and drivetrain component longevity. Major automotive lubricant brands including Shell, Castrol, and Mobil have commercialized nanodiamond-additive oil formulations in premium product tiers. The healthcare and life sciences sector accounts for 16.2% of end-user revenue at USD 308 Million in 2025, encompassing drug delivery research, medical device coating, and diagnostic imaging applications. Defense and aerospace applications hold 14.8% at USD 281 Million in 2025, with nanodiamond applications in quantum sensing, thermal management coatings, and wear-resistant component treatments across military and aerospace programs. Other industrial applications including cutting tools, thermal interface materials, and electroplating represent the remaining 12.0% at USD 228 Million in 2025.

By Particle Size

The 2–5 nanometer particle size range is the dominant category in the nano diamond market by particle size, representing 52.4% of size segment revenue in 2025 at USD 996 Million. This size range corresponds to the primary particle output of detonation synthesis and is optimal for polishing applications, lubricant additives, and polymer composite reinforcement where small particle size maximizes surface area interaction and minimizes surface roughness contribution. Detonation nanodiamonds in this size range are the most commercially mature and cost-competitive category, with the broadest application base across industrial and advanced technology markets. Particle aggregation in this size range remains a technical challenge, with surface functionalization chemistry representing a critical differentiator among suppliers in achieving stable dispersions for polishing slurry and lubricant additive applications.

The 5–10 nanometer size range accounts for 30.6% of the particle size segment in 2025 at USD 581 Million, preferred for precision polishing applications requiring more controlled material removal rates and for quantum technology applications where larger crystal volumes provide higher nitrogen-vacancy center densities for sensing applications. Particles above 10 nanometers represent 17.0% of the market at USD 323 Million in 2025, used in abrasive grinding applications, electroplating, and composite reinforcement programs where particle size contributes to mechanical interlocking and load-bearing performance rather than surface area chemistry effects.

Regional Analysis

Asia Pacific Nano Diamond Market

Asia Pacific leads the global nano diamond market with a 42.6% share in 2025, equivalent to USD 810 Million. China is the dominant country market, accounting for approximately 54% of Asia Pacific revenue, driven by the world's largest semiconductor manufacturing expansion program, growing automotive lubricant additive adoption, and the Chinese government's strategic investment in advanced nanomaterial production capabilities. China's semiconductor self-sufficiency initiative has accelerated domestic nanodiamond polishing slurry procurement, with SMIC, Yangtze Memory Technologies, and ChangXin Memory Technologies specifying nanodiamond compounds for their advanced DRAM and NAND fabrication processes. Domestic Chinese producers including Beijing Grish Hitech and Henan Yuxing Abrasives are expanding their nanodiamond production capacities to capture this growing domestic semiconductor demand.

Japan is the second-largest Asia Pacific nano diamond market, contributing approximately 22% of regional revenue in 2025. Japanese precision engineering companies including Nikon, Canon, and Sumitomo Electric are significant consumers of nanodiamond polishing compounds for optical lens finishing and semiconductor equipment component processing. Japan's quantum technology initiative, supported by the Cabinet Office's Quantum Technology and Innovation Strategy, is directing investment toward nitrogen-vacancy nanodiamond quantum sensing research programs at institutions including RIKEN and the National Institute for Materials Science. South Korea represents approximately 16% of regional revenue, driven by Samsung and SK Hynix semiconductor manufacturing polishing demand and LG's automotive lubricant additive research programs. Asia Pacific is projected to grow at a CAGR of 13.8% through 2034, maintaining its position as the largest and fastest-growing regional nano diamond market.

North America Nano Diamond Market

North America holds a 26.4% share of the global nano diamond market in 2025, equivalent to USD 502 Million. The United States is the dominant country market, with nanodiamond demand concentrated in semiconductor fabrication polishing applications, defense and quantum technology research programs, and biomedical research applications. The U.S. CHIPS and Science Act, which allocated USD 52.7 Billion for domestic semiconductor manufacturing expansion, is driving capital expenditure at Intel, TSMC Arizona, Samsung Texas, and Micron facilities that will generate sustained demand growth for nanodiamond polishing consumables through the forecast period. The U.S. Department of Defense's quantum sensing research programs, including investments through DARPA's quantum information science initiative, represent a growing procurement channel for high-purity nitrogen-vacancy nanodiamond particles.

U.S.-based nanodiamond companies including Adamas Nanotechnologies and International Technology Center are developing biomedical and quantum-grade nanodiamond products that command premium pricing and target high-value specialty market segments beyond the industrial applications that dominate Asian and European demand. Canada contributes approximately 14% of North American nano diamond market revenue in 2025, with nanodiamond adoption in oil sands drilling fluid lubrication and automotive component manufacturing programs. Mexico represents a smaller but growing market as its automotive manufacturing sector adopts nanodiamond lubricant additives for domestic production programs. North America is projected to grow at a CAGR of 11.6% through 2034, with quantum technology and biomedical applications providing high-growth incremental demand above the steady base of semiconductor and automotive consumption.

Europe Nano Diamond Market

Europe accounts for 20.4% of the global nano diamond market in 2025, generating USD 388 Million in revenue. Germany leads the European segment, with nanodiamond demand driven by the country's precision engineering, automotive, and chemical industries. German chemical companies including BASF are incorporating nanodiamond lubricant additives into automotive and industrial lubricant product formulations, while Bosch, Continental, and ZF Friedrichshafen evaluate nanodiamond-enhanced coatings for precision automotive components. Finland is a significant nano diamond market contributor through Carbodeon, one of Europe's most technically advanced nanodiamond manufacturers, which supplies ultra-dispersed diamond products to European and Asian polymer composite and lubricant additive customers.

Switzerland contributes through Microdiamant AG and Van Moppes, both established precision diamond abrasive manufacturers with significant nanodiamond polishing compound product lines serving European precision optics and semiconductor equipment industries. Germany's PlasmaChem GmbH is a leading European supplier of functionalized nanodiamond suspensions for research and specialty application markets. The European Union's Horizon Europe program has directed significant research funding toward nanodiamond quantum technology applications, supporting consortium projects at universities and research institutes across Germany, France, and the Netherlands that are advancing nitrogen-vacancy nanodiamond quantum sensing toward commercial applications. Europe is projected to grow at a CAGR of 11.2% through 2034.

Middle East & Africa Nano Diamond Market

The Middle East and Africa region holds a 6.2% share of the global nano diamond market in 2025, totaling USD 118 Million. Israel is the dominant country market within the region, with Ray Techniques Ltd. operating as a regional leader in HPHT synthetic nanodiamond production for abrasive applications, and several Israeli defense technology companies incorporating nanodiamond materials into quantum sensing and thermal management programs for defense applications. Israel's advanced manufacturing sector, anchored by its semiconductor and precision optics industries, is a growing consumer of nanodiamond polishing and surface treatment products.

The UAE is investing in nanomaterial research and production as part of its industrial diversification strategy, with government-backed research institutions at Masdar City and Khalifa University conducting nanodiamond application research. Saudi Arabia's NEOM project and industrial diversification programs include advanced materials manufacturing components that present longer-term nanodiamond application opportunities in construction composites and precision manufacturing. South Africa hosts diamond mining operations whose fine diamond byproduct streams are increasingly being evaluated as nanodiamond precursor materials, potentially enabling Southern African nano diamond production capacity development. The Middle East and Africa region is projected to grow at a CAGR of 13.4% through 2034, supported by Israel's technology sector and Gulf region industrial diversification investment.

Latin America Nano Diamond Market

Latin America accounts for 4.4% of the global nano diamond market in 2025, totaling USD 84 Million. Brazil is the dominant country market, driven by its automotive manufacturing sector's adoption of nanodiamond lubricant additives, its growing semiconductor and electronics assembly industry consuming nanodiamond polishing materials, and university research programs in Rio de Janeiro and São Paulo investigating nanodiamond biomedical applications. Brazil's automotive sector, the largest in Latin America, represents the primary commercial nano diamond demand channel, with multinational automotive lubricant manufacturers including Shell and Castrol distributing nanodiamond-additive oil products through the Brazilian aftermarket channel.

Mexico contributes through its large automotive manufacturing base, which is the world's seventh-largest vehicle producer, creating industrial lubricant additive demand for nanodiamond products applied in transmission and drivetrain component manufacturing processes. Argentina's precision engineering and scientific instrument manufacturing sectors represent niche nanodiamond polishing compound consumption. The region's pharmaceutical and biomedical research community, particularly in Brazil, is actively investigating nanodiamond drug delivery applications through academic and public health research programs, though commercial biomedical nanodiamond consumption remains in early developmental stages. Latin America is projected to grow at a CAGR of 10.8% through 2034.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Production Method

- Detonation Synthesis

- High-Pressure High-Temperature (HPHT) Synthesis

- Chemical Vapor Deposition (CVD)

By Application

- Polishing and Abrasives

- Lubricant Additives

- Polymer and Composite Reinforcement

- Biomedical (Drug Delivery, Imaging)

- Quantum Technology (Nitrogen-Vacancy Sensing)

By End-User Industry

- Electronics and Semiconductor

- Automotive

- Healthcare and Life Sciences

- Defense and Aerospace

- Other Industrial

By Particle Size

- 2–5 nm

- 5–10 nm

- Above 10 nm

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 1.9 B |

| Forecast Revenue (2034) | USD 5.4 B |

| CAGR (2025-2034) | 12.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Production Method (Detonation Synthesis, High-Pressure High-Temperature (HPHT) Synthesis, Chemical Vapor Deposition (CVD)), By Application (Polishing and Abrasives, Lubricant Additives, Polymer and Composite Reinforcement, Biomedical (Drug Delivery, Imaging), Quantum Technology (Nitrogen-Vacancy Sensing)), By End-User Industry (Electronics and Semiconductor, Automotive, Healthcare and Life Sciences, Defense and Aerospace, Other Industrial), By Particle Size (2–5 nm, 5–10 nm, Above 10 nm) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | CARBODEON LTD., ADAMAS NANOTECHNOLOGIES INC., NANOCARBON RESEARCH INSTITUTE, PLASMACHEM GMBH, RAY TECHNIQUES LTD., MICRODIAMANT AG, VAN MOPPES, BEIJING GRISH HITECH CO., LTD., HENAN YUXING ABRASIVES CO., LTD., INTERNATIONAL TECHNOLOGY CENTER, SP3 DIAMOND TECHNOLOGIES, ELEMENT SIX (DE BEERS GROUP), SANDVIK AB, SAINT-GOBAIN SURFACE CONDITIONING, HYPERION MATERIALS & TECHNOLOGIES, RICH STONE LIMITED, ZHENGZHOU SINO-CRYSTAL DIAMOND CO., LTD., Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Polishing & Abrasives, Lubricant Additives, Polymer & Composite Reinforcement, Biomedical Drug Delivery & Imaging, Quantum Technology NV-Center Sensing), By End-User Industry (Electronics & Semiconductor, Automotive, Healthcare & Life Sciences, Defense & Aerospace, Industrial), By Particle Size (2–5 nm, 5–10 nm, Above 10 nm) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

, By Application (Polishing & Abrasives, Lubricant Additives, Polymer & Composite Reinforcement, Biomedical Drug Delivery & Imaging, Quantum Technology NV-Center Sensing), By End-User Industry (Electronics & Semiconductor, Automotive, Healthcare & Life Sciences, Defense & Aerospace, Industrial), By Particle Size (2–5 nm, 5–10 nm, Above 10 nm) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

, By Application (Polishing & Abrasives, Lubricant Additives, Polymer & Composite Reinforcement, Biomedical Drug Delivery & Imaging, Quantum Technology NV-Center Sensing), By End-User Industry (Electronics & Semiconductor, Automotive, Healthcare & Life Sciences, Defense & Aerospace, Industrial), By Particle Size (2–5 nm, 5–10 nm, Above 10 nm) Industry Region & Key Players – Market Dynamics, Competitive Landscape, Innovation Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Nano Diamond Market?

The Global Nano Diamond Market was valued at USD 1.9 Billion in 2025, projected to reach USD 5.4 Billion by 2034 at a CAGR of 12.4% from 2026–2034. Growth is driven by rising applications in nanotechnology, biomedical drug delivery, advanced coatings, electronics, and high-precision polishing solutions across multiple industries.

Who are the major players in the Nano Diamond Market?

CARBODEON LTD., ADAMAS NANOTECHNOLOGIES INC., NANOCARBON RESEARCH INSTITUTE, PLASMACHEM GMBH, RAY TECHNIQUES LTD., MICRODIAMANT AG, VAN MOPPES, BEIJING GRISH HITECH CO., LTD., HENAN YUXING ABRASIVES CO., LTD., INTERNATIONAL TECHNOLOGY CENTER, SP3 DIAMOND TECHNOLOGIES, ELEMENT SIX (DE BEERS GROUP), SANDVIK AB, SAINT-GOBAIN SURFACE CONDITIONING, HYPERION MATERIALS & TECHNOLOGIES, RICH STONE LIMITED, ZHENGZHOU SINO-CRYSTAL DIAMOND CO., LTD., Others

Which segments covered the Nano Diamond Market?

By Production Method (Detonation Synthesis, High-Pressure High-Temperature (HPHT) Synthesis, Chemical Vapor Deposition (CVD)), By Application (Polishing and Abrasives, Lubricant Additives, Polymer and Composite Reinforcement, Biomedical (Drug Delivery, Imaging), Quantum Technology (Nitrogen-Vacancy Sensing)), By End-User Industry (Electronics and Semiconductor, Automotive, Healthcare and Life Sciences, Defense and Aerospace, Other Industrial), By Particle Size (2–5 nm, 5–10 nm, Above 10 nm)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date