- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Natural Gas Dehydration Equipment Market Forecast 2034 | CAGR 6.4%

Global Natural Gas Dehydration Equipment Market Size, Share, Growth & Industry Analysis By Technology (TEG Absorption, Molecular Sieve, Silica Gel/Alumina Desiccant, Refrigeration Dehydration), By Application (Midstream Processing & Pipelines, LNG Liquefaction, Upstream Gathering, Offshore FPSO), By Equipment Type (Absorber Columns, Reboilers, Adsorbent Vessels, Pumps, Controls), By Operation (Upstream, Midstream, Downstream/LNG) Industry Trends, Competitive Landscape & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

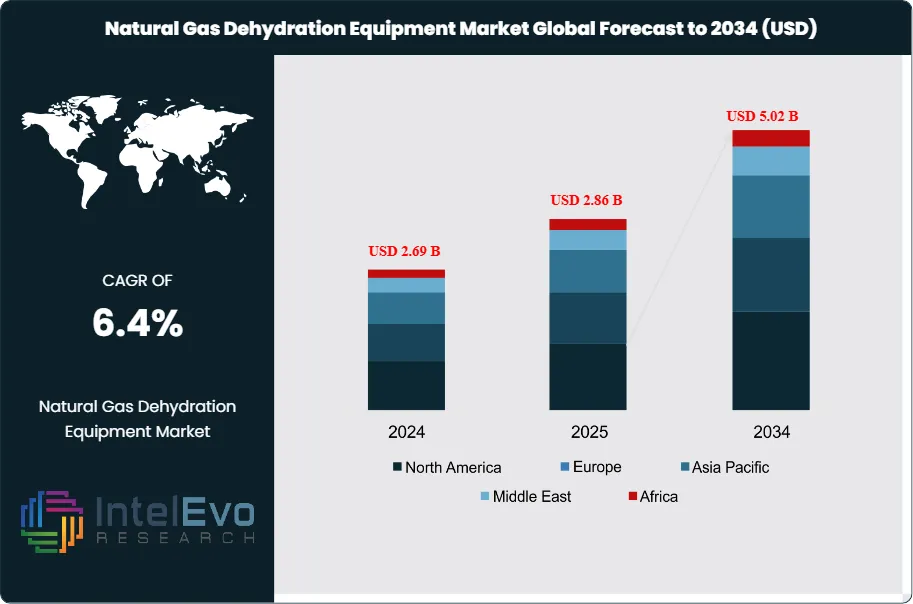

| USD 2.86 Billion | USD 5.02 Billion | 6.4% | North America, 41.2% |

The Natural Gas Dehydration Equipment Market was valued at approximately USD 2.69 Billion in 2024 and reached USD 2.86 Billion in 2025. The market is projected to grow to USD 5.02 Billion by 2034, expanding at a CAGR of 6.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 2.16 Billion over the analysis period, driven by rising natural gas production volumes, expanding LNG export infrastructure, and the tightening of gas quality specifications across transmission pipeline and processing operations worldwide.

Get More Information about this report -

Request Free Sample ReportNatural gas dehydration is a mandatory gas conditioning step in virtually every upstream, midstream, and LNG application. Raw wellhead gas contains water vapor at concentrations that, if untreated, would cause hydrate formation in high-pressure pipelines, corrosion of carbon steel transmission infrastructure, and condensation damage in cryogenic liquefaction processes. The Natural Gas Dehydration Equipment market encompasses the full range of technologies and hardware used to reduce the water content of gas streams to pipeline and process specifications — most commonly to a water dewpoint below minus 8 degrees Celsius for transmission gas per ASTM D1446 and GOST R 53367 standards, and to below minus 70 degrees Celsius for LNG feedgas per ISO 16903.

Triethylene glycol (TEG) absorption remains the dominant dehydration technology, accounting for approximately 58.4% of global dehydration equipment installations in 2025. TEG contactors, glycol circulation pumps, reboilers, and glycol regeneration systems constitute the core equipment package for the majority of midstream gas processing plants and offshore production facilities. The expansion of U.S. natural gas production — averaging 103 Bcf/d in 2025 per EIA data — continues to drive significant capital investment in field dehydration across the Permian Basin, Haynesville, and Marcellus/Utica shale plays, where each new gathering system expansion requires new TEG or molecular sieve dehydration capacity.

Molecular sieve dehydration is the preferred technology for low-dewpoint duty applications, including LNG feedgas conditioning and cryogenic gas processing. The global LNG liquefaction capacity additions through 2030 — including the Plaquemines LNG, Golden Pass LNG, and North Field East expansion projects — are generating the highest-value procurement contracts in the Natural Gas Dehydration Equipment market, as LNG feedgas dehydration requires ultra-low water content specifications that only molecular sieve technology can reliably achieve. These projects collectively represent a USD 1.2 Billion addressable market for molecular sieve dehydration equipment through 2030.

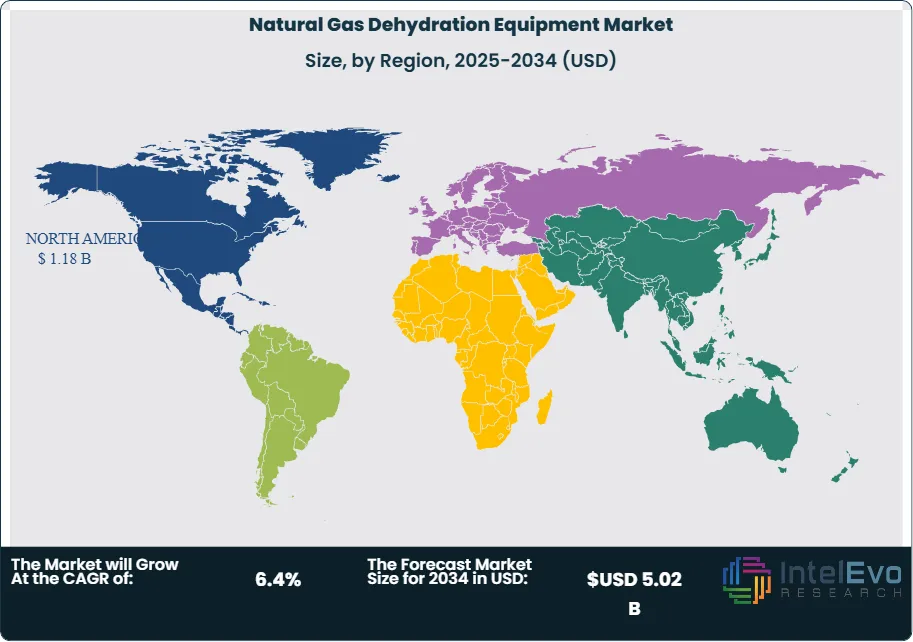

North America leads the Natural Gas Dehydration Equipment market with 41.2% share at USD 1.18 Billion in 2025, followed by the Middle East and Africa at 24.6%. The MEA region carries the highest CAGR of 7.6% through 2034, reflecting LNG megaproject activity in Qatar and UAE and new gas monetization programs across East Africa. Environmental regulation is an emerging market force: EPA 40 CFR Part 63 Subpart HH regulations on TEG dehydration unit benzene emissions are driving glycol unit upgrades and condensate recovery system installations across U.S. onshore gas processing operations.

, By Application (Midstream Processing & Pipelines, LNG Liquefaction, Upstream Gathering, Offshore FPSO), By Equipment Type (Absorber Columns, Reboilers, Adsorbent Vessels, Pumps, Controls), By Operation (Upstream, Midstream, Downstream/LNG) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Key Takeaways

- Market Growth: The global Natural Gas Dehydration Equipment market was valued at USD 2.86 Billion in 2025 and is forecast to reach USD 5.02 Billion by 2034, at a CAGR of 6.4% during 2025–2034.

- Segment Dominance (By Technology): TEG (Triethylene Glycol) dehydration systems dominate the technology segment with 58.4% market share in 2025 (USD 1.67 Billion), reflecting their cost-effectiveness and operational reliability across onshore and offshore midstream applications.

- Segment Dominance (By Application): Midstream gas processing and transmission pipeline conditioning is the largest application at 46.8% share (2025, USD 1.34 Billion), driven by expanding U.S. gathering and processing infrastructure in unconventional shale plays.

- Driver: Global natural gas production growth — with U.S. output reaching 103 Bcf/d in 2025 and global LNG trade volumes at 420 MTPA — is the primary demand driver, requiring dehydration equipment at every point in the gas value chain from wellhead to export terminal.

- Restraint: EPA 40 CFR Part 63 Subpart HH benzene emission regulations on TEG units are generating compliance retrofit costs estimated at USD 45,000-120,000 per unit, creating capital expenditure pressure on smaller independent midstream operators with large TEG unit fleets.

- Opportunity: LNG feedgas molecular sieve dehydration for new U.S. export terminals and the QatarEnergy North Field expansion represents an addressable market of USD 1.2 Billion through 2030, with each LNG train requiring 6-12 molecular sieve vessels at USD 2-8 Million per vessel.

- Trend: Digitalization of dehydration equipment — including IoT-enabled glycol circulation pump monitoring, automated reboiler temperature control, and remote dewpoint analyzer integration — reached 28.4% of new dehydration unit installations in 2025, up from 11% in 2021.

- Regional Analysis: North America leads the Natural Gas Dehydration Equipment market with 41.2% share and USD 1.18 Billion in revenue in 2025, anchored by Permian Basin and Marcellus shale gas gathering infrastructure expansion and EPA-driven TEG unit upgrade programs.

Competitive Landscape

The Natural Gas Dehydration Equipment market is moderately fragmented, with the top four suppliers — Exterran Holdings, SLB (NATCO), Frames Group, and Peerless Manufacturing (CECO) — collectively holding approximately 46% of global revenue in 2025. Competition is primarily project-bid-driven for large LNG and offshore applications, and price-competitive for standard TEG glycol unit packages in the North American midstream sector. M&A activity has been meaningful: Exterran's USD 420 Million acquisition of CECO's gas processing assets in February 2025 was the sector's largest transaction in recent years, consolidating the TEG dehydration equipment supply chain in North America.

| Company | HQ | Position | Key Offering | Geo Strength | Recent Move |

| Exterran Holdings | USA | Leader | CECO Glycol Dehydration Units | North America | Acquired CECO Environmental gas processing assets for USD 420M (Feb 2025) |

| Schlumberger (SLB) | USA | Leader | NATCO TEG Dehydration Systems | North America / MEA | Expanded NATCO modular dehydration line for offshore applications (May 2025) |

| Frames Group | Netherlands | Leader | FRAMES TEG Dehydration Skids | Europe / Middle East | Signed multi-unit dehydration contract with QatarEnergy for USD 85M (Jan 2025) |

| Peerless Manufacturing (CECO) | USA | Challenger | Peerless Mist Eliminator / Dehydration | North America | Launched 4th-gen molecular sieve dehydration module (Aug 2025) |

| Kimray Inc. | USA | Challenger | Kimray Glycol Circulation Pump Systems | North America | Released IoT-enabled glycol pump monitoring kit for remote sites (Apr 2026) |

| HC Petroleum Equipment | China | Niche Player | HC-TEG Modular Dehydration Skids | Asia Pacific | Expanded manufacturing capacity by 30% at Shandong facility (Nov 2025) |

| Enerflex Ltd. | Canada | Challenger | Enerflex Integrated Gas Processing | North America / Latin America | Commissioned 3 dehydration-compression packages for YPF Vaca Muerta (Mar 2026) |

| Sulzer AG | Switzerland | Niche Player | Sulzer MellapakPlus Dehydration Packing | Europe / MEA | Signed technology license agreement with ADNOC Gas Processing (Sep 2025) |

| Exterran / Global Power Equipment | USA | Niche Player | Standard Xchange Glycol Reboiler Systems | North America | Launched enhanced-duty reboiler for sour-gas TEG duty (Jan 2026) |

By Technology

| Technology | Market Share (2025) | Revenue (2025) |

| TEG (Triethylene Glycol) Absorption | 58.4% | USD 1.67 Billion |

| Molecular Sieve (Solid Desiccant) | 24.6% | USD 0.70 Billion |

| Silica Gel / Alumina Desiccant | 9.2% | USD 0.26 Billion |

| Refrigeration Dehydration | 7.8% | USD 0.22 Billion |

TEG absorption dominates the Natural Gas Dehydration Equipment market with 58.4% technology share at USD 1.67 Billion in 2025. The TEG dehydration unit consists of a contactor column where wet gas contacts countercurrently flowing lean TEG, a glycol-to-glycol heat exchanger, a flash separator, and a reboiler-regenerator that restores TEG to greater than 98.5% purity for recirculation. TEG units are favored for their low capital cost relative to capacity, operational simplicity, and suitability for a wide range of inlet gas water contents and flow rates. Standard TEG glycol unit packages range from 2 MMscfd skid-mounted field units to 500 MMscfd custom-engineered onshore gas plant installations. The primary technical limitation of TEG dehydration is its inability to achieve dewpoints below approximately minus 40 degrees Celsius in standard atmospheric-pressure regeneration configurations — a constraint that restricts TEG applicability in LNG feedgas and cryogenic process conditioning duty. EPA Subpart HH regulations governing BTEX emissions from TEG reboiler still vents are driving investment in condenser coils, vapor recovery units, and enclosed combustion devices across the U.S. TEG fleet.

Molecular sieve dehydration captures 24.6% of market revenue at USD 0.70 Billion in 2025 and is the fastest-growing technology segment at 9.8% CAGR through 2034. Molecular sieves — principally Type 3A and 4A zeolite adsorbents — achieve water dewpoints below minus 100 degrees Celsius in cycling twin-tower or multi-bed configurations, making them indispensable for LNG feedgas conditioning, NGL recovery plant inlet dehydration, and cryogenic processing ahead of turbo-expander demethanizer trains. Each LNG liquefaction train of 5-8 MTPA capacity typically requires a molecular sieve dehydration unit containing 6-12 pressure vessels — each 2-4 meters in diameter and 10-15 meters tall — packed with 30-100 tonnes of activated molecular sieve adsorbent. The North Field Expansion in Qatar, Plaquemines LNG in Louisiana, and Tortue FLNG offshore West Africa collectively drive USD 400+ Million in molecular sieve dehydration equipment procurement through 2027.

Silica gel and activated alumina desiccant dehydration holds 9.2% share at USD 0.26 Billion in 2025. These bulk desiccant materials are used in smaller-scale applications — primarily instrument gas drying, gas turbine fuel conditioning, and inlet dehydration for gas engines at remote production sites. Silica gel units are low-cost, disposable, and well-suited to intermittent duty cycles where continuous glycol circulation is uneconomical. Refrigeration dehydration — which condenses water vapor by chilling the gas stream to near-hydrate formation conditions — accounts for 7.8% of market revenue at USD 0.22 Billion and is primarily deployed in gas sweetening plant inlet conditioning ahead of amine absorption units, where partial water condensation upstream of the amine contactor reduces heat duty.

By Application

| Application | Market Share (2025) | Revenue (2025) |

| Midstream Processing & Transmission | 46.8% | USD 1.34 Billion |

| LNG Liquefaction & Conditioning | 22.4% | USD 0.64 Billion |

| Upstream Wellhead & Gathering | 18.6% | USD 0.53 Billion |

| Offshore Production & FPSO | 12.2% | USD 0.35 Billion |

Midstream gas processing and pipeline transmission conditioning is the largest application for Natural Gas Dehydration Equipment, accounting for 46.8% of global revenue at USD 1.34 Billion in 2025. Gas processing plants — which extract NGLs from rich gas streams ahead of transmission — require inlet dehydration to protect cryogenic equipment and meet transmission pipeline quality specifications. The U.S. midstream sector is the world's largest dehydration equipment market by unit volume, with over 12,000 active TEG dehydration units estimated across U.S. gathering and processing operations per Gas Processors Association (GPA) data. New gas processing plant construction in the Permian Basin — where five large-scale processing plants with combined capacity exceeding 1.5 Bcf/d commenced commissioning in 2024-2025 — drives substantial new dehydration equipment procurement.

LNG liquefaction and feedgas conditioning captures 22.4% of the market at USD 0.64 Billion in 2025. This application is the highest-value segment per unit of equipment, as LNG feedgas molecular sieve dehydration trains are among the most capital-intensive process equipment items in a liquefaction plant, with each multi-vessel dehydration unit costing USD 15-40 Million depending on capacity and molecular sieve specification. The global LNG liquefaction capacity pipeline — with over 150 MTPA of new capacity under construction or in final investment decision phase as of 2025 — creates a multi-year high-value procurement horizon for molecular sieve dehydration equipment manufacturers and vessel fabricators.

Upstream wellhead and gathering dehydration holds 18.6% share at USD 0.53 Billion in 2025. These applications involve compact, skid-mounted TEG or desiccant units installed at wellhead locations, flowline manifolds, and satellite gathering stations to prevent hydrate formation and pipeline corrosion in produced gas streams before compression and transport to central processing facilities. In unconventional shale plays, the proliferation of multi-well pad development — with 8-16 wells per pad in the Permian Basin — concentrates wellhead dehydration load at centralized pad-level skid packages rather than individual well units. Offshore production and FPSO dehydration accounts for 12.2% of revenue at USD 0.35 Billion, with these applications commanding significant equipment price premiums due to weight and space constraints, IECEx/ATEX area classification requirements, and corrosion-resistant materials specifications.

By Equipment Type

| Equipment Type | Market Share (2025) | Revenue (2025) |

| Contactor / Absorber Columns | 31.4% | USD 0.90 Billion |

| Glycol Reboilers & Regeneration Units | 22.6% | USD 0.65 Billion |

| Molecular Sieve Vessels & Adsorbent | 20.8% | USD 0.60 Billion |

| Glycol Pumps & Circulation Equipment | 14.2% | USD 0.41 Billion |

| Instrumentation, Analyzers & Controls | 11.0% | USD 0.31 Billion |

Contactor columns — the primary gas-liquid contact vessels where wet gas meets circulating glycol — represent the largest equipment category at 31.4% share (USD 0.90 Billion in 2025). These pressure vessels are engineered per ASME Section VIII and API 12J standards, with structured packing or valve tray internals selected based on gas flow rate, inlet water loading, and allowable pressure drop. Glycol reboilers and regeneration units account for 22.6% at USD 0.65 Billion, serving the critical function of water stripping from rich glycol to restore lean glycol purity. Molecular sieve vessels and adsorbent materials together represent 20.8% at USD 0.60 Billion; the adsorbent itself constitutes a recurring consumable market, with Type 4A molecular sieve having a typical replacement cycle of 3-5 years in dehydration service. Glycol pumps and circulation equipment at 14.2% (USD 0.41 Billion) are high-reliability fluid handling components, with gas-driven Kimray pumps dominating the remote site segment due to their zero-electrical requirement design. Instrumentation, dewpoint analyzers, and automated control systems account for 11.0% at USD 0.31 Billion and are the fastest-growing equipment sub-category as digitalization of dehydration unit monitoring accelerates.

Regional Analysis

| Region | Share (2025) | Revenue (2025) | CAGR (2025–2034) |

| North America | 41.2% | USD 1.18 Billion | 5.8% |

| Middle East & Africa | 24.6% | USD 0.70 Billion | 7.6% |

| Europe | 16.4% | USD 0.47 Billion | 5.2% |

| Asia Pacific | 12.8% | USD 0.37 Billion | 8.4% |

| Latin America | 5.0% | USD 0.14 Billion | 7.1% |

North America

North America holds 41.2% of the Natural Gas Dehydration Equipment market with USD 1.18 Billion in revenue in 2025, growing at a 5.8% CAGR through 2034. The United States accounts for approximately 84% of the regional total, anchored by the world's most active gas gathering and processing sector. U.S. dry gas production averaged 103 Bcf/d in 2025 per EIA data, sustaining strong capital investment in midstream infrastructure across the Permian Basin, Haynesville, and Marcellus/Utica plays. The Gas Processors Association estimates over 12,000 active TEG dehydration units in U.S. field service as of 2025, with an annual replacement and upgrade market of approximately 800-1,000 units per year. EPA 40 CFR Part 63 Subpart HH regulations on TEG unit BTEX emissions have created a mandatory retrofit market for condensate recovery units, vapor recovery systems, and enclosed combustors, adding incremental capital expenditure to the operational TEG unit fleet. Canada's WCSB — primarily the Montney and Duvernay tight-gas plays in British Columbia and Alberta — sustains active dehydration equipment procurement, with cold-climate specifications requiring trace heating, insulation packages, and cold-weather startup provisions. Mexico's Pemex midstream segment and private-sector gas processors are secondary demand sources.

Middle East & Africa

The Middle East and Africa hold 24.6% of the Natural Gas Dehydration Equipment market at USD 0.70 Billion in 2025, with the highest regional CAGR at 7.6% through 2034. Qatar is the region's most significant single-country market, with QatarEnergy's North Field Expansion — targeting a production increase from 77 MTPA to 126 MTPA of LNG capacity — driving multi-year procurement of both TEG field dehydration and molecular sieve LNG feedgas conditioning equipment. Frames Group's January 2025 contract win for 6 TEG dehydration skid packages valued at USD 85 Million exemplifies the scale of procurement associated with this project. Saudi Arabia's Master Gas System Phase III expansion, ADNOC's Hail and Ghasha sour-gas development, and Kuwait's Al-Zour refinery gas processing complex are additional MEA demand centers requiring significant dehydration equipment investment. In Africa, the Coral Sul FLNG in Mozambique, Tortue FLNG on the Mauritania/Senegal border, and Nigeria's NLNG Train 7 expansion are driving molecular sieve dehydration equipment procurement across the sub-Saharan LNG segment. The GCC's sour-gas programs — involving high H2S-content reservoirs — impose additional dehydration equipment specifications including 316L stainless steel wetted parts and NACE MR0175 material compliance.

Europe

Europe accounts for 16.4% of the Natural Gas Dehydration Equipment market at USD 0.47 Billion in 2025, growing at a 5.2% CAGR through 2034. Norway is the region's largest single country market, with Equinor's offshore production portfolio requiring extensive subsea and topside dehydration infrastructure across North Sea producing fields. The Johan Sverdrup Phase II, Snøhvit LNG plant, and Hammerfest LNG export terminal all maintain active dehydration equipment maintenance and lifecycle management programs. The Netherlands, as Europe's gas distribution hub via the Gasunie network and the TTF trading point, sustains TEG dehydration infrastructure across its extensive onshore transmission system. Germany's underground gas storage facilities — critical for European energy security following the 2022 supply disruption — require inlet dehydration for gas injection streams, driving dehydration equipment procurement for storage site conditioning. The UK's North Sea decommissioning wave presents a mixed picture: declining production volumes reduce new equipment demand, but dehydration unit integrity management for remaining life extension generates service and parts market revenue. Romania's Neptun Deep Black Sea development, targeting first gas in 2027, will require significant offshore dehydration equipment procurement.

Asia Pacific

Asia Pacific holds 12.8% of the Natural Gas Dehydration Equipment market at USD 0.37 Billion in 2025, expanding at the second-highest regional CAGR of 8.4% through 2034. China is the largest single-country market within the region, with CNPC, CNOOC, and Sinopec collectively executing large-scale gas gathering, processing, and dehydration infrastructure programs in the Sichuan Basin, Tarim Basin, and South China Sea. China's domestic manufacturers — including HC Petroleum Equipment and Yancheng Tester International — supply cost-competitive TEG dehydration units to domestic operators, limiting international vendor penetration to specialty molecular sieve and advanced instrument packages. Australia's LNG industry — encompassing the Ichthys, Prelude FLNG, Gorgon, and North West Shelf projects — requires ongoing dehydration equipment maintenance, lifecycle sieve replacement, and plant capacity expansion work. India's ONGC and GAIL are expanding gas gathering and processing infrastructure in the Krishna-Godavari deepwater block and Rajasthan onshore fields, creating incremental demand for both TEG and molecular sieve dehydration equipment. Indonesia's Tangguh LNG expansion and Malaysia's MLNG complex on Sabah are additional Asia Pacific high-value dehydration equipment demand centers.

Latin America

Latin America holds 5.0% of Natural Gas Dehydration Equipment revenue at USD 0.14 Billion in 2025, growing at a 7.1% CAGR through 2034. Argentina's Vaca Muerta tight-gas play is the region's most active new dehydration equipment market: YPF, TotalEnergies, and Pampa Energia are executing pad drilling campaigns that require modular TEG dehydration and compression packages for field gathering service. Enerflex's March 2026 commissioning of three integrated dehydration-compression packages for YPF at 50 MMscfd capacity each illustrates the scale of Vaca Muerta gas infrastructure development. Brazil's Petrobras operates TEG and molecular sieve dehydration units across its pre-salt gas processing vessels and onshore processing facilities, with the Rota 3 gas pipeline project creating new dehydration equipment installation opportunities. Colombia's Ecopetrol midstream expansion in the Llanos Basin and Bolivia's aging gas processing plants undergoing rehabilitation are secondary demand sources in the region.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Technology

- TEG (Triethylene Glycol) Absorption

- Molecular Sieve (Solid Desiccant)

- Silica Gel / Alumina Desiccant

- Refrigeration Dehydration

By Application

- Midstream Processing and Transmission Pipeline

- LNG Liquefaction and Conditioning

- Upstream Wellhead and Gathering

- Offshore Production and FPSO

By Equipment Type

- Contactor / Absorber Columns

- Glycol Reboilers and Regeneration Units

- Molecular Sieve Vessels and Adsorbent

- Glycol Pumps and Circulation Equipment

- Instrumentation, Analyzers and Controls

By Operation

- Upstream

- Midstream

- Downstream / LNG

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.86 B |

| Forecast Revenue (2034) | USD 5.02 B |

| CAGR (2025-2034) | 6.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Technology, (TEG (Triethylene Glycol) Absorption, Molecular Sieve (Solid Desiccant), Silica Gel / Alumina Desiccant, Refrigeration Dehydration), By Application, (Midstream Processing and Transmission Pipeline, LNG Liquefaction and Conditioning, Upstream Wellhead and Gathering, Offshore Production and FPSO), By Equipment Type, (Contactor / Absorber Columns, Glycol Reboilers and Regeneration Units, Molecular Sieve Vessels and Adsorbent, Glycol Pumps and Circulation Equipment, Instrumentation, Analyzers and Controls), By Operation, (Upstream, Midstream, Downstream / LNG) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | EXTERRAN HOLDINGS, SLB (NATCO GROUP), FRAMES GROUP, PEERLESS MANUFACTURING (CECO ENVIRONMENTAL), KIMRAY INC., ENERFLEX LTD., SULZER AG, HC PETROLEUM EQUIPMENT, AXIP ENERGY SERVICES (CHENIER MIDSTREAM EQUIPMENT), VALERUS FIELD SOLUTIONS, PIONEER NATURAL RESOURCES / MIDCOAST ENERGY (US MIDSTREAM), YANCHENG TESTER INTERNATIONAL, JOHN ZINK HAMWORTHY COMBUSTION (KOCH ENGINEERED SOLUTIONS), ATLAS COPCO GAS AND PROCESS, HANOVER COMPRESSOR (ARCHROCK), Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Midstream Processing & Pipelines, LNG Liquefaction, Upstream Gathering, Offshore FPSO), By Equipment Type (Absorber Columns, Reboilers, Adsorbent Vessels, Pumps, Controls), By Operation (Upstream, Midstream, Downstream/LNG) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Midstream Processing & Pipelines, LNG Liquefaction, Upstream Gathering, Offshore FPSO), By Equipment Type (Absorber Columns, Reboilers, Adsorbent Vessels, Pumps, Controls), By Operation (Upstream, Midstream, Downstream/LNG) Industry Trends, Competitive Landscape & Forecast 2026–2034")

, By Application (Midstream Processing & Pipelines, LNG Liquefaction, Upstream Gathering, Offshore FPSO), By Equipment Type (Absorber Columns, Reboilers, Adsorbent Vessels, Pumps, Controls), By Operation (Upstream, Midstream, Downstream/LNG) Industry Trends, Competitive Landscape & Forecast 2026–2034")

Frequently Asked Questions

How big is the Natural Gas Dehydration Equipment Market?

Natural gas dehydration equipment market valued at USD 2.69B in 2024, reaching USD 5.02B by 2034, growing at a CAGR of 6.4% from 2026–2034.

Who are the major players in the Natural Gas Dehydration Equipment Market?

EXTERRAN HOLDINGS, SLB (NATCO GROUP), FRAMES GROUP, PEERLESS MANUFACTURING (CECO ENVIRONMENTAL), KIMRAY INC., ENERFLEX LTD., SULZER AG, HC PETROLEUM EQUIPMENT, AXIP ENERGY SERVICES (CHENIER MIDSTREAM EQUIPMENT), VALERUS FIELD SOLUTIONS, PIONEER NATURAL RESOURCES / MIDCOAST ENERGY (US MIDSTREAM), YANCHENG TESTER INTERNATIONAL, JOHN ZINK HAMWORTHY COMBUSTION (KOCH ENGINEERED SOLUTIONS), ATLAS COPCO GAS AND PROCESS, HANOVER COMPRESSOR (ARCHROCK), Others

Which segments covered the Natural Gas Dehydration Equipment Market?

By Technology, (TEG (Triethylene Glycol) Absorption, Molecular Sieve (Solid Desiccant), Silica Gel / Alumina Desiccant, Refrigeration Dehydration), By Application, (Midstream Processing and Transmission Pipeline, LNG Liquefaction and Conditioning, Upstream Wellhead and Gathering, Offshore Production and FPSO), By Equipment Type, (Contactor / Absorber Columns, Glycol Reboilers and Regeneration Units, Molecular Sieve Vessels and Adsorbent, Glycol Pumps and Circulation Equipment, Instrumentation, Analyzers and Controls), By Operation, (Upstream, Midstream, Downstream / LNG)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Natural Gas Dehydration Equipment Market

Published Date : 30 Mar 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date