- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Nano Encapsulation Market Size, Share & Forecast | CAGR 11.4%

Global Nano Encapsulation Market Size, Share, Growth Analysis By Material Type (Lipid-Based Nanocapsules, Polymeric Nanocapsules, Inorganic Nanocapsules, Cyclodextrin Inclusion Complexes, Biopolymer-Based Nanocapsules), By Application (Pharmaceuticals, Food & Beverage, Personal Care & Cosmetics, Agriculture, Industrial Applications), By Release Mechanism, By End-Use Industry, Competitive Landscape, Industry Trends & Forecast 2026-2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

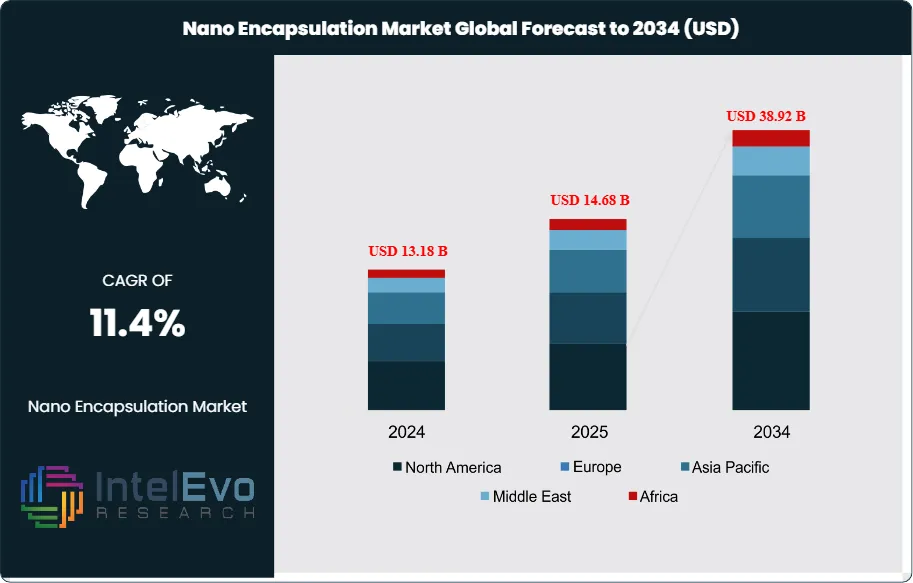

| USD 14.68 Billion | USD 38.92 Billion | 11.4% | North America, 35.8% |

The Nano Encapsulation Market was valued at approximately USD 13.18 Billion in 2024 and reached USD 14.68 Billion in 2025. The market is projected to grow to USD 38.92 Billion by 2034, expanding at a CAGR of 11.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 24.24 Billion over the analysis period, reflecting the broad and accelerating commercial deployment of nano encapsulation technology across pharmaceuticals, food and beverage, personal care, agriculture, and textiles.

Get More Information about this report -

Request Free Sample ReportNano encapsulation refers to the process of enclosing active substances — including drugs, nutrients, flavors, fragrances, pesticides, and bioactive compounds — within nanoscale polymeric, lipid, or inorganic shells ranging from 1 to 1,000 nanometers. The principal commercial benefit is controlled and targeted release: encapsulated actives are protected from environmental degradation, masked for taste or odor, and delivered to specific tissue targets or product zones with greater precision than conventional formulations. The pharmaceutical segment accounts for the largest share of the nano encapsulation market, holding 38.2% of global revenue in 2025 (USD 5.61 Billion), driven by the surge in lipid nanoparticle (LNP)-based drug delivery following the commercial validation of LNP technology in mRNA vaccines for COVID-19. LNP-enabled mRNA therapeutics in oncology, rare diseases, and infectious disease prevention are now a defined segment of the global pharmaceutical pipeline, and each new application drives incremental demand for nano encapsulation material inputs and process development services.

The food and beverage industry represents the second largest application vertical, capturing 26.4% of nano encapsulation market revenue in 2025 (USD 3.88 Billion). Encapsulation of omega-3 fatty acids, probiotics, vitamins, and natural colorants addresses the dual challenge of product stability and clean-label formulation, both of which are under intense retailer and regulatory scrutiny. The EU's Farm to Fork Strategy and the FDA's guidance on bioactive ingredient stability in fortified foods have created a regulatory environment that rewards encapsulation-enabled formulation precision. In personal care and cosmetics, where nano encapsulation holds an 18.3% share in 2025 (USD 2.69 Billion), encapsulated retinol, peptides, and fragrance actives have become standard in premium skincare due to their documented efficacy advantages over conventional delivery formats.

AI-assisted formulation design is reducing nano encapsulation development timelines by an estimated 30 to 40% compared to traditional trial-and-error screening, by predicting polymer-active compatibility, shell permeability, and release kinetics from molecular simulation data. Supply chain diversification following post-pandemic disruptions has prompted several large consumer goods and pharmaceutical companies to dual-source nano encapsulation inputs and relocate critical formulation steps closer to end markets, benefiting North American and European toll-encapsulation service providers. North America held 35.8% of the global nano encapsulation market in 2025, supported by concentrated pharmaceutical investment and a deep base of food ingredient innovation companies. Asia Pacific held 28.6%, with China and India driving both volume demand in food fortification and expanding pharmaceutical API encapsulation capacity. The nano encapsulation market trajectory through 2034 reflects durable demand across multiple end-use sectors, with no single vertical controlling growth.

, By Application (Pharmaceuticals, Food & Beverage, Personal Care & Cosmetics, Agriculture, Industrial Applications), By Release Mechanism, By End-Use Industry, Competitive Landscape, Industry Trends & Forecast 2026-2034")

Key Takeaways

- Market Growth: The global nano encapsulation market is projected to grow from USD 14.68 Billion in 2025 to USD 38.92 Billion by 2034, at a CAGR of 11.4% during the forecast period 2026–2034.

- Segment Dominance: By material type, lipid-based nanocapsules led the nano encapsulation market in 2025 with a 41.3% revenue share, reflecting the commercial dominance of lipid nanoparticle (LNP) platforms in pharmaceutical drug delivery.

- Segment Dominance: By application, the pharmaceutical and biotechnology segment captured 38.2% of nano encapsulation market revenue in 2025 (USD 5.61 Billion), anchored by LNP-mediated nucleic acid therapeutics and targeted oncology drug delivery systems.

- Driver: Rapid expansion of mRNA therapeutics and nucleic acid drug pipelines drove nano encapsulation demand; over 380 LNP-formulated clinical programs were active globally as of 2025, each requiring nano encapsulation process development and material supply.

- Restraint: High manufacturing complexity and the absence of standardized nano encapsulation characterization methods under ICH and FDA guidelines added 15 to 22 months to regulatory approval cycles, constraining time-to-market for first-time nano-formulation entrants.

- Opportunity: The agricultural nano encapsulation segment, projected to reach USD 4.8 Billion by 2034 from USD 1.62 Billion in 2025, represents the largest underpenetrated growth opportunity as precision agriculture adoption and pesticide reduction mandates accelerate globally.

- Trend: Bio-based and biodegradable encapsulation materials — including zein, chitosan, and cellulose derivatives — accounted for 27.4% of new nano encapsulation product launches in 2025, a share projected to reach 48% by 2030 as sustainability mandates reshape procurement criteria across food and personal care verticals.

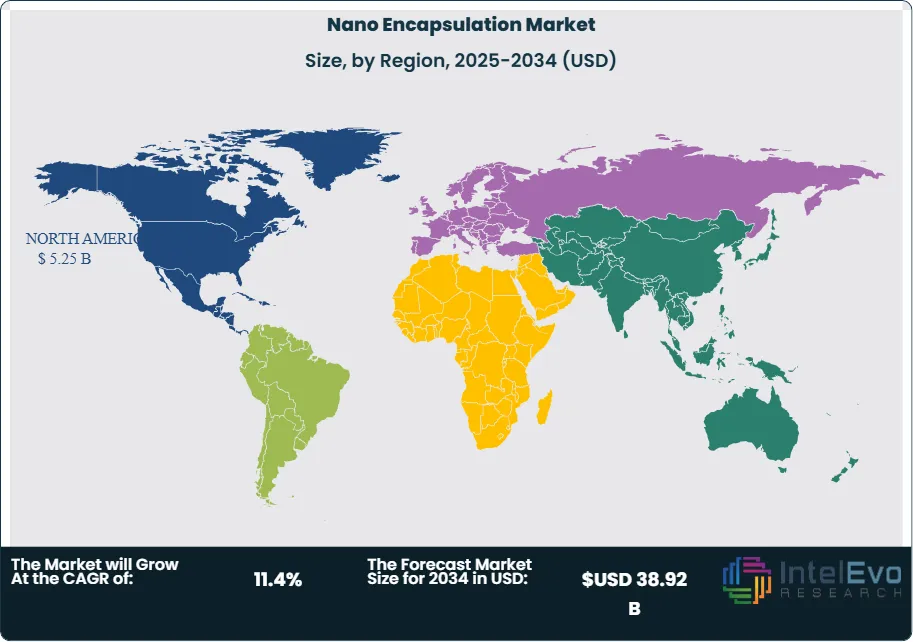

- Regional Analysis: North America dominated the nano encapsulation market in 2025 with a 35.8% share equating to USD 5.25 Billion in revenue, driven by pharmaceutical R&D concentration, food ingredient innovation investment, and a mature contract encapsulation services industry.

Competitive Landscape Overview

The nano encapsulation market is moderately fragmented, with the top four players — BASF SE, Encapsys LLC, Givaudan SA, and International Flavors and Fragrances (IFF) — collectively holding an estimated 34.6% combined revenue share in 2025. Competition is primarily technology-driven, with differentiation occurring across encapsulation shell material type, release mechanism (pH-triggered, temperature-activated, enzymatic, mechanical shear), particle size distribution control, and application-specific regulatory compliance credentials (FDA GRAS, EU Novel Food, ICH Q6A). M&A activity increased materially in 2024 to 2025 as large flavor and fragrance companies acquired specialty nano encapsulation IP to strengthen their controlled-release delivery portfolios in food and personal care markets.

Competitive Landscape Matrix

| Company Name | HQ (Country) | Market Position | Key Product/Platform | Geographic Strength | Recent Strategic Move |

| BASF SE | Germany | Leader | Encapsulated Aroma Systems (MicroPearls) | Europe | Jan 2025: launched BioEncap line of bio-based polymer nanocapsules for food and agri applications. |

| Encapsys LLC (Appvion) | USA | Leader | Thermo-Chromic Microcapsules | North America | Mar 2025: expanded North Carolina production capacity by 40% to meet food-grade encapsulation demand. |

| Givaudan SA | Switzerland | Leader | Actilease Delivery Systems | Europe | Feb 2025: acquired Vika Ingredients' encapsulation IP portfolio for USD 310 Million to deepen flavor delivery capabilities. |

| International Flavors & Fragrances (IFF) | USA | Challenger | Encapsulated Fragrance Beads | North America | Apr 2025: formed a joint venture with a South Korean materials firm to co-develop wash-activated encapsulated actives. |

| Ingredion Incorporated | USA | Challenger | Hi-Cap 100 Modified Starch Encapsulation | North America | Jun 2025: launched a plant-based encapsulation matrix targeting clean-label nutraceuticals. |

| Lonza Group | Switzerland | Niche Player | Capsugel Vcaps Plus (Hard-Shell NE) | Europe | May 2025: partnered with a pharma CDMO network to supply nano-encapsulated lipid formulation services for GLP-1 generics. |

| Balchem Corporation | USA | Niche Player | ReaShure Precision Release | North America | Nov 2024: signed a USD 45 Million supply agreement with a top-5 US animal nutrition company for rumen-protected encapsulates. |

| Symrise AG | Germany | Niche Player | SyMatrix Encapsulation Platform | Europe | Aug 2025: introduced cold-water-dispersible nano-encapsulated omega-3 system for functional beverage manufacturers. |

By Material Type

Lipid-based nanocapsules represent the dominant material type in the nano encapsulation market, accounting for 41.3% of global revenue in 2025 (USD 6.06 Billion). This category encompasses lipid nanoparticles (LNPs), solid lipid nanoparticles (SLNs), nanostructured lipid carriers (NLCs), liposomes, and nanoemulsions. Their commercial leadership reflects the pharmaceutical industry's adoption of LNP technology as the preferred delivery vehicle for nucleic acid therapeutics, including mRNA vaccines, siRNA drugs, and antisense oligonucleotides. Ionizable lipid chemistry — the core innovation enabling endosomal escape and cytoplasmic payload delivery — was successfully commercialized through COVID-19 mRNA vaccines and is now being applied to oncology, genetic disease, and cardiovascular indications. In food applications, nanoemulsions and liposomes encapsulate omega-3 fatty acids, curcumin, and fat-soluble vitamins with superior bioavailability versus unencapsulated formats, driving adoption among functional food and nutraceutical manufacturers seeking clinically validated efficacy claims. The lipid nano encapsulation sub-segment is projected to maintain above-average growth through 2034, supported by a pharmaceutical pipeline in which LNP-enabled modalities represent an estimated 18% of all drugs in Phase II and III clinical trials globally as of 2025.

Polymeric nanocapsules and nanoparticles represent the second largest material segment, holding 28.7% of nano encapsulation market revenue in 2025 (USD 4.21 Billion). Poly(lactic-co-glycolic acid) (PLGA), polyethylene glycol (PEG), chitosan, and zein are the most commercially deployed polymers, spanning pharmaceutical sustained-release formulations, agricultural controlled-release pesticides, and personal care active delivery. PLGA's FDA-approved status for biomedical use and its well-characterized biodegradation profile make it the default polymer for injectable sustained-release drug products. In agriculture, polymer encapsulation of herbicides and fungicides has demonstrated 25 to 40% reduction in active ingredient loading per hectare while maintaining efficacy, supporting both cost savings and environmental compliance with EU pesticide reduction targets under the European Green Deal's Farm to Fork Strategy. Chitosan-based nano encapsulation is expanding rapidly in food and nutraceuticals given its natural origin, antimicrobial properties, and mucoadhesive characteristics that enhance gastrointestinal bioavailability of encapsulated actives.

Inorganic nanocapsules — including silica, calcium phosphate, and carbon-based shells — accounted for 14.6% of nano encapsulation market revenue in 2025 (USD 2.14 Billion). Mesoporous silica nanoparticles (MSNs) with tunable pore architecture are applied in pharmaceutical research for on-demand drug release and theranostic platforms. Calcium phosphate nanocapsules serve as biocompatible mineral carriers for nucleic acids and proteins, with growing application in oral vaccine delivery. Cyclodextrin-based encapsulation systems held 9.2% of market share in 2025, widely used for solubility enhancement of poorly water-soluble drugs (BCS Class II and IV) and flavor stabilization in packaged food products. Biopolymer and protein-based nanocapsules — including zein, whey protein, and albumin nanoparticles — comprised the remaining 6.2%, primarily serving food and cosmetic applications where the encapsulant itself contributes functional or nutritional value to the final product.

By Application

Pharmaceuticals and biotechnology constitute the largest application segment in the nano encapsulation market, contributing 38.2% of global revenue in 2025 (USD 5.61 Billion). Drug delivery applications span oncology (targeted nanoparticle-antibody conjugates for tumor accumulation), nucleic acid therapeutics (LNP-formulated mRNA, siRNA, and plasmid DNA), transdermal drug delivery (polymeric nanoparticles for enhanced skin penetration), and oral bioavailability enhancement for BCS Class II drugs. The FDA's Nanotechnology Interest Group within CDER has processed 39% more nano-formulated IND applications between 2022 and 2025 compared to the preceding three-year period, indicating accelerating pipeline activity. The shift toward precision medicine and personalized dosing further drives nano encapsulation demand, as patient-specific formulation requires fine-grained release profile control only achievable through nanoscale encapsulation architecture. CDMO capacity for LNP manufacturing has expanded by an estimated 55% globally between 2022 and 2025, with Lonza, Samsung Biologics, and specialized lipid formulation CDMOs leading investment in new suite installations.

Food and beverage applications captured 26.4% of the nano encapsulation market in 2025 (USD 3.88 Billion). Key encapsulated actives include omega-3 fatty acids (DHA and EPA), probiotics, vitamins D and B12, iron, zinc, natural colorants such as anthocyanins and beta-carotene, and flavor compounds. Encapsulation solves two persistent formulation challenges: it masks off-flavors from functional ingredients such as fish oil and plant proteins, and it protects labile compounds from oxidation, heat, and light degradation during processing and shelf life. The global functional food and beverage market exceeded USD 285 Billion in 2025, with encapsulated ingredient formats commanding a 12 to 18% price premium over unencapsulated equivalents in retail SKUs. Clean-label requirements are reshaping material selection within this sub-segment, with modified starch, cellulose, and protein-based shells displacing synthetic polymer carriers in new product development programs across North America and Europe.

Personal care and cosmetics represented 18.3% of nano encapsulation market revenue in 2025 (USD 2.69 Billion). Encapsulated retinol (vitamin A), vitamin C derivatives, peptides, hyaluronic acid, and fragrances are standard formulation components in anti-aging skincare, with encapsulation documented to increase retinol skin penetration by 2 to 4 times versus unencapsulated formats in controlled clinical studies. Encapsulated fragrance in laundry care products — released upon mechanical friction during wear — is the largest single personal care application by volume. Agricultural nano encapsulation held 11.0% market share in 2025 (USD 1.62 Billion), with the remainder distributed across textiles (phase-change material encapsulation for thermal comfort garments), electronics (encapsulated adhesives and conductive inks), and nutraceuticals sold outside food retail channels.

By End-Use Industry

The pharmaceutical and life sciences industry dominated nano encapsulation end-use demand in 2025, accounting for 40.1% of global market revenue. This figure includes not only finished drug product encapsulation but also upstream demand from contract research organizations (CROs), CDMOs, and academic biotech spinouts conducting preclinical and clinical formulation development. The food, beverage, and nutraceutical industry represented 28.3% of end-use demand in 2025, with the largest buyers being global consumer goods companies running functional food and fortified beverage portfolios. The personal care and homecare industry accounted for 19.4% of end-use demand, with premium skincare brands and multinational home care manufacturers representing the highest-volume purchasers of encapsulated actives and fragrances. Agricultural end-users contributed 8.6% of the nano encapsulation market in 2025, a share projected to grow materially as precision agriculture deployment accelerates across North America, Brazil, and Southeast Asia. Industrial and textile end-users collectively represented 3.6% of market revenue, a small but technically sophisticated segment anchored by specialty chemical and performance fabric manufacturers.

Regional Analysis

North America Nano Encapsulation Market

North America held the largest share of the global nano encapsulation market in 2025 at 35.8%, representing USD 5.25 Billion in revenue. The United States accounted for approximately 88% of regional demand, with pharmaceutical LNP formulation services and food ingredient encapsulation driving the bulk of spending. The concentration of LNP-focused CDMOs and biotechnology companies in the Boston-Cambridge corridor, San Francisco Bay Area, and Research Triangle has established a dense commercial supply chain for lipid encapsulation materials, ionizable lipid synthesis, and encapsulation process development. The FDA's Center for Drug Evaluation and Research (CDER) has provided regulatory clarity on LNP characterization requirements through its 2024 guidance on complex drug substances, reducing formulation development uncertainty and accelerating IND submissions. In the food sector, the FDA's GRAS notification process for novel encapsulation materials has facilitated commercialization of clean-label chitosan and zein carriers, with over 22 GRAS notices related to nano-encapsulated food ingredients filed between 2022 and 2025. Canada contributed approximately 9% of North American nano encapsulation market revenue, with activity concentrated in functional food fortification and agricultural controlled-release inputs. Mexico represented approximately 3%, primarily through pharmaceutical manufacturing facilities supplying encapsulated APIs for North American brand owners. North America's nano encapsulation market is expected to grow at a 10.6% CAGR through 2034, slightly below the global average, as the region transitions from growth phase to maturity in pharmaceutical LNP applications while agricultural encapsulation expands.

Europe Nano Encapsulation Market

Europe represented 23.4% of the global nano encapsulation market in 2025 with USD 3.44 Billion in revenue. Germany led the regional market, driven by BASF's encapsulation materials business, the country's strong food ingredient manufacturing base, and pharmaceutical formulation investment from companies including Bayer and Merck KGaA. The EU's Novel Food Regulation (EU 2015/2283) and the Farm to Fork Strategy's 2030 targets — which include a 50% reduction in pesticide use and a 50% reduction in sales of antimicrobials — are providing strong regulatory pull for nano encapsulation in both the food and agricultural sectors. Switzerland held the second largest European position in nano encapsulation market revenue in 2025 through Givaudan and Lonza's encapsulation businesses, the latter supplying lipid formulation development services to European pharmaceutical and biotech clients. France contributed approximately 14% of European nano encapsulation revenue, with INRAE (National Research Institute for Agriculture, Food and Environment) sustaining active encapsulation research programs that feed into commercial partnerships. The UK maintained meaningful nano encapsulation market activity through university-spinout companies focusing on siRNA delivery and agricultural encapsulation, supported by Innovate UK grant funding. REACH regulation requirements and the EU's nanomaterial transparency initiative (mandatory disclosure of nano-ingredients in cosmetics and food under EU 1169/2011) have elevated manufacturing standards across the region, differentiating compliant European suppliers in international procurement.

Asia Pacific Nano Encapsulation Market

Asia Pacific held 28.6% of the global nano encapsulation market in 2025 (USD 4.20 Billion) and is the fastest-growing region, projected at a 13.8% CAGR through 2034. China accounted for approximately 48% of regional revenue, with state-backed investment in pharmaceutical nano-formulation capacity under the 14th Five-Year Plan and rapidly expanding domestic nutraceutical and functional food markets driving demand. China's National Medical Products Administration (NMPA) issued revised guidelines on nano-drug characterization in 2024, providing a clearer regulatory framework for LNP and polymeric nanoparticle-based IND applications, which has attracted foreign CDMO investment in China-based nano encapsulation facilities. India represented approximately 17% of Asia Pacific nano encapsulation revenue in 2025, with the country's established generic pharmaceutical industry investing in nano-formulation capabilities to address BCS Class II drug bioavailability enhancement and compete for LNP CDMO contracts from North American and European innovators. Japan contributed approximately 16% of regional revenue, with its food technology sector representing a disproportionate share of activity: Japanese consumers' acceptance of functional food formats and willingness to pay premium prices for efficacy-demonstrated encapsulated ingredients make Japan a priority commercialization market for global encapsulation companies. South Korea contributed approximately 9% of regional revenue, with K-beauty's global expansion driving sustained demand for encapsulated retinol, peptide, and natural extract carriers in skincare product lines exported globally.

Latin America Nano Encapsulation Market

Latin America accounted for 7.4% of the global nano encapsulation market in 2025, equivalent to USD 1.09 Billion. Brazil dominated the regional market at approximately 56% of Latin American revenue, supported by its large food processing industry, growing nutraceuticals sector, and significant agricultural market where encapsulated pesticide and fertilizer inputs are in increasing demand under precision farming programs. Brazil's Empresa Brasileira de Pesquisa Agropecuaria (Embrapa) has conducted extensive research on nanoencapsulated agrochemical formulations tailored to tropical crop conditions, providing a knowledge base that supports commercial adoption by domestic agri-input distributors. The Brazilian Health Regulatory Agency (ANVISA) issued updated guidance on nanotechnology-based cosmetics and food ingredients in 2024, aligning local regulatory requirements more closely with EU frameworks and enabling international companies to register nano encapsulation-based products more efficiently. Mexico represented approximately 27% of Latin American revenue in 2025, with pharmaceutical manufacturing for both domestic consumption and North American export driving demand for GMP-grade encapsulation materials and services. Argentina contributed approximately 10% of regional nano encapsulation market revenue, with its pharmaceutical and food technology sectors sustaining steady demand. Latin America's nano encapsulation market is projected to grow at a 12.9% CAGR through 2034, with agricultural applications representing the largest incremental opportunity.

Middle East and Africa Nano Encapsulation Market

The Middle East and Africa region held 4.8% of the global nano encapsulation market in 2025 (USD 0.70 Billion), the smallest regional share but with a projected CAGR of 13.4% through 2034. The UAE is the most developed nano encapsulation market in the region, with Dubai's life sciences free zones and Abu Dhabi's health technology investment agenda attracting specialty pharmaceutical and nutraceutical companies requiring encapsulation-enabled formulation capabilities. Saudi Arabia's Vision 2030 healthcare initiative has directed capital toward domestic pharmaceutical manufacturing, with encapsulated drug delivery formats receiving specific attention in the government's import substitution strategy for complex formulations. South Africa anchors the Sub-Saharan segment, where nano encapsulation demand is primarily driven by the pharmaceutical generics industry and HIV/tuberculosis treatment program requirements for improved oral bioavailability formulations. The Egyptian pharmaceutical market, the largest in Africa by revenue, is experiencing early-stage adoption of nano encapsulation for oral and topical drug products as local manufacturers invest in formulation technology to compete against imported branded products. Food fortification programs supported by international agencies including WHO and the World Food Programme are creating institutional demand for encapsulated micronutrients — particularly iron, iodine, and vitamin A — in staple food vehicles across the region.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Material Type

- Lipid-Based Nanocapsules (LNPs, SLNs, NLCs, Liposomes, Nanoemulsions)

- Polymeric Nanocapsules (PLGA, PEG, Chitosan, Zein)

- Inorganic Nanocapsules (Silica, Calcium Phosphate, Carbon-Based)

- Cyclodextrin Inclusion Complexes

- Biopolymer / Protein-Based Nanocapsules

By Application

- Pharmaceuticals and Biotechnology

- Food and Beverage

- Personal Care and Cosmetics

- Agriculture

- Textiles and Industrial

By End-Use Industry

- Pharmaceutical and Life Sciences

- Food, Beverage, and Nutraceuticals

- Personal Care and Homecare

- Agriculture

- Industrial and Textiles

By Release Mechanism

- pH-Triggered Release

- Temperature-Activated Release

- Enzymatic Degradation Release

- Mechanical / Friction-Activated Release

- Diffusion-Controlled Sustained Release

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 14.68 B |

| Forecast Revenue (2034) | USD 38.92 B |

| CAGR (2025-2034) | 11.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Material Type, (Lipid-Based Nanocapsules (LNPs, SLNs, NLCs, Liposomes, Nanoemulsions), Polymeric Nanocapsules (PLGA, PEG, Chitosan, Zein), Inorganic Nanocapsules (Silica, Calcium Phosphate, Carbon-Based), Cyclodextrin Inclusion Complexes, Biopolymer / Protein-Based Nanocapsules), By Application, (Pharmaceuticals and Biotechnology, Food and Beverage, Personal Care and Cosmetics, Agriculture, Textiles and Industrial), By End-Use Industry, (Pharmaceutical and Life Sciences, Food, Beverage, and Nutraceuticals, Personal Care and Homecare, Agriculture, Industrial and Textiles), By Release Mechanism, (pH-Triggered Release, Temperature-Activated Release, Enzymatic Degradation Release, Mechanical / Friction-Activated Release, Diffusion-Controlled Sustained Release) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BASF SE, ENCAPSYS LLC (APPVION), GIVAUDAN SA, INTERNATIONAL FLAVORS AND FRAGRANCES (IFF), INGREDION INCORPORATED, LONZA GROUP, BALCHEM CORPORATION, SYMRISE AG, ROYAL DSM (DSM-FIRMENICH), EVONIK INDUSTRIES AG, CAPSUGEL (LONZA GROUP), LYCORED GROUP, FRIESLANDCAMPINA DOMO, BENEFIQ TECHNOLOGIES, DEGUSSA AG (EVONIK), AVEKA GROUP, SOUTHWEST RESEARCH INSTITUTE (SWRI), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Pharmaceuticals, Food & Beverage, Personal Care & Cosmetics, Agriculture, Industrial Applications), By Release Mechanism, By End-Use Industry, Competitive Landscape, Industry Trends & Forecast 2026-2034")

, By Application (Pharmaceuticals, Food & Beverage, Personal Care & Cosmetics, Agriculture, Industrial Applications), By Release Mechanism, By End-Use Industry, Competitive Landscape, Industry Trends & Forecast 2026-2034")

, By Application (Pharmaceuticals, Food & Beverage, Personal Care & Cosmetics, Agriculture, Industrial Applications), By Release Mechanism, By End-Use Industry, Competitive Landscape, Industry Trends & Forecast 2026-2034")

Frequently Asked Questions

How big is the Nano Encapsulation Market?

The Global Nano Encapsulation Market was valued at USD 13.18 Billion in 2024 and is projected to reach USD 38.92 Billion by 2034, growing at a CAGR of 11.4% from 2026 to 2034, driven by increasing demand in pharmaceuticals, food & beverages, nutraceuticals, cosmetics, and targeted drug delivery applications.

Who are the major players in the Nano Encapsulation Market?

BASF SE, ENCAPSYS LLC (APPVION), GIVAUDAN SA, INTERNATIONAL FLAVORS AND FRAGRANCES (IFF), INGREDION INCORPORATED, LONZA GROUP, BALCHEM CORPORATION, SYMRISE AG, ROYAL DSM (DSM-FIRMENICH), EVONIK INDUSTRIES AG, CAPSUGEL (LONZA GROUP), LYCORED GROUP, FRIESLANDCAMPINA DOMO, BENEFIQ TECHNOLOGIES, DEGUSSA AG (EVONIK), AVEKA GROUP, SOUTHWEST RESEARCH INSTITUTE (SWRI), Others

Which segments covered the Nano Encapsulation Market?

By Material Type, (Lipid-Based Nanocapsules (LNPs, SLNs, NLCs, Liposomes, Nanoemulsions), Polymeric Nanocapsules (PLGA, PEG, Chitosan, Zein), Inorganic Nanocapsules (Silica, Calcium Phosphate, Carbon-Based), Cyclodextrin Inclusion Complexes, Biopolymer / Protein-Based Nanocapsules), By Application, (Pharmaceuticals and Biotechnology, Food and Beverage, Personal Care and Cosmetics, Agriculture, Textiles and Industrial), By End-Use Industry, (Pharmaceutical and Life Sciences, Food, Beverage, and Nutraceuticals, Personal Care and Homecare, Agriculture, Industrial and Textiles), By Release Mechanism, (pH-Triggered Release, Temperature-Activated Release, Enzymatic Degradation Release, Mechanical / Friction-Activated Release, Diffusion-Controlled Sustained Release)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date