- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Nanopharmaceuticals Market Size, Share & Forecast | 14.4% CAGR

Global Nanopharmaceuticals Market Size, Share, Growth Analysis By Product Type (Liposomes, Polymeric Micelles, Solid Lipid Nanoparticles, Nanoemulsions, Microemulsions, Other Nanocarrier Systems), By Application (Cancer, Autoimmune Disorders, Inflammation, Infectious Diseases, Neurological Disorders, Cardiovascular Diseases), By End-User (Pharmaceutical Companies, Biotechnology Firms, Research Institutes) Industry Trends, Innovation Landscape, Competitive Analysis, Regional Insights & Forecast 2025–2034

Report Overview

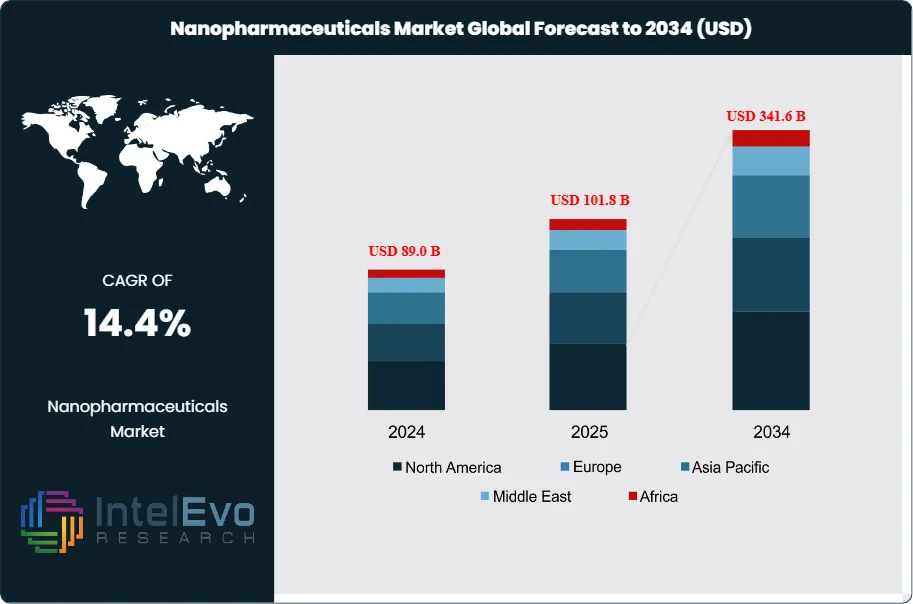

The Nanopharmaceuticals Market was valued at USD 89.0 Billion in 2024 and is estimated to reach approximately USD 101.8 Billion in 2025. With continued expansion driven by advancements in nanotechnology-based drug delivery systems, the market is projected to grow from around USD 116.5 Billion in 2026 to nearly USD 341.6 Billion by 2034, registering a compound annual growth rate (CAGR) of about 14.4% during the forecast period from 2026 to 2034.

Get More Information about this report -

Request Free Sample ReportNanopharmaceuticals apply nanobiotechnology to drug development and targeted delivery, including the use of nanoparticles as therapeutic agents. Demand continues to rise as health systems manage a higher load of chronic diseases, led by cancer, cardiovascular disease, and advanced liver conditions. Oncology represents an estimated 45% of 2024 revenue, supported by nano-enabled formulations that improve biodistribution and increase drug concentration at tumor sites while limiting off-target exposure. Injectable products account for about 55% of sales, reflecting hospital-based administration, predictable pharmacokinetics, and established reimbursement pathways, while oral nanoformulations expand as developers target adherence and long-term disease management.

Supply expansion tracks a stronger clinical pipeline and sustained R&D spending across large pharmaceutical companies and specialist biotechs. Firms scale lipid nanoparticles, polymeric nanoparticles, liposomes, and nanoemulsions to extend drug half-life and reduce systemic adverse events, which supports premium pricing in specialty indications. However, manufacturing and quality control remain binding constraints. Complex characterization, sterility assurance, and batch-to-batch consistency increase cost of goods and extend technology transfer cycles, which elevates the strategic value of advanced CDMOs and platform-based manufacturing partnerships.

Regulatory agencies apply tighter scrutiny as products move from trials into broader use. The U.S. FDA and EMA emphasize chemistry, manufacturing, and controls requirements, immunogenicity assessment, and post-market surveillance for nano-enabled therapies. These expectations raise compliance cost and can extend review cycles, but they also strengthen barriers to entry for firms with mature CMC capabilities. Key risks include unexpected safety signals related to nanotoxicity, supply-chain volatility for specialized lipids and polymers, IP fragmentation around platform components, and payer resistance when outcomes data fails to justify price premiums.

Technology investment is shifting competitive advantage. AI accelerates formulation screening, predicts stability, and improves candidate selection, while automation and digital quality systems tighten process control and release testing. North America holds roughly 38% of 2024 revenue due to mature biologics infrastructure and deep late-stage capital. Europe contributes about 27% through regulated manufacturing clusters, while Asia Pacific approaches 25% and leads growth at roughly 16% CAGR, with China, India, Singapore, and South Korea emerging as priority investment hotspots for scale-up capacity and clinical execution.

, By Application (Cancer, Autoimmune Disorders, Inflammation, Infectious Diseases, Neurological Disorders, Cardiovascular Diseases), By End-User (Pharmaceutical Companies, Biotechnology Firms, Research Institutes) Industry Trends, Innovation Landscape, Competitive Analysis, Regional Insights & Forecast 2025–2034")

Key Takeaways

- Market Growth: The market expands at estimated: 14.4% CAGR, 2026-2034, supported by broader clinical adoption and pipeline maturation. Total revenue reaches estimated: 89.0 billion USD, 2024.

- Segment Dominance : Liposomes lead by type and generate the highest revenue at estimated: 32.0% share, 2022. This leadership reflects established formulation know-how and scalable manufacturing at estimated: 21.6 billion USD, 2022.

- Segment Dominance: Cancer remains the largest application and accounts for 36.0% share, 2022. This demand concentrates spending in oncology at estimated: 24.3 billion USD, 2022.

- Driver: Developers push targeted delivery to improve efficacy and safety, lifting adoption by estimated: 11.0% year-over-year, 2024. Nanocarriers extend therapeutic performance with estimated: 18.0% improvement in drug half-life, 2024.

- Restraint: Complex characterization and GMP scale-up raise costs and delay launches by estimated: 9.0 months, 2024. Regulatory and quality requirements increase total development spend by estimated: 12.0% per program, 2024.

- Opportunity: Pharmaceutical companies remain the leading end users and drive commercialization at estimated: 52.0% share, 2022. Strategic investment accelerates platform pipelines by estimated: 2.8 billion USD, 2024.

- Trend: AI-enabled formulation screening and automated process control shorten development cycles by estimated: 15.0%, 2024. Digitalized quality systems reduce batch variability by estimated: 10.0%, 2024.

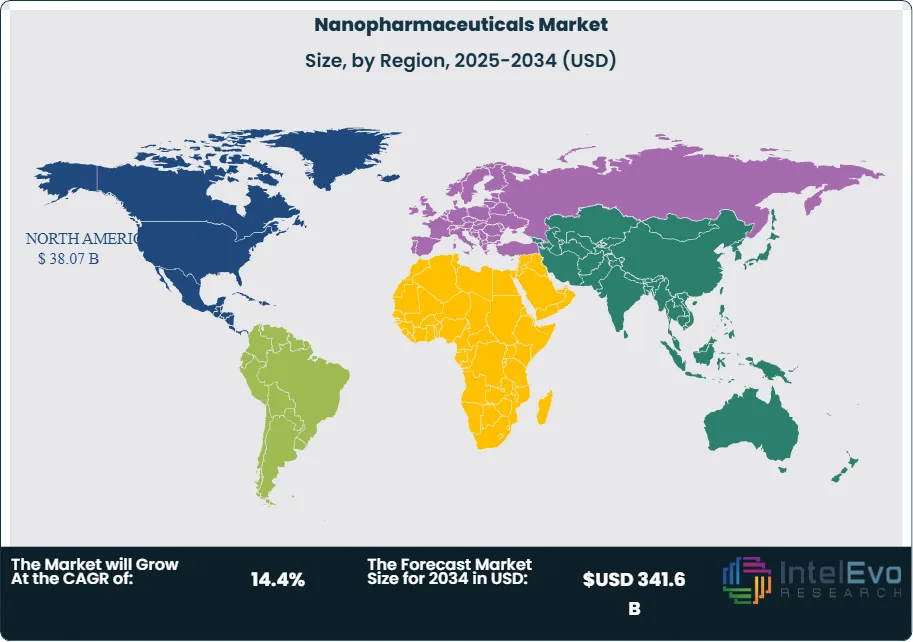

- Regional Analysis: North America leads regional revenue with 37.4% share, 2022, supported by strong reimbursement and manufacturing capacity. Asia Pacific posts the fastest growth at estimated: 16.0% CAGR, 2024-2034, with expanding clinical and CDMO ecosystems.

By Type

The nanopharmaceuticals market in 2025 remains strongly anchored in lipid- and polymer-based delivery platforms, with liposomes retaining the leading position by revenue contribution. Liposomes account for an estimated 30 to 35 percent of global market share, supported by decades of clinical validation and broad regulatory acceptance. Their phospholipid bilayer structure enables efficient encapsulation of both hydrophilic and hydrophobic drugs, which improves stability and circulation time. This makes liposomes a preferred choice for oncology, antifungal, and vaccine-related formulations, particularly in hospital-administered injectables.

Polymeric micelles represent a fast-growing category, expanding at an estimated CAGR of over 15 percent through 2034. These carriers rely on biodegradable polymers to enhance solubility and control drug release profiles, which supports their use in chronic and precision therapies. Pharmaceutical developers increasingly apply polymeric micelles to reduce systemic toxicity while maintaining therapeutic concentration at target sites. Their adoption continues to rise in cancer and autoimmune pipelines.

Solid lipid nanoparticles, nanoemulsions, and microemulsions play a complementary but increasingly strategic role. Solid lipid nanoparticles attract interest for their cellular penetration and controlled release, particularly in breast, lung, and hepatic cancers. Nanoemulsions and microemulsions support ocular, topical, oral, and intravenous delivery, with nanoemulsions widely used as precursors for nanocrystals of poorly soluble active ingredients. Together, these platforms strengthen formulation flexibility across complex drug portfolios.

By Application

Cancer remains the largest application area in the nanopharmaceuticals market, representing approximately 36 percent of total revenue in 2025. The segment continues to expand as global cancer incidence rises steadily, with annual new cases projected to exceed 20 million by the early 2030s. Nanopharmaceuticals improve tumor targeting, reduce off-target toxicity, and support combination therapies, which reinforces their clinical and commercial relevance in oncology.

Solid lipid nanoparticles and liposomal formulations demonstrate strong performance in treating breast, lung, liver, and colorectal cancers. These systems improve intracellular uptake and drug retention compared to conventional chemotherapies. As oncology pipelines shift toward targeted and biologic agents, nanocarriers increasingly serve as enabling technologies rather than optional add-ons.

Inflammation and autoimmune disorders form the second major application group. Nanopharmaceuticals support controlled immune modulation and sustained release, which improves outcomes in rheumatoid arthritis, inflammatory bowel disease, and dermatological conditions. Adoption in these indications grows at a mid-teens CAGR, driven by long-term therapy needs and demand for reduced adverse effects.

By End-Use

Pharmaceutical companies remain the dominant end users of nanopharmaceutical technologies in 2025, accounting for over half of total market demand. Large drug manufacturers integrate nanocarriers into branded and specialty drug pipelines to enhance bioavailability, extend patent life, and improve clinical differentiation. Precision delivery supports higher success rates in late-stage trials, which justifies sustained investment.

Biotechnological companies and research institutes represent the fastest-expanding end-user segment. Growth exceeds 16 percent annually as smaller firms focus on platform-based nanomedicine development and translational research. Academic and public-private collaborations play a key role in early-stage discovery and clinical validation, particularly in oncology and rare diseases.

By Region

North America continues to lead the global nanopharmaceuticals market with an estimated 37 to 38 percent share in 2025. Strong R&D funding, advanced regulatory frameworks, and the presence of major pharmaceutical players support early adoption and commercialization. The United States remains the primary contributor due to robust oncology pipelines and reimbursement structures.

Europe ranks second, driven by strong clinical research infrastructure in Germany, the United Kingdom, and France. Regulatory alignment across the region supports cross-border trials and manufacturing scale-up. Public funding for nanomedicine research remains a stabilizing factor.

Asia Pacific records the fastest growth rate through 2034, with an estimated CAGR above 16 percent. Rising cancer prevalence, expanding pharmaceutical manufacturing in China and India, and increased government investment accelerate market expansion. Latin America and the Middle East and Africa show slower growth, constrained by limited awareness, lower R&D intensity, and delayed adoption of advanced drug delivery technologies.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Product Type

- Liposomes

- Polymeric Micelles

- Solid Lipid Nanoparticles

- Microemulsion

- Nanoemulsion

- Other Product Types

By Application

- Cancer

- Autoimmune Disorders

- Inflammation

- Other Applications

By End-User

- Pharmaceutical Companies

- Biotechnological Companies

- Research Institutes

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 101.8 B |

| Forecast Revenue (2034) | USD 341.6 B |

| CAGR (2025-2034) | 14.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Product Type (Liposomes, Polymeric Micelles, Solid Lipid Nanoparticles, Microemulsion, Nanoemulsion, Other Product Types), By Application (Cancer, Autoimmune Disorders, Inflammation, Other Applications), By End-User (Pharmaceutical Companies, Biotechnological Companies, Research Institutes) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | Novartis AG, Pfizer Inc., Sanofi S.A., Eli Lilly, Hoffmann-La Roche Ltd., Abbott, Johnson & Johnson, Merck & Co., Inc., Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Cancer, Autoimmune Disorders, Inflammation, Infectious Diseases, Neurological Disorders, Cardiovascular Diseases), By End-User (Pharmaceutical Companies, Biotechnology Firms, Research Institutes) Industry Trends, Innovation Landscape, Competitive Analysis, Regional Insights & Forecast 2025–2034")

, By Application (Cancer, Autoimmune Disorders, Inflammation, Infectious Diseases, Neurological Disorders, Cardiovascular Diseases), By End-User (Pharmaceutical Companies, Biotechnology Firms, Research Institutes) Industry Trends, Innovation Landscape, Competitive Analysis, Regional Insights & Forecast 2025–2034")

, By Application (Cancer, Autoimmune Disorders, Inflammation, Infectious Diseases, Neurological Disorders, Cardiovascular Diseases), By End-User (Pharmaceutical Companies, Biotechnology Firms, Research Institutes) Industry Trends, Innovation Landscape, Competitive Analysis, Regional Insights & Forecast 2025–2034")

Frequently Asked Questions

How big is the Nanopharmaceuticals Market?

The Global Nanopharmaceuticals Market was valued at USD 89.0 Billion in 2024 and is projected to reach USD 341.6 Billion by 2034, growing at a CAGR of 14.4% from 2026–2034. Explore key trends in nanotechnology-based drug delivery, market drivers, innovations in nanomedicine, and future opportunities in the pharmaceutical industry.

Who are the major players in the Nanopharmaceuticals Market?

Novartis AG, Pfizer Inc., Sanofi S.A., Eli Lilly, Hoffmann-La Roche Ltd., Abbott, Johnson & Johnson, Merck & Co., Inc., Other Key Players

Which segments covered the Nanopharmaceuticals Market?

By Product Type (Liposomes, Polymeric Micelles, Solid Lipid Nanoparticles, Microemulsion, Nanoemulsion, Other Product Types), By Application (Cancer, Autoimmune Disorders, Inflammation, Other Applications), By End-User (Pharmaceutical Companies, Biotechnological Companies, Research Institutes)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date