- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Natural Gas Refueling Stations Market Size 2025–2034 | CAGR 8.1%

Global Natural Gas Refueling Stations Market Size, Share & Growth Analysis By Station Type (CNG Filling Stations, LNG Filling Stations), By Application (Vehicle, Marine/Ship, Others), By End-User (Automotive, Aerospace, Logistics & Transportation, Public Transit), By Ownership Model & Region With Key Players – Industry Overview, Market Dynamics, Infrastructure Development, Competitive Strategies, Emerging Trends & Forecast 2025–2034

Report Overview

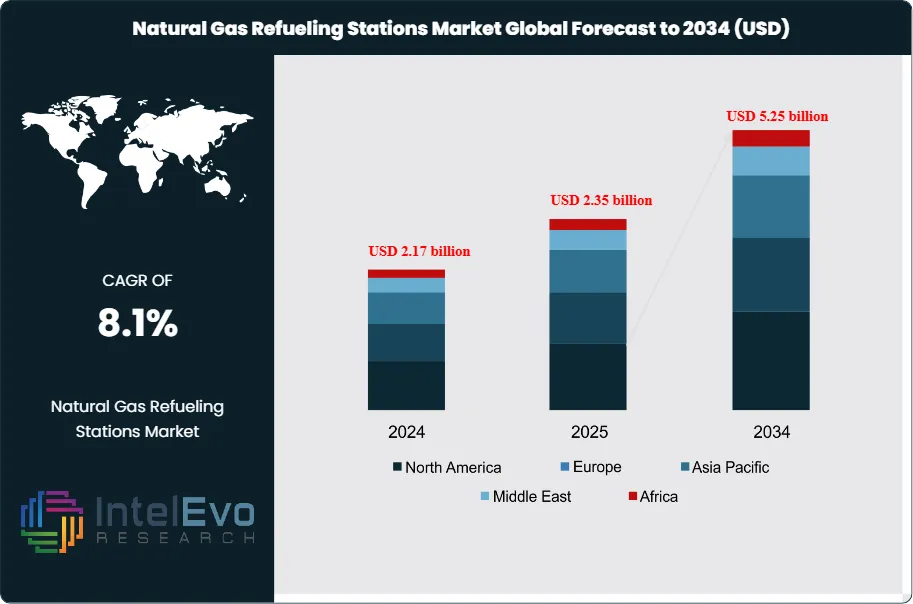

The Natural Gas Refueling Stations Market is expected to reach about USD 2.35 billion in 2025. It is projected to grow to around USD 5.25 billion by 2034, showing a steady CAGR of roughly 8.1% from 2026 to 2034. This market growth is driven by the increasing use of compressed and liquefied natural gas vehicles in commercial fleets, public transport, and logistics. These sectors are looking for lower fuel costs and cleaner emissions. Government support for alternative fuel infrastructure, along with stricter emission regulations and funding for clean transport routes, is speeding up the development of these stations. As global energy transition plans progress, the natural gas refueling infrastructure is set to serve as an important link between traditional fuels and zero-emission transport options.

Get More Information about this report -

Request Free Sample ReportDemand for natural gas refueling stations reflects the expansion of natural gas vehicle fleets in public transport, freight logistics, and municipal services. Operators favor natural gas buses and heavy-duty trucks for lower fuel expenses and lower exhaust emissions. In the United States, transport applications already account for about 14% of natural gas consumption, while natural gas represents around 32% of total energy use, underscoring the fuel’s strategic role in decarbonization. Fleet managers in emerging markets adopt natural gas as a bridge solution between conventional fuels and zero-emission powertrains, which supports stable station utilization and long-term contracts.

On the supply side, the market expands through both public-access corridors and depot-based private stations. Investment continues in compressed natural gas and liquefied natural gas configurations that serve long-haul and urban duty cycles. Government incentives, tax credits, and emissions regulations in North America, Europe, and parts of Asia encourage station rollouts and integration with wider gas pipeline networks. Natural gas vehicles emit up to 20% less CO2 than comparable gasoline units, which helps operators meet tightening fleet emission targets. However, exposure to natural gas price volatility, permitting delays, and community concerns about local air quality can slow project timelines and affect return profiles.

Technology progress reshapes station design, operations, and economics. Operators deploy automated monitoring, predictive maintenance, and digital twins to optimize compressor uptime and reduce unplanned outages. AI-based demand forecasting aligns fuel inventory, pricing, and capacity planning with observed traffic patterns and telematics data. Payment systems evolve toward cloud-based platforms that integrate fleet cards, real-time billing, and carbon reporting. Regionally, Asia-Pacific accounts for an estimated 38% of new station investments, led by China and India, followed by Europe at roughly 28% with a focus on cross-border corridors. North America represents about 24% of spending, with emphasis on heavy-duty trucking lanes. These regional commitments position natural gas refueling stations as an important component in the global transition to cleaner transport and industrial energy.

, By Application (Vehicle, Marine/Ship, Others), By End-User (Automotive, Aerospace, Logistics & Transportation, Public Transit), By Ownership Model & Region With Key Players – Industry Overview, Market Dynamics, Infrastructure Development, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Key Takeaways

- Market Growth: The global Natural Gas Refueling Stations Market stands at USD 2.35 billion in 2025 and is projected to reach USD 5.25 billion by 2034, reflecting a 8.1% CAGR, 2026-2034. This growth trajectory signals steady capital deployment into refueling infrastructure aligned with natural gas vehicle expansion.

- Segment Dominance: CNG filling stations hold a leading position with a 76.4% share, 2024, anchoring the revenue base of the natural gas refueling ecosystem. This share likely corresponds to estimated: 3,000 active CNG stations worldwide, 2024, as operators prioritize lower-cost compression assets over liquefaction.

- Segment Dominance: Maintenance services represent a core profit pool with a 52.3% share of service-related revenues, 2024, underscoring the importance of uptime and reliability. The automotive sector accounts for 86.4% of demand, 2024, making light and heavy vehicles the primary utilization driver for station throughput.

- Driver: Fleet operators pursue lower total cost of ownership and emissions, with estimated: 15.0% fuel cost savings per kilometer, 2024 when shifting from diesel to natural gas. These economics, combined with a projected 6.8% CAGR, 2024-2034 for station investments, drive sustained adoption.

- Restraint: High upfront capital requirements for compressors, storage, and safety systems can increase project costs by estimated: 20.0% versus conventional fuel stations, 2024. Limited grid connectivity and permitting complexity can delay deployments by estimated: 12.0 months per project, 2024.

- Opportunity: Scaling refurbishment and maintenance contracts could unlock an incremental estimated: 1.5 billion USD, 2030 in recurring revenues across global station fleets. Converting even an additional estimated: 5.0% of heavy-duty trucks to natural gas, 2028 would materially raise station utilization.

- Trend: Operators increasingly deploy remote monitoring, predictive analytics, and automated control, with estimated: 30.0% of stations adopting digital asset management platforms, 2027. AI-enabled optimization can cut unplanned downtime by estimated: 10.0%, 2026 and improve maintenance scheduling efficiency.

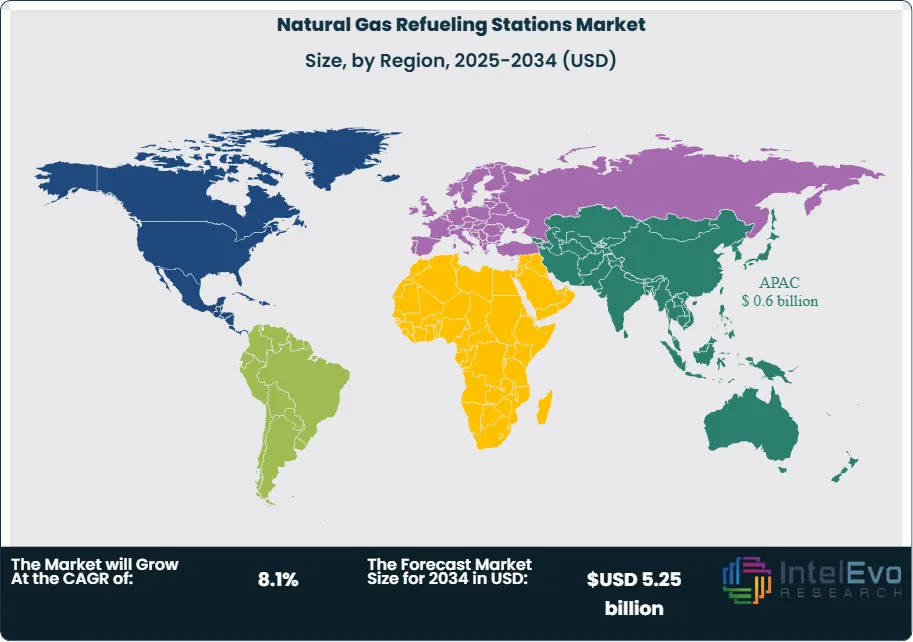

- Regional Analysis: Asia-Pacific leads with a 32.7% market share, 2024, translating to 0.6 billion USD, 2024 in regional value. The region is poised to sustain an estimated: 7.5% CAGR, 2024-2034 as China and India expand urban and highway CNG corridors and incentivize commercial fleet conversion.

Type Analysis

CNG filling stations continue to lead the market in 2025 with a share above 76 percent. Their position reflects the strong uptake of CNG in passenger and commercial fleets that seek lower emissions and predictable fuel pricing. CNG stations also benefit from consistent policy backing in major markets, which has supported rapid additions to public and private fueling networks.

Most countries with expanding gas mobility programs prioritize CNG because the required compression systems are cheaper to install and operate than LNG solutions. This has encouraged operators to enhance station layouts, compressor reliability, and storage capacity. LNG stations remain relevant for long-haul corridors, yet their adoption grows at a slower rate due to higher investment thresholds and more complex handling requirements.

Application Analysis

Maintenance services represent the largest share of application-level revenue, accounting for more than 52 percent in 2025. Natural gas fueling systems require frequent inspection to ensure pressure stability, safe gas transfer, and proper functioning of compressors and metering equipment. As the number of stations continues to rise across Asia Pacific, North America, and Europe, recurring maintenance becomes central to operational continuity.

The increased integration of digital metering, automated controls, and cloud-linked monitoring expands the scope of service contracts. Operators now require support for software updates, fault detection systems, and secure payment technologies in addition to mechanical upkeep. This shift reinforces the value of long-term service agreements as operators seek to reduce downtime and maintain compliance with regional safety regulations.

End-Use Analysis

The automotive segment accounts for more than 86 percent of total market activity in 2025. Most natural gas stations are designed for passenger vehicles, buses, and heavy trucks, which remain the largest users of CNG and LNG solutions. Growth in commercial logistics and the continued replacement of diesel fleets with natural gas alternatives support this strong concentration.

Independent service providers play a central role in this segment. They typically expand faster than large utilities or national operators because they adapt quickly to local market requirements and secure high-traffic sites for new installations. Their presence accelerates adoption among fleet operators seeking reliable access to fuel without heavy upfront investment.

Regional Analysis

Asia Pacific leads the global market with a share of roughly 33 percent, equal to about 0.6 billion USD in 2025. China and India continue to expand national CNG corridors, while government-backed fleet conversion programs support further capacity additions. Investment momentum remains strong as both countries widen their gas import and pipeline infrastructure.

North America follows with steady year-on-year growth supported by abundant natural gas supply and incentives for public and private fleets. Federal and state-level programs encourage new station development, particularly in logistics corridors. The region also benefits from high adoption of digital control systems and improved compressor technologies.

Europe, Latin America, and the Middle East & Africa expand at varying speeds. Europe accelerates deployments to meet emission targets across transport sectors. Latin America invests selectively in metropolitan CNG networks, while parts of the Middle East focus on diversifying transport fuels. These combined developments reinforce the global transition toward natural gas as a cleaner and commercially viable transport fuel.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Type

- CNG Filling Stations

- LNG Filling Stations

By Application

- Vehicle

- Ship

- Others

By End User

- Automotive

- Aerospace

- Others

Regions

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.35 billion |

| Forecast Revenue (2034) | USD 5.25 billion |

| CAGR (2025-2034) | 8.1% |

| Historical data | 2020-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2025-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Type, CNG Filling Stations, LNG Filling Stations, By Application, Vehicle, Ship, Others, By End User, Automotive, Aerospace, Others |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | IGS Energy, Énergir, ANGIEnergy Systems, Inc., Sunoco LP, OPAL Fuels Inc., ZeitEnergy, LLC., CGRS, Inc., Trillium Energy Solutions, Clean Energy Fuels, CommTank, TotalEnergies, Megha Engineering & Infrastructures Ltd, Snam S.p.A., FASTECH, Other Key Players |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Application (Vehicle, Marine/Ship, Others), By End-User (Automotive, Aerospace, Logistics & Transportation, Public Transit), By Ownership Model & Region With Key Players – Industry Overview, Market Dynamics, Infrastructure Development, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By Application (Vehicle, Marine/Ship, Others), By End-User (Automotive, Aerospace, Logistics & Transportation, Public Transit), By Ownership Model & Region With Key Players – Industry Overview, Market Dynamics, Infrastructure Development, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

, By Application (Vehicle, Marine/Ship, Others), By End-User (Automotive, Aerospace, Logistics & Transportation, Public Transit), By Ownership Model & Region With Key Players – Industry Overview, Market Dynamics, Infrastructure Development, Competitive Strategies, Emerging Trends & Forecast 2025–2034")

Frequently Asked Questions

How big is the Natural Gas Refueling Stations Market?

The Natural Gas Refueling Stations Market is projected to grow from USD 2.35 billion in 2025 to USD 5.25 billion by 2034, expanding at a CAGR of 8.1% during 2026–2034, driven by clean fuel adoption, government incentives, and rising demand from commercial fleets and public transport infrastructure.

Who are the major players in the Natural Gas Refueling Stations Market?

IGS Energy, Énergir, ANGIEnergy Systems, Inc., Sunoco LP, OPAL Fuels Inc., ZeitEnergy, LLC., CGRS, Inc., Trillium Energy Solutions, Clean Energy Fuels, CommTank, TotalEnergies, Megha Engineering & Infrastructures Ltd, Snam S.p.A., FASTECH, Other Key Players

Which segments covered the Natural Gas Refueling Stations Market?

By Type, CNG Filling Stations, LNG Filling Stations, By Application, Vehicle, Ship, Others, By End User, Automotive, Aerospace, Others

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Natural Gas Refueling Stations Market

Published Date : 31 Jan 2026 | Formats :Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date