- Home

- Industries

Aerospace And Defence

Aerospace And Defence

Agriculture

Agriculture

Automotive And Transportation

Automotive And Transportation

Banking And Finance

Banking And Finance

Business

Business

Chemicals And Materials

Chemicals And Materials

Consumer And Retail

Consumer And Retail

Electronics And Semiconductors

Electronics And Semiconductors

Food And Beverages

Food And Beverages

Machinery & Equipments

Machinery & Equipments

Manufacturing And Construction

Manufacturing And Construction

Medical Devices

Medical Devices

Others

Others

Pharmaceuticals And Healthcare

Pharmaceuticals And Healthcare

Power And Energy

Power And Energy

Sports

Sports

Technology

Technology

- Services

- News Room

- About us

- Contact Us

-

Global Neoantigen Vaccine Market Size & Forecast 2034 | CAGR 14.4%

Global Neoantigen Vaccine Market Size, Share, Growth & Industry Analysis By Vaccine Type (Personalized Neoantigen Vaccines, Off-the-Shelf Neoantigen Vaccines, Combination Neoantigen Vaccines), By Platform Technology (mRNA-Based, Peptide-Based, Viral Vector, Cell-Based & Dendritic Cell Platforms), By Indication (Melanoma, Non-Small Cell Lung Cancer, Colorectal Cancer, Others), By End-User (Hospitals, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034

Report Overview

| Market Size (2025) | Forecast Value (2034) | CAGR (2026–2034) | Largest Region (2025) |

| USD 2.8 Billion | USD 9.4 Billion | 14.4% | North America, 48.2% |

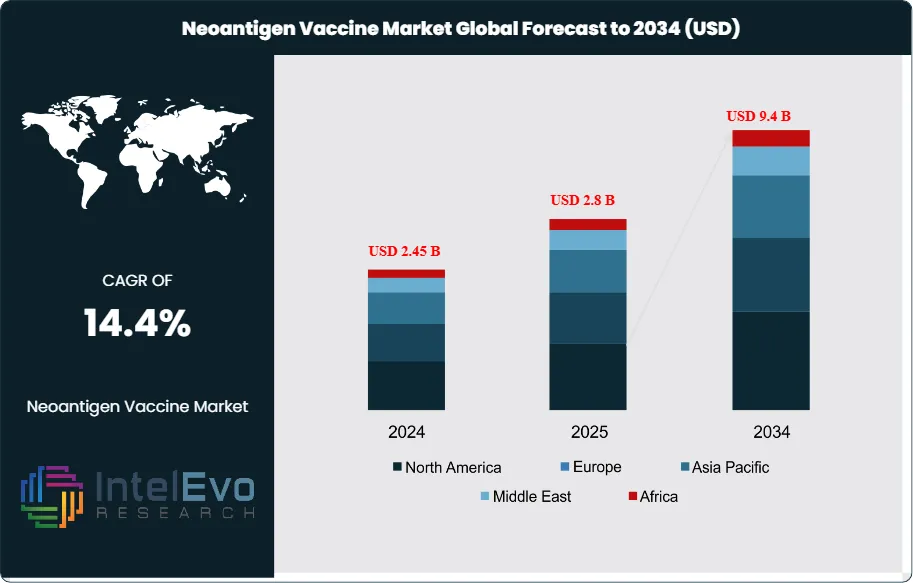

The Neoantigen Vaccine Market was valued at approximately USD 2.45 Billion in 2024 and reached USD 2.8 Billion in 2025. The market is projected to grow to USD 9.4 Billion by 2034, expanding at a CAGR of 14.4% during the forecast period from 2026 to 2034. This represents an absolute dollar opportunity of USD 6.6 Billion over the analysis period. Neoantigen vaccines represent a transformative approach to cancer immunotherapy, utilizing tumor-specific mutations to generate highly personalized therapeutic interventions. The field has transitioned from early clinical exploration to commercial viability, with regulatory pathways now established across major jurisdictions.

Get More Information about this report -

Request Free Sample ReportClinical validation data from Phase II and Phase III trials have demonstrated durable response rates exceeding 40% in melanoma and non-small cell lung cancer indications. The FDA granted Breakthrough Therapy Designation to seven neoantigen vaccine candidates between 2023 and 2025, accelerating review timelines and attracting institutional investment. Manufacturing scalability remains the primary technical barrier, with current production costs averaging USD 85,000 to USD 150,000 per patient. However, advances in automated peptide synthesis and mRNA platform technologies have reduced manufacturing timelines from 12 weeks to approximately 4–6 weeks. The neoantigen vaccine market benefits from convergent technology platforms spanning genomic sequencing, bioinformatics, and immunology.

North America commands 48.2% of global market share in 2025, driven by concentrated clinical trial activity at major academic medical centers and favorable reimbursement frameworks. Europe follows with 28.5% market share, supported by the EMA's PRIME designation pathway and cross-border clinical collaboration networks. Asia Pacific is the fastest-growing region at 18.2% CAGR through 2034, led by China's NMPA expedited review programs and Japan's Sakigake designation system. Investment activity remains strong, with venture capital deployment in the neoantigen space totaling USD 2.3 Billion in 2024. Strategic partnerships between biopharmaceutical companies and technology platforms have accelerated, with 24 major licensing agreements executed in the 18 months ending March 2025. The competitive environment is evolving toward integrated platform models combining antigen discovery, manufacturing, and clinical development capabilities.

, By Platform Technology (mRNA-Based, Peptide-Based, Viral Vector, Cell-Based & Dendritic Cell Platforms), By Indication (Melanoma, Non-Small Cell Lung Cancer, Colorectal Cancer, Others), By End-User (Hospitals, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034")

Key Takeaways

- Market Growth: The neoantigen vaccine market expands from USD 2.8 Billion in 2025 to USD 9.4 Billion by 2034, reflecting a 14.4% CAGR driven by clinical advancement and manufacturing innovation.

- Segment Dominance (Vaccine Type): Personalized neoantigen vaccines hold 62.4% market share in 2025, generating USD 1.75 Billion in revenue due to superior clinical efficacy in solid tumors.

- Segment Dominance (Indication): Oncology applications account for 94.8% of the market in 2025, with melanoma and lung cancer representing the primary therapeutic targets.

- Driver: Rising cancer incidence rates and clinical validation of neoantigen approaches drive market expansion, with 58 active Phase II/III trials globally as of Q1 2025.

- Restraint: High manufacturing costs averaging USD 100,000 per patient limit adoption, particularly in price-sensitive healthcare systems and emerging markets.

- Opportunity: Combination therapy protocols with checkpoint inhibitors present a USD 4.2 Billion addressable market segment by 2034.

- Trend: mRNA-based neoantigen platforms gain market share, with 45% of new clinical candidates utilizing lipid nanoparticle delivery systems as of 2025.

- Regional Analysis: North America leads with 48.2% market share and USD 1.35 Billion revenue in 2025, supported by extensive clinical infrastructure and payer coverage frameworks.

Competitive Landscape Overview

The neoantigen vaccine market exhibits moderate fragmentation, with the top four companies holding a combined 52.3% market share in 2025. Competition centers on platform technology differentiation, clinical pipeline depth, and manufacturing scalability. BioNTech and Moderna lead with mRNA-based platforms, while Gritstone bio and Neon Therapeutics focus on peptide and viral vector approaches. Strategic acquisition activity intensified in 2024, with three major transactions exceeding USD 500 Million each. Partnerships between technology platforms and large pharmaceutical companies dominate business development activity, enabling clinical and commercial scale.

| Company | HQ | Position | Key Product | Geo Strength | Recent Strategic Move |

| BioNTech SE | Germany | Leader | BNT122 (Autogene cevumeran) | Europe/N. America | Phase II expansion in pancreatic cancer (Jan 2025) |

| Moderna Inc. | USA | Leader | mRNA-4157/V940 (with Merck) | North America | Phase III initiation in melanoma (Mar 2025) |

| Gritstone bio | USA | Challenger | GRANITE/SLATE Platform | North America | Gilead partnership for combination trials (Dec 2024) |

| Neon Therapeutics | USA | Challenger | NEO-PV-01 Platform | North America | Integration with BioNTech pipeline completed (Feb 2025) |

| Genocea Biosciences | USA | Niche | GEN-009 (ATLAS Platform) | North America | Phase I/II data release for solid tumors (Jan 2025) |

| Nouscom AG | Switzerland | Niche | NOUS-209 (Viral Vector) | Europe | Series C funding of USD 72M secured (Mar 2025) |

| Agenus Inc. | USA | Challenger | AutoSynVax Platform | N. America/Europe | Expanded manufacturing capacity in MA facility (Dec 2024) |

| Transgene SA | France | Challenger | TG4050 (myvac Platform) | Europe | EMA PRIME designation received for head/neck cancer (Feb 2025) |

| ISA Pharmaceuticals | Netherlands | Niche | SLP Platform | Europe | Regeneron partnership for combination therapy (Jan 2025) |

| Evaxion Biotech | Denmark | Niche | EVX-01 (AI-Immunology) | Europe/N. America | Phase II melanoma trial enrollment completed (Mar 2025) |

By Vaccine Type

Personalized neoantigen vaccines dominate the market with 62.4% share and USD 1.75 Billion revenue in 2025. These vaccines are manufactured for individual patients based on tumor mutational analysis and represent the highest-efficacy approach to neoantigen targeting. Clinical response rates in personalized vaccine trials consistently exceed those of off-the-shelf alternatives, with objective response rates of 35–45% in advanced melanoma. Manufacturing complexity remains the primary challenge, requiring 4–6 weeks from biopsy to treatment initiation. Investment in automated peptide synthesis and AI-driven epitope prediction has reduced turnaround times by 40% since 2022. The personalized segment is projected to maintain market leadership through 2034, growing at 13.8% CAGR.

Off-the-shelf neoantigen vaccines account for 28.3% market share and USD 792 Million revenue in 2025. These vaccines target shared neoantigens common across patient populations, enabling scalable manufacturing and immediate availability. The segment addresses accessibility barriers inherent in personalized approaches and serves patients whose tumors lack sufficient unique mutations. Clinical development focuses on microsatellite instability-high tumors where shared neoantigen prevalence is highest. Growth is projected at 15.6% CAGR through 2034 as shared antigen discovery accelerates. Combination therapy protocols increasingly incorporate off-the-shelf vaccines as backbone treatments.

Combination neoantigen vaccines hold 9.3% market share at USD 260 Million in 2025. These products combine personalized neoantigens with shared tumor-associated antigens to broaden immune response coverage. The approach addresses tumor heterogeneity by targeting multiple antigen classes simultaneously. Clinical trials demonstrate enhanced response durability compared to single-modality vaccines. Manufacturing complexity increases costs but improves therapeutic coverage. The segment is projected to reach 12.1% market share by 2034 as clinical validation data matures and combination protocols standardize.

By Platform Technology

mRNA-based platforms lead with 48.6% market share and USD 1.36 Billion in 2025 revenue. The COVID-19 pandemic validated mRNA vaccine technology at scale, creating manufacturing infrastructure and regulatory precedent applicable to cancer vaccines. mRNA platforms offer rapid design iteration, simplified manufacturing compared to cell-based approaches, and favorable immunogenicity profiles. Lipid nanoparticle delivery systems enable efficient cellular uptake and cytoplasmic translation. BioNTech and Moderna dominate this segment through established manufacturing networks and clinical development expertise. Growth at 15.2% CAGR positions mRNA platforms to maintain leadership through 2034.

Peptide-based vaccines capture 31.2% market share at USD 874 Million in 2025. Synthetic long peptides offer manufacturing simplicity and established safety profiles derived from decades of vaccine development. The platform excels in precision targeting of specific epitopes with defined immunological characteristics. Manufacturing scalability is superior to cell-based approaches, though immunogenicity often requires adjuvant support. Peptide platforms are particularly suited to off-the-shelf applications targeting shared neoantigens. Growth at 12.8% CAGR reflects steady clinical advancement and manufacturing optimization.

Viral vector platforms account for 15.4% market share and USD 431 Million in 2025. Adenoviral and modified vaccinia Ankara vectors deliver strong immune responses through efficient antigen presentation pathways. Manufacturing complexity limits scalability but enables sustained antigen expression. Nouscom and Transgene lead clinical development with differentiated vector platforms. Pre-existing immunity to common viral vectors presents formulation challenges addressed through chimeric or rare serotype selection. The segment grows at 14.1% CAGR as manufacturing constraints ease through vector production innovation.

Cell-based and dendritic cell platforms represent 4.8% market share at USD 134 Million in 2025. Autologous dendritic cell vaccines offer potent antigen presentation but face manufacturing bottlenecks and cost pressures. The approach requires patient leukapheresis, ex vivo cell processing, and individualized manufacturing. Clinical efficacy data remains mixed, with response rates trailing newer platform technologies. The segment is projected to decline in relative market share as mRNA and peptide platforms advance, though absolute revenue grows modestly at 8.4% CAGR through 2034.

By Indication

Melanoma accounts for 34.6% of oncology applications with USD 920 Million revenue in 2025. The indication leads adoption due to high tumor mutational burden enabling robust neoantigen identification and established immunotherapy responsiveness. Clinical validation is most advanced in melanoma, with Moderna/Merck Phase III trials demonstrating 44% reduction in recurrence risk when combined with pembrolizumab. Adjuvant settings represent the primary treatment context, preventing recurrence in resected stage III/IV disease. Growth at 13.2% CAGR reflects continued label expansion and combination therapy adoption.

Non-small cell lung cancer represents 26.8% of oncology revenue at USD 712 Million in 2025. High mutational burden in smoking-associated NSCLC creates favorable conditions for neoantigen targeting. Clinical trials focus on adjuvant and maintenance settings following standard chemotherapy or checkpoint inhibitor treatment. BioNTech and Gritstone bio lead development with combination protocols incorporating anti-PD-1/PD-L1 agents. The indication is projected to grow at 15.8% CAGR through 2034 as first-line combination trials mature.

Colorectal cancer accounts for 15.4% market share at USD 409 Million in 2025. Microsatellite instability-high tumors represent the primary target population due to elevated neoantigen load and checkpoint inhibitor sensitivity. Off-the-shelf vaccine approaches gain traction given shared neoantigen prevalence in MSI-H disease. Clinical development expands to microsatellite stable disease through combination with immunogenic cell death inducers. Growth at 16.4% CAGR is projected through 2034 as patient selection criteria refine and combination protocols optimize.

Other oncology indications including pancreatic, head and neck, bladder, and ovarian cancers collectively represent 23.2% of market revenue at USD 616 Million in 2025. Pancreatic cancer trials by BioNTech demonstrate early clinical promise despite historically poor immunotherapy responsiveness. Head and neck squamous cell carcinoma benefits from HPV-associated antigen targeting approaches. Bladder and ovarian cancer trials focus on maintenance settings following platinum-based chemotherapy. The aggregate segment grows at 14.6% CAGR as indication breadth expands beyond initial tumor types.

Regional Analysis

North America Neoantigen Vaccine Market

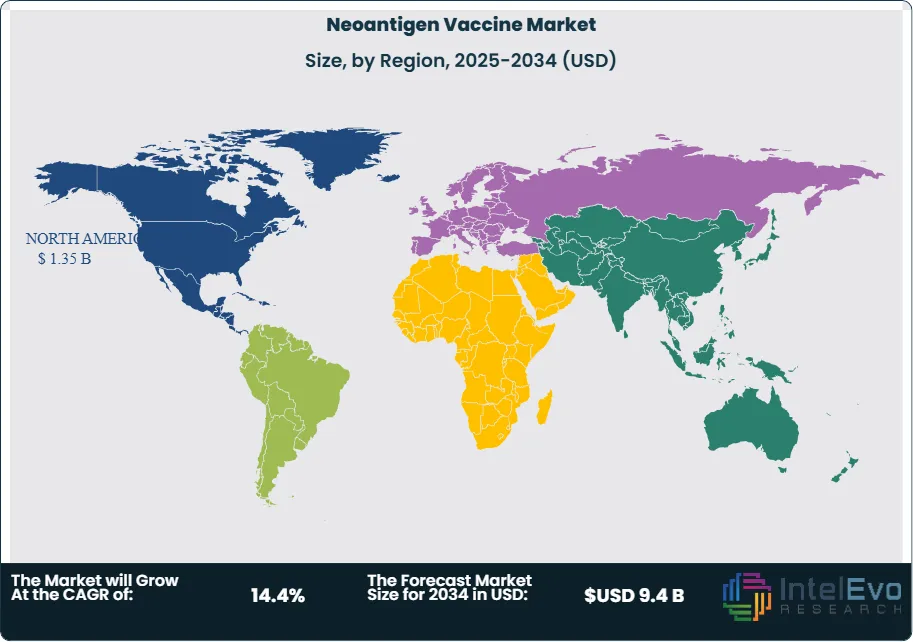

North America commands 48.2% of the global neoantigen vaccine market with USD 1.35 Billion revenue in 2025. The United States accounts for 92% of regional revenue driven by concentrated clinical trial activity, favorable FDA regulatory pathways, and established payer coverage for personalized cancer therapies. The FDA Breakthrough Therapy Designation program has accelerated review timelines for seven neoantigen vaccine candidates since 2023. Academic medical centers including Memorial Sloan Kettering, MD Anderson, and Dana-Farber serve as primary clinical development hubs. Venture capital and pharmaceutical company investment in U.S.-based neoantigen platforms exceeded USD 1.8 Billion in 2024. Canada contributes 6% of regional revenue with clinical trial activity centered in Toronto and Vancouver oncology networks. Reimbursement frameworks under provincial health systems are evolving to accommodate personalized vaccine costs. Mexico represents 2% of regional revenue with emerging clinical trial sites in Mexico City medical centers. North America is projected to maintain market leadership through 2034, growing at 13.6% CAGR as commercial product launches accelerate.

Europe Neoantigen Vaccine Market

Europe holds 28.5% global market share with USD 798 Million revenue in 2025. Germany leads regional activity at 28% of European revenue, hosting BioNTech headquarters and extensive clinical trial networks across university hospitals. The EMA PRIME designation pathway has enabled expedited assessment for three neoantigen vaccine candidates. France contributes 22% of European revenue with Transgene and academic centers driving development. The United Kingdom accounts for 18% of regional revenue with Cancer Research UK funding supporting early-stage clinical trials. The UK Medicines and Healthcare products Regulatory Agency offers innovation licensing for cell and gene therapies applicable to neoantigen vaccines. Switzerland hosts Nouscom and clinical trial activity at University Hospital Zurich. Cross-border collaboration through European Organisation for Research and Treatment of Cancer facilitates multi-national trial enrollment. Health technology assessment frameworks present reimbursement challenges given personalized vaccine costs. Europe is projected to grow at 14.2% CAGR through 2034 as centralized EMA procedures streamline market access.

Asia Pacific Neoantigen Vaccine Market

Asia Pacific represents 16.8% of the global market with USD 470 Million revenue in 2025 and is the fastest-growing region at 18.2% CAGR through 2034. China accounts for 45% of regional revenue driven by NMPA expedited review pathways and domestic biopharmaceutical investment. Shanghai and Beijing serve as clinical development centers with partnerships between domestic biotechs and global pharmaceutical companies increasing. Japan contributes 32% of regional revenue with PMDA Sakigake designation enabling accelerated review for innovative cancer therapies. The Japanese market benefits from established oncology specialty infrastructure and favorable reimbursement through the National Health Insurance system. South Korea accounts for 12% of regional revenue with Samsung Biologics and domestic CDMOs expanding manufacturing capabilities for cell and gene therapies. Australia contributes 8% with clinical trial activity at Peter MacCallum Cancer Centre and Melanoma Institute Australia. India represents an emerging opportunity with growing oncology treatment infrastructure and regulatory framework evolution. Asia Pacific growth reflects increasing cancer incidence, healthcare infrastructure development, and regulatory modernization enabling clinical trial activity.

Latin America Neoantigen Vaccine Market

Latin America accounts for 3.8% of global market share with USD 106 Million revenue in 2025. Brazil leads at 52% of regional revenue with ANVISA regulatory pathways accommodating clinical trials and compassionate use programs. Hospital Israelita Albert Einstein and Instituto do Cancer do Estado de Sao Paulo serve as primary trial sites. Mexico contributes 28% of regional revenue with clinical activity at Instituto Nacional de Cancerologia and private oncology networks. Argentina represents 12% of regional revenue with Buenos Aires medical centers participating in global clinical trials. Chile contributes 8% with emerging oncology infrastructure and regulatory cooperation with FDA pathways. Regional growth at 14.8% CAGR through 2034 reflects improving clinical trial infrastructure and increasing access to advanced cancer therapies. Manufacturing capacity remains limited with clinical supply sourced primarily from North American and European facilities.

Middle East and Africa Neoantigen Vaccine Market

Middle East and Africa represents 2.7% of global market share with USD 76 Million revenue in 2025. The United Arab Emirates leads at 35% of regional revenue with Dubai and Abu Dhabi positioning as medical tourism destinations and clinical trial hubs. Cleveland Clinic Abu Dhabi and other international healthcare facilities offer access to advanced oncology treatments. Saudi Arabia accounts for 28% of regional revenue with Vision 2030 healthcare investments expanding oncology infrastructure. King Faisal Specialist Hospital leads clinical development activity. Israel contributes 22% of regional revenue with Weizmann Institute research feeding clinical translation at Sheba Medical Center and Hadassah Medical Center. South Africa represents 15% of regional revenue with clinical trial activity concentrated in Cape Town and Johannesburg academic centers. Regional growth at 15.4% CAGR through 2034 reflects healthcare infrastructure investment and increasing access to specialized oncology care. Regulatory harmonization efforts across Gulf Cooperation Council countries may streamline market access.

Get More Information about this report -

Request Free Sample ReportMarket Key Segments

By Vaccine Type

- Personalized Neoantigen Vaccines

- Off-the-Shelf Neoantigen Vaccines

- Combination Neoantigen Vaccines

By Platform Technology

- mRNA-Based Platforms

- Peptide-Based Platforms

- Viral Vector Platforms

- Cell-Based and Dendritic Cell Platforms

By Indication

- Melanoma

- Non-Small Cell Lung Cancer

- Colorectal Cancer

- Other Oncology Indications

By End-User

- Hospitals and Cancer Centers

- Specialty Clinics

- Academic and Research Institutions

Regional Analysis and Coverage

- North America

- Latin America

- East Asia And Pacific

- Sea And South Asia

- Eastern Europe

- Western Europe

- Middle East & Africa

| Report Attribute | Details |

| Market size (2025) | USD 2.8 B |

| Forecast Revenue (2034) | USD 9.4 B |

| CAGR (2025-2034) | 14.4% |

| Historical data | 2021-2024 |

| Base Year For Estimation | 2025 |

| Forecast Period | 2026-2034 |

| Report coverage | Revenue Forecast, Competitive Landscape, Market Dynamics, Growth Factors, Trends and Recent Developments |

| Segments covered | By Vaccine Type, (Personalized Neoantigen Vaccines, Off-the-Shelf Neoantigen Vaccines, Combination Neoantigen Vaccines), By Platform Technology, (mRNA-Based Platforms, Peptide-Based Platforms, Viral Vector Platforms, Cell-Based and Dendritic Cell Platforms), By Indication, (Melanoma, Non-Small Cell Lung Cancer, Colorectal Cancer, Other Oncology Indications), By End-User, (Hospitals and Cancer Centers, Specialty Clinics, Academic and Research Institutions) |

| Research Methodology |

|

| Regional scope |

|

| Competitive Landscape | BIONTECH SE, MODERNA INC., GRITSTONE BIO INC., NEON THERAPEUTICS (BIONTECH), GENOCEA BIOSCIENCES, NOUSCOM AG, AGENUS INC., TRANSGENE SA, ISA PHARMACEUTICALS B.V., EVAXION BIOTECH A/S, ADVAXIS INC., IMMATICS N.V., ONCOVIR INC., SUMITOMO DAINIPPON PHARMA ONCOLOGY, ELICIO THERAPEUTICS, ACHILLES THERAPEUTICS, Others |

| Customization Scope | Customization for segments, region/country-level will be provided. Moreover, additional customization can be done based on the requirements. |

| Pricing and Purchase Options | Avail customized purchase options to meet your exact research needs. We have three licenses to opt for: Single User License, Multi-User License (Up to 5 Users), Corporate Use License (Unlimited User and Printable PDF). |

, By Platform Technology (mRNA-Based, Peptide-Based, Viral Vector, Cell-Based & Dendritic Cell Platforms), By Indication (Melanoma, Non-Small Cell Lung Cancer, Colorectal Cancer, Others), By End-User (Hospitals, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034")

, By Platform Technology (mRNA-Based, Peptide-Based, Viral Vector, Cell-Based & Dendritic Cell Platforms), By Indication (Melanoma, Non-Small Cell Lung Cancer, Colorectal Cancer, Others), By End-User (Hospitals, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034")

, By Platform Technology (mRNA-Based, Peptide-Based, Viral Vector, Cell-Based & Dendritic Cell Platforms), By Indication (Melanoma, Non-Small Cell Lung Cancer, Colorectal Cancer, Others), By End-User (Hospitals, Clinics, Research Institutes) Industry Trends & Forecast 2026–2034")

Frequently Asked Questions

How big is the Neoantigen Vaccine Market?

Global Neoantigen vaccine market valued at USD 2.45B in 2024, reaching USD 9.4B by 2034, growing at a CAGR of 14.4% from 2026–2034.

Who are the major players in the Neoantigen Vaccine Market?

BIONTECH SE, MODERNA INC., GRITSTONE BIO INC., NEON THERAPEUTICS (BIONTECH), GENOCEA BIOSCIENCES, NOUSCOM AG, AGENUS INC., TRANSGENE SA, ISA PHARMACEUTICALS B.V., EVAXION BIOTECH A/S, ADVAXIS INC., IMMATICS N.V., ONCOVIR INC., SUMITOMO DAINIPPON PHARMA ONCOLOGY, ELICIO THERAPEUTICS, ACHILLES THERAPEUTICS, Others

Which segments covered the Neoantigen Vaccine Market?

By Vaccine Type, (Personalized Neoantigen Vaccines, Off-the-Shelf Neoantigen Vaccines, Combination Neoantigen Vaccines), By Platform Technology, (mRNA-Based Platforms, Peptide-Based Platforms, Viral Vector Platforms, Cell-Based and Dendritic Cell Platforms), By Indication, (Melanoma, Non-Small Cell Lung Cancer, Colorectal Cancer, Other Oncology Indications), By End-User, (Hospitals and Cancer Centers, Specialty Clinics, Academic and Research Institutions)

How can this market research report help my business make strategic decisions?

Our market research reports provide actionable intelligence, including verified market size data, CAGR projections, competitive benchmarking, and segment-level opportunity analysis. These insights support strategic planning, investment decisions, product development, and market entry strategies for enterprises and startups alike.

How frequently is the data updated?

We continuously monitor industry developments and update our reports to reflect regulatory changes, technological advancements, and macroeconomic shifts. Updated editions ensure you receive the latest market intelligence.

Select Licence Type

Connect with our sales team

Why IntelEvoResearch

100%

Customer

Satisfaction

24x7+

Availability - we are always

there when you need us

200+

Fortune 50 Companies trust

IntelEvoResearch

80%

of our reports are exclusive

and first in the industry

100%

more data

and analysis

1000+

reports published

till date